Adesh Hemant Tiwari

Introduction :

Now a days as we all know importance and use of automated software for accounting as well as for record keeping has been increased. Risk factor also has challenging role while conducting the audit in automated environment. To facilitate these challenges there are already many theorems are present but the important thing is how far we can use them while working in audit and assurance field.

Out of these theorems one is Benford’s law which is mainly concerns with numeric indicators related to manipulation of accounts and records.

Benford’s law describes the relative frequency distribution for leading digits of numbers in datasets.

In this article we are discussing the possible ways to implement this theorem with understanding our needs and business practices of record keeping.

Facts of Law:-

it is an observation that in many real-life sets of numerical data, the leading digit is likely to be small. Generally In sets that obey the law, the number 1 appears as the leading significant digit about 30% of the time, while 9 appears as the leading significant digit less than 5% of the time. If the digits were distributed uniformly, they would each occur about 11.1% of the time.[Wikipedia]

Benford’s law also makes predictions about the distribution of second digits, third digits, digit combinations, and so on.

In short it is the frequency of occurrence of digits at first or second place in any relevant database as the case may be which is commonly observed in practice and probability is described by using percentage which is calculated by using formula = Log10(1+1/n).

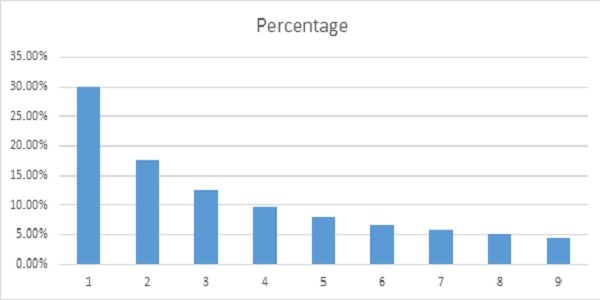

For calculating of probability of digit 1 we can put 1 in n’th place and got 30.1% and so on up to 9th digit, the probability percentage is stated below:-

If N is 1 then=30.1%

If 2 then=17.6%

If 3 then=12.5%

If 4 then=09.7%

If 5 then=07.9%

If 6 then=06.7%

If 7 then=05.8%

If 8 then=05.1%

If 9 then=04.6%

So we can calculate percentage of our data say Expenses list etc. by taking first digit of distribution and if occurrence is different than as above stated percentages then there is possibility of manipulation. The higher the difference higher is risk of manipulation.

Simple comparison of first-digit frequency distribution from the data with the expected distribution according to Benford’s law ought to show up any anomalous results [Wikipedia].

One practical use for Benford’s law is fraud and error detection. It’s expected that a large set of numbers will follow the law, so accountants, auditors, economists and tax professionals have a benchmark what the normal levels of any particular number in a set are.

Many audit software provides function which calculate deviation so one can calculate risk of manipulation.

However this law is not always stands true when:-

1. Distributions that would not be expected to obey Benford’s law

2. Where numbers are assigned sequentially: e.g. cheque numbers, invoice numbers.

3. Where numbers are influenced by human thought: e.g. prices set by psychological thresholds ($9.99)

4. Accounts with a large number of firm-specific numbers: e.g. accounts set up to record $100 refunds.

5. Accounts with a built-in minimum or maximum

6. Distributions that do not span an order of magnitude of numbers.

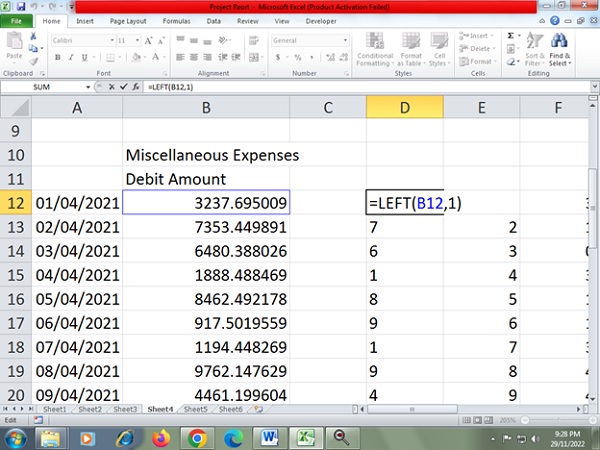

For using this law in excel:-

Select the first digit of your distribution by using “left” function.

Here the first digit is first number of 01-04-2021 miscellaneous expenses i.e.3 and for 02-04-2021 its 7 and so on.

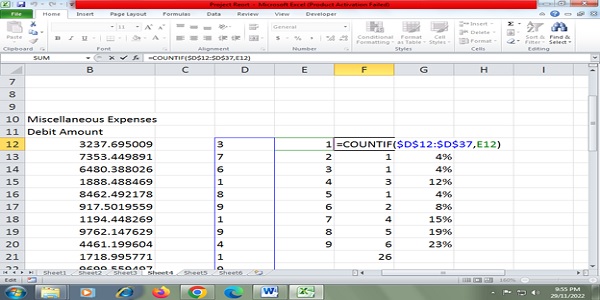

Then count how many times a single digit is repeated by using “count if” function and do this for all 1 to 9 digit

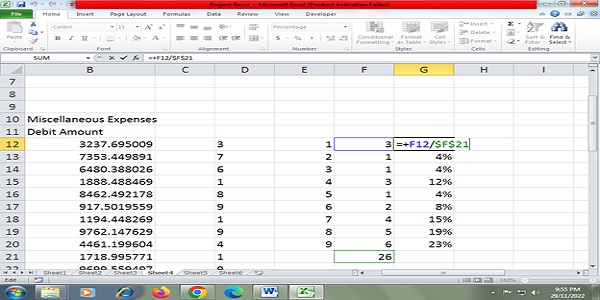

And calculate percentage of the same and compare with above stated numbers.

Let’s see with example :-

Suppose you have a list of miscellaneous expenses provided for vouching and have day wise expenses bifurcation like:-

01-04-20XX- 1240/-

02-04-20XX- 5647/-

03-04-20XX- 2758/-

04-04-20XX- 4487/-

05-04-20XX- 6512/- and so on.

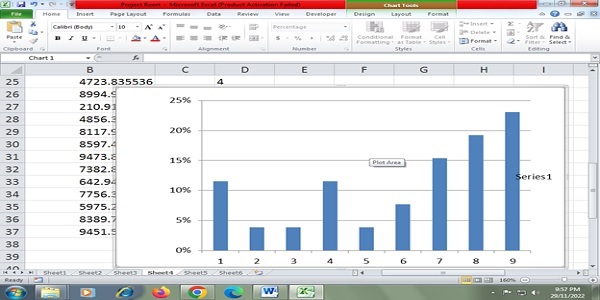

So in a column select the first digit by using “Left” Function, it will come 1,5,2,4,6 respectively for above, then apply “count if” function to calculate how many times 1 is repeated, do this for 1 to 9 digit and calculate percentage of repetition of each digit to the total of “count if column” you will got the result. Lastly compare the result with Benford’s law percentage and you will got the deviations.

If deviation is high then consider the risk of manipulation and fraud and proceed with further audit procedures.

Similarly like first digit the law provides for second and third digit as below:-[Wikipedia]

| Digit | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| 1st | — | 30.1% | 17.6% | 12.5% | 9.7% | 7.9% | 6.7% | 5.8% | 5.1% | 4.6% |

| 2nd | 12.0% | 11.4% | 10.9% | 10.4% | 10.0% | 9.7% | 9.3% | 9.0% | 8.8% | 8.5% |

| 3rd | 10.2% | 10.1% | 10.1% | 10.1% | 10.0% | 10.0% | 9.9% | 9.9% | 9.9% | 9.8% |

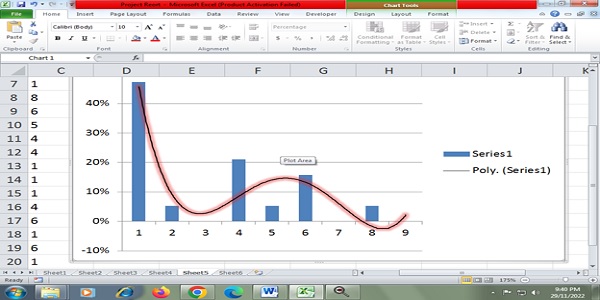

Now let us see what happen if data created by computer generated numbers or by manually typing.

As per the law if the data is created by computer generated numbers then your curve will be look like this:-

It means each number have nearly equal chance of occurrence at first place.

It means each number have nearly equal chance of occurrence at first place.

And when fictitious data is prepared by human beings it will look like:-

Mostly as bell shaped curve.

By applying the law and observing deviations one can reduce the risk of fraud say if your number 4 is not in accordance with the percentage described in law then you may go through the vouchers which are begins with number 4 or vouchers which have leading digit number 4.

Conclusion:

When there is large set of database one can use this tool for sampling purpose also, for example the deviations can be checked carefully. This law can be used by firms in excel where there is no automated software for auditing the data. However as already said, this law not always stands true and therefore other audit tools and professional judgement after considering the circumstances of the case and objective of the auditor should also be taken into account for the application of this law.