Case Law Details

Vardhman Acrylics Limited Vs Commissioner of Customs (Imports) (CESTAT Mumbai)

The appeals were filed by the appellant against the Commissioner (Appeals)’ order dated 28.06.2019, which upheld the denial of interest on the delayed refund of Extra Duty Deposit (EDD) collected during provisional assessment of imports made from a related foreign supplier. The imports, made between October 1997 and April 1998, were provisionally assessed because the valuation of related-party transactions was under examination by the Special Valuation Branch (SVB). The appellant executed provisional duty bonds and deposited EDD ranging from 1% to 5% of the declared assessable value in accordance with CBEC instructions.

The SVB, by Order-in-Original dated 26.10.1998, held that the relationship between the importer and the overseas supplier had not influenced the transaction value and accepted the declared invoice value. It directed that all pending provisional assessments be finalized accordingly and that the EDD be refunded wherever applicable. Based on this order, the appellant filed refund applications on 22.01.1999. However, the department challenged the SVB order, leading to prolonged litigation before the Commissioner (Appeals), the Tribunal, and the Bombay High Court. Ultimately, the departmental challenge failed, and the provisional assessments were finalized in 2008. Although the refund amounts were sanctioned, they were credited to the Consumer Welfare Fund on the ground of unjust enrichment, resulting in further rounds of litigation.

The issue of unjust enrichment was repeatedly examined. After several remands by the Tribunal, it was finally held that the incidence of the EDD had not been passed on to any other person. Consequently, the Assistant Commissioners sanctioned refunds of ₹96,42,224 and ₹74,23,079 in November 2015. However, no interest was granted on these refunds. The appellant challenged the denial of interest, but both the original authority and the Commissioner (Appeals) rejected the claim, leading to the present appeals before the Tribunal.

The Tribunal identified three issues for determination: whether there was delay in sanctioning the refund, whether interest under Section 27A of the Customs Act was payable, and the period for which such interest, if payable, should be calculated. It examined the provisions of Sections 14, 17, 18, 27 and 27A of the Customs Act, the Customs (Provisional Duty Assessment) Regulations, 1963, and the Customs Refund Application (Form) Regulations, 1995, along with CBEC circulars governing provisional assessments and SVB investigations.

The Tribunal distinguished EDD from customs duty. It observed that EDD is not defined as “duty” under the Customs Act but is a deposit collected during SVB investigations to ensure timely submission of information by importers while provisional assessments remain pending. Although its amount is calculated as a percentage of the declared value, EDD remains a deposit and not customs duty. It may be adjusted only if additional duty becomes payable after final assessment; otherwise, it is refundable. The Tribunal held that, in the present case, since the declared transaction value was accepted and no additional duty became payable, the EDD was clearly refundable.

The Tribunal further held that the refund claim could become effective only after final assessment of the Bills of Entry. While the appellant had submitted refund applications in January 1999, the effective orders determining the refundable amount arose only when the provisional assessments were finalized through Orders-in-Original dated 26.03.2008 and 22.05.2008. Accordingly, the statutory period under Section 27A for payment of interest had to be reckoned from the expiry of three months after these refund-determining orders and continue until the actual payment of the refund.

The Tribunal observed that the department had no authority to keep the refund application pending indefinitely merely because the underlying order was under challenge. It noted that the Customs Act provides for scrutiny and disposal of refund applications but does not permit indefinite pendency. It also referred to CBEC instructions emphasizing that provisional assessments should ordinarily be finalized within six months and that refund claims should be processed expeditiously to avoid interest liability.

The Tribunal relied on several judicial precedents concerning EDD refunds and delayed payment of interest. It referred to decisions holding that EDD is a deposit rather than customs duty and that such deposits become refundable upon completion of provisional assessment. It also relied on decisions directing payment of interest where refunds of EDD were delayed beyond the statutory period. At the same time, it noted that the Supreme Court’s decision in Mafatlal Industries Ltd. dealt with refund of duty and not EDD, and therefore did not directly govern the present dispute.

The Tribunal concluded that once the provisional assessments were finalized in 2008 and the department determined that no adjustment of EDD was required, the refund ought to have been paid within the statutory period. Since the refund was actually sanctioned only in November 2015, the delay attracted liability to pay interest under Section 27A of the Customs Act. The Tribunal held that interest was payable on the delayed refund from the expiry of three months after the Orders-in-Original dated 26.03.2008 and 22.05.2008 until the date of actual refund. Accordingly, the denial of interest by the lower authorities was not sustainable.

FULL TEXT OF THE CESTAT MUMBAI ORDER

These appeals have been filed by M/s Vardhman Acrylics Limited, Mumbai (herein after, referred to as “the appellants”, for short) assailing Order-in-Appeal No. MUM-CUS-RN-IMP-55&56/2019-20 dated 28.06.2019 (herein after, referred to as “impugned order” for short) passed by the Commissioner of Customs (Appeals), Mumbai Zone-I.

2.1. Briefly stated, the facts of the case are that the appellants herein inter alia, are engaged in the manufacture of acrylic fibre, acrylic tow for which they had imported various equipment, from their overseas supplier M/s Marubeni Corporation, Japan in accordance with the terms and conditions of an Equipment Supply Contract. For the purpose of such import of equipment, the appellants have filed seven Bills of Entry (B/Es) during 17.10.1997 to 24.04.1998 with the Customs appraising group VA and two B/Es on 28.11.1997 and 09.01.1998 before EPCG appraising group in the Commissionerate of Customs, New Custom House, Mumbai. Since the imports were from related party, the assessments were carried out by the customs authorities provisionally pending determination of influence of relationship on the declared assessable value in respect of import of goods supplied by foreign supplier to the appellants, under Customs Valuation (Determination of Price of Imported goods) Rules, 1988 [herein after, referred to as, “CVR of 1988”, for short] read with Section 14 of the Customs Act, 1962. The goods were allowed clearance on provisional assessment basis by the customs authorities on execution of provisional duty bond along with security/bank guarantee and upon payment of 1% to 5% of declared assessable value as Extra Duty Deposit (EDD) by the appellants in terms of Circular No.1/1998 dated 01.01.1998 and the earlier instructions issued by the Central Board of Excise & Customs (CBEC), New Delhi.

2.2 Accordingly the import transactions under various B/Es, as above at Mumbai, besides import transactions at other ports were handled centrally to the Special Valuation Branch (SVB), GATT Valuation Cell, Mumbai for detailed examination of the valuation aspects of such imports. Upon detailed examination of records, contracts, joint venture agreement, documents submitted by the appellants, the Assistant Commissioner of Customs, GATT valuation cell, Mumbai by issue of Order-in-Original No. S/9-50 GATT/97GVC dated 26.10.1998 have held that the relationship has no influence on the pricing between the appellants-importer and the related party supplier; and the transaction value and invoices raised for import of goods were accepted. Therefore, it was held by the original authority in the said order dated 26.10.1998, read with corrigendum dated 17.11.1998, that the declared invoice value for the imported goods as submitted in the B/Es by the appellants shall be accepted under Rule 4(3)(a) of CVR, 1998. Further it was also held that all pending provisionally assessed B/Es of the appellants importer shall be finalised accordingly and the Revenue deposit/EDD may be refunded subject to applicability. It was also mentioned in the said order that this decision will remain in force till present method of invoicing remains unchanged or for a period of three years from the date of such order, for a final review after such period.

2.3 On the basis of aforesaid order-in-original dated 26.10.1998, the appellants importer had filed two separate refund applications both dated 22.01.1999 before the Assistant Commissioner of Customs, Appraising Group VA and EPCG Appraising Group, New Custom House, Mumbai for Rs. 96,42,224/- and Rs.74,23,079/-, respectively. In the meantime, Revenue had filed an appeal before the Commissioner of Customs (Appeals) challenging the order of the original authority dated 26.10.1998 in accepting the transaction value in SVB valuation. The Commissioner of Customs (Appeals) vide Order-in-Appeal No.01/2001-MCH dated 02.01.2001 rejected the departmental appeal on the ground that the technical know-how fees had nothing to do with the manufacture or sale of the imported goods supplied to the appellants and provision of Rule 9(b)(iv) of CVR, 1998 were not invokable in the present case. In the appeal filed by the department against such order of the Commissioner (Appeals) before the Tribunal, by an order dated 23.01.2002, the appeal was dismissed, on the ground that the Review order in this case was passed after lapse of the prescribed period of one year under Section 129D of the Customs Act, 1962, and hence such review order was treated as non-est. Considering that the department had not sanctioned refund of EDD, the appellants had approached before the Hon’ble High Court of Bombay in Writ Petition No.1149/2003. In the judgement dated 07.09.2004, by referring to the Customs Reference No.1 of 2004, the Hon’ble High Court of Bombay allowed the WP to be withdrawn by the appellants-importer and Revenue was permitted to withdraw the amount deposited/EDD by appellants, pursuant to the order of this Court along with accrued interest. Further, the appeal was restored to the file of the Tribunal for fresh hearing and decision on merits of the case. In the Order No. A/465/WZB/06-C.III(CSTB) dated 08.06.2006 passed by the Tribunal, by upholding the order dated 02.01.2001 passed by the Commissioner (Appeal), the Tribunal had rejected the appeal filed by Revenue. Since the refund of EDD was not sanctioned by the department, the appellants having got a favourable order in the first round of litigation, had again approached the Hon’ble High Court of Bombay in Writ Petition No. 2592 of 2007. In the judgement dated 20.12.2007, based on the statement made by the Counsel appearing for Revenue that the refund application is in process and after giving hearing to the petitioners order will be passed within three weeks on the petitioners furnishing the information as called for by them, the petition was disposed of. Accordingly, the provisionally assessed B/Es were finalised on 20.02.2008 and the Assistant Commissioner of Customs, Appraising Group-VA vide Order-in-Original (O-in-O) dated 26.03.2008, had sanctioned the refund of Rs. Rs. 96,42,224/- and similarly the Assistant Commissioner of Customs, Appraising Group-EOCG vide Order-in-Original dated 22.05.2008, had sanctioned the refund Rs.74,23,079/-, but both of them in their respective O-in-O have ordered for crediting the same to Consumer Welfare Fund for the reason that the appellants had taken depreciation benefit on such imported plant and machinery, the claim amount has not been shown separately as break-up figures in the ‘Balances/Deposits with Government Authorities; in the books of account, and thereby the appellants had passed on the benefit to the consumer indirectly.

2.4 In the appeal filed against the order of original authority dated 26.03.2008 & 22.05.2008, before the Commissioner (Appeals) the matter was under litigation for a number of times/iteration. In the order dated 31.12.2008, the Commissioner (Appeals) held that the unjust enrichment angle was not applicable and in the appeal before the Tribunal, such order of the Commissioner (Appeals) was set aside and the matter was remanded back to him. In the order dated 14.01.2010, the Commissioner (Appeals) held that the appellants had not successfully crossed the bar of unjust enrichment. In the appeal of the appellants filed before the Tribunal, vide Order dated 20.02.2013, the order dated 14.01.2010 of the Commissioner (Appeals) was set aside and the matter was again remanded back to him. Once again vide Order-in-Appeal dated 28.06.2013, the Commissioner (Appeals) held that the appellants had not successfully crossed the bar of unjust enrichment and rejected the appeal filed by the appellants. In further appeal filed by the appellants, the Tribunal vide Order No. A/641642/15/ CB dated 07.01.2015 had held that the incidence of revenue deposit has not been passed on to any other person and thus remanded the matter back to the original authority for deciding on the refund claim. This was also followed by another Order No. M/2635/L5/CB dated 18.05.2015 for rectifying the mistake in mentioning of two amounts of refund claim arising from 7 B/Es and 2 B/Es. In pursuance of this order of the Tribunal, the Assistant Commissioner of Customs, Gr.VA, NCH, Mumbai vide order-in-original dated 13.11.2015 had sanctioned the refund claim for an amount of Rs.96,42,224/- in favour of the appellants. Similarly, the Assistant Commissioner of Customs, EPCG Group, NCH, Mumbai vide order-in-original dated 06.11.2015 had sanctioned the refund claim for an amount of Rs.74,23,079/- in favour of the appellants. However, no interest was paid on such refund claims sanctioned to the appellants. In the appeal preferred by the appellants against the orders of the original authority dated 13.11.2015 & 06.11.2015, the Commissioner of Customs (Appeals) vide orders dated 28.09.2017 & 27.09.2017, respectively, remanded the matter back to the original authority for deciding the issue of interest payable on refund.

2.5 In deciding the matter of interest payable on sanction of refund vide Orders-in-Original dated 07.02.2018 (issued on 28.02.2018) and dated 14.02.2018 (issued on 28.02.2018), the Assistant Commissioners of Customs Appraising Groups VA & EPCG have held that no interest is payable on refund amount sanctioned vide order dated 13.11.2015 & 06.11.2015 and rejected the claim of interest. In the appeal preferred against the said orders of the original authority before the Commissioner (Appeals) vide the common impugned order dated 28.06.2019, he had rejected the appeals filed by the appellants and upheld the orders of the original authority. Feeling aggrieved with the impugned order, the appellants have preferred these appeals before the Tribunal.

3. We heard both sides and have considered the submissions advanced by the learned Advocate appearing for the appellants and the learned Authorized Representative of the Department. We have also carefully perused the records of the case and the additional written submissions given in the form of paper books along with relied upon case laws on both sides.

4. In the impugned order dated 28.06.2019, the facts of the case have been brought out in detail and the same has also been captured in the preceding paragraphs 2.1 to 2.5 of this order. We find that the issues arising for consideration before us from this appeal is to determine the following:

(i) In the case of sanction of refund of Extra Duty Deposit (EDD) of Rs.96,42,224/- vide Order-in-Original No. 1218/AC/Gr.V/15-16 dated 13.11.2015 and Rs.74,23,079/- vide Order-in-Original No. 670/AC/EPCG/15-16 dated 06.11.2015, whether there is any delay in sanction of refund to the appellants or not?

(ii) if there is a delay, then whether interest under Section 27A of the Customs Act, 1962 is payable to the appellants or not;

(iii) if any interest is payable on account of delay in the above refund, then for what period such interest under Section 27A ibid, is payable?

The period of dispute in the present case is from October, 1997 to April, 1998, as the nine B/Es covered under the present dispute were filed under Section 46 ibid during the period 17.10.1997 to 24.04.1998.

5.1 In order to address the issues under consideration before this Tribunal, we would like to refer the relevant legal provisions contained in the Customs Act, 1962 and the rules/regulations made thereunder as it existed during relevant point of time of the dispute and the relevant facts evidenced through various orders, documents dealing with the issue, for coming to a proper conclusion about the subject issues of determination referred above.

Customs Act, 1962

“Definitions.

Section 2.—

In this Act, unless the context otherwise requires,—

(2) “assessment” includes provisional assessment, re-assessment and any order of assessment in which the duty assessed is nil;

(15) “duty” means a duty of customs leviable under this Act;

(24) “value”, in relation to any goods, means the value thereof determined in accordance with the provisions of sub-section (1) or sub-section (2) of Section 14;

Valuation of goods for purposes of assessment.

Section 14.—(1) For the purposes of the Customs Tariff Act, 1975 (51 of 1975) or any other law for the time being in force whereunder a duty of customs is chargeable on any goods by reference to their value, the value of such goods shall be deemed to be the price at which such or like goods are ordinarily sold, or offered for sale, for delivery at the time and place of importation or exportation, as the case may be, in the course of international trade, where—

(a) the seller and the buyer have no interest in the business of each other; or

(b) one of them has no interest in the business of the other, and the price is the sole consideration for the sale or offer for sale :

Provided that such price shall be calculated with reference to the rate of exchange as in force on the date on which a bill of entry is presented under section 46, or a shipping bill or bill of export, as the case may be, is presented under section 50.

(1A) Subject to the provisions of sub-section (1), the price referred to in that sub-section in respect of imported goods shall be determined in accordance with the rules made in this behalf…..

Assessment of duty.

Section 17.—

(1) After an importer has entered any imported goods under section 46 or an exporter has entered any export goods under section 50 the imported goods or the export goods, as the case may be, or such part thereof as may be necessary may, without undue delay, be examined and tested by the proper officer.

(2) After such examination and testing, the duty, if any, leviable on such goods shall, save as otherwise provided in section 85, be assessed.

(3) For the purpose of assessing duty under sub-section (2), the proper officer may require the importer, exporter or any other person to produce any contract, broker’s note, policy of insurance, catalogue or other document whereby the duty leviable on the imported goods or export goods, as the case may be, can be ascertained, and to furnish any information required for such ascertainment which it is in his power to produce or furnish, and thereupon the importer, exporter or such other person shall produce such document and furnish such information.

(4) Notwithstanding anything contained in this section, imported goods or export goods may, prior to the examination or testing thereof, be permitted by the proper officer to be assessed to duty on the basis of the statements made in the entry relating thereto and the documents produced and the information furnished under sub-section (3); but if it is found subsequently on examination or testing of the goods or otherwise that any statement in such entry or document or any information so furnished is not true in respect of any matter relevant to the assessment, the goods may, without prejudice to any other action which may be taken under this Act, be reassessed to duty.

(5) Where any assessment done under sub-section (2) is contrary to the claim of the importer or exporter regarding valuation of goods, classification, exemption or concessions of duty availed consequent to any notification therefor under this Act, and in cases other than those where the importer or the exporter, as the case may be, confirms his acceptance of the said assessment in writing, the proper officer shall pass a speaking order within fifteen days from the date of assessment of the bill of entry or the shipping bill, as the case may be.”

Provisional assessment of duty

Section 18.

(1) Notwithstanding anything contained in this Act but without prejudice to the provisions contained in section 46—

(a) where the proper officer is satisfied that an importer or exporter is unable to produce any document or furnish any information necessary for the assessment of duty on the imported goods or the export goods, as the case may be ; or

(b) where the proper officer deems it necessary to subject any imported goods or export goods to any chemical or other test for the purpose of assessment of duty thereon ; or

(c) where the importer or the exporter has produced all the necessary documents and furnished full information for the assessment of duty but the proper officer deems it necessary to make further enquiry for assessing the duty,

the proper officer may direct that the duty leviable on such goods may, pending the production of such documents or furnishing of such information or completion of such test or enquiry, be assessed provisionally if the importer or the exporter, as the case may be, furnishes such security as the proper officer deems fit for the payment of the deficiency, if any, between the duty finally assessed and the duty provisionally assessed….”

Claim for refund of duty.

Section 27.

(1) Any person claiming refund of any duty and interest, if any, paid on such duty—

(i) paid by him in pursuance of an order of assessment ; or

(ii) borne by him,

may make an application for refund of such duty and interest, if any, paid on such duty to the Assistant Commissioner of Customs or Deputy Commissioner of Customs—

(a) in the case of any import made by any individual for his personal use or by Government or by any educational, research or charitable institution or hospital, before the expiry of one year ;

(b) in any other case, before the expiry of six months,

from the date of payment of duty and interest, if any, paid on such duty, in such form and manner as may be specified in the regulations made in this behalf and the application shall be accompanied by such documentary or other evidence (including the documents referred to in section 28C) as the applicant may furnish to establish that the amount of duty and interest, if any, paid on such duty in relation to which such refund is claimed was collected from, or paid by, him and the incidence of such duty and interest, if any, paid on such duty had not been passed on by him to any other person :

Provided that where an application for refund has been made before the commencement of the Central Excises and Customs Laws (Amendment) Act, 1991, such application shall be deemed to have been made under this sub-section and the same shall be dealt with in accordance with the provisions of sub-section (2):

Provided further that the limitation of one year or six months, as the case may be, shall not apply where any duty and interest, if any, paid on such duty has been paid under protest :

Provided also that in the case of goods which are exempt from payment of duty by a special order issued under sub-section (2) of section 25, the limitation of one year or six months, as the case may be, shall be computed from the date of issue of such order:

Provided also that where the duty becomes refundable as a consequence of judgment, decree, order or direction of the appellate authority, Appellate Tribunal or any court, the limitation of one year or six months, as the case may be, shall be computed from the date of such judgment, decree, order or direction.

Explanation I.—For the purposes of this sub-section, “the date of payment of duty and interest, if any, paid on such duty”, in relation to a person, other than the importer, shall be construed as “the date of purchase of goods” by such person.

Explanation II.—Where any duty is paid provisionally under section 18, the limitation of one year or six months, as the case may be, shall be computed from the date of adjustment of duty after the final assessment thereof.

(2) If, on receipt of any such application, the Assistant Commissioner of Customs or Deputy Commissioner of Customs is satisfied that the whole or any part of the duty and interest, if any, paid on such duty paid by the applicant is refundable, he may make an order accordingly and the amount so determined shall be credited to the Fund :

Provided that the amount of duty and interest, if any, paid on such duty as determined by the Assistant Commissioner of Customs or Deputy Commissioner of Customs] under the foregoing provisions of this subsection shall, instead of being credited to the Fund, be paid to the applicant, if such amount is relatable to—

(a) the duty and interest, if any, paid on such duty paid by the importer or the exporter, as the case may be, if he had not passed on the incidence of such duty and interest, if any, paid on such duty to any other person;

(b) the duty and interest, if any, paid on such duty on imports made by an individual for his personal use;

(c) the duty and interest, if any, paid on such duty borne by the buyer, if he had not passed on the incidence of such duty and interest, if any, paid on such duty to any other person;

(d) the export duty as specified in section 26;

(e) drawback of duty payable under sections 74 and 75;

(f) the duty and interest, if any, paid on such duty] borne by any other such class of applicants as the Central Government may, by notification in the Official Gazette, specify;….

Interest on delayed refunds.

Section 27A. If any duty ordered to be refunded under sub-section (2) of section 27 to an applicant is not refunded within three months from the date of receipt of application under sub-section (1) of that section, there shall be paid to that applicant interest at such rate, not below ten 1[five] per cent and not exceeding thirty per cent per annum as is for the time being fixed by the Board 2[by the Central Government, by notification in the Official Gazette,] on such duty from the date immediately after the expiry of three months from the date of receipt of such application till the date of refund of such duty :…”

Customs (Provisional Duty Assessment) Regulations, 1963

Notification No. 181-Cus., dated 13th July, 1963.

“In exercise of the powers conferred by section 157 of the Customs Act, 1962 (52 of 1962), read with section 18 of the said Act, the Central Board of Revenue makes the following regulations, namely:

1. Short title.-

These regulations may be called the Customs (Provisional Duty Assessment) Regulations, 1963.

2. Conditions for allowing provisional assessment.-

Where the proper officer on account of any of the grounds specified in subsection (1) of section 18 of the Customs Act, 1962 (52 of 1962), is not able to make a final assessment of the duty on the imported goods or the export goods, as the case may be, he shall make an estimate of the duty that is most likely to be levied hereinafter referred to as the provisional duty. If the importer or the exporter, as the case may be, executes a bond in an amount equal to the difference between the duty that may be finally assessed and the provisional duty and deposits with the proper officer such sum not exceeding twenty per cent of the provisional duty, as the proper officer may direct, the proper officer may assess the duty on the goods provisionally at an amount equal to the provisional duty.

3. Terms of the bond.-

(a) Where provisional assessment is allowed pending the production of any document or furnishing of any information by the importer or the exporter, as the case may be, the terms of the bond shall be that such document shall be produced or such information shall be furnished within one month or within such extended period as the proper officer may allow, and the person executing the bond shall pay the deficiency, if any, between the duty finally assessed and the duty provisionally assessed.

(b) Where provisional assessment is allowed pending the completion of any test or enquiry, the terms of the bond shall be that the person executing the bond shall pay the deficiency, if any, between the duty finally assessed and the duty provisionally assessed.

4. Surety or security of the bond.- The proper officer may require that the bond to be executed under these regulations may be with such surety or security, or both, as he deems fit.”

Customs Refund Application (Form) Regulations, 1995

M.F. (D.R.) Notification No. 34/95-Cus. (N.T.), dated 26-5-1995.

“In exercise of the powers conferred by sub-section (1) of section 157 , read with clause (aa) of sub-section (2) of the said section of the Customs Act, 1962 (52 of 1962), hereinafter referred to as the Act, and in supersession of the Customs Application (Form) Regulations, 1991, except as respect things done or omitted to be done before such supersession, the Central Board of Excise and Customs hereby makes the following regulations, namely :-

Regulation 1. Short title and commencement. – (1) These regulations may be called the Customs Refund Application (Form) Regulations, 1995. (2) They shall come into force with effect from the date of their publication in the Official Gazette.

Regulation 2. Form and manner of filing application for refund. – (1) An application for refund shall be made in the prescribed Form appended to these regulations in duplicate to the 1 [Assistant Commissioner of Customs or Deputy Commissioner of Customs], having jurisdiction over the Customs port, Customs airport, land customs station or the warehouse where the duty of customs was paid.

(2) The application shall be scrutinised for its completeness by the Proper Officer and if the application is found to be complete in all respects, the applicant shall be issued an acknowledgement by the Proper Officer in the prescribed Form appended to these regulations within ten working days of the receipt of the application.

(3) Where on scrutiny, however, the application is found to be incomplete, the Proper Officer shall, within ten working days of its receipt, return the application to the applicant, pointing out the deficiencies. The applicant may resubmit the application after making good the deficiencies, for scrutiny.

Explanation . – For the purposes of payment of interest under section 27A of the Act, the application shall be deemed to have been received on the date on which a complete application, as acknowledged by the Proper Officer, has been made.”

5.2 At the outset, it is also made clear that in the above appeals the disputed period pertains to pre-introduction of ‘self-assessment’ concept under the definition clause of ‘assessment’ in Section 2(2) ibid as well as in the legal provisions contained in Section 17 ibid relating to ‘Assessment of duty’. Therefore, assessments under Sections 17 and 18 ibid were mandated to be performed by the proper officer of customs under the customs statute.

6.1 According to Section 14 of the Customs Act, 1962, and the erstwhile CVR of 1988 and now the Customs Valuation (Determination of Value of Imported Goods) Rules, 2007, the assessable Value should be the “Transaction Value”, i.e., the price actually paid or payable after adjustment by various factors influencing valuation and subject to (a) compliance with the valuation conditions and (b) satisfaction of the Customs authorities with the truth and accuracy of the declared value. In terms of Section 14 ibid, import transactions involving buyer and seller, where they are related to each other, commonly referred to as ‘related party transactions’, the valuation aspect of such imports are examined by Special Valuation Branches (SVB) located, at that relevant time, in the major Custom Houses at Mumbai, Calcutta, Chennai and Delhi. In such cases, the goods are first assessed provisionally, and the importer is required to fill-up a questionnaire and furnish a list of documents so that finalisation of provisional assessments is expedited.

6.2 For making provisional assessment, the proper officer of customs is required to estimate the duty to be levied i.e., the provisional duty and the duty that may be finally assessed or re-assessed. Thereafter, the importer or the exporter has to execute a bond in an amount equal to the difference between the duty that may be finally assessed or re-assessed and the provisional duty. He shall also deposit with the proper officer such sum not exceeding twenty per cent of the provisional duty, as the proper officer may direct. The terms of the bond include the following undertakings to be given by the importer/exporter viz., (i) The importer or exporter shall pay the deficiency, if any, between the duty finally assessed or re-assessed, as the case may be, and the duty provisionally assessed. (ii) Where provisional assessment is allowed pending the production of any document or furnishing of any information, the importer / exporter shall produce the same within one month or within such extended period as the proper officer may allow. In terms of extant CBEC instructions, the provisional assessments must be finalized expeditiously, well within 6 months. However, in cases involving machinery contracts or large project imports, where imports take place over long period, such finalization may take more time. Here too, CBEC directs the customs field formations that efforts should be made to finalize the cases within 6 months of the date of import of the last consignment covered by the contract. [Refer CBEC Instructions F.No.512/5/72-Cus.VI, dated 23-4-1973 and F.No.511/7/77-Cus.VI, dated 9-I-1978 and Circular No. 17/2011-Cus., dated 8-4-2011].

6.3 In terms of the CBEC’s instructions vide F.No.512/5/72-Cus.VI dated 23.04.1973 and F.No.511/7/77-Cus.VI. dated 09.01.1978, the provisional assessments must be finalized expeditiously, well within 6 months. Thus, it could be inferred that even though there is no specific time limit prescribed in the Regulations of 1963/2011, either for submission of documents by the importer or for finalizing the provisional assessment by the proper officer of customs, the endeavour of the department is to obtain finalization of provisionally assessed duties at the earliest as may be possible under the Customs statute. This also becomes clear from the subsequent Customs (Provisional Duty Assessment) Regulations, 2011, introduced with effect from 25.11.2001, where it is specifically provided that in case of provisional assessment which is pending the production of any document or furnishing of any information by the importer or the exporter, the bond referred to in regulation shall inter alia, contain an undertaking that he shall produce such document or information within one month or within such extended period as the proper officer may allow.

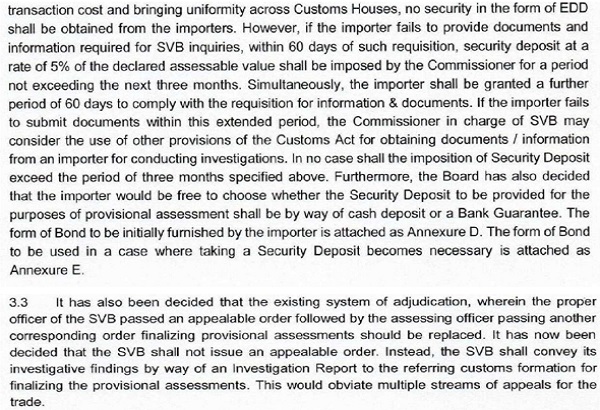

7. From careful examination of the legal provisions of the Customs Act, 1962 particularly Sections 2(2), 2(15), 18, the phrase “duty” has been used therein and has also been defined to mean duty of customs leviable under the Customs Act, 1962. However, the phrase “Extra Duty Deposit” has not been either defined or mentioned in any of the provisions of the Customs Act, 1962. In the regulations made in exercise of the powers vested with the Board/CBEC under Section 157 ibid, for carrying the purposes of the Customs Act, 1962, there is mention of the term “deposit” in determining the sum, not exceeding twenty per cent of the provisional duty, to be paid by the importer, besides execution of bond and security at the time of provisional assessment. The relevant regulations relevant for the period of dispute is Customs (Provisional Duty Assessment) Regulations, 1963. In the Circular No.01/1998-Customs dated 01.01.1998 issued for prescribing the instructions in handling the cases by SVB, such “Extra Duty Deposit (EDD)” to be obtained is specified at the rate of 1% and in certain situations, enhancement of such deposit to 5% has also been mentioned. The relevant extract of the said instructions in the said Circular dated 01.01.1998 is given below:

“The existing instructions and the procedure observed in the various Custom Houses in regard to cases taken up by the Special Valuation Branch of the Custom Houses have been reviewed by the Board in the context of several representations received from the trade and industry about inordinate delays in the finalisation of cases involving related personal transactions, payment of royalty and licence fees, technical collaboration agreements between the seller and buyer and also the financial burden on account of the requirement of the extra duty deposit etc.

2. On the basis of this review, the Board has taken the following decisions :

xxx xxx xxx xxx

8. The amount of extra duty deposit presently kept at 5% of the value of the goods should henceforth be reduced to 1% of the value.

9. Furthermore, where provisional assessment is being resorted to, the investigation and finalisation of the assessment should be completed within three months of the registration of the case in the SVB of the designated Custom House. If no decision is given within 4 months of the registration of the case, the obtaining of the extra duty deposit should be discontinued. The time- frame for finalisation of investigation should be strictly adhered to irrespective of whether the importer has furnished all the required information or not.

10. As regards the cases pending with the SVB of various Custom Houses pending as on 30-4-1997, steps should be taken to complete the investigation and have the issues finally settled by 28th February, 1998. All the concerned Chief Commissioners and Commissioners are requested to put in extra efforts by way of re-deploying officers to achieve this target. As for cases registered from 1-6-1991 to 31-12-1997, all the pending cases should be completed by 30-4-1998.

11. In view of the tight time-frame laid down for finalisation of SVB cases in para 9 above, the Commissioners of Customs should institute special monitoring arrangements and review periodically each pending cases and taken suitable steps to arrive at a decision. The Commissioners are wholly responsible for adhering to the prescribed time-frame.”

8.1 Further, for appreciation of the disputed issue over the past 25 years, we have also seen the subsequent instructions issued for the procedure prescribed for investigation of related party transactions in import cases under SVB. The Central Board of Excise & Customs (CBEC) had issued one another circular No.5/2016-Customs dated 09.02.2016, where the procedure of obtaining EDD in case of provisional assessments have been elaborately explained. Even though this circular has been issued subsequent to the disputed period, for understanding the nature of EDD and its implication in refund of the same, for the purpose of the appreciation of issues under dispute, it would be useful to refer the same. The relevant paragraphs of the said circular has been extracted and given below:

Circular No. 5 /2016 -Customs

F.No. 465/12/2010-Cus V

Government of India

Ministry of Finance

Department of Revenue

Central Board of Excise & Customs

******

New Delhi. the 9th February 2016

To,

All Principal Chief Commissioners Customs

All Principal Chief Commissioner of Customs & Central Excise

All Chief Commissioners of Customs,

All Chief Commissioners of Customs & Central Excise,

All Directorate-Generals. Chief Departmental Representative,

All Principal Commissioners of Customs,

All Principal Commissioners of Customs & Central Excise

All Commissioners of Customs

All Commissioners of Customs & Central & Excise

Sub: Procedure for investigation of related party import cases and other cases by the Special Valuation Branches – reg.

The ‘Special Valuation Branch’ (hereinafter referred to as “SV13–) was created as an institution specializing in investigation of transactions involving special relationships between buyer – seller or those involving other special circumstances surrounding the sale of imported goods, both of which have a bearing on the assessable value. Detailed instructions were issued vide Circular Nos. 1/98 – Customs dated 1.1.98 and 11/2001-Customs dated 23.2.2001, prescribing the procedure to be observed by the Custom Houses for referring cases to Special Valuation Branches and time lines to be followed for finalising such cases.

2. However. trade and industry has been repeatedly representing regarding delays in finalisation of SVB investigations, continued uncertainty due to provisional assessments. increase in transaction costs due to extra duty deposits and burdensome procedure of renewal of SVB orders. Board has also taken cognizance of the WCO’s Guide to Customs Valuation and Transfer Pricing (June 2015) and the fact that the circulars 1/98 and 11/2001 were based upon the Customs Valuation (Determination of Price of imported goods), Rules, 1988. which have since been superseded by the Customs Valuation (Determination of Value of Imported Goods) Rules. 2007. Accordingly, after considering the above and the large number of SVB investigations pending in various Customs Houses, a need has been felt to streamline the procedures relating to investigations by SVBs.

xxx xxx xxx xxx

3.2 The Board has reviewed the practice relating to levy of ‘Extra Duty Deposits’ (EDD) in cases where SVB investigations are undertaken. It has been taken into consideration that ‘Extra Duty Deposit’ @ 1% of declared assessable value is being obtained from the importer for a period of 4 months during which time he is required to submit required documents and information to the SVB. In the event of his failing to do so, the EDD can be increased to 5% till such time the importer complies. Upon the importer complying with the requisition for documents and information, Circular 11/2001 – Cus dated 23.2.2001 provides that EDD shall be discontinued. while imports will continue to be assessed provisionally till the completion of investigations. In other words, the imports were continued to be assessed provisionally on the basis of a PD Bond but without any EDD. It has also been noted that many importers have represented on delays in dispensing of EDD, even though they have provided the required information and a period of 4 months has passed without the case having been decided. Therefore, the Board has decided that while reference to SVB requires the assessments to be provisional, for the sake of reducing

8.2 On careful perusal of the above along with statutory provisions of Customs Act, 1962, it clearly transpires that the term “duty” refers to the duties of customs leviable under Section 14 of the Customs Act, 1962 read with the Customs Tariff Act, 1975; whereas, the term “Extra Duty Deposit” (EDD) refers to the deposit of certain prescribed percentage of declared assessable value, pending submission of documents in respect of related party transactions under SVB investigation. This EDD is in addition to and separate from the deposit of certain sum, being the prescribed percentage of differential duty between the provisionally assessed duty and the duty that may be finally assessed, which is taken as security under Customs (Provisional Duty Assessment) Regulations, 1963/2011. Therefore, we are of the considered view that the provisions relating refund of ‘duty’ as contained in Section 27 of the Customs Act, 1962 and those relating to “Extra Duty Deposit” arising on account of ordering of provisional assessment of duty till finalization of such provisional assessments for determination of duty finally payable by the importer under Section 18 ibid, in respect of SVB cases implemented through CBEC Circular cannot be equated to as “duty”. Further, EDD is secured by Revenue for a specific purpose of obtaining the documentation in time, for enabling timely finalization of provisional assessments by the department, whereas the “duty” and “security of duty” are determined by the proper officer of customs for securing the payment of the deficiency, if any, between the duty as may be finally assessed or re-assessed, as the case may be, and the duty provisionally assessed. Therefore, we are also of the prima facie view, that the EDD is paid by an importer, pending finalization of provisional assessment for a specific purpose and its estimation based on differential duty as a measure and its continuation cannot be dependent on finalization of assessment. In other words, the duties of customs paid under any type of assessment i.e., provisional, re-assessment, final assessment etc., are in the nature of ‘duty’ as defined under Section 2(15) ibid, “Extra Duty Deposit” by its nature and as explained in the CBEC circular is in the nature of ‘deposit of certain sum’ in order to ensure timely submission of information by the importers under SVB investigation, for the purpose of expeditious finalization of provisional assessments made under Section 18 ibid. Though the quantum of EDD deposit is determined on the basis of declared value, such measure of the deposit cannot by itself convert its nature to be a ‘duty’. Further, such quantum of deposit has also been prescribed at 1% and at 5% depending upon the circumstances as prescribed in CBEC circular. Further, upon furnishing of required information by the importers the requirement of payment of EDD is dispensed with by CBEC, while continuing the imports under SVB to be assessed under provisional assessment. Therefore, it also transpires from the above, that payment of EDD is for a specific time period, during the pendency of provisional assessment on account of SVB investigation, and it is only for the purpose of submitting the requisite information by the importer for determination of duty that is finally to be assessed by the proper officer of customs under Section 18 ibid. At the most EDD can be kept as reserve or ‘advance’ being in the nature of ‘deposit’ which is obtained by Revenue as an ‘extra amount’, which could be adjusted with the duty finally determined (on account of valuation of related party transaction), in case the security obtained during provisional assessment is insufficient and the importer had not paid the differential amount due on account of finalization of provisional assessment. Even though, such deposits made in the form of EDD may be available for adjustment against the deficiency of finally determined duty, in the context of present case where in comparison to the provisionally assessed duty paid there is no case of insufficiency in the duty already paid, as the transaction values were accepted, the EDD amount is refundable. Further, since the purpose and the manner of collection of EDD is to ensure timely submission of information, in cases where the EDD is not required to make the deficiency of finally assessed duty, in our considered view, the same is refundable to the importer, by applying legal provisions of Section 27A ibid mutadis mutandis to EDD as it applies to the duty, as EDD is collected for purpose of Sections 17 & 18 ibid.

8.3 On careful examination of the Order-in-Original No. S/9-50 GATT/97 GVC dated 26.10.1998, it clearly transpires that the provisionally assessed B/Es on account of SVB investigation in respect of related party transactions between the appellants importer and M/s Marubeni Corporation, Japan was finalised under Rule 4(3)(a) of CVR, 1988 read with Section 14 of the Customs Act, 1962 by accepting the declared invoice value for the imported goods as the transaction value to be adopted for the purpose of determining finally assessed customs duty. It was also ordered that all pending provisionally assessed B/Es of the appellants importer at different ports/Customs formation shall be finalised accordingly. Further, the said order have also held that the decision of accepting the value declared by the appellants importer will remain in force till the present method of invoicing remains unchanged and that on the expiry of 3 years from the date of this order, if there was no renewal, then it is the practice that the said order stands expired and the assessing groups may resort to provisional assessment again with EDD equivalent to 1% of the assessable value, in respect of related party transactions. The relevant portion of the said order-in-original dated 26.10.1998 is extracted and is given below:

”ORDER

In keeping with the aforesaid facts I, hereby, thus order to accept the transaction value and invoices raised accordingly for goods in terms of Rule 4(a) of Customs Valuation Rule 1988 when the same is imported by M/s. Vardhman Acrylics Ltd, from M/s. Marubeni Corporation Japan after proper and usual scrutiny. Accordingly, all the pending provisional cases also may be finalized and Revenue deposit if any may be refunded subject to applicability.

The above decisions have been taken on the basis of pary’s statement and declarations made in their various letters to this branch. In case, there is any factual error or omission in declarations, the same should immediately be brought to this Branch. These decisions will remain in force till the existing collaboration/ agency/ distribution/ agreement/ arrangements and present method of invoicing or pricing remain unchanged. Any change affecting the invoice value materially should be intimated to this branch without delay.

This decision is subject to occasional review/for a final review after a period of 3 years. These decisions shall be review after a period of 3 years. These decisions shall be reviewed as and when information additional or contrary to what is stated is available.”

8.4 The above order finalizing the aspect of valuation of imported goods for the purpose of determining the relationship having influenced the transaction value or otherwise, was reviewed by the department and the same was appealed against by the department and was also agitated before the Tribunal and Hon’ble High Court of Bombay for long period till the refund amount was sanctioned to the appellants vide Order dated 06.11.2015 and 13.11.2015. Therefore, the direction in the said order dated 26.10.1998 for finalization of provisional assessments have not been implemented by the department. Consequent to the passing of such order dated 26.10.1998, the appellants importer have filed two refund applications both dated 22.01.1999 claiming refund of EDD for an amount of Rs.96,42,224/- & Rs.74,23,079/-, and the same was received under acknowledgement at the respective Appraising Groups VA & EPCG of New Custom House, Mumbai on 25.01.1999. Perusal of the case records indicate that the said the refund claim was filed in the prescribed form “Application for refund of duty/interest” in Part-A containing particulars itemized under Sl. No. 1 to 13; Declaration by the claimant, along with Annexure providing the amount of refund under each of the B/Es and in total.

8.5 From the case records, we do not find that any action had been taken by the department on such refund claims made by the appellant, possibly, since the SVB order dated 26.10.1998 was under appeal. However, much later in response to the refund claim filed by the appellants importer, the Assistant Commissioner of Customs, Gr.VA, New Custom House, Mumbai letter dated 08.07.2016 had informed them that the CBEC Circular No.59/95 dated 05.06.1995 clearly states that “no interest is payable in respect of revenue deposits (for example deposits for project import etc.)”. The said instructions as contained in Circular dated 05.06.1995 are extracted and given below:

“Subject : Customs Refund Application (Form) Regulations, 1995 – Interest on Refund Instructions – Regarding.

I am directed to say that with the enactment of the Finance Bill, 1995 with effect from 26-5-1995 Section 27A relating to payment of interest on delayed refund of customs duties have become part of the Customs Act, 1962. Consequently, Notification No. 32/95(N.T.) Customs, dated 26-5-1995 has been issued by the Board to specify the rate of interest payable by the Department in the case of delayed refunds to customs duties in terms of the said Section 27A. The rate of interest fixed for the time being vide the said notification is simple interest of 15% per annum. Instructions have already been issued by TRU as a part of the Budget instructions regarding the payment of interest and the calculation of period for which interest is payable.

2. In order to give effect to the aforesaid provisions and to streamline the procedure for processing of refund applications the Customs Refund Application (Form) Regulations, 1995 have been prescribed by the Board in terms of Notification No. 34/95(N.T.) Customs, dated 26-5-1995. These regulations supersede the Customs Application (Form) Regulations, 1991.

3. The new regulations provide for the form and manner in which an application of refund is to be made. As may be seen, the regulations also provide for the scrutiny of an application and its return to the applicant within a period of 10 working days, if it is found incomplete in any manner or detail. If however, the application is found to be complete in all respects for the purpose of processing the refund claim the same is to be acknowledged within the period of 10 working days. The interest free period of 3 months for processing the claim will be deemed to start from the date of receipt of the complete refund application.

4. The afore indicated provisions warrant that the Department is geared to meet the new standards required by law as the payment of interest by the Government in cases of delayed settlement of refund cases would be detrimental to Government revenue. Accordingly, steps are to be taken by the Commissioners of Customs to closely monitor the performance of the refund cells of the Custom Houses to ensure that all refund claims are settled at the earliest and in any case before the period the interest liability starts. In this direction the centralisation of all types of refund claims and their settlement procedure may be examined by the Commissioners for greater efficiency and accountability.

5. As the period of interest determination starts from the date of receipt of a complete refund application, the responsibility of proper scrutiny of the applications for determining the completeness or otherwise of the applications can not be under estimated. Accordingly, particular importance is to be given to this area of work and it may be ensured that there should be proper selection of officers conversant with such work. In case of delays not warranted in the administrative system, perhaps, Government would be constrained to recover the interest paid from the official who were responsible for such delays.

6. The finalisation of refund claims are to be closely monitored and it may be ensured that these are decided without fail within the period provided. No Interest liability should normally lie on the Government. It is further desired that all refund claims in future be settled at the level of Assistant Commissioner only (and not by Superintendent/Appraiser). It may be noted that the interest is payable only in respect of delayed refunds of customs duties. No Interest is payable in respect of deposits (for example deposits for project import, etc.) Pre audit system as well as issue of cheques should be ensured at utmost speed.

7. I am directed to say that the Board has desired that this aspect of tax administration be given due importance in view of the revenue implications. Accordingly, the Commissioners of Customs concerned may evolve a suitable procedure for implementing the new legal provisions. Suitable detailed Standing Order to departmental officers may be issued. Trade may also be advised of this procedure for filing claims in complete forms by issue of a Public Notice. Copies of Standing Order/Public Notice may be endorsed to the Board [Director (Cus.)] and to DGIACCE, Delhi.”

8.6 On plain reading of sub-section (2) of Section 27 ibid, it transpires the said legal provision mandates the Assistant/Deputy Commissioner of Customs, on receipt of refund claim application, to satisfy himself whether the whole of any part of the duty or interest paid by the applicant is refundable or otherwise, and if refundable then credit such amount to the consumer welfare fund or pay the amount of refund to the applicant if the unjust enrichment angle is fulfilled. The Customs Refund Application (Form) Regulations, 1995 issued vide Notification No.34/95-Customs dated 26.05.1995 as amended in terms of powers vested with the Board vide Section 157(2)(aa) ibid, provide for the form and manner of filing application for refund under Section 27 ibid. The prescribed proforma for submission of refund claim is given in Part-A and Part-B which is to be filed by the claimant of refund; and the proper officer of customs, within ten days of its receipt, upon scrutiny, shall point out deficiency, if any, and return the application to the applicant/claimant for re-submitting the refund claim application after making good the deficiencies, as per prescribed proforma in Part-C. On perusal of the case records, it is found that the appellants importer had submitted the refund claim application in the prescribed format Part-A and Part-B. However, in view of the appeal filed by the department against the SVB Order dated 26.10.1998, the respective Assistant Commissioners of the appraising group did not scrutinize or act upon the refund claim of EDD made by the appellants.

8.7 We also find that the legal provisions governing refund of duty, inter alia, provide for scrutiny of refund claim application and require the proper officer to either reject the refund claim if found not eligible; or to sanction the refund claim and further to pass on the refund amount to the Consumer Welfare Fund; or to the applicant, in case it is established that the burden of duty claimed as refund has not been passed on by the claimant to any other person. There is no provision for keeping it pending indefinitely, on the ground that the decision or order from which the refund is arising is appealed against.

8.8 In the protracted litigation of the present case, the provisionally assessed duties were finally assessed on the basis of the SVB order dated 26.10.1998, by accepting that no further addition to the declared value of imported goods is required by passing the Orders-in-Original/ Refund Order No.792/AC/Gr.VA/RG/2007-08 dated 26.03.2008 and No.228/08 dated 22.05.2008. However, in both these orders, it was concluded that the importer appellants had failed to show that the burden of refund amount claimed has not been passed to their customers or any other person and thus the refundable amount was ordered for crediting to the Consumer Welfare Fund. However, after further appeals before the Commissioner (Appeals) and the Tribunal for a number of times, and finally on careful reexamining of the facts and the balance sheets by the Assistant Commissioner of Appraising Groups-VA & EPCG, and on the basis of the factual examination of the unjust enrichment angle by the Tribunal in Final Order dated 07.01.2015, it was found that the refund amounts is payable to the appellant importer. Further, the Assistant Commissioner of Appraising Groups-VA & EPCG have also recorded in their order that the earlier order dated 26.03.2008 & 22.05.2008 directing to credit the refund amount to the Consumer Welfare Fund (CWF) has not been carried out and thus were available for sanction to the appellant importer, and thus were accordingly sanctioned to them. Further, in terms of the legal provision of Section 27 ibid as prevalent at the relevant time, a person could claim refund of duty, which was paid by him in pursuance of an order of assessment, by making an refund application. In the factual matrix of the present case, even though an application for refund was made before the Assistant Commissioner of Customs, Appraising Group VA and EPCG, the effective order of assessment upon finalization of provisional assessment, initiating the clock for refund claim had arisen only on account of passing of Orders-in-Original dated 26.03.2008 & 22.05.2008. Therefore, we are of the view the application for refund could be effective only from that date, on which the two orders were passed for refund of the amount of EDD not being required to be adjusted after finally agreeing to the fact that correct amount of duty to be paid on the imports was already paid by the appellants at the stage of initial import itself. Thus, the period for which interest on delayed refund, if any, would start from the expiry of three months from the respective date of the orders of original authority determining the amount refundable to the applicant, thus enabling appellants importer for filing the claim for refund, to till the date of actual payment of the refund amount. In other words, when the legal provision under Section 27 ibid, as it stood at the relevant point of time, allowed any person for filing of a refund claim of duty paid by him only ‘in pursuance of an order of assessment’. Therefore, prior to such passing of an order in finally assessing the duty liability, upon finalization of SVB angle of valuation of imported goods arising from related party transaction, no refund claim can be entertained under Section 27 ibid.

8.9 Further, we are also of the considered view, that once the issue of eligibility to sanction refund amount to the appellants importer was determined by finalizing the provisional assessments after accepting the finality of order of SVB dated 26.10.1998 before the Hon’ble High Court of Mumbai in W.P. No. 2592 of 2007, the appellants importer were eligible to be sanctioned with the refund amount claimed by them. The assessments were finalized by the respective Appraising Groups of VA & EPCG on 22.02.2008 and 24.03.2008 respectively, and the refund was sanctioned on the basis of the application for refund that was already available with them vide orders dated 26.03.2008 and 22.05.2008, by directing credit of refund amount to CWF. Therefore, when the issue of finalized duty recoverable from the appellants importer having been determined, and that the amount refundable being in the nature of EDD, these are liable to refunded to the appellants. However, such refund were finally sanctioned by the Assistant Commissioner of Appraising Groups of VA & EPCG subsequently vide Orders dated 13.11.2015 and 06.11.2015.

8.10 Further, it is not the case of the Department that the EDD paid by the appellants importer was required to adjust the deficiency arising on account of determination of final assessment of duty amount, as in none of the Orders-in-Original passed by the jurisdictional Assistant Commissioners in charge of appraising, such EDD amount was required for adjustment. On the other hand, the provisionally assessed duty paid by the appellants importer was sufficient to discharge the finalised duty, as the transaction value was accepted for final assessment and the EDD was required to be refunded to them. Therefore, from the facts of the case, the amount of EDD is eligible to be paid back/refunded to the appellants importer, once a speaking order was passed on 13.11.2015 and 06.11.2015 in terms of the legal provisions of the Customs statute for accepting the declared value as transaction value, in finally assessing the duty liability.

9.1 Besides the above, we also find that the department had subsequently issued Public Notice No. 5/2012, dated 17-01-2012 for handling the matters of refund of duty, particularly between Centralized Section and Appraising groups, Refund for avoiding inconveniences to the trade and industry. The extract of the said PN is given below:

“Refund in case of Amendments to Bill of Entry

1. Difficulty has been expressed by Trade to get the refund in the matter where Bills of Entry are to be finalised prior to sanction of refund, for example in the case of appellate orders revising assessments already finalized etc. In such cases Refund Section, on receipt of refund claims, issues deficiency memo to importer for producing re-assessed Bill of Entry or amendment certificate.

2. In order to address the inconvenience caused to Trade, in cases of the refund as above, following steps should be taken by the Refund Section.

(i) Refund Section shall accept the claim and no deficiency memo be issued to get the Bill of Entry re-assessed.

(ii) Refund Section officer after scrutinizing the refund claim, if required, shall forward the file to concerned assessing group for re-assessment/ finalization/amendment.

(iii) Assessing group will re-assess the Bill of Entry on priority basis within five working days. Concerned Group should get the deficiencies rectified, get documents or indemnity bond from applicant wherever required within such period. In case assessing group further notices any discrepancies while reassessing/finalizing the Bill of Entry the same may be intimated to Refund Section.

(iv) Refund Section will monitor the file movement and ensure that the claim is settled within the statutory period.

Any difficulties faced by the Trade or Officers in this regard may be brought to the notice of ADC/Refund. [Commissioner of Customs (Import), ACC, Mumbai, Public Notice No. 5/2012, dated 17-01-2012]”

Though this instruction was not applicable in the present case, as it was issued subsequently, the central theme of the department is that finalization of B/Es under provisional assessment were to be completed early within short window of five days. On careful perusal of the facts of the present case, we are of the considered view that the Assistant Commissioner who has finalized the provisional assessment should have also processed the refund application consequent to such finalization, within the prescribed time and pass necessary orders on the refund claim as per law. This course of action would have been consistent not only with the legal provisions but also the various decisions of the Hon’ble High Courts in the matter of refund of EDD. Therefore, in our considered view, non-payment of refund of EDD within three months from the date of passing of Orders-in-Original dated 26.03.2008 and 22.05.2008, is saddled with the liability to pay interest at the prescribed rate, in terms of Section 27A of the Customs Act, 1962. This is also evidential from both the refund claims dated 22.01.1999, complete in all respects, for an amount of Rs.96,42,224/- and Rs.74,23,079/- was duly received at the New Custom House, Mumbai on 25.01.1999, and the same had not been disposed of by the department and was kept pending with them, for deciding the final order of assessment enabling refund of EDD.

9.2 The various cases in which the matter of refund of EDD and interest for delay in refund beyond the prescribed time limit was dealt with by various judicial forum supports our above view. The relevant extract of the judgements passed by the Hon’ble High Court/Tribunal are given below:

(1) Assistant Commissioner of Customs (Refunds), Chennai Vs. Dalmia Cement (Bharat) Ltd. reported in (2025) 31 Centax 343 (Mad.) in W.A.No. 1084 of 2020 and C.M.P.No. 13255 of 2020, decided on 2-12-2020

“8. The alleged reason assigned by the Department that there was some investigation pending of which no details are placed on record, is not at all a justifiable reason in the light of Board’s own Circular as quoted by the learned Single Judge. No such material has been placed before this court to justify the action of the Customs Department not to finalise the Provisional Assessment for 16 years and even by now to keep the EDD a mere Security Deposit by Importer/ Petitioner with them like this.

9. The direction of the learned Single Judge, is, therefore, perfectly justified and does not call for any interference by this court in the present intra-court Appeal. Such an innocuous and correct direction of the learned Single Judge is also not complied with by the Revenue Department so far even though there was no interim order in favour of the Customs Department against the order of the learned Single Judge.

10. Section 27A of the Act provides that interest to be paid on such refund to be not below 5% and not exceeding 30% per annum may be fixed. It has also been brought to our notice that vide Notification 75/2003-Cus.(NT) dated 12th September 2003, issued under Section 27A of the Act the interest at the rate of 6% has been fixed by the Central Government.

11. Accordingly, we direct refund of the EDD amount to the Petitioner/ respondent herein forthwith within a period of 4 weeks from today with interest at the rate of 6% from 17.12.2007 till the actual refund and if there is a delay in making the refund of EDD beyond 4 weeks from today, interest at the increased rate of 9% would be payable by the Appellant Department and the excess interest in such case would be recovered from the Officer concerned who delays the matter any further.”

(2) Commissioner of Customs, Bangalore Vs. Hitachi Koki India Pvt. Ltd. reported in 2012 (281) E.L.T. 207 (Kar.)

“4. Against the said order, second appeal was filed before the Appellate Tribunal which set aside both the orders and remanded the matter back to the assessing. authority. After remand, the additional value laid was excluded and the provisional transaction value declared was accepted. In the meanwhile, the assessee had paid additional value. Therefore, he wrote letters demanding refund of the said amount. However, the same came to be rejected by the assessing authority on the ground that it was barred by time. Aggrieved by the same, he preferred an appeal. The appellate authority held that, the refund claim that has been preferred by the assessee is not customs duty, but it is extra duty deposit. Thus, this amount cannot be equated with the duty payable by the assessee against the import of the goods by them. At the moot, it can be treated as a precautionary measure to cover up/make good the difference of duty payable by them after completion of final assessment. Therefore, the appellate authority held that the time limit stipulated under Section 27 of the Customs Act, 1962 is not applicable in the instant case. The provisions under Section 18(1) and 18(2) could have been followed and refund would have been granted automatically after completion of final assessment and cancellation of PD bonds. In coming to that conclusion, he relied on two judgments of the Tribunal at Bangalore and Chennai and thus the order of the assessing authority was set aside and a direction was issued to refund the money. Aggrieved by the same, the assessee preferred an appeal to the Tribunal. The Tribunal agreed with the said reasoning, dismissed the appeal. Aggrieved of the said order, the revenue is before this court in appeal.

5. From the aforesaid facts it is clear that, the refund is not sought for the excise duty paid in excess of what was payable under law. The refund was sought in respect of the additional value insisted upon by the department being the value of technical knowhow and royalty. It was added to the excise duty payable. When the assessee authority held that the customs duty paid by the assessee was proper and no additional duty need be paid, they were under an obligation to refund this additional amount which was collected, which had no basis. In such circumstances, Section 27 is not attracted. That is the view taken by the appellate authorities relying on the judgment of the Tribunal earlier. Therefore, the impugned order is legal and valid and does not suffer from any legal infirmity which calls for interference, No substantial question of law arises for consideration. Accordingly, appeal is dismissed.”

(3) Nittan India Tech Pvt. Ltd.Vs. Deputy Commissioner of Customs (Refund), Chennai reported in (2025) 34 Centax 104 (Mad.)

“9. It is further submitted that the Extra Duty Deposit (EDD) is merely a deposit and not customs duty payable on the importation of goods in terms of Section 12 of the Customs Act, 1962. It is further submitted that this very aspect was considered by this Court in Commissioner of Customs, Chennai v. Aristo Spinners Pvt. Ltd., 2008 (226) E.L.T. 42 (Mad.), wherein, it was held as under:-

“As the amount in question relates to encashed Bank Guarantee, the same cannot be considered as Customs duty and hence section 27 of the Customs Act, 1962, which provides for refund of any duty and interest, if any, paid on such duty in pursuance of an order of assessment, cannot be invoked as there is no payment of duty in pursuance of an order to safeguard the interest of the revenue in the event of the importer committing default in performing the export obligation cast upon him for the purpose of availment of concession in importing the capital goods.”

16. Having considered the arguments advanced by the learned counsel for the petitioner and the learned Standing Counsel for the respondent.

17. In my view, there is no justification in the impugned order passed by the respondent rejecting the request of the petitioner for refund of the amount paid by the petitioner pursuant to Circular No.11/2001-Cus dated 23.02.2001 of the Central Board of Indirect Taxes. Content of which has been extracted in Paragraph No.2 of this order.

17(A) The amount that was collected by the Assessing Officer in view of the Special Valuation Branch (SVB) proceedings are nothing to deposit and not a customs duty as is contemplated under Section 12 of the Customs Act, 1962, although such deposit were eligible to be appropriated towards the duty liability of the petitioner after final assessment of the Bill of Entry.

17(B) As such, amount that has been calculated over and above the tax duty payable by the petitioner is to be refunded back only after the Bill of Entries filed are finally assessed and assessment is completed. Needless to state, such refund will be subject to the petitioner satisfying that there will be no unjust enrichment on account of refund in terms of Section 27 of the Customs Act, 1962.

18. That apart, it is submitted that the impugned order is also in gross violation of principles of natural justice as the petitioner’s reply dated 22.04.2021 has not been considered while passing the impugned order.

19. Under these circumstances, the impugned order is set aside with consequential relief. The respondents are directed to complete the proceedings within a period of six months from the date of receipt of a copy of this order.”

9.3 We also find that the judgment of the Hon’ble Supreme Court in Mafatlal Industries Ltd. Vs. Union of India – 1997 (89) E.L.T. 247 (S.C.) have not dealt with the refund of EDD, as they had dealt with in the said case three types of levy of duty i.e. unconstitutional levy of duty, duty levied under erroneous interpretation of law and duty levied under mistake of law. Therefore, we are unable to take guidance from the aforesaid judgement for dealing with the present issue. This may be seen from the relevant paragraph of the said judgment of the Hon’ble Supreme Court referred above.

(4) MAFATLAL INDUSTRIES LTD. Versus UNION OF INDIA – 1997 (89) E.L.T. 247 (S.C.)

“131. As stated by me earlier in Paragraph 5 of this judgment, the claims for refund can be classified broadly into 3 groups. They are –

(I) the levy is unconstitutional – outside the provisions of the Act or not contemplated by the Act.

(II) the levy is based on misconstruction or wrong or erroneous interpretation of the relevant provision of the Act, Rules or Notifications; or by failure to follow the vital or fundamental provisions of the Act or by acting in violation of the Fundamental Principles of judicial procedure.

(III) mistake of law – the levy or imposition was unconstitutional or illegal or not exigible in law (without jurisdiction) and, so found in a proceeding initiated not by the particular assessee, but in a proceeding initiated by some other assessee either by the High Court or the Supreme Court, and as soon as the assessee came to know of the judgment, (within the period of limitation) he initiated action for refund of the tax paid by him, due to mistake of law.”

However, the aspect of unjust enrichment that is required to be fulfilled by the claimant of refund as held in the above judgement, was proved by the appellant before the proper officers of customs and the eligible refund has been properly sanctioned by the proper officers in the present case, in compliance with the above judgement of the Hon’ble Supreme Court.

9.4 We further find in the case of Bihar Foundry & Castings Limited Vs. Union of India & Ors. – (2026) 42 Centax 3 (Jhar.), it was held that the provisional assessment must be finalized within six months’ time in terms of CBEC’s Instructions issued to field formations vide F. No. 512/5/72-Cus.VI dated 23.04.1973; and F. No. 511/7/77-Cus.VI dated 09.01.1978 and Circular No. 17/2011-Cus., dated 08.04.2011, and thus the show cause notices and order adjudication orders determining differential duty was quashed as void ab initio. The relevant paragraph of the said order is extracted below:

“21. It is not out of place here to mention that Rule 5 of Customs (Finalization of Provisional Assessment) Regulation, 2018 (the 2018 Regulation) applies only to provisional assessment made after 14-08-2018; hence, in the case at hand it cannot be applied on the provisional assessments of the 4 Bill of Entries as they are made in the year 2012. The limitation for finalization to the case at hand would be governed by Para 3.1 of the CBIC Instruction as per which the finalization of provisional assessment is to be made expeditiously, well within 6 months whereas in the instant case the finalization is done after 6 years to 9 years.”