Month: February 2020

1,168 articlesService Tax

Service Tax

No Service Tax on Rent from bullock Carts with Tyres & without bullocks or driver used in Sugarcane Transportation

Company Law

Company Law

SPICE+- FAQs with Analysis of Part A and B

Income Tax

Income Tax

Is AIR based Notice under section 147 void ?

Income Tax

Income Tax

Section 80-IBA Affordable Housing Scheme: Analysis of Section, FAQs, Relevant Case Laws and Updated with Finance Act 2020

Income Tax

Income Tax

Section 10(38) – Tax on Long Term Capital gains from on the transfer of equity oriented funds

Income Tax

Income Tax

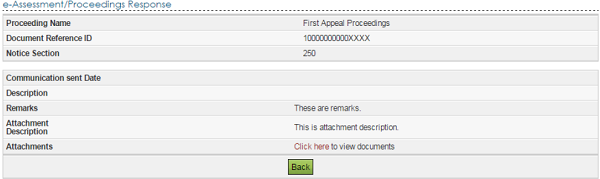

How to opt for Online Assessment and Submit Online response

Goods and Services Tax

Goods and Services Tax

Self-adhesive HAUV Polyester Film with U.V. Printing classifiable under Chapter 3919

Corporate Law

Corporate Law

NCLAT : Defaulting company liable to repay FDR amount alongwith interest to its deposit holders

Goods and Services Tax

Goods and Services Tax

AAR cannot decide on question which is already pending before department

Goods and Services Tax

Goods and Services Tax