Introduction:

GST, which was implemented on 1st July 2017, replaced numerous Indirect Taxes with a single tax system. However, several concepts from the previous tax laws have been carried forward into the GST framework. One such concept is the Input Service Distributor (ISD). Additionally, with the introduction of GST, a new concept called cross charge was also introduced. Although these concepts are distinct, they both involve the allocation of input taxes among various registered entities under the GST regime. Consequently, industries are faced with the choice of adopting either the ISD mechanism or the cross charge mechanism. This article aims to elucidate both concepts, providing valuable insights to help industries make informed decisions. The article will particularly benefit companies that have multiple registered entities operating under the same Permanent Account Number (PAN). In simple terms, cross charge refers to the reimbursement of expenses by the head office from its branches. In this context, the branches or factories serve as revenue centers, while the head office functions as a cost center. Hence, the head office allocates the expenses incurred at its location to all of its branch offices.

Cross Charge under GST

- Schedule-I: Supply of goods or services or both between related persons or between distinct persons as specified in section 25, when made in the course or furtherance of business

- Schedule III: Activities or transactions specified in Schedule III is treated neither as supply of goods nor as supply of service. Schedule III includes services by an employee to an employer in course of furtherance of business.

Cross Charge- Important Aspects:

1. The cross charge to distinct persons within the entity.

2. The facility of acceptance of invoice value as open market value [where the recipient branch is fully eligible for ITC].

3. It is a fact that till date very small number of entities have put in place a system to cross charge or used the Input Service Distributor option.

4. This needs to be done in such a way that at least a monthly invoice from HO to branch and branch to HO is started.

5. For the past period one invoice or one invoice per financial year both ways may suffice.

6. The taxpayer may re-look at their understanding and policies with branches, to avoid any possible tax demand.

7. Organisation must create cost centres to each of its units located across India and on periodical intervals may review the inward and outward supplies, i.e. both income and expenditures to tackle issues arising relating to cross-charge.

Cross Charge-Centralized Billing for the following expenses,

- Core/centralized accounting expenses

- Top management expenses

- Advertisement expenses

- Sales and marketing expenses

- Finance charges, Treasury administration expenses

- Cash management expenses

- Legal expenses and Audit fee (Statutory Audit, Internal Audit etc.)

- Tax/Management consultant fee

- Royalty fee and License Fee

EXAMPLE FOR CROSS CHARGE MECHANISM:

EXAMPLE 1.

ABC Limited has Head office in Delhi), following centralized billing and payment mechanism. XYZ Limited has 2 registrations at Mumbai and Bangalore. HO has availed certain support services-IT/software on payment of IGST. However, such support services would be used at both the locations of Mumbai and Bangalore. When HO charges for the said support services to respective locations, it shall be required to supply under an appropriate invoice & Cross charge the value of support services accordingly.

- Valuation: Transaction value, as per Rule 28 of CGST Rules – OMV, Kind & quantity, Cost+10%. Both location – eligible to full ITC, the value declared in the invoice would be deemed to be the open market value of goods or services.

EXAMPLE 2.

The corporate office of Akash limited in Mumbai paid GST of Rs. 10 lacs on the rent of its corporate office of Rs. 50 lakhs during FY 2020-21. Now it is recovering or charging the same from its factory site situated in Himachal Pradesh. The said transaction would be covered under the provisions of cross charge. This would mean that Head Office would raise tax invoice on and pay GST on the same.

Akash limited appointed a consultant to design the structure of plants for its plants in Himachal and Faridabad at a fee of Rs. 10 lakhs. The invoice for the same had been issued to the head office situated in Mumbai. Now the head office is apportioning such expenses to the branches, it shall be treated an ISD transaction.

Akash Limited and Rishi Private Limited are sister concerns.

Invoice in respect of consultancy services consumed by latter was received in the name of the former. Now, under these circumstances, former recovers the expense from the latter.

In this example, since the service is consumed by Rishi Private Limited whereas invoice is issued in name of Akash Limited, the condition of receipt of Services under section 16(2) is violated and hence No ITC could be claimed.

Therefore, this transaction would neither be covered under cross charge nor under ISD. The said amount would be recovered by way of Journal entry in books of accounts.

Reporting of cross charge in GST returns

- There is no separate row in the table that is exclusively meant for cross charge transactions. These transactions will be reported on the same lines as regular supply of goods or services.

- The nature of the cross-charge transaction, whether it is inward supply or outward supply, will form the basis for where they are reported in the relevant form.

- In the case of inward supply, the reporting will be made in the GSTR-3B form as regular inward supply.

- In the case of outward supply, the reporting will have to be made in both the GSTR-3B as well as the GSTR-1.

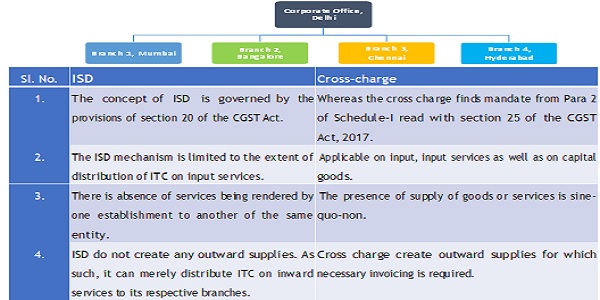

Input Service Distributor

- Applicable to supplier of services only

- Applicable to such supplier of services having more than one registration under the same PAN

2 (61) “Input Service Distributor” means an

Office of the supplier of goods or services or both

which receives tax invoices issued under section 31 towards the receipt of input services and

issues a prescribed document

for the purposes of distributing the credit of central tax, State tax, integrated tax or Union territory

tax paid on the said services to a supplier of taxable goods or services or both

having the same Permanent Account Number as that of the said office;

DIFFERENCE BETWEEN INPUT SERVICE DISTRIBUTION AND CROSS CHARGE

| Tax charged on invoices for input services | Tax can be distributed as | |

| Recipient is within same state | Recipient is in another state | |

| IGST | IGST or CGST and SGST | IGST |

| CGST/SGST | CGST/SGST | IGST/TGST |

- Credit of CGST as IGST and IGST as IGST, by way of issue of a prescribed document,

- Credit of SGST as IGST

- Credit of CGST and IGST as CGST

- Credit of SGST and IGST as SGST

Input Service Distribution- conditions

- Prescribed documents

- Such document to be issued on recipient

- Should not exceed the credit available

- Used by a particular location- distributed only to that location

- Used by more than one location (operational) – distribute on pro rata.

- Credit distributed in excess of what was available

- Excess credit distributed to one or more recipient of credit

- Recovery of such excess credit with interest from the recipient of credit.

EXAMPLE:

The corporate office of PSG EXPORTS is situated at New Delhi, with its different units registered in various States across India at, Bangalore, Mumbai, Kolkata and New Delhi. The software license and upgrading of software service is received and used at all the locations, however, the invoice is received at corporate office only. For that reason, the Delhi corporate office has to act as ISD to distribute the credit. (All values are exclusive of taxes and the GST applicable rate is 18% CGST 9% and SGST 9%)

In Illustration above, if the value of service received is Rs. 20,00,000/- (intra-State supply), then how the credit will be distributed to all such recipients?

- Turnover during the relevant period-

| REGISTRATION | TURNOVER |

| DELHI | 75,00,000 |

| BANGALORE | 50,00,000 |

| MUMBAI | 85,00,000 |

| KOLKATTA | 40,00,000 |

| TOTAL | 2,50,00,000 |

Manner of Distribution of Credit:

Total amount of credit to be distributed [20,00,000 × 18%] Rs.3,60,000/-

Calculation of ITC attributable-

| REGISTRATION | TURNOVER |

| DELHI | 7500000/25000000 x 360000 = 108000 |

| BANGALORE | 5000000/25000000 x 360000 = 72000 |

| MUMBAI | 8500000/25000000 x360000 = 122400 |

| KOLKATTA | 4000000/25000000 x360000 = 57600 |

How the credit will be available to all such recipients i.e., as CGST/SGST or IGST?

In respect of Delhi recipient (i.e., located in the same State in which ISD is located), attributable ITC of Rs. 1,08,000/- will be distributed as ITC of CGST/SGST i.e., Rs. 54,000/- as CGST and Rs. 54,000/- as SGST In respect of other recipients (i.e., located in a State other than that of ISD), attributable ITC will be distributed as IGST equal to CGST + SGST i.e., ITC on account of IGST will be available as follows:

- Bangalore Rs. 72,000/-

- Mumbai Rs. 1,22,400/-

- Kolkata Rs. 57,600/-

If the software service is used only for Bangalore and Kolkata. Then how the credits will be distributed?

Bangalore 5000000/9000000X360000 = 200000

Kolkata 4000000/9000000 X 360000 = 160000

Let us assume that there is a business entity which has Head Office (HO) at BANGLORE (HO) and two branch offices at MUMBAI (BO-1) and Chennai (BO-2), as shown in the matrix above. The HO procures security service (IS – 1) for the entire organisation from a security agency located in Delhi, which deploys 10 security guards at HO and 5 each at BO-1 and BO-2.

2.2. The HO has a personnel Department which looks after the personnel administration such as maintenance of leave record, performance evaluation, and promotion of all the employees posted at HO, BO-1 and BO-2. The activity performed by the personnel department of HO is marked as C-1. The Technical Maintenance Department of the HO does the maintenance of all the machines installed at HO, BO-1 and BO-2. The activity performed by the Technical Maintenance Department of the HO is marked as C-2.

2.3. Usually Head Office as well as branch offices would undertake software development projects for their clients. In a software development project undertaken for a client by BO-2, two engineers will be posted at BO-1 and another to assist BO-2. The activity performed by the two engineers of BO-1 for the software development project undertaken by BO-2 is marked as B-1 in the matrix above, depicting the flow of the above services within the three distinct persons of the same organisation.

3. The issues that may arise with regard to taxability of supply of services between distinct persons in terms of sub-section (4) of section 25 of the CGST Act as shown in the above matrix are being clarified in the form of questions and answers as detailed below: –

3.1. Question– Is it mandatory to distribute input tax credit (hereinafter referred to as ‘ITC’) in respect of input services (IS-1), procured by HO but attributable to both HO and BOs, following the Input Service Distributor (ISD) procedure?

Answer –Yes, it is mandatory to follow ISD procedure laid down in Section 20 of CGST Act read with rule 39 of the Central Goods and Services Tax Rules, 2017 (hereinafter referred to as ‘the CGST Rules’) for distribution of ITC in respect of input services procured by HO from a third party but attributable to both HO and BO or exclusively to one or more BOs.

3.2. Question–Whether the input service (IS-1) procured by HO from a third party for use by the BOs, the ITC of which is distributed in accordance with the ISD procedure, be treated as a supply by HO to the BOs and will it be taxable in the hands of HO.

Answer – No, the services procured by HO from a third party for use at HO and BOs, or exclusively for use by BOs, the ITC of which is distributed in accordance with the ISD procedure laid down in Section 20 of the CGST Act read with rule 39 of the CGST Rules, would not be separately treated as supply by the HO to the BOs.

3.3. Question– If HO considers that procurement, distribution and management of common input services for use by HO and BOs as per ISD provisions leads to an expense, how can it apportion these expenses to the BOs?

Answer–HO may incur certain expenses on procurement, distribution and management of common input services. The HO may or may not apportion and recover such expenses from BOs. Nevertheless, such procurement, distribution and management of services by the HO for the BOs is a separate service provided by the HO to the BOs. It should be invoiced by the HO to the BOs to the extent of expense incurred by the HO. It is a service distinct from those services the ITC in respect of which has been distributed through the ISD procedure. It is for the HO to value the service as per the principles laid down in para 3.6 below.

3.4. Question– If the HO generates some services internally such as common administration by maintaining common administration team for BOs and HO (C1 in the matrix above), or common IT maintenance through a maintenance team at HO (C2 in the matrix above), where the team members are the employee of the HO, are these employees providing any service to the BOs?

Answer –

3.4.1. The offices or establishments of an organisation in different States are establishments of distinct persons under sub-section (4) of section 25 of the CGST Act and Explanation 1 of section 8 of the Integrated Goods and Services Tax Act, 2017 (hereinafter referred to as ‘the IGST Act’). GST law envisages these distinct registered persons to be independent entities, though part of one legal entity, and they can be providing services to each other.

3.4.2. Whether employees posted in HO, who look after administration of HO and BOs or maintenance of machines installed in the HO and BOs or perform similar other functions for the organization as a whole or for a particular BO which is a distinct person, are providing service to BOs is not the correct perspective to be determined here. The correct perspective for examining the issue at hand would be to determine whether the HO and BOs are providing services to each other and not whether the employee of HO is providing services to the BOs. In this case, it is the HO which is providing services to BOs.

3.5. Question– What is the legal basis for concluding that HO is providing services to the BOs in the above example?

Answer –HO and BOs are distinct persons in terms of sub-section (4) of section 25 of the CGST Act. They are also related persons as defined in Explanation (a) to section 15 of the CGST Act. It may be noted that the supply of goods or services or both between related persons or between distinct persons, when made in the course or furtherance of business is a supply even if it is made without consideration in terms of para 2 of Schedule I to the CGST Act. Thus, services produced or generated in HO by its employees and used by or supplied to BOs, with or without consideration, are supplies liable to GST. The HO should invoice such supplies to the BOs, whether HO charges any consideration for such supplies from BOs or not, is immaterial. The same principle would apply for supply of services by a BO to another BO (B 1in the above matrix) or by a BO to the HO.

3.6. Question– How would these services provided by one entity to another of a body corporate, registered as distinct entities (C1 and C2 in the above matrix) be valued?

Answer-

3.6.1. As regards valuation of such supplies, since HO and BOs located in different States are related persons, value of such supplies cannot be determined under sub- section (1) of section 15 of CGST Act. The same has to be determined under sub- section (4) of Section 15 of CGST Act read with the rules made thereunder. According to rule 28 of the CGST Rules, the value of supply of goods or services between distinct persons or related persons shall,

a) be the open market value of such supply;

b) if the open market value is not available, be the value of supply of goods or service of like kind and quality;

c) if the value is not determinable under clause (a) or (b), be the value as determined by the application of rule 30 or rule 31 of the CGST Rules, in that order.

3.6.2. The rule further provides that where the recipient is eligible for full ITC, the value declared in the invoice shall be deemed to be the open market value of the goods or services.

3.6.3. Illustration -HO has sent an annual expense budget of Rs 10 lakh for the administrative division looking after the personnel administration of the employees in HO as well as two BOs located in two different States. The value of services supplied by the HO to BO-I may be determined under rule 31 of the CGST Rules using any reasonable means consistent with the principles of valuation contained in the CGST ACT. For example, value “V” of service provided by HO to BO-1 for managing administration of staff can be determined as follows:

Value “V” = (Y/N) x Rs.10,00,000/-

Where, Y is the number of employees in BO-1;

And N is the total number of employees posted in the HO and two BOs.

3.7. Question– If there is an input service, clearly attributable to a BO, can it be contracted by the HO and paid for by the HO. How would this credit be transferred to the BO?

Answer – HO can distribute ITC in respect of input services procured on behalf of BO following the ISD procedure laid down in section 20 of CGST Act read with rule 39 of the CGST Rules. There is no restriction on HO acting as common procurement centre for all the services required by a business. If a service is specifically attributable to a BO, it shall be distributed to that BO only in terms of clause (c) of sub-section (2) of section 20 of the CGST Act.

3.8. Question– There are some services internally generated which are clearly identifiable as those pertaining to another distinct person, how would these be taxed? For example, if two persons in BO 1 do work related to IT development for a project contracted by BO-2 (service B 1 in the above matrix), how would it be taxed?

Answer-

3.8.1. In this case, BO-1 is providing service to BO-2 by way of assistance in the IT development work undertaken by BO-2. BO-1 should invoice this service to BO-2 and pay GST on it. Value of the service may be determined by using any reasonable means as illustrated below:

3.8.2. Illustration – Assuming that each of the two engineers of BO-1, who assisted in the software development project undertaken by BO-2 as shown in the above matrix, draws salary and emoluments on cost to the company (CTC) basis of Rs. 1.00 lakh per month and puts in, on an average, 200 hours of work per month, and devoted 50 hours each for the project undertaken by BO-2, the value of service (B1) supplied by BO-1 to BO-2, by way of assistance in a project belonging to BO-2, may be determined using reasonable means under rule 31 of the CGST Rules as under:

Value of service B 1= Employee cost + Establishment cost of supplying 100 man-hours.

Employee cost of 100 man-hours supplied by BO-1 to BO-2 may be calculated in this example as under:

= (100000/200) *50*2

To this may be added the establishment cost of supplying 100 man-hours following any reasonable method consistent with the generally accepted accounting principles as illustrated in para 3.6.3 above.

3.8.3. It may be noted that the question pertains to clearly identifiable service for which BO maintains record. This does not warrant that activities and services of individual employees are required to be monitored in terms of its usage by various BOs and HO. Where such accounting is not done in the normal course of business, answer as given for question 3.6 shall apply.

Illustrative example to explain the ISD and Cross Charge Mechanism

Commerce Limited has Head office in Maharashtra along with two manufacturing unit in Gujarat and Uttar Pradesh (UP). Commerce Limited has following data and wants to determine the cross – charge value to be charged to other units.

Extract of Profit and Loss Account of ABC Limited for the month of May 2018

Identification of expenses for cross charging:

First and foremost, cross charging from Head office shall be done only for expenses borne by it but they are common expenses or related to other units. Therefore, Head office need to identify such expenses as under-

1. These expenses are directly attributable to Gujarat unit and are borne by Gujarat unit only. Thus, question of cross charging by Head office does not arise.

2. These expenses are directly attributable to Uttar Pradesh unit and are borne by Uttar Pradesh unit only. Thus, question of cross charging by Head office does not arise.

3. This expense is related to and borne by Head office, Maharashtra and thus, same should not be charged to other units.

4. Interest on loan is exempted supply under GST regime which means no GST would have been charged by lender on such expenses. In our view, such exempted supply should not be considered for cross charging. If such interest is considered in calculation then there may be GST liability on such exempted supply also as Head office would be making outward supply in the form of Business Support Service which is taxable supply.

Based on above, green highlighted expenses should be charged to concerned units.

IDENTIFICATION OF CROSS CHARGING:

The basis for cross charging would be very subjective and depends upon the industry practice. However, a standard approach could be taking taxable turnover made by concerned units which is also akin to the manner of distribution of common credits by ISD under CGST Act. Some other basis of cross charge could be the number of employees, space, plant capacity utilization or other reasonable basis that are used for costing purposes. Based on this following shall be the ratio for distributing the common expenses.

|

Units |

Taxable turnover in lakhs (Rs.) | Ratio (%) |

| Head Office- Maharashtra | 400 | 27.00 |

| Gujarat Unit | 500 | 33.00 |

| Uttar Pradesh Unit | 600 | 40.00 |

| Total | 1500 | 100.00 |

Identification of directly attributable expenses:

There could some expenses which are directly related to any specific units but the same have been borne by the Head office. In such cases, instead of distributing the ITC on such expenses as per the specific ratio, it shall be directly apportioned to the concerned unit.

In the instant case, Advertisement expenses of Rs.70 lakhs is borne by Head office but it directly related to Uttar Pradesh unit and hence such cost shall be directly charged to Uttar Pradesh as whole without any allocation to the other establishments.

Distribution of common expenses:

Such common expenses should be distributed to concerned units in turnover ratio as calculated above

| Nature of common expenses | Amount in Lakhs (Rs.) | Maharashtra (27.00%) | Gujarat (33.00%) | Uttar Pradesh (40%) |

| Meeting and events/ Brand promotion | 40 | 11 | 13 | 16 |

| Audit fee | 10 | 2.5 | 3 | 4 |

| Legal and Professional fees | 22 | 1 | 3 | 8.8 |

| Total | 72 | 14.5 | 19 | 28.8 |

Calculation of cross charge value

Head office shall raise the tax invoice on Gujarat and Uttar Pradesh Units considering below mentioned taxable values

|

|

Particulars | Gujarat Unit | Uttar Pradesh Unit |

| Directly attributable cost | – | 70.00 | |

| ADD | Apportionment of common expenses | 19.00 | 28.80 |

| Total Cost | 19.00 | 98.80 | |

| ADD | 10% mark up | 1.90 | 9.88 |

| Taxable Value (110% of Cost) | 20.9 | 108.68 |

PRACTICAL APPROACH TO THE PROBLEMS: Companies may consider the following:

- ISD registration for third-party expenses which are attributable to branches: All expenses at HO should be taken in ISD and then distributed.

- Authorities questioning not taking of ISD registration, view also articulated by the Draft Circular that ISD is mandatory.

- Levying GST on cross-charge (HO to branch services or vice-versa) and pay the same under protest on a going forward basis.

- Option to be evaluated after considering the following:

- Availability of credit to the recipient locations.

- Cash outflow issues and possibility of utilization.

- Even if employee cost is not considered – cross charge a fixed amount under the deemed OMV concept Could result in substantial compliance burden (a company having branches in 30 States may have to raise 900 GST invoices, all of which could be creditable) – however, would avoid unwarranted litigation.

IMPLICATIONS AND POSSIBLE SCENERIOS:

– Companies who have neither followed ISD nor cross-charge mechanism

– Companies who have followed ISD mechanism, but not done cross-charge

– Companies who have only done cross-charge, not levied GST on employee cost: either from the date of introduction of GST / subsequently

o Accepted the view that there is a ‘supply’ if not paid ‘under protest’ and hence, could result in demand of GST on attributable employee cost interest consequences

– Companies who have done cross-charge, and levied GST on employee cost: however subsequently

o Interest exposure

The view of the Government is evident from the Draft Circular & the Press note seems to be that GST applicable on common functions provided by HO to the branch

Could result in issuance of issuance of SCN and litigation

> Don’t file an application of Advance Ruling – if negative, would lead to a legal compulsion to charge GST.

> File an immediate Representation on the issue with the GST Council/CBIC.

> Any levy would lead to substantial litigation across the taxpayers.

> Levy of tax leads to substantial impractical difficulties and is difficult to operate, any levy should justify costs incurred to administer such levy.

> Increase in compliance burden and complicates the structure of GST, credit available in most cases and hence revenue neutral.

> Artificial attribution / allocation of costs is in any event not in line with the concept of GST / destination-based consumption tax.

> Additional point on past practice of cross-charge vs. ISD / giving legal sanctity to cross charge.

HOW TO RESOLVE THIS SITUATION:

- Companies may consider the following:

√ ISD registration for third-party expenses which are attributable to branches: All expenses at HO should be taken in ISD and then distributed.

√ Authorities questioning not taking of ISD registration, view also articulated by the Draft Circular that ISD is mandatory.

√ Levying GST on cross-charge (HO to branch services or vice-versa) and pay the same under protest on a going forward basis.

Option to be evaluated after considering the following:

-

- Availability of credit to the recipient locations.

- Cash outflow issues and possibility of utilization.

- Even if employee cost is not considered – cross charge a fixed amount under the deemed OMV concept.

- Could result in substantial compliance burden (a company having branches in 30 States may have to raise 900 GST invoices, all of which could be creditable) – however, would avoid unwarranted litigation.

Legal proposition on the issue:

Columbia Asia Hospitals case – AAR [2018 (15) GSTL 722 – AAR]

- The question before AAR was: “Whether the activities performed by the employees at the corporate office in the course of or in relation to employment such as accounting, other administrative and IT system maintenance for the units located in the other States as well i.e. distinct persons as per Section 25(4) of the Central Goods and Services Tax Act, 2017 (CGST Act) shall be treated as supply as per Entry 2 of Schedule I of the CGST Act or it shall not be treated as supply of services as per Entry 1 of Schedule III of the CGST Act?

The applicant was already paying IGST on common services procured from outside and charged to other units.

> The ruling was sought only as to employee cost.

> They were not charging GST on employee cost, attributable to other units, as employment is outside GST.

> It was argued that employee of HO, is employee of the entity and hence employee of all the units and just because the different units are “distinct persons” under GST, they do not cease to be common employees of all units of the entity.

Findings of AAR: Regarding the second issue related to the activities performed by the employees at the corporate office in the course of or in, relation to employment, the employees employed in the Corporate Office are providing services to the Corporate Office and hence there is an employee-employer relationship only in the IMO. The other offices are distinct persons and therefore the employees in the IMO have no employer employee relationship with other offices.

The services provided to the employer, i.e., the corporate office by the persons employed by the corporate office is in the nature of the employee employer relationship. Further, since the corporate office and the units are distinct persons under the Act, there is no such relationship between the employees of one distinct entity with another distinct entity, at least as per the Goods and Services Tax Act, even if they are belonging to the same legal entity.

Columbia Asia Hospitals case – AAAR [2019 (20) GSTL 763 – AAAR]

Upheld the ruling of AAR. “The services of the employees at the IMO in so far as they are benefiting the other registered units of the appellant, will not be termed as ‘employee-employer relationship’ and will therefore not fall within the purview of Entry 1 of Schedule III”

The AAAR has also made certain observations on ISD Vs Cross Charge. Second proviso to Rule 28. Provided further that where the recipient is eligible for full input tax credit, the value declared in the invoice shall be deemed to be the open market value of the goods or services. (Specs makers – AAAR). Where full ITC is not eligible – Open market value (Apportionment on a reasonable basis). – Issue invoice. Recipient can take ITC. No need for “payment” within 180 days.

CONCLUSION:

GST law emphasis state wise registration and each registration is being treated as distinct person. The common expenses may be either distributed via ISD or may be charged via cross charge. Both the options attract their respective compliances which shall be adhered to with all the provisions of the GST law, which at times may be cumbersome also especially with regards to maintenance of accounts and record along with audit provisions under GST regime. However, for supplies made between distinct taxable persons, cross charge is the only option in my humble view. ISD mechanism brings in a lot of structure in the manner of distribution of credits, it also increases the compliance burden as monthly returns need to be filed for entities registered as an ISD. Cross charge mechanism offers flexibility and is also, the only mechanism that can be employed for distribution of credits related to goods and capital goods. Both mechanisms have their own merits and demerits and needs to be evaluated carefully before arriving at a decision.

Author Bio