As per Press Release and Via notification No. 23/2017 dated 17th August, 2017, extension has been granted for filing of first monthly summary return for the month of July, 2017 i.e. FORM GSTR-3B upto 28th Aug, 2017. Let’s analyse the same further:

Ques. 1 What is the due date of filing FORM GSTR-3B in case there is no transitional credit??

Ans. In case there is no transitional credit, the last date for filing FORM GSTR-3B is 20th August, 2017.

Ques.2 What is the due date of filing in case where transitional credit is to be claimed??

Ans. As per latest notification, in case where transitional credit is to be claimed, last date of filing FORM GSTR-3B is 28th August, 2017. The taxpayers who want to avail the transitional input tax credit should also calculate their tax liability after estimating the amount of transitional credit as per Form TRANS I. They have to make full settlement of the liability after adjusting the transitional input tax credit before 20th August, 2017. However, in such cases, they will get time upto 28th August, 2017 to submit Form TRANS I and Form 3B. In case of shortfall in the amount already paid vis-à-vis the amount payable on submission of Form 3B, the same will have to be paid with interest @ 18% for the period between 21st August, 2017 till the payment of such differential amount.

In other words, in case the transitional credit is to be claimed, then last date for filing FORM TRANS-1 & FORM 3B is 28th August, 2017.

| Sl. No. | Class of registered persons | Last date for furnishing of return in FORM GSTR-3B | Conditions |

| 1. | Registered persons entitled to avail input tax credit in terms of section 140 of the said Act read with rule 117 of the said Rules but opting not to file FORM GST TRAN- 1 on or before the 28th August, 2017 | 20th August, 2017 | – |

| 2. | Registered persons entitled to avail input tax credit in terms of section 140 of the said Act read with rule 117 of the said Rules and opting to file FORM GST TRAN-1 on or before the 28th August, 2017 | 28th August, 2017 | (i) compute the “tax payable under the said Act” for the month of July, 2017 and deposit the same in cash as per the provisions of rule 87 of the said Rules on or before the 20th August, 2017;

(ii) file FORM GST TRAN-1 under subrule (1) of rule 117 of the said Rules before the filing of FORM GSTR-3B (iii) where the amount of tax payable under the said Act for the month of July, 2017, as detailed in the return furnished in FORM GSTR-3B, exceeds the amount of tax deposited in cash as per item (i), the registered person shall pay such excess amount in cash in accordance with the provisions of rule 87 of the said Rules on or before 28th August, 2017 along with the applicable interest calculated from the 21st day of August, 2017 till the date of such deposit. |

| 3. | Any other registered person | 20th August, 2017 | – |

–

| CRUX

In both the cases: 1. Whether the transitional credit is to be claimed, or 2. Whether the transitional credit is not to be claimed Tax Liability has to be paid off before 20th August, 2017 |

Ques.3 What is tax Liability??

Ans. “Tax payable under the said Act” means the difference between the tax payable for the month of July, 2017 as detailed in the return furnished in FORM GSTR-3B and the amount of input tax credit entitled to for the month of July, 2017 under Chapter V and section 140 of the said Act read with the rules made thereunder.

Quesues.4 How to calculate tax liability in case where transitional credit is not to be claimed??

Ans. If a Registered persons planning not to avail transitional credit for discharging the tax liability for the month of July, 2017 or new registrants who do not have any transitional credit to avail need to follow the steps as detailed below:

Ans. I. Calculate the tax payable as per the following formula: Tax payable = (Output tax liability + Tax payable under reverse charge) – input tax credit availed for the month of July, 2017;

II. Tax payable as per (i) above to be deposited in cash on or before 20.08.2017 which will get credited to electronic cash ledger;

III. File the return in FORM GSTR-3B on or before 20.08.2017 after discharging the tax liability by debiting the electronic credit or cash ledger.

Ques. 5 How to calculate tax liability in case where transitional credit is to be claimed??

Ans. If a Registered persons planning to avail transitional credit for discharging the tax liability for the month of July, 2017 need to follow the steps as detailed below:

I. Calculate the tax payable as per the following formula: Tax payable = (Output tax liability + Tax payable under reverse charge) – (transitional credit + input tax credit availed for the month of July, 2017);

II. Tax payable as per (i) above to be deposited in cash on or before 20.08.2017 which will get credited to electronic cash ledger;

III. File FORM GST TRAN-1 (which will be available on the common portal from 21.08.2017) before filing the return in FORM GSTR-3B;

IV. In case the tax payable as per the return in FORM GSTR-3B is greater than the cash amount deposited as per (ii) above, deposit the balance in cash along with interest @18% calculated from 21.08.2017 till the date of such deposit. This amount will also get credited to electronic cash ledger;

V. File the return in FORM GSTR-3B on or before 28.08.2017 after discharging the tax liability by debiting the electronic credit or cash ledger.

Ques. 6 How to pay off tax liability??

Ans. Following are the steps to pay off the tax liability:

1. Go to https://services.gst.gov.in/services/login

2. Under services tab, click on payment

3. Click on Create challan. A window will appear like this:

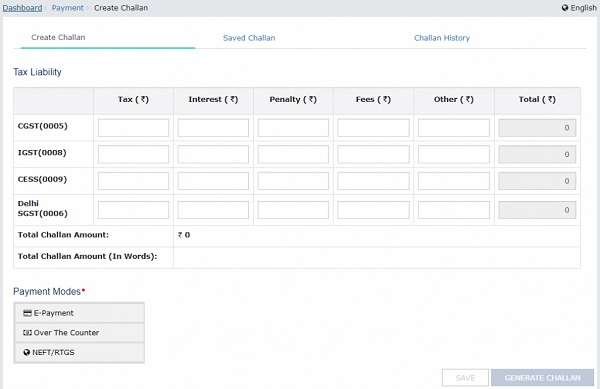

4. Fill in the complete bifurcation i.e. CGST, IGST, SGST, click on CREATE CHALLAN.

Three modes of payments are available:

1. E- payment- Internet banking and debit/credit cards of authorized bank

2. OTC- Over the counter payment through authorized bank (for payment of tax liability below Rs. 10,000)

3. NEFT/RTGS- Payment through NEFT/RTGS from any bank

4. Fill in the complete bifurcation i.e. CGST, IGST, SGST, click on CREATE CHALLAN.

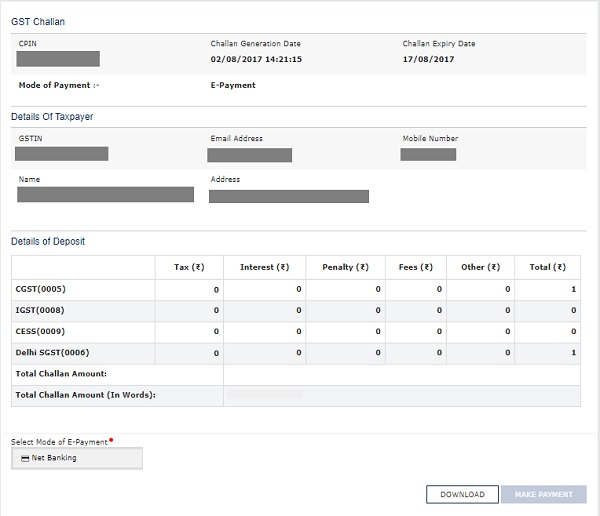

5. Once you click on create challan, a summary page will appear, containing all the details of challan. Select the method of payment by choosing the bank through which payment will be made. Click on Make Payment. This will take you to the net banking account of the bank specified by you.

6. Make online payment through Net- Banking.

Once the payment is made you will receive a challan containing all the details of tax paid. Thereafter the tax paid challan (CIN) will be credited to the cash ledger account of the taxpayer.

Conclusion:

Taxpayers were in huge dilemma for filing first monthly return in case where transitional credit is to be claimed. But post these notification, press releases, finally, to a large extent taxpayers are relaxed as the date for filing of return in case where transitional credit is to be claimed is being extended till 28th Aug, 2017.

References:

Form GSTR-3B Due date extended with Conditions; No Change in due date of Payment

Clarification regarding availability of Transitional Credit for GST

Return filing In Form GSTR-3B- Due Date & transitional credit

Author: C S Ekta Maheshwari is the Author of this article and is Company Secretary by profession. The Author can be reached at csektamaheshwari14@gmail.com

Disclaimer: The entire contents of this article is solely for information purpose and have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation.. It doesn’t constitute professional advice or a formal recommendation. The author has undertook utmost care to disseminate the true and correct view and doesn’t accept liability for any errors or omissions. You are kindly requested to verify & confirm the updates from the genuine sources before acting on any of the information’s provided herein above.

Author Bio

dear sir

we have balance credit of vat as on 30-06-2017 we have not adjested this credit on payment of july 2017 Gst payment now we file trans 1 & we adjested this vat credit in on payment of Aug 2017 payment of gst

we have filing GST return of july 2017 & then after we have adjested tran-1 credit in aug 2017 for payment of aug 2017 gst

i am aged person .request modification rq B2B RETURN WO WE REQUEST YOU SIR WE ARE REQUEST PLEASE GIVE MODIFICATION RETRUN HOW WE GET ITC AND CREDIT INPUT TAX BY MISTAKETO WORK PLEASE HOW WE CAN REVISED B2B RETRUN AT EARLY ARE OUR DEALERS AL ARE BLMES ME PLEASE HELP THIS IS THE FIRSAT TIME REQUESTED