Given the current Geo-Political and Economic Situation prevalent across the Globe, US Sanctions on use of US Dollar for Transactions with Iran & Russia and considering the continuous weakening of the Indian Rupee (INR), and to promote growth of global trade with emphasis on exports from India and to support the increasing interest of global trading community in INR, the Reserve Bank of India (RBI) vide A.P. (DIR Series) Circular No.10, dated 11 July 2022 has allowed International Settlement of Trade in INR for export and / or import of goods and services as an additional arrangement for Invoicing, Payment, and Settlement of Exports / Imports in INR.

International Trade Settlement in Indian Rupees (INR) : A Right Step to Internationalization of the Indian Rupee

> The Settlement in Indian Rupees (INR) is a right step aiming to internationalization of the Indian Rupee and to promote growth of global trade with emphasis on exports from India and to support the increasing interest of global trading community in INR.

> Specially keeping in view of the Restrictions for trade settlements in US Dollar for Transactions with Iran & Russia and to address strained situations like scarcity of Forex Reserves in case of Countries like Sri Lanka, the decision is an important step rightly taken to facilitate trade in INR.

> This would ease India’s hard currency outflow substantially. Reduce the Dependency on US dollar requirements and Strengthen Rupee. This mechanism also may Reduce Cost of Conversion Charges of Exporters and Importers.

> This is an additional arrangement for invoicing payment, and settlement of exports / imports and would co-exist with the current practice of trade settlement in freely convertible foreign exchange (FOREX).

International Trade Settlement – Current Practices

> At present, all export contracts and invoices shall be denominated either in freely convertible currency or Indian rupees but export proceeds shall be realized in freely convertible currency.

> The Practice of Export invoicing in INR is already existing however, the payment must come through Vostro Accounts maintained by foreign banks with a bank in India.

> Trade with Nepal and Bhutan in INR is covered by special arrangements which is existing for a long time.

> Also Asian Clearing Union (ACU) Transactions which shall be denominated in ACU Dollar are existing for promoting regional co-operation and with the objective to facilitate payments among member countries (Bangladesh, Bhutan, India, Iran, Maldives, Myanmar, Nepal, Pakistan and Sri Lanka) for eligible transactions on a multilateral basis, thereby economizing on the use of foreign exchange reserves and transfer costs, as well as promoting trade among the participating countries.

> India had a barter-like mechanism for trade settlement with Iran, wherein Indian oil refiners were paying in Rupees to a local Iranian bank and the funds were used by Iran to pay for imports from India.

Salient Features of RBI Circular

Reserve Bank of India (RBI) issued A.P. (DIR Series) Circular No.10, dated 11 July 2022, under Foreign Exchange Management Act, 1999 (FEMA) .

Some of the Salient Features of the said Circular are :

> All exports and imports under this arrangement may be denominated and invoiced in Rupee (INR).

> Exchange rate between the currencies of the two trading partner countries may be market determined.

> The settlement of trade transactions under this arrangement shall take place in INR.

> An authorized bank would require an approval from the RBI to implement this arrangement.

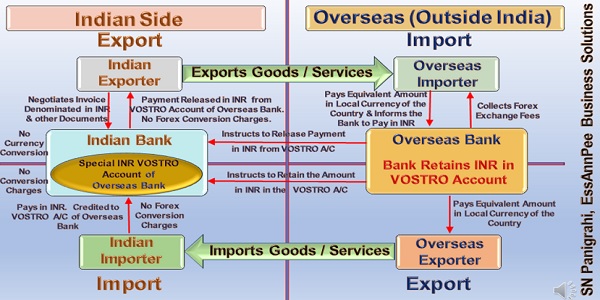

> Indian banks will be permitted to open a Special Vostro Account (SV Account) of the correspondent bank of the trading country.

> Indian importers undertaking imports through this mechanism shall make payment in INR which shall be credited into the Special Vostro account of the correspondent bank of the partner country, against the invoices for the supply of goods or services from the overseas seller / supplier.

> Indian exporters, undertaking exports of goods and services through this mechanism, shall be paid the export proceeds in INR from the balances in the designated Special Vostro account of the correspondent bank of the partner country.

> Payment towards advance for exports from SV Account is, however, subject to the availability of funds, executed export orders / export payments in the pipeline.

> Advance against export may also be received in INR.

> Set-off of export receivables shall also be permitted subject to existing RBI master directions.

Details of how the Scheme Operates can be Viewed @

Amendments Carried out by DGFT in Sync with RBI Circular : Realizations in Indian Rupees – Export Benefits Allowed

♦ DGFT Notified vide Notification No. 33/2015-2020, Dated: 16th September, 2022 by inserting the Para 2.52(d), to permit Invoicing, payment and settlement of exports and imports in INR in sync with RBI’s A.P. (DIR Series) Circular No. 10 dated 11th July, 2022.

♦ Further, DGFT vide Notification No. 43/2015 -2020-DGFT, Dated: 9th November, 2022, made Amendments under FTP, to permit exports benefits / fulfilment of Export Obligations for Invoicing, payment and settlement of exports and imports in INR, as per RBI’s A.P. (DIR Series) Circular No. 10 dated 11th July, 2022. Accordingly amendments in FTP were made in para 46 (Import for export); 2.53 (Export to Iran —Realizations in Indian Rupees to be eligible for FTP benefits / incentives); 3.20 (Status Holder); 4.21 (Currency for Realization of Export Proceeds)

♦ Vide Public Notice No. 35/2015-20-DGFT; Dated 9th November, 2022, Amendment made in Para 5.11 of the HBP, to permit the Invoicing, payment and settlement of exports and imports in INR for Export Proceeds under EPCG Scheme

Export Realizations in Indian Rupees – Export Benefits : RoDTEP & Duty Drawback

RoDTEP Scheme

As per Para 4 of Notification No. 76/2021-Cus(NT) dated September 23, 2021, Duty Credit allowed under the RoDTEP scheme is subject to realization of sales proceeds within the period allowed by the RBI. But no specific mention about realization in any Particular Currency. So Realizations in Indian Rupees is entitled for RoDTEP Benefits.

Duty Drawback

Similarly, Section 75 of the Customs Act, 1962, and the Customs and Central Excise Duties Drawback Rules, 2017, only say that the sales proceeds must be realized, but not mentioned particular currency. So, the entitlements of Drawback will be available against payments received through SVAs also.

Refunds due to Zero-Rated Exports under GST

Rule 96A of GST Rule: Export of Goods or Services under Bond or Letter of Undertaking

Rule 96A (1) (a) for Export of Goods states Exporter to Pay the Tax due along with the interest if the goods are not exported out of India within three months from the date of issue of the invoice for export. Here in this Rule it states only condition of Exporting the Goods Out of India, but Not Stated any Condition of Realization of Export Proceedings.

Rule 96A (1) (b) for Service Exports states Exporter to Pay the Tax due along with the interest if payment of such Services is not received by the exporter in convertible foreign exchange or in Indian rupees, wherever permitted by the Reserve Bank of India. Here in this Rule states Realization either in Convertible Foreign Exchange or in INR as permitted by RBI.

Rule 96B of GST Rule: Recovery of Refund of Unutilized Input Tax Credit or Integrated Tax Paid on Export of Goods where export proceeds not realized.

Rule 96B Refers to sale proceeds in respect of such Export Goods have not been realized, in full or in part, in India within the period allowed under the Foreign Exchange Management Act, 1999 (42 of 1999). This Rule also Not states any thing specific about Realization of Export Proceeds in convertible foreign exchange or in Indian rupees.

Therefore, from the above Rules it is very clear that Export Refunds are allowed even if the Export Proceeds are Received in INR.

Positive Net Foreign Exchange Earnings (NFE)

Certain Mandatory provisions of Achieving Positive Net Foreign Exchange Earnings (NFE) under SEZ Act, 2005 & SEZ Rules, 2006 and also corresponding provisions of FTA in respect of EOU need to be suitably amended for allowing Export Proceeds Received through SVA in INR.

Conclusion

Trade settlement through INR Denominated Special Vostro Account (SV Account) by RBI is a welcome move that would facilitate trade with sanctioned countries like Iran and Russia wherein it has increasingly become difficult to use United States Dollar (US$) or Euro denominated correspondence account for trade settlement.

Rupee Settlement mechanism introduced amid a steadily falling rupee, would help India pay for its imports using rupees instead of U.S. dollars from its foreign exchange reserves. This will to some extent Lessen Draining of Forex and Reduce the Dependency on US dollar requirements and Strengthen Rupee. This mechanism also may Reduce Cost of Conversion Charges for Exporters and Importers.

India has received responses from four to five countries for its mechanism for international trade settlement in rupees, while other nations have also shown interest, according to Deputy Governor of Reserve Bank of India

As per reliable sources, Russia is the only country that has shown interest in the new arrangement for now, and Nine Russian Banks have been permitted to set up Vostro accounts to facilitate rupee-based trade. In 2021-22, India’s exports to Russia stood at $3,254.68 million, while imports from Moscow were valued at $9,869.99 million. If Rupee Settlement mechanism goes well to convert trade with Russia under this route, it can potentially pay for a chunk of its oil and defense imports in INR. This would ease India’s hard currency outflow substantially.

However, it is expected that trade settlement in INR with countries where India has trade surplus will be successful, but settlement with trade deficit countries would be difficult unless a strong line of credit mechanism is also put in place.

Several Asian economies such as Indonesia, the United Arab Emirates (UAE), Sri Lanka, Myanmar, and India are also in discussion with each other to settle trade in their domestic currencies.

Though proper amendments are suitably made in respect of Export Incentives and Refunds, certain other Mandatory provisions of Achieving Positive Net Foreign Exchange Earnings (NFE) under SEZ Act, 2005 & SEZ Rules, 2006 and also corresponding provisions of FTA in respect of EOU need to be suitably amended for allowing Export Proceeds Received through SVA in INR.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author Bio

Dear Sir,

We have been exporting goods to Nepal in INR, will it be considered for EPCG Licence obligation

Thanks. Only Iran is doing it as of now, while UAE is negotiating. Saudi Arabia is the largest trading partner in the Middle East. It would be great if KSA and other Middle Eastern countries come fwd to deal in INR