Day: May 28, 2017

13 articlesGoods and Services Tax

Goods and Services Tax

Analysis of Goods & Service Tax (GST) on Real Estate Industry

Income Tax

Income Tax

Addition based on mere Sales Tax Dept observations not sustainable

Corporate Law

Corporate Law

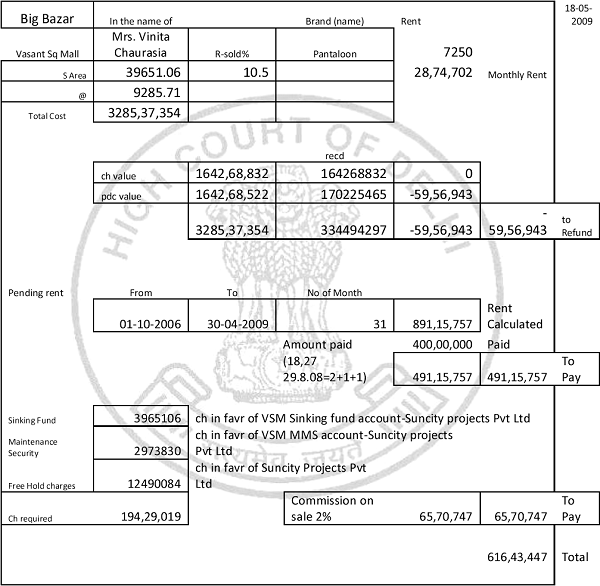

Husbands Income Not Sole Criterion to award Maintenance amount

Income Tax

Income Tax

In absence of incriminating material found during search concluded assessments cannot be reopened U/s. 153A

Goods and Services Tax

Goods and Services Tax

Way Bills and its Rules under GST

Income Tax

Income Tax

Section 153C proceedings not valid if initiated on the basis of document not belonging to Assessee

Income Tax

Income Tax

Trust for sole benefit of an individual can claim section 54F deduction

Income Tax

Income Tax

Full value of consideration used in section 48 does not have reference to market value

Income Tax

Income Tax

Reopening based on reappraisal of existing material is invalid

Income Tax

Income Tax