Ratio Analysis and it’s Usefulness: A ratio shows the arithmetical relationship between two figures that have some meaningful relationship between them. Financial ratios, thus, focus attention on the interrelationships between various items of financial statements.

Example : There can be a meaningful relationship between sale and direct expenditures but not between sales and depreciation. Similarly there is a meaningful relationship between PBIT and Equity Share Capital + Preference Share Capital + Debentures + Long term Loans. So there can be numerous ratios as per the need of the circumstance as and when required. The relationship would change if certain underlying business conditions change. Hence, a change in the ratio of gross profit to sales in a particular year would indicate that either the relevant business conditions have changed or that the figures are not reliable.

An auditor can use ratio analysis to identify anything abnormal or anything which deviates from the expected and the known. The rationale underlying the use of ratio analysis is that while absolute quantities can be manipulated easily, it may be quite difficult to manipulate all the figures which are interrelated. Such manipulation normally causes widespread repercussions and can be detected more easily. Example: Sales figure can be easily manipulated through forged invoices but it is difficult to get manipulated GP, NP and Direct Expenses ratios. This is because it may not be possible for the management to manipulate all the interrelated figures, i.e. cash, debtors, purchases, stocks, production, etc. The ratio of cost of material consumed to inventory i.e. inventory turnover or quantitative ratio of inputs to outputs would indicate that something abnormal has happened. Even if all these are adjusted fall in the ratios of expenses to sales would put the auditor to enquiry.

The use of ratios as an effective tool of audit, an auditor should be capable of:

- Identifying and measuring the basic interrelationships in financial data through computation of appropriate ratios; and

- Examining and interpreting the ratios and their significance in the light of actual business circumstances.

Interpretation of ratios depends on the skill and experience of the auditor. In addition, the auditor also need to have a thorough understanding of accounting procedures and concepts, a practical appreciation of business problems and an insight into the economic conditions in which the particular enterprise operates. Ratios highlight only symptoms. It is for the auditors to study these symptoms properly, correlate them, and reach definite conclusions or identify areas for further enquiry. Each ratio reflects a certain symptom and all the symptoms should be analyzed as whole.

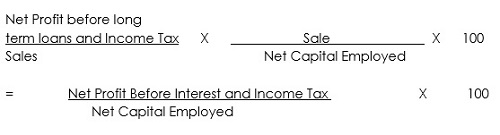

Some meaningful ratios for the Auditors:

A. Return on Investment (ROI): This ratio is the broadest measure of the overall performance of the enterprise. It take care of many things – Cost – Price relationship of various products, Operating Efficiencies and efficiency with which an enterprise uses it’s funds and thus shows the net effect of various performances ratios.

Formula :

Net Profit before Interest on Long – Term Loans and Income Tax X 100

Net Capital Employed

Net capital employed is the amount of funds invested in a business and is calculated from the balance sheet in either of the following two ways:

1. Equity share capital plus preference share capital plus reserve and surplus plus long term loans and long term liabilities minus miscellaneous expenditure and debit balance of profit and loss account (if any such item appear on the assets side of the balance sheet).

2. Fixed Assets plus Current Assets plus investments minus current liabilities.

ROI itself is the function of the net profit ratio and the capital turnover rate. i.e.

Thus if an auditor finds that the ROI of an enterprises is lower/higher than in previous years, He should make an analysis by working out the net profit and capital turnover rate.

Constituents of Capital Turnover Rate: This rate measures the effectiveness with which an enterprises uses the resources at it’s disposal. It ensure making adequate sales by managing funds properly and keeping them in constant use. Proper fund management is to maintain fixed assets, Inventory, Debtors, cash at optimum level. This also includes constitution of optimum credit, inventory and purchase policy.

Constituents of Net Profit Ratio: Net Profit is derived through Operating Profit which is result of Various Direct Expenditures, Indirect Varaible Expenditures and Indirect Fixed Expenditures.

Following Diagram can further explain it:

An auditor may through this analysis may find out whether the variation in the capital turnover the variation in the capital turnover rate are the result of actual changes in business circumstances or whether they arises due to a manipulation of figures.

Conclusions which can be deduced from following ratios (Other than existence of manipulation):

Fixed Assets Turnover Rate : Effectiveness with which the fixed assets are utilized.

Stock Turnover Rate : Accumulation/ Shortage of Stock

Debtors Turnover Rate: Changes in Credit Policy Or changes in collection procedure/Performance

Creditors Turnover Rate: Changes in Credit period enjoyed or changes in payment terms

B. Ratios related with profitability: Relating Sales with net profit (before interest on long term loans and income tax), and various items of direct and indirect costs and gross profit an auditor can gather useful information about operating efficiency of an enterprise. Variation in any of these ratios in a particular year would call for further enquiry by the auditor.

Net Profit Ratio: Variation may indicate either the gross gain or indirect cost have change in relation to sales (as %). For Further analysis one should resort to:

1. Material Cost Ratio: i.e. Relationship of cost of material consumed with sales.

2. Conversion cost Ratio: i.e. Manufacturing Expenses (Excluding Material) to sales. Separate ratio showing the relationship of each such item with sales.

3. Administrative Overheads and Selling and Distribution Overheads to sales

4. Gross Profit Ratio: It primarily depends on conversion process and on the market forces of supply and demand as regard raw material and finished goods. One should analyze gross profit ratio of all products separately and compare with those of previous year. Changes may be due to changes in sales price, prices of raw material, labor cost etc.

C. Ratios Related with Financial Position: These ratios indicate the financial health of an enterprise. These ratios relate various items of balance sheet with each other to show whether or not an enterprise is in a position to meet its obligation as and when they become due. These obligations may be both short term and long term. Ratios indicating financial health are calculated from the balance sheet. Such ratios are relevant for auditor from two angles. Firstly they assist him in understanding certain structural relationships relating to the financing of the enterprises. Secondly, abnormalities in these ratios may indicate that certain figures in the financial statements need a closer examination. Some such ratios are:

1. Current Ratio: As and when the activity level increases beyond a certain limit without corresponding increase in capital employed current ratio should normally fall. Similarly Current ratio may increase if activity level reduces without corresponding reduction in capital employed (such situation is signaled by reduced ROI)

2. Acid Test Ratio

3. Debt Equity Ratio: In case of abnormally high ratio it may signal threats as to solvency if profitability is low.

4. Long – Term Ratio: it shows relationship between fixed assets and long term funds employed in the business. Ideally Long term funds should be more than long term application for a healthy business.

| Long Term Funds | Fixed Assets |

| Short Term Funds | Current Assets |

Author Bio