1. Definitions

A. Financial Instruments

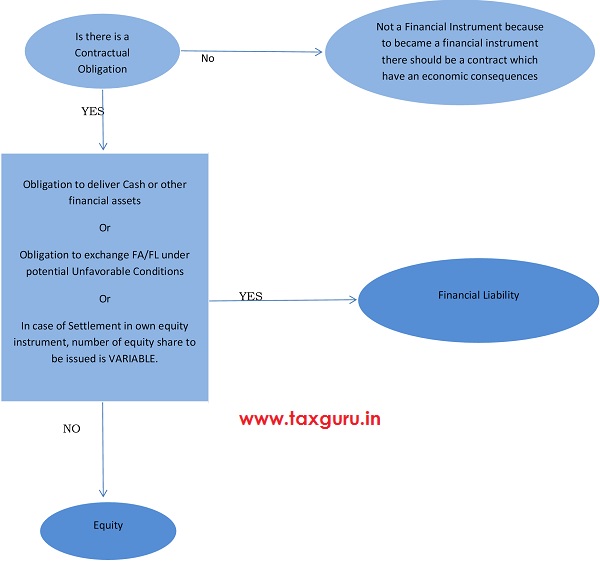

A financial instrument is any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity. Followings do not affect the main characteristic of contract:

-

- May or may be in writing.

- May or may not be enforceable by law.

Contract here simply mean, a contract between two parties that has a clear economic consequences.

Examples: Income tax payable is not a financial liability since it is not imposed by a contract.

Provision and contingencies are also not financial liability since there is no contract.

B. Equity

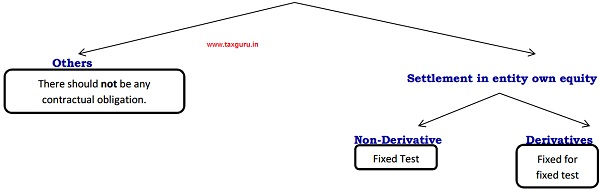

Equity is defined as residual interest after netting off liability from assets. To become equity instrument an instrument should not contain contractual obligations to deliver cash or other FA. In the case of settlement of entity own equity instrument fixed test and fixed for fixed test for non-derivative and derivative instruments respectively is to be passed to classify as equity instrument.

As per INDAS 32.16

To be equity instruments, an instrument should not contain any obligation of neither to deliver cash or other financial assets to another entity nor to exchange financial assets/ financial liability with another entity under potential unfavourable conditions. (Off course if there is an obligation then it is a liability).

In case of settlement by issuing entity own equity instruments.

Case 1- Non derivative

There should be no contractual obligation to deliver variable number of its own equity instruments.

That is if there is contractual obligation for fixed number of share then it is considered as equity.

(Fixed Number of equity share. i.e. only fixed test)

Case 2- Derivative

There should be of fixed amount of cash and for fixed number of equity share. (Fixed Number of equity share+ fixed amount of cash. i.e. fixed for fixed test)

Rights option warrants issued for fixed amount of cash to acquire fixed number of equity share are equity if issued to all existing shareholders of the same class.

The main feature that distinguishes equity from liability is fixed number of equity share for fixed amount of cash.

Example:

Ram buys products from Shyam for Rs.2lacs on 01.01.2019 and amount is to be paid after 3 months i.e. 01.04.2019.

Case-1

Ram agreed to pay amount in cash after 3 months. Since it is clear cut case of contractual obligation, therefore it is a financial liability.

Case-2

Ram agreed to pay amount by issuing his own equity instruments at current market price which is let say Rs.20. In this case, since settlement is made in own equity instruments and is a non-derivative contract and further number of share to be issued is fixed (2,00,000/20=10,000 shares). Hence it is an equity instrument and is to be shown in equity on balance sheet date as on 31.03.2019.

Case-3

Ram agreed to pay amount by issuing his own equity instruments at market price as on 01.04.2019 which is let say Rs.20 on that date. In this case, since settlement is made in own equity instruments and is a non-derivative contract but number of share to be issued is not fixed on 01.01.2019. Hence it is financial liability and is to be shown in liability on balance sheet as on 31.03.2019. It can also be seen from this case that Ram is primarily not issuing equity shares to Shyam but is using equity as currency to pay off debt.

An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities.

C. Financial Liability

A financial liability is any liability that is:

(a) A contractual obligation:

i. To deliver cash or another financial asset to another entity; or

ii. To exchange financial assets or financial liabilities with another entity under conditions that are potentially unfavourable to the entity; (that is derivatives instruments for chances of loss are present) see example below or

(b) A contract that will or may be settled in the entity’s own equity instruments and is:

i. A non-derivative for which the entity is or may be obliged to deliver a variable number of the entity’s own equity instruments; (That is Non Derivative +Variable Number of Share, if share are fixed then it is considered as equity, not liability, known as Fixed test). or

ii. A derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity’s own equity instruments. (That is Derivative +Variable Number of Share, if share are fixed and at fixed price then it is considered as equity, not liability, known as fixed for fixed test).

Followings are equity instruments

- Rights, options or warrants to acquire a fixed number of the entity’s own equity instruments for a fixed amount of any currency are equity instruments(F2F test is passed), if the entity offers the rights, options or warrants pro rata to all of its existing owners of the same class of its own non-derivative equity instruments.

- The equity conversion option embedded in a convertible bond denominated in foreign currency to acquire a fixed number of the entity’s own equity instruments is an equity instrument if the exercise price is fixed in any currency. (F2F test is passed).

Above shall not apply to the followings (Because they are specifically considered as equity on fulfilment of certain given conditions):

- Puttable financial instruments that are classified as equity instruments in accordance with paragraphs 16A and 16B,

- Instruments that impose on the entity an obligation to deliver to another party a pro rata share of the net assets of the entity only on liquidation and are classified as equity instruments in accordance with paragraphs 16C and 16D, or

- Instruments that are contracts for the future receipt or delivery of the entity’s own equity instruments.

Example of potentially unfavourable/ favourable conditions:

Suppose Ram buys call option (c+) on equity share of Altd at exercise price of Rs.1000 and premium paid amounting to Rs.50. Since Ram buys call option he is in a position of gain when the market is bullish in trend (when price rises) and in position of loss when market is bearish in trend (when price falls). Hence in case of bullish it is potentially favourable condition for Ram and in case of bearish it is potentially unfavourable condition for Ram.

Exceptions to the definition of financial liability

As per IndAS 32.19, however there are some limited exception to the above principal of classification of equity and financial liability. In these exception instruments have the characteristics of a financial liability but still it is considered as equity.

Broadly two types of instruments are covered:

- Puttable financial instruments (Eg: units of Mutual Funds)

> A puttable instrument is a financial instrument that gives the holder the right to put the instrument back to the issuer for cash or another financial asset or is automatically put back to the issuer on the occurrence of an uncertain future event or the death or retirement of the instrument holder.

Since it is evident from the definition of puttable financial instruments that it has clear cut characteristics of financial liability because there is an obligation of the issuer to pay off the debt when holder put the instrument back. Now think about mutual funds, the units of mutual funds are payable at NAV whenever holder put units backs to issuer and get the NAV as on that date. In this case there is no equity for mutual fund because all the units are payable as and when they demanded.

- Instruments that impose on an entity an obligation to deliver net assets on liquidations.

Some short term join ventures are formed for a particular duration of project let say 3years, in that case also equity issued to co ventures are subject to payment after 3years. In this case also there is a feature of contractual obligation to pay and this is also a financial liability. Then there is no equity for these short term duration ventures.

Hence to cop-up these loops some exception has been drawn which are discussed below.

But before this let us consider some features of equity shares in general.

1. It entitle holder to get share in net assets of the entity and share in distributable profit only not any other payment.

2. At the time of liquidation and at the time of distribution of profit equity holder stand at last.

3. These are non-redeemable.

This exception applies if all of the following conditions are fulfilled by the instrument (IndAS 32.16A, 16B, 16C and 16D):

1. Instrument entitles the holder to a pro rata share of the entity’s net assets in the event of the entity’s liquidation. In other words, the instrument should not entitle its holder to get any other payment except net assets upon liquidation. (1st feature of equity share)

2. It is in the class of instruments that is subordinate (at last) to all other classes of instruments, that is, in its present form, it has no priority over other claims to the entity’s assets on liquidation (2nd Feature of equity)

3. All financial instruments in the most subordinate class have identical features or contractual obligation as the case may be: For example, the formula or method used to calculate the repurchase or redemption price is the same for all instruments in that(Linked with condition 2).

4. In case of puttable instruments, apart from the contractual obligation for the issuer to repurchase or redeem the instrument for cash or another financial asset, there are no other contractual obligations:

-

- to deliver cash or another financial asset, or

- to settle in variable number of entity’s own equity instruments.

5. In case of puttable instruments, the total expected cash flows attributable to the instrument over the life of the instrument are based substantially on the:

-

- profit or loss,

- change in the recognised net assets or

- change in the fair value of the recognised and unrecognised net assets

- of the entity over the life of the instrument (excluding any effects of the instrument). (i.e only get net assets more or less 1st Feature)

6. The issuer must have no other financial instrument or contract that has:

-

- Total cash flows on same terms as (5) above, with the effect of substantially restricting or fixing the residual return to the puttable instrument holders.

D. Financial Assets

A financial asset is any asset that is:

(a) Cash;

(b) An equity instrument of another entity;

(c) A contractual right:

(i) To receive cash or another financial asset from another entity; or

(ii) To exchange financial assets or financial liabilities with another entity under conditions that are potentially favourable to the entity (that is derivatives instruments for chances of gain are present); or

(d) A contract that will or may be settled in the entity’s own equity instruments and is:

(i) A non-derivative for which the entity is or may be obliged to receive a variable number of the entity’s own equity instruments;(that is Non Derivative +Variable Number of Entity own equity instruments, if it is fixed number of share at fix price then equity and shown as deduction from equity) or

(ii) A derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity’s own equity instruments. (That is Derivative +Variable Number of Entity own equity instruments, if it is fixed number of share at fix price than equity and shown as deduction from equity).

Above shall not apply to the followings (Because they are specifically considered as equity on fullfilment of certain given conditions):

- Puttable financial instruments classified as equity instruments in accordance with paragraphs 16A and 16B.

- Instruments that impose on the entity an obligation to deliver to another party a pro rata share of the net assets of the entity only on liquidation and are classified as equity instruments in accordance with paragraphs 16C and 16D, or

- Instruments that are contracts for the future receipt or delivery of the entity’s own equity instruments.

Disclaimer

Any views or opinions represented above are personal and belong solely to the author and do not represent those of people, institutions or organizations that the author may or may not be associated with in professional or personal capacity, unless explicitly stated. Any views or opinions are not intended to malign any religion, ethnic group, club, organization, company, or individual.

Author Bio

Thank you very much! Your explanation is understandable.

Thanks

I am truly grateful for your detailed explanation, especially with examples. Thank you!

Thanks

Cleared a lot of confusion because of this article. Thanks!