1. Introduction:

1.1. In the Indirect Taxation, both assessee and the Department have been conferred with a right of two or three stage appellate remedies. Against the orders passed by the officers of the rank of Principal Commissioner /Commissioner of Central Excise/Customs/Service Tax or passed by ADG ( Adjudication), DRI/DGCEI in the capacity of an adjudicating authority, the first appeal lies before the Customs, Excise & Service Tax Appellate Tribunal (i.e. CESTAT).

1.2. However, against the orders passed by the officers, who are lower than the rank of Principal Commissioner /Commissioner of Central Excise /Customs /Service Tax, the first appeal lies to the Commissioner (Appeals) and there from, appeals lies either to the Joint Secretary ( Revision Application) or CESTAT, as the case may be.

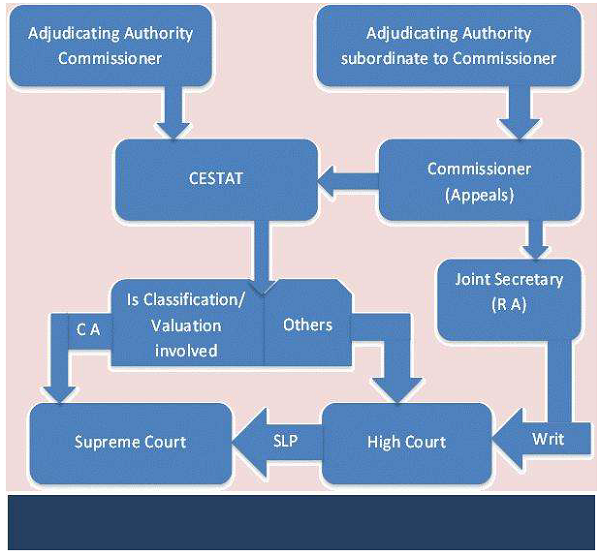

1.3. Against the Order Passed by CESTAT, the Appeal lies before the High Court (in cases other than cases relating to determination of the rate of duty or value of goods) or before the Supreme Court directly if the case relates to the Rate of duty or value of goods, as the case may be. Where the order of the Tribunal does not relate to determination of rate of duty or value of goods, an appeal lies to the High Court. Appellate remedies in Customs/Excise/Service tax matters can be easily understood from the flow diagram i.e. Fig. 1 given below:-

Figure – 1

2. About Customs, Excise & Service Tax Appellate Tribunal (CESTAT)

2.1 The provision for establishing the Customs, Excise and Gold (Control) Appellate Tribunal i.e. CEGAT (now renamed as Customs, Excise & Service Tax Appellate Tribunal i.e. CESTAT with effect from 14.5.2003 vide the Finance Act, 2003) was made in the Finance Act, 1980. The Tribunal was constituted with effect from 11.10.1982 vide MF (DR) Notification No. 223/82- Customs, dated 11.10.1982.

2.2 The CESTAT is headed by its President. There is provision for a Senior Vice-President and Vice-Presidents, besides Judicial Members and Technical Members. The work of the Tribunal has been distributed amongst various Zonal / Regional Benches.

2.3 Special Benches consist of not less than two members, at least one being a Judicial Member and one a Technical Member. Regional Benches deal with matters other than those falling within the jurisdiction of the Special Benches. These consist of two Members – one a Judicial Member and one a Technical Member.

2.4 There is also a provision for Single Member Benches which are competent to dispose of cases within the specified monetary limits falling within the jurisdiction of Regional Benches.

2.5 At present, CESTAT functions through 9 Zonal / Regional Benches located at New Delhi, Mumbai, Chennai, Kolkata, Bangalore, Ahmedabad, Allahabad, Chandigarh & Hyderabad. Jurisdiction of Zonal /Regional Benches of CESTAT is given in Table-1 below:-

Table – 1

| Sr. No. | Title of the Bench | Location | Jurisdiction |

| 1. | North Zonal Bench | New Delhi | States of Madhya Pradesh, Chhattisgarh, Uttarakhand, Rajasthan, and NCR of Delhi |

| 2. | Western Zonal Bench (Mumbai) | Mumbai | States of Maharashtra & Goa |

| 3. | West Zonal Bench (Ahmedabad) | Ahmedabad | State of Gujarat and Union Territories of Dadra & Nagar Haveli and Daman & Diu |

| 4. | South Zonal Bench (Chennai) | Chennai | State of Tamil Nadu and Union Territory of Pondicherry except Yanam Commune |

| 5. | South Zonal Bench (Benga lu ru) | Bengaluru | State of Karnataka, Kerala and UT of Lakshadweep. |

| 6. | East Zonal Bench | Kolkata | States of Bihar, Jharkhand, Orissa, West Bengal, Assam, Manipur, Meghalaya, Nagaland, Sikkim, Tripura, Arunachal Pradesh, Mizoram and Union Territory of Andaman & Nicobar islands. |

| 7. | Regional Bench, Chandigarh (with effect from 01.12.15) | Chandigarh | Union Territory of Chandigarh, the States of Punjab & Haryana, Jammu& Kashmir and Himachal Pradesh. [notified vide notification No. 02/2015 dated 04.11.2015 issued by Registrar, CES TA TI |

| 8.. | Regional Bench, Allahabad ( with effect from 1 .9 .2015) | Allahabad | State of Uttar Pradesh

[notified vide notification No. 01/2015 dated 04.11.2015 issued by Registrar, CES TA TI |

| 9.. | Regional Bench, Hyderabad (with effect from 14.12.2015) | Hyderabad | Territorial jurisdiction of erstwhile state of Andhra Pradesh i.e. Andhra Pradesh, Telangana and Yanam commune of the Union Territory of Pondicherry.[notified vide notification No. 03/2015 dated 06.11.2015 issued by Registrar, CES TAT] |

3. Summary of Relevant Legal Provisions at a Glance

The summary of legal provisions dealing with filing of appeal before CESTAT is given in Table 2 below:-

Table – 2

| Sr. No. | Section /Rules /notification/Circular /Instructions |

Subject |

| Customs | ||

| 1. | Section 129 of the CA, 1962 | Provides for constitution of the Appellate Tribunal |

| 2 | Section 129 A of CA, 1962 | Provides mechanism for filing appeal against the Orders of Principal Commissioner/Commissioner/ADG (Adjudication) DRI or Commissioner (Appeals) |

| 3 | Section 129B of CA, 1962 | Lays down provisions providing for following the Principles of natural justice, timeline for deciding appeals, and rectification of mistakes by Tribunal while passing order. |

| 4 | Section 129C of CA, 1962 | Provides various procedures to be followed by CESTAT. |

| Central Excise | ||

| Section 35 B of the CEA Act, 1944 | Provides mechanism for filing appeal against the Orders of Principal Commissioner/ Commissioner/ ADG (Adjudication) DGCEI or Commissioner (Appeals) | |

| Section 35C of the CEA, 1944 | Lays down provisions providing for following the Principles of natural justice, timeline for deciding appeals, and rectification of mistakes by Tribunal while passing order. | |

| 7. | Section 35D of the CEA, 1944 | Provides various procedures to be followed by CESTAT. |

| Service Tax | ||

| 8 | Section 86 of FA, 1994 | Provides for filing of Appeal before CESTAT. |

| Rules | ||

| 9. | Customs, Excise and Service Tax Appellate Tribunal (Procedure) Rules, 1982 | Provide various procedures to be followed at CESTAT |

| 10 | Central Excise (Appeals) Rules, 2001 | Proscribe various procedures to be followed at Appellate stages and the Forms in which Appeals/Cross Objections are to be filed. |

| 11 | Customs (Appeals) Rules, 1982 | |

| 12 | Rule 9 of Service Tax Rules, 1994 | |

| Relevant CBEC Circulars /Instructions | ||

| 13 | Circular No. 935/25/2010-CX, dated 21.09.2010 | Measures to streamline the processing of departmental litigation before the Courts and Tribunal |

| 14 | Instruction issued vide F. No. 390/Misc./100 /2010-JC, dated 22.09.2011 | Filing of appeal in the wrong forum in matters relating to valuation or determination of rate of duty |

4. Mechanism to file appeal before CESTAT: Important features

Summary of important features of mechanism to file appeal before CESTAT under Custom, Central Excise and Service Tax laws has been given in Table- 3 below.

Table – 3

| Sr. No. | Description | Particulars/ Details | Relevant Statutory Provision/ Authority (*) |

|

| 1 | Statutory provisions relating to filing of Appeal before CESTAT | In Central Excise | Section 35B, 35C & 35D of CEA, 1944 | |

| In Customs | Section 129A, 129 B & 129C of CA, 1962 | |||

| In Service Tax | Section 86 of FA, 1994 | |||

| 2 | Time limit for filing appeal before CESTAT |

In Central Excise:-

3 months from the date of communication of order. |

Section 35B(3) of CEA, 1944 | |

| In Customs:-

3 months from the date of communication of order. |

Section 129A(3) of CA, 1962 | |||

| In Customs:- 3 months from the date of communication of order. |

Section 86(1) of FA, 1994 | |||

| 3 | Prescribed Forms for filing appeals by the party and for filing memorandum of Cross Objections | Central Excise | E.A.-3 [for filing appeal by the Party] E.A.-4 [for filing Memorandum of Cross Objections] | Rule 6 of Central Excise Appeals Rules, 2001 |

| Customs | C.A.-3 [for filing appeal by the Party] C.A.-4 [for filing Memorandum of Cross Objections] | Rule 6 of the Customs Appeals Rules, 1982 |

||

| Service Tax | ST-5 [for filing appeal by the Party]

ST-6 [for Memorandum of Cross Objections] |

Rule 9 of the STR | ||

| 4. | Form for filing appeal before Tribunal by Department | C. Ex. | EA-5 | Rule 7 of Central Excise (Appeals) Rules, 2001 |

| Custom | CA-5 | Rule 7 of the Customs (Appeals) Rules, 1982 |

||

| Service Tax | ST-7 | Rule 9(2) & 9(2A) of the Service Tax Rules, 1994 |

||

| 5 | Quantum of pre- deposit at the time of |

1. If the appeal is filed against the O-I-O passed by the Principal Commissioner/ Commissioner /ADG (adjudication) DRI/DGCEI: 7.5% of the duty and/or penalty 2. If the appeal is filed against the O-I-A passed by the Commissioner (Appeals): 10% of the duty and/ or penalty | Section 35F of CEA, 1944 and Section 129E of CA, 1962; Ref: CBEC Circular No. 984/8/ 2014-CX dated 16.09.2014 | |

P.S.: CEA means Central Excise Act, 1944; CA means Customs Act, 1962; FA means Finance Act, 1994; and STR means Service Tax Rules.

5. Time Limit for Filing Appeal before CESTAT

As per Section 35B (3) of the Central Excise Act, 1944, and Section 129A (3) of the Customs Act, 1962, the appeal before CESTAT should be filed within three months of the communication of the order, whether it is filed by the party or by the department. However, the Appellate Tribunal may admit an appeal or permit the filing of a memorandum of cross-objections after the expiry of the relevant period, if it is satisfied that there was sufficient cause for not presenting it within that period.

Similarly, as per Section 86(1) of the Finance Act, 1994, the appeal in service tax matters has to be filed within three months of the date of receipt of the order.

6. Important Points regarding procedures to be followed at CESTAT/ Appeal Rules

Various procedures to be followed at CESTAT are enumerated in the Customs, Excise and Service Tax Appellate Tribunal (Procedure) Rules, 1982. For text of these Rules, e-book on filing Appeals before CESTAT-Part II may be referred. However, important details of the CESTAT Procedure Rules are explained below:-

- The language of the Tribunal shall be English. However, the parties to a proceeding before the Tribunal are allowed to file documents drawn up in Hindi. Moreover, a Bench may also permit the use of Hindi in its proceedings [Ref: Rule 5 of the CESTAT (procedure) Rules]

- The final order passed by Tribunal is in English. However, the Tribunal may pass such orders in Hindi if deemed fit. If order passed by Tribunal is in Hindi, then every such order is required to be accompanied by duly attested English translation of the same.

- The appeals have to be filed by the appellant in person or by an agent to the concerned officer in the prescribed Form, or may send the same by registered post [Ref: Rule 6 of the CESTAT (Procedure) Rules]

- Each aggrieved person is required to file a separate appeal and common appeals or joint appeals are not allowed [Ref: Rule 6 A of the CESTAT (Procedure) Rules].

- The parties to the appeal are not entitled to produce any additional evidence, however, in specific circumstances, the Tribunal may permit to produce additional evidence or affidavit etc. as detailed in the said Rule [Ref: Rule 23 of the CESTAT (Procedure) Rules].

The offices of the Tribunal remains open daily from 9.30 A.M. to 6.00 P.M. except on Saturdays, Sundays and other public holidays. Further, no work, unless of urgent nature, is admitted after 5.30 P.M. [Ref: Rule 42 of the CESTAT (Procedure) Rules]

7. Forms for Filing Appeals before CESTAT

7.1 Rule 6 of the Central Excise (Appeals) Rules, 2001 prescribes Forms in which appeals are required to be filed before Tribunal in Central Excise Matters. The Form prescribed for filling appeal before Tribunal is EA-3, whereas the Memorandum of cross-objections is required to be filed in Form No. E.A.-4. Each of these Form has to be filed in quadruplicate and is required to be an equal number of copies of the order appealed against (one of which at least shall be a certified copy).

7.2 Similarly, as per Rule 6 of the Customs (Appeals) Rules, 1982, relevant forms for appeal and memorandum of cross objections prescribed are C.A.-3 & C.A.-4 respectively.

7.3 In service tax matters, as per Rule 9 of the Service Tax Rules, 1994, relevant forms for appeal and memorandum of cross objections prescribed are Form ST-5 & ST-6 respectively.

8. Fees for Filing Appeal before CESTAT

8.1 As per Section 35(B)(6) of the Central Excise Act, 1944, Section 129A(6) of the Customs Act, 1962 and Section 86(6) of the Finance Act, 1994, an appeal to the Appellate Tribunal is required to be accompanied by a fee as given below in the Table -4.

| Where the amount of Central Excise Duty/ Customs duty/ Service Tax and interest demanded and penalty levied is five lakh rupees or less | Rs.1,000/- |

| Where the amount of duty/ tax and interest demanded and penalty levied is more than five lakh rupees but not exceeding fifty lakh | Rs.5,000/- |

| Where the amount of duty/ tax and interest demanded and penalty | Rs.10,000/- |

| levied is more than fifty lakh rupees, |

No fee is payable in the case of Departmental appeal or a memorandum of cross‑

objections.

As per Section 35(B)(7) of the Central Excise Act, 1944, Section 129A(7) of the Customs Act, 1962 and Section 86(6A) of the Finance Act, 1994, every application made before the Appellate Tribunal, (a) in an appeal for rectification of mistake or for any other purpose; or (b) for restoration of an appeal or an application, is required to be accompanied by a fee of five hundred rupees. However, no such fee is payable in the case of an application filed by the Department.

9. Order by CESTAT

The Appellate Tribunal may, if sufficient cause is shown, at any stage of hearing of an appeal, grant time, from time to time, to the parties or any of them and adjourn the hearing of the appeal. However, no such adjournment shall be granted more than three times to a party during hearing of the appeal. The Appellate Tribunal may, after giving the parties to the appeal an opportunity of being heard, pass such orders thereon as it thinks fit, confirming, modifying or annulling the decision or order appealed against or may refer the case back to the authority which passed such decision or order with such directions as the Appellate Tribunal may think fit, for a fresh adjudication or decision, as the case may be, after taking additional evidence, if necessary.

10. Time Limit for Decision by CESTAT

The Appellate Tribunal shall, where it is possible to do so, hear and decide every appeal within a period of three years from the date of filing appeal. The Appellate Tribunal is required to send a copy of every such order passed to the Commissioner of Central Excise and the party to the appeal.

11. Rectification of Mistake

As per Rule 31A of Customs, Excise and Service Tax Appellate Tribunal (Procedure) Rules 1982, an application for rectification of a mistake apparent from the record, under sub-section (2) of section 129B of the Customs Act, or sub-section (2) of section 35C of the Central Excise Act, 1944, or sub-section (2) of section 81A of the Gold (Control) Act, is to be heard by a Bench consisting of the Members who heard the appeal giving rise to the application, unless the President directs otherwise.

The Appellate Tribunal may, at any time within six months from the date of the order, with a view to rectifying any mistake apparent from the record, amend any order passed by it and shall make such amendments if the mistake is brought to its notice by the Principal Commissioner or Commissioner of Central Excise or the other party to the appeal. However, in case of an amendment, having the effect of enhancing an assessment or reducing a refund or otherwise increasing the liability of the other party, the Appellate Tribunal is required to give notice to him of its intention to do so and after allowing him a reasonable opportunity of being heard. [Ref: Section 35C(2) of Central Excise Act, 1944 & Section 129 B(2) of Customs Act, 1962]

12. Departmental Appeals before CESTAT [Commonly known as Review Proceedings]

A. Appeal against the Orders passed by the Commissioner (Appeals)

12.1 As per Section 35B(2) of the Central Excise Act, 1944, the Committee of Commissioners of Central Excise may, if it is of opinion that an order passed by the Commissioner (Appeals) is not legal or proper, direct any Central Excise Officer authorised by him in this behalf to appeal to the Appellate Tribunal against such order.

12.2 In cases, where the Committee of Commissioners of Central Excise differs in its opinion regarding appeal against the order of the Commissioner (Appeals), the matter is required to be referred to the jurisdictional Principal Chief

Commissioner/Chief Commissioner. If the Principal Chief Commissioner or Chief Commissioner after consideration of the order is of opinion that the order is not legal or proper, then he may direct any Central Excise Officer to file appeal before CESTAT against such order.

12.3 Similar provisions are contained in Section 1 29A (2) of the Customs Act, 1962 and Section 86 (2A) of the Finance Act, 1994.

B. Application against the Orders passed by the Principal Commissioner or the Commissioner of Central Excise/ ADG (Adjudication) DGCEI/DRI:-

12.4 As per Section 35E(1) of the Central Excise Act, 1944, the Committee of Principal Chief Commissioner /Chief Commissioners of Central Excise may, of its own motion, call for and examine the record of any proceeding in which a Principal Commissioner or Commissioner of Central Excise as an adjudicating authority has passed any decision or order for the purpose of satisfying itself as to the legality or propriety of any such decision or order and may, by order, direct such Commissioner or any other Commissioner to apply to the Appellate Tribunal for determination of such points arising out of the decision or order as may be specified by the Committee of Chief Commissioners of Central Excise in its order.

12.5 Where the Committee of Principal Chief /Chief Commissioners of Central Excise differs in its opinion as to the legality or propriety of the decision or order of the Principal Commissioner or the Commissioner of Central Excise, the matter is required to be referred to the Board for consideration. The Board after considering the facts of the decision or order, may, by order, direct such Commissioner or any other Commissioner to apply to the Appellate Tribunal for determination of such points arising out of the decision or order as may be specified in its order.

12.6 Similar provisions are contained in Section 129D(1) of the Customs Act, 1962 and Section 86(2) of the Finance Act, 1994.

C. Time limits for filing departmental appeals

12.7 As per Section 35E (3) of Central Excise Act, 1944, every order u/s 35E(1) shall be made within a period of three months from the date of communication of the decision or order to be appealed. However, w.e.f. 06.08.2014, it has been provided that the Board may, on sufficient cause being shown, extend the said period by another thirty days.

12.8 As per Section 35E(4) of the Central Excise Act, 1944, after the said order by the Committee of Chief Commissioners, the appeal before CESTAT shall be filed within one month of the said order. Further, it has been provided that the appeal should be filed within a period of one month from the date of communication of the said order.

12.9 However, as the appeals against the order of the Commissioner (Appeals) are covered under Section 35B(2), the total time available for filing appeal is 3 months only.

12.10 Similar provisions are contained in Section 129D(3) & 129D(4) of the Customs Act, 1962.

12.11 As per Section 86(3) of the Finance Act, 1994, the appeal against the orders of Commissioner or Commissioner (Appeals) is required to be filed within four months from the date on which the order sought to be appealed against is received by the Committee of Chief Commissioners or, as the case may be, the Committee of Commissioners.

D. Constitution of Review Committees of Principal Chief Commissioners or Chief Commissioners

Section 35B (1B) of Central Excise Act, 1944, Section 129A(1B) of Customs Act, 1962 and Section 86(1A) of Finance Act, 1994 empower CBEC to constitute the Committees of two Chief Commissioners for the purpose of judging the acceptability of the Orders passed by the Principal Commissioners/Commissioners. Similarly, Committee of two Commissioners is to be constituted for the purpose of judging the acceptability of the orders passed by the Commissioner (Appeals).

In exercise of the above powers, CBEC has issued several ORDERs constituting Committees of Principal Chief /Chief Commissioners & Committee of Principal Commissioners/ Commissioners as explained in Table -5 below:-

Table – 5

| Order No. & date | Details of the Committee |

| Committee of Principal Chief /Chief Commissioners | |

| Office Order No. 2/2014-CE, dated 15.10.2014 | Jurisdictions of Committee of two Principal Chief Commissioners/ Chief Commissioners in Central Excise matters |

| Office Order No. 3/2014-Cus, dated 15.10.2014 read with corrigendum issued vide Office Order – 10 dated 12.11.2014 | Jurisdictions of Committee of two Principal Chief Commissioners/Chief Commissioners in Customs matters |

| Office Order No. 4/2014-ST, dated 15.10.2014 read with corrigendum issued vide Office Order – 10 dated 12.11.2014 | Jurisdictions of Committee of two Principal Chief Commissioners/ Chief Commissioners in Service Tax matters |

| Committee of Principal Commissioners/Commissioners | |

| Office Order No. 5/2014-CE dated 22.10.2014 read with corrigendum issued vide Office Order – 10 dated 12.11.2014 | Jurisdictions of Committee of two Principal Commissioners /Commissioners in Central Excise matters |

| Office Order No. 7/2014-Cus & 8/2014 dated 22.10.2014 read with corrigendum issued vide Office Order – 10 dated 12.11.2014 | Jurisdictions of Committee of two Principal Commissioners/ Commissioners in Customs matters |

| Office Order No. 6/2014-ST dated 22.10.2014 read with corrigendum issued vide Office Order –10 dated 12.11.2014 | Jurisdictions of Committee of two Principal Commissioners/Commissioners in Service Tax matters |

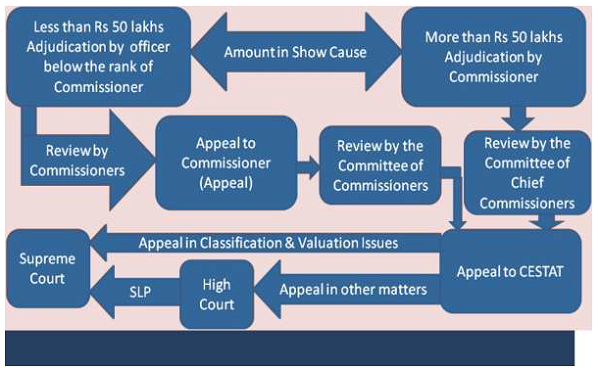

E. Provisions relating to the review of the order passed by the Adjudicating authority / Appellate Authority in Customs/ Excise/ Service Tax matters.

The flow diagram explaining the review mechanism of the order passed by the Adjudicating /Appellate Authorities in Customs/Central Excise /Service Tax matters is given below in Figure 2.

Figure – 2

F. Forms Prescribed for filing Departmental Appeals.

Separate form has been prescribed for the department to file appeal before Tribunal. The various Forms prescribed are as under:

(a) Rule 7 of Central Excise Appeal Rules, 2001 provides that an appeal before the Appellate Tribunal u/s 35B (1) of the Central Excise Act, 1944 should be made in Form No. E.A. 5.

(b) Rule 7 of Customs (Appeals) Rules, 1982 provides that an appeal before the Appellate Tribunal should be made in Form No. C.A.-5.

(c) Rules 9(2) & 9(2A) of the Service Tax Rules, 1994, provides that appeal before the Appellate Tribunal should be made in Form No. S.T.-7.

For viewing format of the above said forms and new alpha-numeric codes prescribed for numbering the Order in original passed by Commissioners/ Commissioner (Adjudication) and Order in Appeal passed by the Commissioner (Appeals), refer to e-book on filing appeals before CESTAT- Part IV

13. Deposit, pending appeal, of duty demanded or penalty levied

After enactment of the Finance Act (No.2), 2014 w.e.f. 06.08.2014, Section 35F of the Central Excise Act, 1944 and Section 129E of the Customs Act, 1962 have been substituted with new sections to prescribe mandatory pre-deposit as a percentage of the duty demanded where duty demanded is in dispute or where duty demanded and penalty levied are in dispute. Where penalty alone is in dispute, the pre-deposit shall be calculated on the penalty imposed.

The amended provisions apply to appeals filed after 6th August, 2014. As per Section 35F of Central Excise Act, 1944 and Section 129E of Customs Act, 1962 read with CBEC Circular No. 984/8/2014-CX dated 16.09.2014, at present, the quantum of pre-deposit is

(i) 7.5%, if the appeal is filed against the O-in-O passed by the Commissioner and

(ii) 10%, if the appeal is filed against the O-in-A passed by the Commissioner (Appeals).

To know more about the concept of pre-deposit while filing appeal before Commissioner (Appeals) and CESTAT, please refer to e-book on “pre-deposit for filing appeals”.

14. Monetary limits for filing appeals before the Tribunal/ High Courts and the Supreme Court in Customs, Central Excise and Service Tax

14.1 With the aim to reduce the Government litigation, CBEC has decided that in Revenue matters appeal shall not be filed (a) if the amount involved is not very high and is less than the monetary limit fixed by the Revenue authorities, (b) if the matter is covered by a series of judgments of the Tribunal and the High Courts which have held the field and have not been challenged in the Supreme Court, and (c) where the assessee has acted in accordance with the long standing practice and also merely because of change of opinion on the part of the jurisdictional officers.

14.2 To implement the above intention, w.e.f. 20.10.2010, Section 35R has been inserted in the Central Excise Act, 1944 (also made applicable to Service Tax matters by virtue of Section 83 of the Finance Act, 1994) and Section 131BA has been inserted in the Customs Act, 1962.

14.3 The CBEC has issued several Instructions prescribing monetary limits below which appeals shall not be filed before CESTAT/High Court/Supreme Court. As per the instruction issued by CBEC, the following monetary limits below which appeal is not to be filed in the Tribunal, High Court and the Supreme Court, have been prescribed:

| Sr. No. | Appellate Forum | Monetary limit (in Rs.) |

| 1. | CESTAT | 10 Lacs |

| 2. | HIGH COURTS | 15 Lacs |

| 3. | SUPREME COURT | 25 Lacs |

14.4 The above said monetary limits are not applicable in certain types of cases. It has also been provided that adverse judgments relating to the following should be contested irrespective of the amount involved:-

(a) Where the constitutional validity of the provisions of an Act or Rule is under challenge.

(b) Where notification/instruction/order or Circular has been held illegal or ultra vires.

(c) Classification and refunds issues which are of legal and/or recurring nature

14.5 To know more about „Monetary limits for filing appeals before various forums‟, refer to the e-book on the subject matter available in the library of e-books a on the website of the NACEN, Kanpur i.e. www.nacenkanpur.gov.in.

15. Circular No. 935/25/2010-CX dated 21s t September, 2010 regarding streamlining the litigation before the Courts and CESTAT

15.1 To streamline the processing of departmental litigation before the Courts and Tribunal, CBEC has issued Circular No. 935/25/2010-CX, dated 21st September, 2010. Annexure-III of the said Circular relates to improving the quality of Departmental Representation before CESTAT. It has been decided that the following types of cases shall be taken up by the Joint CDRs before the Tribunal as far as possible:

(i) Cases involving revenue of 3 Crores and more in Central Excise, 1 Crore and more in Customs and 50 lakh and more in Service Tax. For this purpose, total revenue, i.e. aggregate of the amount of duty/tax, penalty and interest (wherever quantified in the order), fine etc. will be the criteria.

(ii) All matters before the Larger Benches. However, in such cases, the Jt. CDRs may take the assistance, if necessary, of the SDR/JDR, who represented the Department before the Referral Bench.

(iii) All matters remanded by the Hon‟ble Supreme Court or High Courts.

(iv) All cases involving important question of law, cases having recurring revenue implication and cases having all India ramifications.

(v) Any other case, as may be assigned by the CDR.

15.2 Para 2 of the said Annexure-III relates to the engagement of Special Counsels in cases involving complexities of law / high revenue stake/ having all India ramifications, relevant portion of which reads as under:-

“A panel of retired officers of the department as Special Counsels was constituted in Aug 2006 (further expanded in 2008) to defend the cases of Revenue with their specialized knowledge in respect of cases involving complexities of law / high revenue stake/ cases involving all India ramifications. The Chief Commissioners may assign the cases to them in accordance with the guidelines laid down in this regard. The Commissioners may take stock of cases of the nature as specified above and recommend to the Chief Commissioner concerned for the engagement of the special counsel out of the said panel. The Chief Departmental Representative may also send his recommendations to the Chief Commissioner concerned for engagement of special counsels, if need be. The Chief Departmental Representative will also provide input to the Chief Commissioners in annual performance review of such special counsels.”

15.3 Para 3 of the said Annexure-III lay special emphasis on the need of briefing the departmental representatives/ special counsels by well conversant officers of the Commissionerate in important matters. The relevant portion reads as under:-

“Board further reiterates that well conversant officer(s) should be sent by the Commissioners to brief the Departmental Representative / Special Counsels in important matters for effective presentation of the case before the Tribunal. The Chief Departmental Representative / Joint Chief Departmental Representative have been advised to bring to the notice of the Chief Commissioners concerned, with a copy to Member (L&J), any instance of failure on the part of the Commissioner to send well conversant officer for briefing whenever it was called for…”

15.4 Annexure IV of the said Circular has suggested the action points for dissemination of judgments in revenue‟s favour. The relevant portion of said Annexure-IV reads as under:-

“(a) Every Commissioner will undertake an exercise to sort out important pro-revenue decisions in respect of his jurisdiction and if it is observed that such cases have not been published / uploaded in the ELT/ STR / RLT; send clear, legible and authenticated copy to them for publication in their journals/ website. The letter addressed to these publications along with the enclosures should also be endorsed to the CDR, CESTAT, New Delhi and all the Chief Commissioners for circulation amongst the JCDRs and Commissioners.

(b) Every authorized representative will send to the JCDR in-charge a list of favourable orders received during the month in which he/ she had appeared either individually or in association with other DR or special counsel. At the end of the quarter, the JCDR in-charge will consolidate the reports received from all authorized representatives and get it verified whether all important pro-revenue orders have been reported or not. In the event of any such order(s) not being reported, copy of order(s) will be sent to the publications as mentioned above for favour of publishing the same and to JCDRs of other benches for their internal circulation. A copy of the reference will be sent to the CDR, CESTAT who will pursue the matter with the publications.”

16. For text of relevant Sections and Rules given in Table- 6 below:-

[Refer to the e-Book on filing of Appeal before CESTAT- Part II.]

Table – 6

| Sr. No. | Section /Rules /notification/Circular /Instructions |

Subject |

| A. Customs | ||

| 1. | Section 129 of the CA, 1962 | Provides for constitution of Appellate Tribunal |

| 2. | Section 129 A of CA, 1962 | Provides mechanism for filing appeal against the Order passed by the Principal Commissioner/ Commissioner/ ADG (Adjudication) DRI or Commissioner (Appeals) |

| 3. | Section 129B of CA, 1962 | Provides for the Principles of natural justice to be followed before passing order, lays down timeline for deciding appeals, procedure to be followed for rectification of mistakes etc. |

| 4. | Section 129C of CA, 1962 | Provides various procedures to be followed at CESTAT. |

| B. Central Excise | ||

| 5. | Section 35 B of the CEA Act, 1944 | Provides mechanism for filing appeal against the Order passed by the Principal Commissioner/ Commissioner/ ADG (Adjudication), DGCEI or Commissioner (Appeals) |

| 6. | Section 35C of the CEA, 1944 | Provides for the Principles of natural justice to be followed before passing order, lays down timeline for deciding appeals, procedure to be followed for rectification of mistakes etc. |

| 7. | Section 35D of the CEA, 1944 | Provides various procedures to be followed at CESTAT. |

| C. Service Tax | ||

| 8 | Section 86 of FA, 1994 | Provides for filing of Appeal before CESTAT in Service Tax matters |

| D. Rules | ||

| 9. | Customs, Excise and Service Tax Appellate Tribunal (Procedure) Rules, 1982 | Provide various procedures to be followed at CESTAT |

| 10. | CEGAT (Countervailing duty and anti-dumping duty) Procedure Rules, 1996 | Provide various procedures to be followed at CESTAT in respect of matters related to anti-dumping duty and Counter vailing duty |

| 11. | Central Excise (Appeals) Rules, 2001 | Provide various procedures to be followed at Appellate stages and the Forms in which appeals/ Memorandum of Cross Objections to be filed. |

| 12. | Customs (Appeals) Rules, 1982 | |

| 13. | Rule 9 of Service Tax Rules, 1994 | |

17. For viewing text of Circulars/Instructions/ Orders/ notifications relating to subject matter of filing of appeal before CESTAT as given in Table -7 below:-

[Refer to the e-book on filing of appeal before CESTAT –Part III].

Table -7

|

S. No. |

Circular/Instruction/Office Order / Notification No and date |

Subject |

| 1. | Circular No. 935/25/2010-CX, dated 21.10.2010 | Measures to streamline the processing of departmental litigation before the Courts and Tribunal |

| 2. | Instruction F. No. 390/ Misc./100 /2010-JC, dated 22.09.2011 | Filing of appeal in the wrong forum in matters relating to valuation or determination of rate of duty |

| 3. | Instruction F. No. 390/Review /2/2012-JC, dated 23.11.2012 | Observations regarding effective functioning of Review Committee of Commissioners |

| 4. | Instruction F. No. 275/30/2014-CX.8A, dated 03.04.2014 | Improving the departmental representation in High Court & CESTAT |

| 5. | Instruction F.No.390/Misc. /67/2014-JC, dated 18.12.2015 | Withdrawal of cases pending before HC/CESTAT on the basis of earlier Supreme Court’s decision on the identical matters. |

| 6. | Instruction F. No.390/CESTAT/69/2014-JC, dated 22.12.2015 | Imposition of cost by CESTAT on grounds of quality of adjudication order. |

| 7. | Instruction issued vide the Member (L & J) letter F.No.1080/09/DLA/MISC /15/757, dated 21.12.2015 | Action Plan to Reduce Litigations |

| 8. | Instruction F. No. 390/Misc. /69/2015-JC, dated 15.12.2015 | Authorizing officers of the Zone to Appear before CESTAT Bench. |

| Constitution of the Committee of Principal Chief /Chief Commissioners | ||

| 10. | Office Order No.1/2014, dated 28.08.2014 as amended vide | Constitution of Review Committee of Chief Commissioners/ Commissioners |

| 11. | Office Order No. 2/2014-CE, dated 15.10.2014 | Jurisdictions of Committee of two Chief Commissioners in Central Excise matters |

| 12. | Office Order No. 3/2014-Cus, dated 15.10.2014 read with corrigendum issued vide Office Order 10 dated 12.11.2014 | Jurisdictions of Committee of two Chief Commissioners in Customs matters |

| 13. | Office Order No. 4/2014-ST, dated 15.10.2014 read with corrigendum issued vide Office Order 10 dated 12.11.2014. | Jurisdictions of Committee of two Chief Commissioners in Service Tax matters |

| Constitution of the Committee of Principal Commissioners/Commissioners | ||

| 14. | Office Order No. 5/2014-CE, dated 22.10.2014 read with corrigendum issued vide Office Order 10, dated 12.11.2014 | Jurisdictions of Committee of two Commissioners in Central Excise matters |

| 15. | Office Order No. 6/2014-ST dated 22.10.2014 read with corrigendum issued vide Office Order 10, dated 12.11.2014 | Jurisdictions of Committee of two Commissioners in Service Tax matters |

| 16. | Office Order No. 7/2014-Cus & 8/2014 dated 22.10.2014 read with corrigendum issued vide Office Order 10 dated 12.11.2014 | Jurisdictions of Committee of two Commissioners in Customs matters |

| 17. | Office Order No. 09/2014, dated 29.10.2014 | Powers to Chief Commissioners to assign the charge of a Commissionerate to another Commissioner within his Zone for limited purpose of review. |

| 18. | Office Order No. 14/2015, dated 30.09.2015 | Provides mechanism in cases when the Principal Commissioners as members of the Committees cannot review their own orders passed in the capacity of Pr. Commissioners. |

| 19. | Office Order No. 24/2015, dated 17.12.2015 | Review Committee of Commissioners of Central Excise, Service Tax and Customs: link officer arrangement to also apply for the purpose of Committee of Commissioners for reviewing order passed by Commissioner (appeals) |

| Delegation of powers to the Chief Commissioners/Principal Commissioners for the purpose of review | ||

| 20. | Notification No. 19/2015-Central Excise (N.T.) Dated 18.09.2015 | These notifications invest powers of review in the Principal Commissioners who have been given additional charge of a Chief Commissioner vide Office Order No. 126/2015, dated 20.08.2015 |

| 21. | Notification No. 94/2015-Customs (N.T.) Dated 18.09.2015 | |

| 22. | Notification No. 18/2015-Service Tax Dated 18.09.2015 | |

18.For Forms prescribed for filing appeal and memorandum of cross objections by the Party /Department before CESTA:-

[Refer to e-book on filing of Appeal before CESTAT- Part IV].

| Sr. No. | Form | Purpose | Relevant Rule |

| Under Customs Act, 1992 | |||

| 1. | C.A. 3 | Form for filing appeal before Tribunal by the party. | Rule 6 of the Customs (Appeals) Rules, 1982 |

| 2. | C.A. 4 | Form for filing Memorandum of Cross Objections before Tribunal | Rule 6 of the Customs (Appeals) Rules, 1982 |

| 3. | C.A. 5 | Form for filing appeal before Tribunal by the Department | Rule 7 of Customs (Appeals) Rules, 1982 |

| Under Central Excise Act, 1944 | |||

| 4. | E.A. 3 | Form for filing appeal before Tribunal by the Party. | Rule 6 of Central Excise (Appeals) Rules, 2001 |

| 5. | E.A 4 | Form for filing Memorandum of Cross Objections before Tribunal. | Rule 6 of Central Excise (Appeals) Rules, 2001 |

| 6. | E.A 5 | Form for filing appeal before Tribunal by the Department | Rule 7 of Central Excise (Appeals) Rules, 2001 |

| Under Finance Act, 1994 ( in respect of Service Tax matters) | |||

| 7. | ST.-5 | Form for filing appeals before Tribunal by the party. | Rule 9 of STR, 1994 |

| 8. | S.T.-6 | Form for filing Memorandum of Cross Objections before Tribunal | Rule 9 of STR, 1994 |

| 9. | S.T. 7 | Form for filing appeal before Tribunal by the Department | Rule 9(2) & 9(2A) of the Service Tax Rules, 1994 |

| Important Circulars | |||

| 10. | CBEC Circular No. 969/03/2013-CX, dated 11.04.2013 | ||

| 11. | CBEC Circular No. 991/15/2014-CX, dated 17.12.2014 regarding new alpha numeric codes for various Commissionerates. | ||

19. Important Websites for Reference

(i) Website of Central Board of Excise and Customs [www.cbec.gov.in] for information relating to latest legal provisions, notification, circulars and instructions on matters relating to Customs, Central Excise and Service tax.

(ii) Website of Customs, Excise and Service Tax Tribunal ( www.cestat.gov.in ) for information relating to the working of CESTAT, Text of the CESTAT (Procedure) Rules, 1982, Orders passed by the various benches of CESTAT etc.

Does a caveat lie before CESTAT?