Financial Accounts under FATCA and CRS

1. Introduction

A Financial Account is an account maintained by a Financial Institution and includes specific categories of accounts as discussed in paragraph 2. Rule 1 14F(1) defines Financial Accounts.

RFIs are required to review the Financial Accounts maintained by them and to identify whether any of Financial Accounts is held by a Reportable Person. Wherever account is held by a Reportable Person, such account becomes Reportable Account.

There are certain types of Financial Accounts which carry low risk of being used to evade tax. These accounts are specifically excluded from review and are called Excluded Accounts (See Para 8).

2. Categories of Financial Accounts

There are broadly five types of financial account:

Table: Who maintains the Financial Accounts

| Accounts | Financial Institution generally considered to maintain them |

| Depository Accounts | The Financial Institution that is obligated to make payments with respect to the account (excluding an agent of a Financial Institution). |

| Custodial Accounts | The Financial Institution that holds custody over the assets in the account. |

| Equity and debt interest in certain Investment Entities | The equity or debt interest in a Financial Institution is maintained by that Financial Institution. |

| Cash Value Insurance Contracts | The Financial Institution that is obligated to make payments with respect to the contract. |

| Annuity Contracts | The Financial Institution that is obligated to make payments with respect to the contract. |

A Financial Institution may maintain more than one type of Financial Account. For example, a Depository Institution may maintain Custodial Accounts as well as Depository Accounts.

3. Depository Account

Depository Account includes any commercial, checking, savings, time, or thrift account, or an account that is evidenced by a certificate of deposit, thrift certificate, investment certificate, certificate of indebtedness, or other similar instrument maintained by a financial institution in the ordinary course of a banking or similar business.

A Depository Account includes an amount that an insurance company holds under an agreement to pay or credit interest thereon.

A Depository Account does not have to be an interest bearing account.

4. Custodial Account

Custodial Account which means an account (other than an insurance contract or annuity contract) for the benefit of another person that holds one or more financial assets.

Custodial account would also include Mutual Fund holding in De-materialized format which would be required to be reported by depository/depository participant only. If mutual fund units are held in a physical format, the entity issuing the units will be responsible for reporting such custodial accounts.

5. Equity and Debt Interest

5.1. Equity and debt interests are financial accounts if they are interests in an investment entity.

An equity interest may vary depending on the nature of the investment entity. Equity interest in an investment entity, being-

(a) a partnership firm means either a capital or profits interest in the partnership firm;

(b) a trust means any interest held by any person treated as a settlor or beneficiary of all or a portion of the trust, or any other natural person exercising ultimate effective control over the trust. A person will be treated as a beneficiary of a trust if he has the right to receive directly or indirectly a mandatory distribution or may receive, directly or indirectly, a discretionary distribution from the trust.

5.2. However, Financial account will not include any equity or debt interest in an entity that is an investment entity solely because it

a. renders investment advice to, and acts on behalf of, or

b. manages portfolios for, and acts on behalf of,

a customer for the purpose of investing, managing, or administering financial assets deposited in the name of the customer with a financial institution, that is not a non-participating financial institution other than such entity.

Therefore, equity interests in Investment entity, which is only an investment advisor or investment manager, are not financial accounts.

5.3. Examples of Investment entity can be collective investment vehicle, mutual fund, exchange traded fund, private equity fund, hedge fund, venture capital fund, leveraged buyout fund, or any similar investment vehicle established with an investment strategy of investing, reinvesting, or trading in Financial Assets.

5.4. There may some situations in which a Financial Institution can circumvent reporting under Rule 114G. Therefore, it has been expressly stated that if class of interests was established for the avoidance of reporting, that class of interest will be Financial Account and will be reported.

5.5. Debt or equity interests in a financial institution (other than as described in para 5.1 & 5.2) would constitute Financial Accounts if:-

- The value of such interests is determined primarily by reference to assets that give rise to US Source Withholdable Payments; and

- The class of interests was established for the avoidance of reporting under the Agreement.

6. Cash Value Insurance Contracts

Insurance contract means a contract under which the issuer agrees to pay an amount upon the occurrence of a specified contingency involving mortality, morbidity, accident, liability, or property risk.

Cash value insurance contract means an insurance contract (other than an indemnity reinsurance contract between two insurance companies) that has a cash value and in case of a U.S. reportable account such value is greater than an amount equivalent to USD 50,000.

Generally, Cash Value Insurance Contract is a type of investment product that has an element of life insurance attached to it. The life insurance element is often small compared to the investment element of the contract. Policyholder is entitled to receive payment on surrender or termination of the contract.

Cash Value Insurance Contracts do not include:

> Indemnity insurance contracts between insurance companies

> Term life insurance contracts

> Property or motor insurance

> Policies indemnifying against economic loss arising from specified circumstances, for example personal injury, theft, etc.

> Micro insurance contracts that do not have a cash value

7. Annuity Contract

Annuity contract means a contract under which the issuer agrees to make payments for a period of time determined in whole or in part by reference to the life expectancy of one or more individuals.

(Ref: Page 50 of CRS and 175 of Commentary)

8. Excluded Accounts

8.1. There are few categories of financial accounts which have low risk of being used to evade tax and thus have been excluded from the need to be reviewed or reported. These accounts are called “Excluded Accounts”. These accounts have been enumerated in Explanation (h) to Rule 114F(1) as under:-

(i) Retirement or pension accounts satisfying certain conditions Explanation (h)(i) to Rule 1 14F(1).

(ii) Non-retirement tax-favored accounts subject to regulations and satisfying certain conditions Explanation (h)(ii) to Rule 1 14F(1).

(iii) Account established under the Senior Citizens Savings Scheme Rules Explanation (h)(iii) to Rule 1 14F(1).

(iv) Term Life Insurance contracts satisfying certain conditions Explanation (h)(iv) to Rule 1 14F(1).

(v) Accounts held by Estates Explanation (h)(v) to Rule 114F(1).

(vi) Escrow Accounts established in connection with court judgments Explanation (h)(vi) to Rule 1 14F(1).

(vii) Depository accounts (other than US reportable accounts) due to non-returned over payments in case of credit card and other accounts and satisfying certain conditions Explanation (h)(vii) to Rule 114F(1).

(Ref: Page 53 of CRS and 184 of Commentary)

Financial Accounts which are Reportable Accounts

1. Introduction

1.1. Once a RFI has identified the Financial Accounts maintained by them, they are required to review those accounts to identify whether any of them are Reportable Accounts. If any of the financial account is found to be reportable account, information in relation to those accounts must be reported in Form 61B.

1.2. In general terms, a Reportable Account means an account, which has been identified pursuant to the due diligence procedure, as held by

(a) a reportable person; or

(b) an entity, not based in United States of America, with one or more controlling persons that is a specified U.S. person; or

(c) a passive non-financial entity (passive NFE) with one or more controlling persons that is a person described in sub-clause (b) of clause (8) of the rule 1 14F.

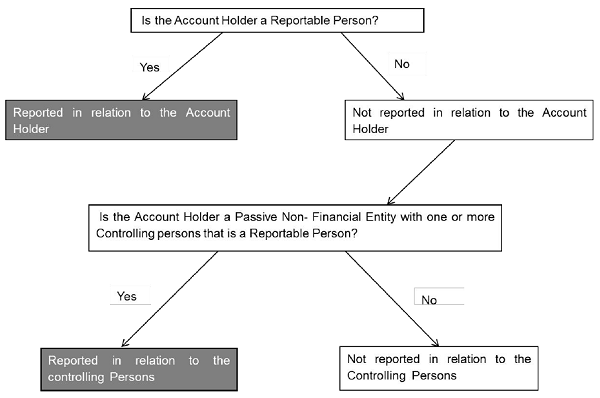

1.3. Thus, an account can be a Reportable Account by virtue of the Account Holder or by virtue of the Account Holders’Controlling Persons. This can be depicted as per following diagram:

2. Reportable Accounts by virtue of the Account Holder

Rule 114F(6)(a) states that “reportable account”is a financial account, which has been identified, pursuant to the due diligence procedures prescribed in Rule 114H, as held by a reportable person.

Reportable person has been defined in the Rule 1 14F(8) and means-

(a) one or more specified U.S. persons; or

(b) one or more persons other than:

i. a corporation the stock of which is regularly traded on one or more established securities markets;

ii. any corporation that is a related entity of a corporation described in item (i);

iii. a Governmental entity;

iv. an International organisation;

v. a Central bank; or

vi. a financial institution

that is a resident of any country or territory outside India (except United States of America) under the tax laws of such country or territory or an estate of a decedent that was a resident of any country or territory outside India (except United States of America) under the tax laws of such country or territory.

Thus, generally speaking, there are two types of reportable person. First one has been defined specifically for USA. Second one is for the other countries.

U.S. Person means,

(a) an individual, being a citizen or resident of the United States of America;

(b) a partnership or corporation organized in the United States of America or under the laws of the United States of America or any State thereof; (c) a trust if,-

(i) a court within the United States of America would have authority under applicable law to render orders or judgments concerning substantially all issues regarding administration of the trust; and

(ii) one or more U.S. persons have the authority to control all substantial decisions of the trust; or

(c) an estate of a decedent who was a citizen or resident of the United States of America;

Specified U.S. person means a U.S. Person, other than the persons referred to in sub-clauses (i) to (xiii) of clause (ff) of Article 1 of IGA which is at Appendix A.

(Ref: Page 57 of CRS and 192 of Commentary)

3. Reportable Accounts by virtue of the Account Holder’s Controlling Persons

3.1. Regardless of whether the Financial Account is a Reportable Account by virtue of the Account Holder, a second test in relation to the Controlling Persons of certain Entity Account Holders needs to be applied to ascertain whether the Controlling Persons of such Entities are residents of countries/territories outside India. If this test is satisfied, the account would be Reportable Account.

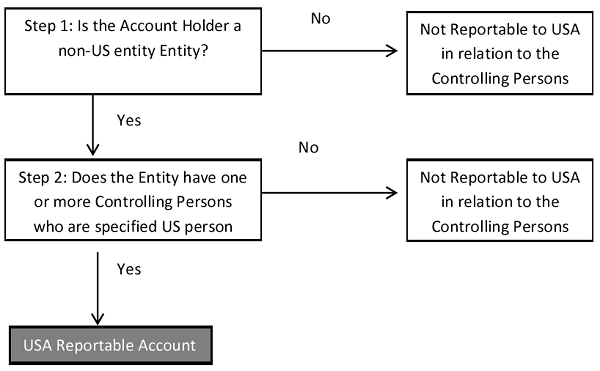

3.2. In case of USA, first it needs to be identified whether account is held by an entity, which is not based in USA and if yes, whether one or more controlling person of entity is specified U.S. person. If both of conditions are satisfied, the account will be US Reportable Account. This can be depicted as per following diagram:

Figure: Steps for USA Reportable Account

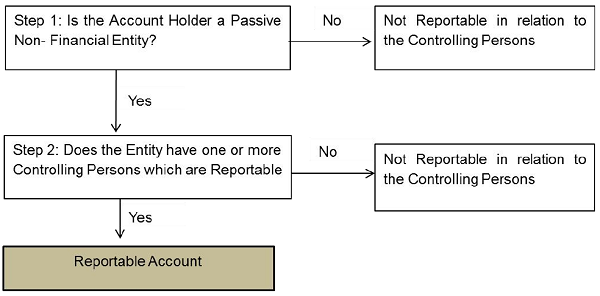

3.3. In the case of other countries/territories, if the account is held by a Passive Non-Financial Entity (NFE) with one or more controlling persons resident in a country/territory outside India, then account will be reportable. This can be depicted as per following diagram:

Figure: Steps for Other Reportable Account

3.4. Non-Financial Entity (NFE) is an entity which is not a financial institution. There are two types of NFE – active and passive. The distinction is important since a financial institution in India is required to apply a higher standard of due diligence to financial accounts held by a passive NFE. The financial institution is required to determine whether the passive NFE is controlled by one or more Reportable persons. Active NFE has been defined in Explanation (A) to Rule 1 14F(6) and includes regularly traded entities etc.

3.5. Passive NFE is defined in Explanation (D) to Rule 1 14F(6) as

(i) any non-financial entity which is not an active non-financial entity; or

(ii) an investment entity described in sub-clause (B) of clause (c) of the Explanation to clause (3) of Rule 114F

(iii) not a withholding foreign partnership or withholding foreign trust

3.6. The general rule is that a Passive NFE is an NFE that is not an Active NFE. The definition of Active NFE includes entities that are publicly traded (or related to a publicly traded Entity), Governmental Entities, International Organisations, Central Banks, or a holding NFEs of non financial groups and essentially excludes Entities that primarily receive passive income or primarily hold amounts of assets that produce passive income (such as dividends, interest, rents etc.).

However, an entity will not be active NFE which functions or holds itself out as an investment fund, such as a private equity fund, venture capital fund, leveraged buyout fund, or any investment vehicle whose purpose is to acquire or fund companies and then hold interests in those companies as capital assets for investment purposes.

3.7. If the Entity Account Holder is a Passive NFE then the Financial Institution must “look-through” the Entity to identify its Controlling Persons. If the Controlling Persons are Reportable Persons then information in relation to the Financial Account must be reported, including details of the Account Holder and each reportable Controlling Person.

Controlling Person

3.8. Controlling Person is defined in Explanation (B) to Rule 1 14F(6). Controlling person means the natural person who exercises control over an entity and includes a beneficial owner as determined under sub-rule (3) of rule 9 of the Prevention of Money-laundering (Maintenance of Records) Rules, 2005. It has been specified that in determining the beneficial owner, the procedure specified in the following circular as amended from time to time shall be applied, namely:-

(i) AML.BC. No.71/14.01.001/2012-13, issued on the 18th January, 2013 by the Reserve Bank of India; or

(ii) CIR/MIRSD/2/2013, issued on the 24th January, 2013 by the Securities and Exchange Board of India; or

(iii) IRDA/SDD/GDL/CIR/0 19/02/2013, issued on the 4th February, 2013 by the Insurance Regulatory and Development Authority.

3.9. Controlling person includes beneficial owner. For different type of entities, beneficial owner are described as below:

| Entity | Beneficial Owner is natural person(s) who whether acting alone or together, or through one or more juridical person |

| Company | a. has a controlling ownership interest (>25%) or

b. who exercises control through right to appoint majority of the directors or to control the management or policy decisions including by virtue of their shareholding or management rights or shareholders agreements or voting agreements |

| Partnership Firm | has ownership of/entitlement to more than fifteen per cent (15 %) of capital or profits of the partnership |

| Unincorporated Association or Body of Individuals | has ownership of or entitlement to more than fifteen per cent (15 %) of the property or capital or profits of such association or body of individuals |

3.10. Where no natural person is identified as above, the beneficial owner is the relevant natural person who holds the position of senior managing official.

3.11. Where the client or the owner of the controlling interest is a company listed on a stock exchange, or is a subsidiary of such a company, it is not necessary to identify and verify the identity of any shareholder or beneficial owner of such companies.

3.12. In the case of a trust, the controlling person means the settlor, the trustees, the protector (if any), the beneficiaries or class of beneficiaries, and any other natural person exercising ultimate effective control over the trust, and in the case of a legal arrangement other than a trust, the said expression means the person in equivalent or similar position. If the settlor, trustee, protector, or beneficiary is an Entity, the Reporting Financial Institution must identify the Controlling Persons of such Entity as discussed above.

3.13. Thus, if the Controlling Persons of a Passive NFE having an account in a Reporting Financial Institution are persons resident of a country/territory outside India, the account becomes a Reportable Account for all such countries/territories outside India , for which the controlling persons are tax resident. The details of the controlling person(s) will also be reportable to the respective country (ies) or territory (ies) outside India.

HUF

3.14. In the case of HUF, the financial account of HUF shall be treated as an entity account. The due diligence of HUF accounts will be same as prescribed under PMLA/ KYC procedures.

(Ref: Page 57 of CRS and 195 of Commentary)

4. Centralized facilities for the clearing, settlement and deposit of securities

In India, an entity designated under federal legislation to provide centralized facilities for the clearing, settlement and deposit of securities, commonly referred to as a Clearing Corporation, will not be treated as maintaining financial accounts. In India, such entities are National Securities Clearing Corporation Ltd (NSCCL), Indian Clearing Corporation Ltd (ICCL) and MCXSX Clearing Corporation Ltd (MCX-SXCCL).

Source- Guidance Note on FATCA and CRS as updated on 30th November 2016

Hi, great article.

Unfortunately I am a victim of low cibil score and was looking measures to improve it as I also wanted to avail a personal loan to renovate my house. Please suggest me as the banks keep cibil score as the fundamental factor in giving loans.