Guidance Note For Forensic Accounting And Investigation Standard No. 140 On Applying Hypotheses are to help the Professional develop and apply the concepts of hypothesis in a manner which are easy to understand, formulated well and executed in a focused manner thereby making the process of evidence gathering more efficient and effective.

Digital Accounting Assurance Board

The Institute of Chartered Accountants of India

1st June, 2023

GUIDANCE NOTE FOR FORENSIC ACCOUNTING AND INVESTIGATION STANDARD NO. 140 ON APPLYING HYPOTHESES

EXPOSURE DRAFT Approved by DAAB (On 1 June’23)

This Guidance Note provides technical clarifications and implementation guidance on how to prepare for and conduct work procedures on Forensic Accounting and Investigation Standard Number 140, on “Applying Hypotheses,” issued by the Institute of Chartered Accountants of India (ICAI) and should be read in conjunction with all the Standards relevant to the topic. The contents of this Guidance Note are recommendatory in nature and do not represent the official position of the ICAI. The reader is advised to apply his best Professional judgement in the application of this Guidance Note considering the relevant context and prevailing circumstances.

1.0 Introduction

1.1 A hypothesis is a provisional, unproven theory, supposition or proposed explanation, based on limited facts, assumptions and observations, the merits of which needs to be established through further examination and study of evidence. Applying hypotheses is a technique that improves the approach and efficiency of undertaking the engagement and achieving its objectives.

1.2 FAIS 140 on “Applying Hypotheses” introduces the concept of hypothesis in a Forensic Accounting and Investigation (FAI) engagement, to make the process of evidence gathering methodical and effective. Hypothesis gives directions to an engagement. Framing hypothesis is a key step in application of forensic methodology since it helps the Professional in developing work procedures to be undertaken.

1.3 Further, similar to gathering evidence to prove the hypothesis, it is equally important that evidence is sought to disprove the hypothesis. Of course, there may be situations where neither is possible (for example where the required evidence is not forthcoming) in which case the hypothesis is considered as not-proved.

1.4 In addition, developing and initiating work procedures through the application of hypotheses provides additional benefits such as:

- Achieves the basic principle of objectivity.

- Allow a balance between professional scepticism and maintaining neutrality.

- Promotes deployment of a focused and intelligent approach.

- Helps deliver an outcome which is reliable and admissible before competent authorities.

2.0 Objectives

2.1 The objectives of the Guidance Note (GN) on Applying Hypotheses are to help the Professional develop and apply the concepts of hypothesis in a manner which are easy to understand, formulated well and executed in a focused manner thereby making the process of evidence gathering more efficient and effective.

2.2 The GN also provides examples and illustrations to help the Professional apply the Hypotheses concepts in a seamless and effective manner all through the engagement.

3.0 Procedures

3.1 Forming a hypothesis is an iterative process, which continues till a hypothesis is found that explains the case under consideration. Also, based on the evidence gathered and changing dynamics of the case, hypotheses can be redrafted or updated.

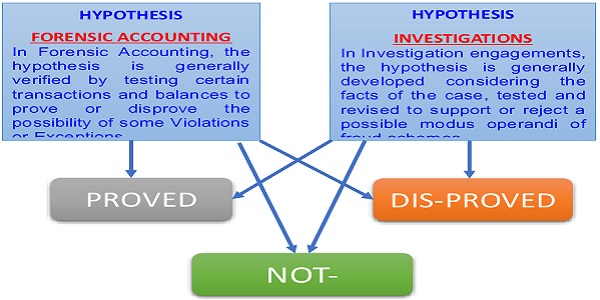

3.2 The Standard also requires testing the evidence gathered on various objective parameters and drawing logical and reliable conclusions for proving, disproving or not proving. The same can be better understood from the following infographic:

3.3 The Hypotheses approach is also sometimes called the case theory approach to solving Forensic and Investigations cases. As an example, to better understand the basic concept of Hypothesis, take the following situation where there are allegations of kick-back to get a government contract. Two scenarios can be considered in which the first does not apply the Hypotheses approach and the second does:

Scenario 1: Professional A starts to review the contract file and based on the information obtained, starts to interview all the staff members who were involved with bidding for the government contract. Included in this list of staff is also the suspect who denies everything. The Professional gathers a lot of information but is not clear what can be used as evidence, and what may not be relevant. Not much success.

Scenario 2: Professional B makes a list of possible theories. If allegation is true, some unusual trail must have been left behind, such as:

- someone in the organisation made contacts with someone in the government under unusual circumstances or odd hours.

- some unusual terms or conditions were amended to accommodate the organisation.

- some exchanges of favours were made to some Government official.

Some, or all of these, theories (or Hypotheses) could be proved or disproved, but in checking these, some relevant evidence would be found to help reach a conclusion.

So, Scenario 2 with Hypotheses, would provide Professional B with a methodical approach to conduct the work procedures and prevent wastage of resources. In addition, as the work procedures progress, the theories may get modified (dropped, added or changed) and thereby minimise chances of digression from the core investigation.

3.4 The final modus operandi emerges only when multiple hypotheses are formulated and tested. Although the hypotheses may or may not be referred to in the Report, the quality of the evidence gathered as a result of application of hypotheses, makes the outcome more reliable.

3.5 A hypothesis is generally formed once an understanding of the background of the case is obtained, which would include the following (indicative list):

- The engagement terms and objectives.

- Nature of allegations or suspected violations.

- Availability of key documents and information.

- Involvement of certain individuals.

- Complexity of systems and processes.

3.6 After obtaining the preliminary understanding as described above, the Professional develops hypotheses and begin testing these through work procedures. A generic suggestive practical approach to forming a hypothesis is given as under:

(a) What might have happened? – Noting down possible modus operandi in terms of the actions and transactions which could have taken place and developing further hypotheses around the same.

(b) Who might be involved? – Listing all those individuals who have a role to play in the process, using the authority matrix, hierarchy and organisation structure as a basis to identify the staff and officials. Conducting public domain searches and open-source intelligence to identify any close connects of these individuals.

(c) Why might the allegations be true? – Link the concepts of pressure, opportunity and rationalisation to the extent possible and understand possible reasons for the actions.

(d) What are the possible concealment methods? – Identify vulnerabilities through a review of previous cases and reports. At this point trail of events, including digital trail, is an important consideration.

(e) When did it take place? – Prepare a timeline of events in chronological form, link it with the involvement of individuals and their presence or absence from the place of action, list out exceptional situations.

(f) How is the fraud being perpetrated? – List down various possibilities on how the suspected modus operandi could have been undertaken based on academic understanding and practical experience.

(g) Determine from where (the sources) the evidence could be gathered:

- On-book vs Off-book – That is, whether it would be identified from review of books of accounts, documentation review and transaction testing or more from applying techniques of interviewing, external inquiries, visits and intelligence.

- Internal vs External to the organisation – That is, whether it would be identified from review of internal records or third-party records and similarly engaging into discussions with internal individuals or external parties linked to the matter.

3.7 The above steps or methodology may be followed keeping in mind the principle of objectivity, i.e., the need for the Professional to avoid the trap of getting focussed too early on a particular path. The Professional avoids the temptation of targeting any particular individual or department while formulating the hypotheses, or getting influenced by certain sub-conscious biases.

3.8 The Professional is aware of the existence of some of biases which may cloud the approach during the engagement, such as:

(a) Authority bias – These are situations where a certain level of extra confidence is given to individuals of higher authority. Authority bias happens if greater weightage is extended to these individuals who hold positions of higher authority over others, despite there being information to the contrary.

(b) Confirmation bias – Situations where existing beliefs are given more emphasis or value over information which contradicts those beliefs. For example, review of data that supports hypothesis and seek evidence that match viewpoints, as well as reject any other information that defies assumptions and beliefs.

(c) Selective Perception – This is the tendency to see a particular situation or issue from a pre-chosen perspective. This is particularly related to team-based behaviour.

(d) Availability Bias – This relates to situations when focus is placed on immediate information or situations that come to our mind. The result is that belief on the information or experience is placed that is recalled or demonstrative or explicative of a situation or scenario. This comes at the expense of looking for additional information that could lead to a further understanding of the situation.

3.9 The above biases are indicative in nature and not exhaustive. Therefore, every engagement has to be treated on its own merit due to its unique circumstances and hypotheses would need to be formulated, modified and tested objectively.

3.10 Fraud indicators (red flags) identified, may also be used to formulate a hypothesis. This is quite relevant so as to ensure that the work procedures are focused on the important matters The Professional should refer to FAIS 120 on “Fraud Risk”.

4.0 Explanations with Examples

4.1 A set of examples, given below, is used to clarify the concepts of Hypotheses and the manner in which they can be applied to different scenarios.

4.2 Example 1: Concerning bank borrowings and NPA account.

4.2.1 Background of the case: A borrower’s account at a particular bank has turned into a Non-Performing Account (NPA) from which the borrower had availed credit facilities. The bank has now appointed the Professional with a mandate to check if there are any irregularities with regard to misrepresentation or manipulation in the books of accounts, or any diversion or siphoning of funds.

4.2.2 Hypotheses: Based on the understanding of the case and the basic review of the documentation and preliminary financial analysis following hypotheses may be formulated for checking:

(a) Promoters and Directors could have potentially mis-utilised the funds for personal purposes or other purposes than those for which funds were granted.

(b) Covenants in the loan agreement could have been violated, such as diverting the inflow of funds to other accounts rather than the specified escrow account.

(c) There could be errors or irregularities in the documentation submitted to avail the loans or during the submissions made for regular monitoring of the account.

(d) Transactions with related or connected parties could have been undertaken to misstate the performance and financial position to avail further finance.

(e) Fictitious purchases could have been booked against which funds would have been disbursed, however, the same could have been received back by the promoters.

4.2.3 Application of the concept of hypotheses and work procedures:

(a) Review of the loan documentation i.e., agreement copies, and negative covenants, along with the details and data submitted to avail the funds.

(b) Review other Bank Account Statements of the borrower to understand the inflow and outflow of funds and modus operandi with regard to avoiding the inflow of funds in the escrow account.

(c) Analysis of commercial sense in the transactions with the related parties along with transaction testing and documentation review for physical movement of goods and realisation of funds.

(d) Analytical work procedures involving data analytics on purchase transactions.

4.2.4 Status: Evidence was gathered and hypothesis had following outcome:

(a) Letter of Credit facility was exploited for inter-group companies and related parties in order to book fictitious sales in the books of accounts of one entity while increasing the purchase in another, hence

(b) Review of the documentation submitted during the continuous monitoring of the account suggested that everything was in line with the actual position and affairs of the borrower, hence

(c) Other bank account statements were not available, hence hypothesis not proved.

4.3 Example 2: Concerning authenticity of Trade Receivables.

4.3.1 Background of the case: Management has appointed the Professional to undertake forensic accounting work procedures in the Trade Receivables area since the entity has multi-location profit centres with common customers, to check if there are any non-existing trade receivables.

4.3.2 Hypotheses: Based on the understanding of the case and the basic review of the documentation and preliminary financial analysis following hypotheses may be formulated for checking:

(a) Collusion between representatives of sales and marketing department along with finance department.

(b) Sales target might not have been met, resulting in loss of performance incentive and thus pressure to indulge in such irregularity.

(c) Any such non-existent trade receivables might have been entered into the system around the same time frame as the appraisal cycle.

4.3.3 Application of the concept of hypotheses and work procedures:

(a) Call for balance confirmations.

(b) Perform data analysis and tests of Abnormal Duplications (e.g., the SSS/SSD “same-same-same”, “same-same-different” tests on the customer master.

(c) Review the documentation for material movement.

(d) Perform detailed ledger scrutiny to analyse the year-on-year movement, during the year movement, identify any trend, etc.

(e) Conduct site visits of the trade receivable account holders to check the actual existence.

(f) Perform public domain checks – to understand the business in which they operate, market repute, reviews and financial strength.

(g) Verify the names of payees as per the books of accounts and cross-check with the names reflected in the Bank Statements and the narrations therein. The same could have apparent mis-matches if any misrepresentation has been done in the books of accounts.

4.3.4 Status: Evidence was gathered and hypothesis had following outcome:

(a) Multiple customer masters were created around the same time with a trend in the suffixes used for such customer names, however, there was no web-based presence of business of such customers, hence proved.

(b) Sales target was met well in time and there were enough sales orders in place, thus that hypothesis disproved.

(c) There was not enough evidence to establish connection or collusion between the sales, marketing and finance department, hence not proved.

4.4 Example 3: Concerning existence of Assets to support the Investments.

4.4.1 Background of the case: Engagement pertains to potential irregularities at a company, with significant investments in fixed assets, property, plant, and equipment as the major components of the balance sheet which could be inflated in value.

4.4.2 Hypotheses: Based on the understanding of the case and the basic review of the documentation and preliminary financial analysis following hypotheses may be formulated for checking:

(a) Fixed Assets additions could only be on paper and physically might not be in existence, done to compensate for the inflated sales numbers so that the tax credit can be created in the books of accounts.

(b) Management might have offloaded their share of investment in the company or they would be planning to raise additional funds.

(c) Overall market is in a declining phase which has impacted sales and thereby investors have raised concerns, resulting in a decline in the share price.

(d) There has been a delay in repayment of certain credit facilities that were maturing, this depicts a potential liquidity crunch, so there is a contradiction with the additions in investments.

4.4.3 Application of the concept of hypotheses and work procedures:

(a) Check for any abnormality between the nature of business vs. amount of investment vs. type of fixed asset.

(b) Existence records of the fixed assets, including title deeds, contracts, deeds, tax records, delivery and physical verification reports.

(c) Compare the amount of investment compared with revenue from operations of those assets for the past few years.

(d) Operating margin vis-à-vis overall investment in fixed assets.

(e) Any principal reduction or sale of fixed assets.

(f) Amount of term loans and other borrowings made against the fixed assets.

(g) Any revaluation of the fixed assets.

(h) Details of parties from whom the fixed assets are purchased.

(i) Details of impairment testing done for the fixed assets etc.

4.4.4 Status: Evidence was gathered and hypothesis had following outcome:

(a) Lack of meaningful income from the assets was noted, hence proved.

(b) Management has not offloaded their share on the company, thus hypothesis disproved.

(c) Primary evidence to support the existence and ownership of the assets was not possible, hence not proved.