On April 17, 2020, Department for Promotion of Industry and Internal Trade came up with an amendment in Foreign Direct Investment Policy, 2017 vide Press Release No. 3 (2020 Series) in order to shield the corporates from hostile acquisitions which may arise due to downward trend in the share prices of the Company. The experts are debating over the legality of this move of the Government and terming it as discriminatory & violative of rules set out by World Trade Organisation (“WTO”) i.e. restricting market access and national treatment. It appears that the decision to restrict FDI came as a reception to the acquisition of a stake in HDFC by the People’s Bank of China through the open market.

Though the intent of this amendment was to inflict definite curtailment for safeguarding against opportunistic acquisitions from neighbouring countries, the overall unambiguous safeguard still remains quizzing. The aforementioned press circular doesn’t mention and define the term “Neighbouring Countries of India”. However, the same shall be construed in accordance with the word “shares land border with India” and shall accordingly mean China, Bangladesh, Pakistan, Myanmar, Nepal, Bhutan and Afghanistan.

The amendment entails the mandatory obligation to take Government approval route before investing into India, directly or indirectly, on each entity of the Neighbouring Country or where the beneficial owners (including individual) is situated in or citizen of Neighbouring Country. In addition to this, any change of ownership of existing or future FDI of an entity in India, directly or indirectly, resulting in the beneficial ownership being situated in a Neighbouring Country would also necessitate prior Government approval.

Ms. Roma Priya, Founder of Burgeon Law said that “The government’s decision on FDI norms was much anticipated in order to eliminate the hostile takeovers. The Indian economy has a great potential and it is important for us to raise our stake in the corporate assets which can grow to be some of the most lucrative business entities. The global economy has been severely hit by the pandemic, and it is going to take a while till the figures bounce back to normalcy. Considering the dominant state of China, many other economies are also mulling about implementing this measure to avoid any opportunistic takeovers by China. Offshore capital is paramount for India’s startup ecosystem and China has been one of the major power backers of our unicorns. Hence, we hope the government issues detailed guidelines in terms of timelines and procedures for seeking approval or creates certain exceptions for startups.”

Any FDI in India require the entity which receives the investment from outside India to file Form FC-GPR within 30 days of allotment of shares via Entity Master Form on FIRMS Portal and acquisition of shares of Indian Entity requires reporting of transfer of shares in Form FC-TRS. The Government of India will face hindrances in keeping an eye on subsequent change in Beneficial Ownership between two non-resident entities which don’t require reporting to Government.

The aforesaid decision will be implemented from the date of FEMA Notification. Previously, a citizen or entity of Bangladesh and Pakistan were required to take prior approval of Government before investing into India. It is unequivocally to be noted that citizen or entity of Pakistan still can’t invest into defence, space, atomic energy and other prohibited sector through any route.

Furthermore, the definition of “Beneficial Owner” remains in question as the same has not been yet clarified by the Press Release. It may be clarified in FEMA Notification and it may resemble with the existing definition given in Section 90 of the Companies Act, 2013 read with Companies (Significant Beneficial Ownership) Rules, 2019 in accordance with the recommendation of Financial Action Task Force. Companies Act, 2013 prescribes two criteria i.e. first is exercising 10% stake in the reporting entity and majority stake in chain of ownership and second is exercising control or significant influence in the reporting company.

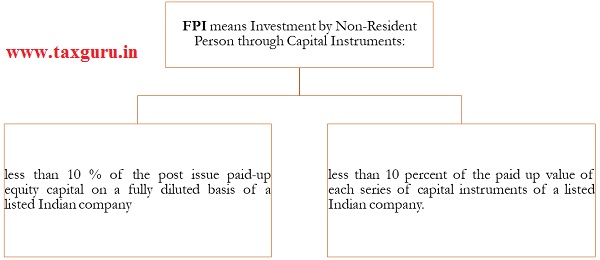

For avoidance of doubt, it is clarified that the aforementioned restriction for taking Government Approval apply to the Foreign Direct Investment (FDI) and not to Foreign Portfolio Investment (FPI). Since the regulations for FPI comes under the ambit of Securities and Exchange Board of India (SEBI), the SEBI is engaged digging and scrutinising the compositions of Foreign Portfolio Investors. The conceptual details about FDI and FPI is set forth below:

Foreign Direct Investment (FDI)

Foreign Portfolio Investments (FPI)

Hence, a person of Neighbouring Country would require approval from Government in following cases only:

1. Investment into Unlisted Indian Company (Even acquiring 1 Equity Share would constitute as FDI)

2. Investment in Listed Entity: 10% or more of the post issue paid-up equity capital on a fully diluted basis of a listed Indian company.

Fully Diluted Basis and Capital Instruments are construed as following:

Fully Diluted Basis means the total number of shares that would be outstanding if all possible sources of conversion are exercised.

Capital Instruments are equity shares, debentures, preference shares and share warrants issued by an Indian company.

The FPI License is granted by Custodian Banks acting in a capacity of Designated Depository Participants on behalf of SEBI in accordance with SEBI (FPI) Regulations, 2014.

Categories of FPI

Chinese Firms are controlling these FPIs in the following manner:

1. Infusing 25% of the Fund Corpus

2. Exercising significant influence and control

3. Controlling composition of board of directors & senior management

SEBI has increased scrutiny to identify the beneficial owners of these funds and also, SEBI has sent a letter to some Asian Countries (especially China) seeking details of Investment. As per the present applicable laws, Chinese Entities can freely acquire up to 10% stake in the Listed Indian Companies without Government Approval. We expect SEBI would come out with an amendment in FPI regulations to avoid hostile acquisitions in Listed Indian Entities at an underneath valuation.

Disclaimer

The entire content of this document has been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness, and reliability of the information provided, we assume no responsibility, therefore. Users of this information are expected to refer to the relevant existing provisions of applicable laws. The user of the information agrees that the information is not professional advice and is subject to change without notice. We assume no responsibility for the consequences of the use of such information.

About the Author- Author ‘SHIVAM GERA’ is a Dynamic and passionate professional with progressive experience in advising on issues in corporate laws, managing implications in commercial transactions, private equity, estate planning, drafting commercial agreements and deal evaluation. Being Career oriented, the author has completed his graduation in commerce from Satyawati College, University of Delhi and Qualified Company Secretary. He is currently working as Assistant Manager at Findoc Financial Services Group. Author can be reached at Contact: +91-8130562651 – Email: shivam@myfindoc.com.

Author Bio