International Financial Services Centres Authority (IFSCA) has released a consultation paper and draft circular proposing a regulatory framework for transition bonds. This move responds to global climate commitments under the Paris Agreement, which demand significant emissions reductions across sectors, including high-emitting, hard-to-abate industries like steel, cement, and aviation. These industries face difficulty accessing green finance despite being crucial for meeting global net zero goals. Transition finance, including transition bonds, aims to bridge this gap by supporting gradual emissions reductions through investments in cleaner technologies and processes.

Despite growing interest in ESG-labelled instruments, transition bonds currently make up less than 1% of the ESG debt market. Challenges include a lack of standard definitions and regulatory clarity. The proposed IFSCA framework includes definitions of eligible activities aligned with global and Indian taxonomies, mandatory credible transition plans, external reviews, and detailed initial and annual disclosure requirements. These disclosures cover transition strategies, emissions targets, use of proceeds, governance, and progress reports.

The initiative seeks to enhance transparency, credibility, and investor confidence while enabling access to finance for industries in the process of decarbonization. It builds on recommendations from an Expert Committee and aligns with frameworks such as those from ICMA, OECD, and the Climate Bonds Initiative.

Stakeholders are invited to submit comments on the draft by April 29, 2025. The final framework will be issued under the IFSCA (Listing) Regulations, 2024. The proposal also reinforces IFSCA’s broader objective of developing GIFT-IFSC into a climate finance hub by supporting inclusive climate transition financing strategies, particularly in developing countries.

*********

INTERNATIONAL FINANCIAL

SERVICES CENTRES AUTHOURITY

CONSULTATION PAPER ON “FRAMEWORK FOR TRANSITION BONDS”

A. Context and Background

1. The Paris Agreement, of which India is a signatory, aims to limit global temperature rise to well below 2°C above pre-industrial levels, with efforts to keep it within 1.5°C. The achievement of this goal requires substantial reductions in GHG emissions across all sectors. The international discussions at COP26 (Glasgow) and COP27 (Sharm el-Sheikh) have also emphasized the need for financial flows to align with long-term decarbonization objectives.

2. As on April 02, 2025, 142 countries, covering 78% of global Gross Domestic Product (GDP) and 76% of global GHG emissions, have adopted net zero targets and around 1173 of the largest 2000 publicly traded companies now have net zero targets1. While these commitments are a positive step, the implementation of these targets will be the real challenge.

3. Globally, around USD 75 trillion of climate investment is needed to achieve the net zero target2. At current estimates, India alone will need to mobilize over $10 trillion in investments to achieve its net zero commitments and meet its climate goals3. Development of green financial markets will be key in ensuring these targets are met and contribute meaningfully to the global effort to limit climate change.

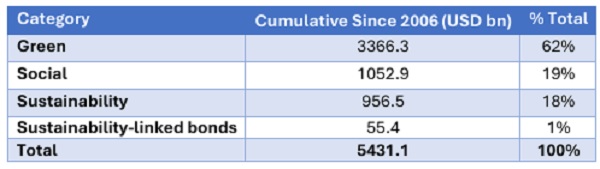

4. In recent years, ESG labelled debt securities (Green, Social, Sustainability and Sustainability-linked) have seen substantial growth, with many government and corporate entities engaging with investors to finance debt while making a net positive environmental or social impact. As on Q3 2024, cumulative listing of ESG labelled debt securities stood at USD 5.4 Tn4.

5. While ESG labelled debt securities have played a key role in mobilizing climate finance, it is generally seen that their application is often limited to sectors/projects that are at near/net zero. For instance, 75% of the green debt volume is directed primarily towards energy, buildings, and transport5. Industries such as steel, cement, heavy duty transport, aviation, and shipping etc., which contribute approximately 40% of global greenhouse gas (GHG) emissions6 and are categorized as ‘hard-to-abate’, face difficulties in accessing finance despite their commitments to long-term decarbonization. Thus, achieving global net zero emissions is not possible without the decarbonization of these sectors.

6. This is where transition finance steps in. Transition finance provides a structured pathway for such industries to reduce their emissions progressively by enabling investments in cleaner technologies, processes and alternative fuels. Instruments such as transition bonds and transition loans can help mobilize capital towards these efforts while ensuring alignment with emission reduction goals.

7. The issuance of Transition Bonds has remained modest with cumulative global Transition Bonds issuance from 2019 to 2023 at $15.26 billion7, accounting for less than 1% of the total ESG-labelled debt market. However, given that hard-to-abate sectors are essential for achieving global net zero targets, significantly scaling up transition finance is critical to driving meaningful decarbonization in these industries.

8. While Transition Bonds hold significant potential, their growth has been slow. Amongst others, lack of clear definitions and standards, insufficient regulatory guidance, and concerns over credibility and transparency have been the key reasons affecting the issuance of such instruments.

9. Instruments such as Transition Bonds hold significant potential in mobilizing capital for decarbonization, particularly in high-emitting industries in developing countries such as India and hence require immediate attention to address the challenges. Thus, it is felt that similar to regulatory framework for Green, Social, Sustainability and Sustainability-linked bonds, a regulatory framework for Transition Bonds would not only assist issuers from hard-to-abate sectors to raise capital but shall also bring credibility amongst investors by ensuring adequate disclosures, independent external review, etc. to mitigate the risk of greenwashing.

B. Definition of Transition

10. Transition finance is a concept that has been defined by multiple international organizations as a financial means to support the shift from high-carbon to low-carbon or net zero economies. Below is a summary of how various organizations defining transition finance:

International Capital Markets Association (ICMA) defines transition finance as “investments that effectively address climate-related risks and contribute to alignment with the goals of the Paris Agreement “.

Organisation for Economic Cooperation and Development (OECD) defined it as a financing approach that “focuses on the dynamic process of becoming sustainable, rather than providing a point-in-time assessment of what is already sustainable, to provide solutions for a whole-of economy decarbonisation”.

G20 Sustainable Finance Working Group (SFWG) report defines transition finance as “financial services supporting the whole-of-economy transition, in the context of the Sustainable Development Goals (SDGs), towards lower and net-zero emissions and climate resilience, in a way aligned with the goals of the Paris Agreement”.

Asian Development Bank (ADB) defines “Transition finance as a concept where financial services are provided to high carbon-emitting industries – such as coal-fired power generation, steel, cement, chemical, papermaking, aviation and construction – to fund the transition to decarbonization.”

According to Climate Bond Initiative (CBI), the ‘Transition label’ can be used for eligible investments that are making a substantial contribution to halving global emissions levels by 2030 and reaching net zero by 2050 but will not have a long- term role to play i.e. beyond 2050 and activities that will have a long term role to play, but at present the long term pathway to net zero goals is not certain.

11. As can be seen from the above, there is no universally accepted or globally aligned definition of “Transition Finance”. However, there are certain national taxonomies that attempt to define “transition”. Given IFSCA’s mandate to develop GIFT-IFSC as a climate finance hub, it is essential to define “Transition” that not only inspires confidence amongst global investors but also considers the socio-economic realities of India and other such developing countries.

12. Despite the variations in definitions, key themes emerge consistently across different frameworks. Transition finance is broadly recognized as a financing approach designed to support the shift from high-carbon to low-carbon or net zero emissions economies, particularly targeting industries and activities that are not yet sustainable but are committed to becoming so. This approach emphasizes the dynamic process of decarbonization, aligning with the Paris Agreement’s goals of limiting global warming ideally to 1.5°C and, at the very least, to well below 2°C. The following key themes emerge across definitions:

i. Alignment with Paris Agreement: Transition finance is fundamentally anchored in the objectives of the Paris Agreement, which aims to limit global warming to 1.5°C above pre-industrial levels or, at a minimum, well below 2°C. This underscores that financing activities must contribute to these global climate goals, ensuring that transition finance serves as a tool to support international efforts to mitigate climate change.

ii. Scope: It targets high-emitting industries or sectors to drive sectoral transitions and contribute to broader economic decarbonization. These sectors are often characterized by a lack of immediate low-carbon alternatives, making them pivotal yet challenging areas for climate action. Transition finance addresses this by employing tailored strategies, including interim solutions like energy efficiency improvements or carbon capture technologies, to support their gradual shift toward net zero emissions.

iii. Transition Plan: Transition finance differs from green finance by supporting entities and activities in the process of becoming sustainable, facilitating a dynamic journey toward decarbonization. To ensure this process is genuine, transition finance requires credible transition plans, backed by clear timelines, targets, and strategies, along with measurable progress to demonstrate tangible environmental impact. This accountability prevents greenwashing, where claims of sustainability might otherwise lack substance, ensuring that financed transitions are transparent, verifiable, and aligned with long-term climate objectives.

C. Expert Committee on Transition Finance

13. IFSCA had set up the Expert Committee on Transition Finance with the following Terms of Reference related to Transition Finance:

i. To recommend a regulatory framework for transition finance instruments.

ii. To advise IFSCA on the approach to developing a reliable and cost-effective ecosystem for transition finance meeting needs of the Indian industry.

14. The Committee broadly provided its recommendations on three parameters:

i. Scope of definition

ii. Policy and Regulation

iii. Financial Mechanism and Financial instruments

The report of the committee can be accessed at https://shorturl.at/Kr81h

D. Framework for Transition Bonds

15. Based on the recommendations of the expert committee, approaches adopted by the various jurisdictions/institutions, and further examination by the IFSCA, a draft circular on the “Framework for Transition Bonds” has been prepared and is proposed to be issued under the Regulation 75(1) and 130(1) of the IFSCA (Listing) Regulations, 2024. The proposed framework provides for:

i. Eligible activities

ii. Trajectory

iii. Independent external reviewer

iv. Disclosures

E. Public Comments

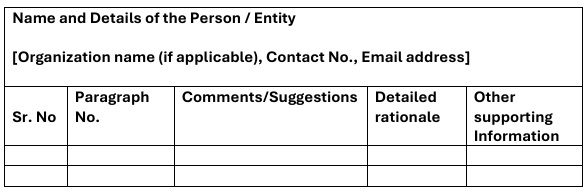

16. Comments and suggestions from the public and stakeholders are invited on the draft “Framework for Transition Bonds” placed at Annex-1.

17. Comments on the draft circular may be sent by email to Mr. Chintan Panchal, Manager, IFSCA at chintan.panchal@ifsca.gov.in and Mr. Karan, Consultant, IFSCA at karan.1@govcontractor.in with a copy to Mr. Pavan Kishor Shah, General Manager, IFSCA at pavan.shah@ifsca.gov.in latest by April 29, 2025.

18. The comments may be provided in the following format (MS Word or MS Excel only):

Annex-1

DRAFT CIRCULAR

F. No. IFSCA-DSF0SFHB/2/2025-Capital Markets April XX, 2025

To,

Recognised stock exchanges in the International Financial Services Centres (IFSCs)

Issuers who propose to list ESG labelled debt securities in the IFSCs

Dear Sir / Madam,

Subject: Framework for Transition Bonds

1. International Financial Services Centres Authority (IFSCA) recognizes the pivotal role of ESG labelled debt securities (Green Bonds, Social Bonds, Sustainability Bonds, Sustainability-linked Bonds) in financing sustainable development and transition to a low-carbon economy. In line with this, a regulatory framework for Green, Social, Sustainable and Sustainability-linked Bonds was brought in by IFSCA as part of its Listing Regulations. Presently, through this framework, the GIFT-IFSC has also witnessed listing of around USD 15.43 Bn ESG labelled debt securities, accounting for 24% of the total USD 64.44 Bn listed as of February 2025.

2. Globally, the sustainable debt market has grown to USD 5.4 Tn as of September 20248. However, capital mobilization for climate action remains concentrated in certain sectors. Notably, 75% of green debt issuance is directed toward energy, buildings, and transport9, while hard-to-abate sectors responsible for 40% of global greenhouse gas (GHG) emissions struggle to access financing. These sectors inter-alia cover steel, cement, heavy duty transport, aviation, and shipping, whose decarbonization is essential for achieving global net zero emissions. While green finance has been instrumental in supporting sectors such as renewable energy, energy-efficient buildings, and clean transport, its scope is often limited to projects that generate immediate or near-term carbon reductions. Thus, hard-to-abate sectors that require a phased transition face challenges in securing finance, despite their commitment to long-term decarbonization.

3. Transition Finance is emerging as a critical enabler to bridge this gap, providing an attractive mechanism for hard-to-abate sectors to raise funds for their brown-to-green transformation.

4. Based on the recommendations of the Expert Committee on Transition Finance set up by the IFSCA, further analysis of the global development on the subject, and keeping in mind the needs of developing countries such as India, the IFSCA hereby specifies the “Framework for Transition Bonds” as under:

Eligible Activities

5. The activities classified as “Transition” under any of the following taxonomies/technology roadmap, shall be eligible to issue and list transition bonds on the stock exchanges in IFSC:

i. ASEAN Taxonomy for Sustainable Finance

ii. Climate Bonds Taxonomy

iii. EU taxonomy for Sustainable Activities

iv. Singapore-Asia Taxonomy for Sustainable Finance

v. Japan (Technology Roadmap for Transition Finance)

vi. Taxonomy(ies) specified by Government of India

vii. Any other taxonomy recognised by IFSCA

Transition Plan

6. An issuer shall have a credible transition plan at the entity level and the said transition plan shall be aligned with Paris Agreement goal to limit global temperature rise to well below 2°C above pre-industrial levels, with efforts to keep it within 1.5°C.

Independent external reviewer

7. The issuer shall appoint independent external reviewer(s) to ascertain that the proposed issuance is in:

a. alignment with the IFSCA ‘Framework for Transition Bonds’

b. provide an assessment of whether the proposed Transition Plan is aligned with the science-based trajectories or relevant regional, sector, or international climate change scenarios

8. The appointment of external reviewer shall be in compliance with the conditions as mentioned in the Regulations 76(3) of IFSCA (Listing) Regulations, 2024.

9. The independent external reviewer(s) may take one or more of the following forms recommended by the International Capital Market Association:

(a) Second Party Opinion;

(b) Verification;

(c) Certification;

(d) Scoring / Rating

The issuer shall ensure that the details regarding the independent external reviewer(s) are adequately disclosed and easily accessible to the investors.

Disclosures

Initial Disclosures

10. The issuer needs to make initial disclosures as per the Regulations 70 and 77 (1) of IFSCA (Listing) Regulations, 2024.

11. The issuer shall make the following additional disclosures in the offer document or information memorandum, as the case may be, in respect of Transition labelled debt securities.

A. Transition Plan & Governance Disclosures

i. Disclosure on an issuer’s transition plan or climate transition strategy. The strategy should address all the relevant material aspect of issuer’s business.

ii. Disclosures on short, medium, and long-term GHG emission reduction targets, which are quantitatively measurable, aligned with the latest available methodology and the Paris Agreement along with baseline year.

ii. Disclosures on governance mechanisms that provides clear oversight of an issuer’s climate transition strategy, including management/board level accountability.

iv. Disclosure on broader sustainability strategy to mitigate relevant environmental and social externalities.

B. Business model environmental materiality

i. Disclosure on the materiality of climate-related eligible projects and the overall emissions profile of an issuer.

C. Climate transition strategy to be ‘science-based’

i. Disclosures on scenario utilised and methodology applied (e.g., ACT, SBTi, IEA etc.). When third-party trajectories are not available, provide disclosure on the industry peer comparison and/or internal methodologies/historical performance.

D. Implementation transparency

i. Disclosures on CapEx roll-out plan consistent with the overall transition strategy and how it communicates CapEx decision-making within the organisation.

ii. Disclosures on phase-out plan regarding activities/products incompatible with the climate transition strategy.

iii. Disclosure on a qualitative and/or quantitative assessment of the potential locked-in GHG emission from an issuer’s key assets and products.

Annual Disclosures

12. The issuer shall make disclosures as per the Regulations 78 (1) of IFSCA (Listing) Regulations, 2024.

13. The issuer shall provide the following additional disclosures to the recognized stock exchange(s) until full utilization of the proceeds, in respect of “Transition” labelled debt securities.

A. Transition Plan & Governance Disclosures

i. Report progress against climate transition strategy, which inter-alia covers:

a) Annual GHG emissions reduction

b) Progress on committed GHG emission reduction targets

c) % CapEx allocated to GHG emission reduction projects vs total CapEx

B. Business model environmental materiality

i. Where Scope 3 emissions are expected to be material but are not yet identified or measured, a timeline for reporting should be disclosed.

C. Climate transition strategy to be ‘science-based’

ii. Report progress focused on any emissions reduction benchmarking orvalidation.

iii. Disclosure on the use of carbon capture technology as well as of high-quality and high-integrity carbon credits and their relative contribution to the GHG emissions reduction trajectory in line with best industry practices (e.g., SBTi, VCMI and ICVCM).

D. Implementation transparency

i. Update and action as against disclosures made initially in reference to the requirements specified at paragraph 11(D).

14. In reference to the disclosure requirements, issuers may consider referring to ICMA’s Climate Transition Finance Handbook10 for further guidance.

15. The circular is issued in exercise of the powers conferred by Section 12 and 13 of the International Financial Services Centres Authority Act, 2019, read with regulations 75(1) and 130(1) of the IFSCA (Listing) Regulations, 2024.

A copy of this Circular is available on the website of the International Financial Services Centres Authority (IFSCA) at www.ifsca.gov.in.

Yours faithfully,

Pavan Shah

General Manager

Division of Sustainable Finance

Capital Markets Department

Email: pavan.shah@ifsca.gov.in

Tel: +91-79-61809844

Notes:

1 https://zerotracker.net/

2 https://www.goldmansachs.com/insights/articles/reaching-net-zero-is-forecast-to-require-nearly-75-trillion-of-investment

3 https://www.ceew.in/press-releases/india-will-require-investments-worth-over-usd-10-trillion-achieve-net-zero-2070-ceew

4 https://www.climatebonds.net/files/reports/cbi mr q3 2024 01c.pdf

5https://www.climatebonds.net/market/data/#use-of-proceeds-charts

6 https://www.weforum.org/stories/2024/12/net-zero-hard-to-abate-sectors-decarbonization/

7 https://zerocarbon-analytics.org/archives/economics/reforming-climate-finance-asia-leads-in-transition-finance

8 https://www.climatebonds.net/files/reports/cbimrq3202401c.pdf

9 https://www.climatebonds.net/market/data/#use-of-proceeds-charts

10 https://www.icmagroup.org/assets/documents/Sustainable-finance/2023-updates/Climate-Transition-Finance-Handbook-CTFH-June-2023-220623v2.pdf