Case Law Details

Brilliant Study Centre Private Limited Vs ITO (TDS) (ITAT Cochin)

Summary: The ITAT Cochin held that payments made by a coaching institute to faculty members engaged for imparting coaching in competitive examinations were liable for tax deduction under Section 194J as professional fees and not under Section 192 as salary. The Tribunal observed that although the institute exercised administrative control over attendance, working hours, leave, and exclusivity, such supervision was necessary for efficient management and did not establish an employer-employee relationship. The faculty members were referred to as consultants, received remuneration comprising fixed and variable components linked to lectures, were not entitled to statutory employee benefits such as provident fund, gratuity, bonus, leave encashment, or medical reimbursement, and independently discharged their professional duties. The Tribunal also noted that the faculty had declared the receipts as professional income under Section 44ADA, which had been accepted by the Revenue. Relying on judicial precedents distinguishing a contract for service from a contract of service, the Tribunal held that TDS under Section 194J was correctly deducted and deleted the demand raised under Sections 201(1) and 201(1A).

The central issue before the Tribunal was whether payments made by a coaching institute to its faculty members were liable for TDS under section 192 as salary or under section 194J as professional fees. The Revenue treated the faculty members as employees and held that the assessee had short-deducted tax by applying section 194J instead of section 192, thereby treating the assessee as an assessee-in-default under sections 201(1) and 201(1A).

The assessee, a well-known coaching institute imparting training for competitive examinations such as NEET, JEE and GATE, had engaged around 121 faculty members and deducted tax under section 194J on the payments made to them. During a survey under section 133A(2A), the Department observed that the institute prescribed working hours, maintained attendance registers, restricted faculty from teaching in competing institutions, required prior approval for leave and followed certain administrative rules. Based on these factors and statements recorded from faculty members, the Assessing Officer concluded that an employer-employee relationship existed and that tax ought to have been deducted under section 192.

The assessee contended that the faculty members were independent professionals engaged on a consultancy basis. They were paid professional fees consisting of fixed and variable components linked to lectures delivered, were not entitled to employee benefits such as provident fund, gratuity, bonus, leave encashment, medical reimbursement or insurance, and there were no written employment contracts. It was further pointed out that the faculty members themselves had disclosed the receipts as professional income under section 44ADA and the Revenue had accepted such treatment in their assessments.

The Tribunal observed that the decisive test was whether the relationship constituted a “contract of service” (employment) or a “contract for service” (professional engagement). Merely because an institution imposes attendance requirements, working hours, leave procedures and certain restrictions for administrative efficiency does not automatically establish an employer-employee relationship. Such controls are common in professional engagements and are intended to ensure smooth functioning of the organisation.

The Tribunal found that the faculty members were referred to as consultants, their remuneration was structured as professional fees with a variable component, they enjoyed autonomy in the manner of teaching, and no statutory employment benefits were provided. Significantly, the institute exercised no control over the professional methods adopted by the teachers while delivering lectures. The absence of employment contracts and the acceptance by the Department of the recipients’ returns showing the receipts as professional income further supported the assessee’s stand.

Relying extensively on the judgment of the Madras High Court in Dr. Mathew Cherian v. ACIT, which analysed the distinction between professional consultants and employees in the context of doctors engaged by hospitals, the Tribunal held that administrative supervision and operational controls are not conclusive indicators of a master-servant relationship. What is relevant is whether the organisation controls the manner in which professional services are rendered. Since the faculty members were free to exercise their professional expertise and teaching methods, the relationship was one of independent professional engagement rather than employment.

The Tribunal also drew support from decisions including Sushilaben Indravadan Gandhi v. New India Assurance Co. Ltd., CIT v. Ivy Health Life Sciences Pvt. Ltd., CIT v. Manipal Health Systems Pvt. Ltd., CIT v. Grant Medical Foundation and CIT v. Yashoda Super Speciality Hospital, all of which emphasised that professionals do not become employees merely because certain organisational controls are imposed.

Accordingly, the Tribunal held that the faculty members engaged by the assessee were independent professionals and not employees. The assessee had correctly deducted tax under section 194J and could not be treated as an assessee-in-default for alleged short deduction of tax. The orders passed under sections 201(1) and 201(1A) were quashed and the assessee’s appeal was allowed.

Ratio: The existence of attendance requirements, fixed working hours, leave regulations, non-compete restrictions and other administrative controls does not by itself create an employer-employee relationship. Where professionals are engaged for their specialised expertise, are not entitled to employment benefits, enjoy autonomy in rendering professional services and are remunerated as consultants, the relationship is one of contract for service and tax is deductible under section 194J rather than section 192.

FULL TEXT OF THE ORDER OF ITAT COCHIN

1. ITA No. 545/Cochin/2026 is filed by Brilliant study Centre Private Limited (the assessee/appellant) against the appellate order passed by the Commissioner of Income Tax (Appeals) – 1 Coimbatore for assessment year 2023 – 24 dated 27th of March 2026 wherein the appeal filed by the assessee against the order passed under section 250 one of the Income Tax Act, 1961 [the Act] by the Income Tax Officer (TDS), Kottayam on 4 April 2025 was dismissed and the assessee was held to be an assessee in default u/s. 201(1) and for levy of interest u/s. 201(1A) of the Act.

2. Aggrieved with the above order the assessee is in appeal before us raising several grounds of appeal as under:-

“1. The learned CIT(A) erred in law and on facts in confirming the order of the ITO(TDS) u/s 201(1)/201(1A) treating the appellant as assessee in default for alleged short-deduction of tax u/s 192 on payments made to faculties.

2. The learned CIT(A) grossly erred in upholding the finding that the faculties engaged by the appellant for imparting coaching in NEET. JEE. GATE. etc. are in employer-employee relationship, when in fact they were engaged on hourly basis as independent professionals rendering specialised services u/s 194J.

3. The learned CIT(A) failed to appreciate that there existed no appointment letters. no written contracts, no provident fund, gratuity, ESI or any other statutory employee benefits, which are sine qua non for an employer-employee relationship.

4. The learned CIT(A) erred in placing reliance on the attendance register and the term “salary” used in certain internal formats, which were common for both employees as well as consultants. He failed to appreciate that these were only administrative measures and the payments to the consultant faculties were purely on hourly basis for professional services.

5. The learned CIT(A) erred in not considering the violation of principles of natural justice in as much as the ITO(TDS) relied upon statements of 21 teachers but supplied only one statement to the appellant despite specific request.

6. The learned CIT(A) erred in not adjudicating the specific ground raised by the appellant that the Department cannot treat the same payments as “salary” in the hands of the assessee while accepting the same as “professional income” in the hands of the recipient teachers in their respective assessments, which tantamounted to approbating and reprobating as per convenience. The learned CIT(A) also failed to consider the crucial decision of the Hon’ble Mumbai ITAT in the case of ITO(TDS)(OSD)1(2) vs. Entertainment Network (I) Ltd. [ITA No. 1352/Mum/2014 & ITA No. 5227/Mum/2014, dated 11.01.2017] specifically cited by the assessee in this issue and further ignored the Service Tax / GST registrations and Service Tax / GST returns filed by the faculties treating the receipts as professional services.

7. The learned CIT(A) erred in not adjudicating the specific ground that once the recipient faculties have paid tax in full on the impugned receipts in their respective assessments and there is no further tax demand from the deductees. no additional liability can be fastened on the appellant (deductor) for any alleged failure to deduct tax at source, in view of the proviso to Section 201(1) of the Act and the binding judgment of the Hon’ble Supreme Court in Hindustan Coca Cola Beverage Pvt. Ltd. vs. CIT (2007) 293 ITR 226 (SC).

8. The learned CIT(A) wrongly relied upon the decision in District Intermediate Education Office vs. /TO (ITAT Hyderabad) which is distinguishable on facts, as the present case relates to expert faculties engaged by a private coaching institute for highly competitive entrance examinations, on hourly basis whereas the one which was considered by Hon’ble Hyderabad Bench were on guest lectures appointed by government based on written contracts.

9. The learned CIT(A) failed to appreciate that the restrictive conditions (non-compete) attract Section 28(va) read with Section 194J(d) and the payments were therefore liable for TDS only @ 10% u/s 194J.

10. The learned CIT(A) erred in not following the ratio laid down by the Hon’ble Supreme Court in Sushilaben lndravadan Gandhi vs. New India Assurance Co. Ltd. (2020) and other binding precedents on “contract for service” vs. “contract of service”.

11. The impugned order of the CIT(A) is bad in law, perverse and liable to be set aside.

PRAYER The orders of CIT(A) and ITO(TDS) may be set aside and the demand of 9,48,753 be annulled.”

3. The brief facts of the case show that assessee is a coaching institute in Kottayam imparting coaching for medical and engineering aspirants. A survey u/s. 133A (2A) of the Act was conducted on 18 December 2023 at the business premises of Brilliant Study Centre and Brilliant Study Centre Private Limited at its main Branch at Kottayam and other centres located across Kerala. The survey was conducted to verify the compliance towards the tax deduction at source provision for the FY 2018 – 19 to AY 2023 – 24.

4. During the survey, summons u/s. 131 of the Act were also issued to the various teachers and managing director of the company. During the survey it was noted that teachers are paid remuneration under professional services covering tax deduction at source as per provisions of section 194J of the Act instead of salary. Therefore on this issue proceedings under section 201(1) & 201(1A) was initiated and a notice was issued on 5 June 2024.

5. In the show cause notice the ld. AO noted the appointment process of the teachers shows that these are employees, however the record shows that these are considered to the professionals. The assessee has recruited 121 No. of teachers in order to impart entrance oriented coaching classes for engineering and medical students. The director of the company in response to the summons u/s. 131 has explained the procedure stating that appointment of the teachers are being done by conducting an interview by the director of the institute and after appointment based on the feedback provided by the students, the teachers were confirmed on regular basis. Further it was found that teachers were initially treated as salaried employees but was shifted to the professional category based on market consideration. This was the allegation of the ld. AO for the reason that in the initial stages the tax was deducted at the rates applicable to salary payment only, however when the faculties are joining from other reputed institutes, the deduction is made of tax at source u/s. 194J of the Act. It was further noted that the teachers appointed by the assessee were not allowed in any other coaching centre. For the purpose of proper attendance of the teachers, an attendance register is also maintained. The statement of the managing director was crossed verified with the statement of 16 teachers of the institute who were also summoned u/s. 131 of the Act. In the statement all these teachers stated that they were appointed on a verbal agreement with the management as faculty members, they are appointed on hourly basis, they were to take classes approximately at an average of 5 to 7 hours daily, for the period of appointment they were not allowed to take classes in other institutes. The teachers are also promised a yearly increase in the remuneration at the rate of approximately 10%. The teachers were also supposed to intimate the leave one day prior to the date of leave. Therefore according to the ld. AO, the assessee has employed all these teachers and taxes required to be deducted at source u/s. 192 of the Act, whereas the assessee has classified all these teachers as professional and has deducted tax at source u/s. 194J of the Act.

6. The assessee responded to the show cause notice of the AO vide letter dated 14 June 2024. According to the reply of the assessee, all these are administrative measures and assessee does not employ all these teachers but they are recruited as professionals and therefore the tax is rightly deducted u/s. 194J of the Act.

7. The ld.AO considered the explanation of the assessee and thereafter held that as effective control, set working hours, termination procedure, policies, leave rules applicable to all the teachers along with non-compete clause and monthly payment of the remuneration as well as medical insurance and provision of transport services clearly shows that the teachers are the employees of the assessee and therefore the tax should have been deducted by applying the provisions of section 192 of the Act. The ld. AO was further confronted that all these teachers have furnished the return of income disclosing the remuneration received by them paid by the assessee to them as professional fees applying the provisions of section 44ADA of the Act which has been accepted by the revenue. The ld. AO rejected the same, relied upon the several judicial precedent and concluded that there exists an employer-employee relationship between the deductor and the teachers and therefore the tax must have been deducted at source u/s. 192 instead of u/s. 194J of the Act. Accordingly the short deduction of tax was worked out at ₹ 765,124, interest under section 201(1A) was computed at ₹ 183,629 resulting into the total tax of ₹ 948,753 by passing an order u/s. 201 of the Act on 4 April 2025.

8. The assessee aggrieved with the above order preferred an appeal before the learned CIT – A wherein the assessee reiterated the submissions made before the ld. AO and stated that the impugned employees employed with entities to whom the remuneration is paid are professionals and not the employees of the assessee. Several judicial precedents were cited before him, however the learned CIT – A held that the degree of control and supervision exercised by the appellant on these persons clearly shows that those persons are employees of the assessee and therefore he dismissed the appeal of the assessee.

9. The assessee is aggrieved with the appellate order and preferred appeal before us.

10. The learned authorised representative submitted the detailed written submission on this issue and further relied on several judicial precedents. The written submissions were also filed at page No. 195 – 198 of the paper book citing several judicial precedents. The claim of the assessee is still the same as was contested before the AO that employees that the professional teachers are not the employees of the assessee but are professional and on payment the taxes are deducted at source u/s. 194J of the Act. These persons are not employees of the assessee and therefore the orders of the learned lower authorities are not sustainable. The learned authorised representative vehemently submitted that issue is squarely covered on the identical facts and circumstances by the decision of the Mumbai Benches of Tribunal in ITA No. 1352/M/2014 and 5227/M/2014 dated 11/one/2017 wherein it has been held that the payment made to the radio jockey on similar terms and conditions are held to be professional fees paid by the company to them and taxes required to be deducted u/s. 194J of the Act. Thus it was stated that the income of these teachers are also taxed under section 44ADA of the Act and therefore the orders of the learned lower authorities are not sustainable.

11. The learned departmental representative vehemently submitted that the facts stated by the ld. AO and confirmed by the learned CIT – A clearly shows that the amount paid by the assessee to the teachers is in the nature of salary as these persons are bound by a contract like an employee and therefore the tax should have been deducted u/s. 192 of the Act.

12. We have carefully considered the rival contention and perused the orders of the learned lower authorities. The only issue involved in this case is that assessee should have deducted tax at source under section 192 of the income tax act or under section 194J of the act. According to the assessee, tax should have been deducted and is deducted by following the provisions of section 194J of the act being the amount paid to the teachers engaged for imparting training were considered as professionals. The learned assessing officer and the learned CIT – A were of the view that assessee has employed the professionals who are teaching at that Institute and therefore payment made to them should have been subject to tax deduction at source under section 192 of the income tax act. The important fact that is to be mentioned here is also the fact that all those persons have filed the return of income as professionals offering the same under the head 44ADA of the act and same have been accepted by the revenue.

13. On carefully considering the arguments of both the parties it is clear that assessee is engaging teachers for imparting education of medical and engineering field

14. We find that the learned assessing officer has reached the conclusion that teachers are employees of the assessee for the reason that assessee exercises total control over the teachers in regard to their timings of work, holidays, call duties based on the exigencies of work, termination, entitlement to private practice, increments and other service rule, attendance etc. The claim of the assessee is that these are required for the purpose of the efficient running of the business of the assessee. Thus The key distinction in this regard is between a contract for service and one of service, and depends on several factors. The regulations, restrictions, guidelines and control exercised in regard to logistical and administrative functions of the workforce are not unique to a reduction organisations and it is difficult to identify any establishment that does not exercise some degree of control over the administrative and logistical functioning of the workforce, be they salaried or otherwise called as a consultant..

15.

16. We find that the identical issue arose before the honourable madras High Court in case of Dr. Mathew Cherian vs. Assistant Commissioner of Income-tax [2023] 151 com 154 (Madras)/[2023] 450 ITR 568 (Madras)[01-09-2022] wherein all those decisions relied upon by the learned revenue authorities are considered and decided by the honourable High Court holding that Where agreement between doctors and hospital revealed that doctors were not entitled for any statutory benefits and doctors held full responsibility for their medical decisions without any interference of hospital, it could be said that intention of parties were to engage in a relationship of equals and not one of master-servant and therefore, department was not justified in issuing reassessment notice under section 148A for taxing income returned by assessees as salary income. The honourable High Court held that:-

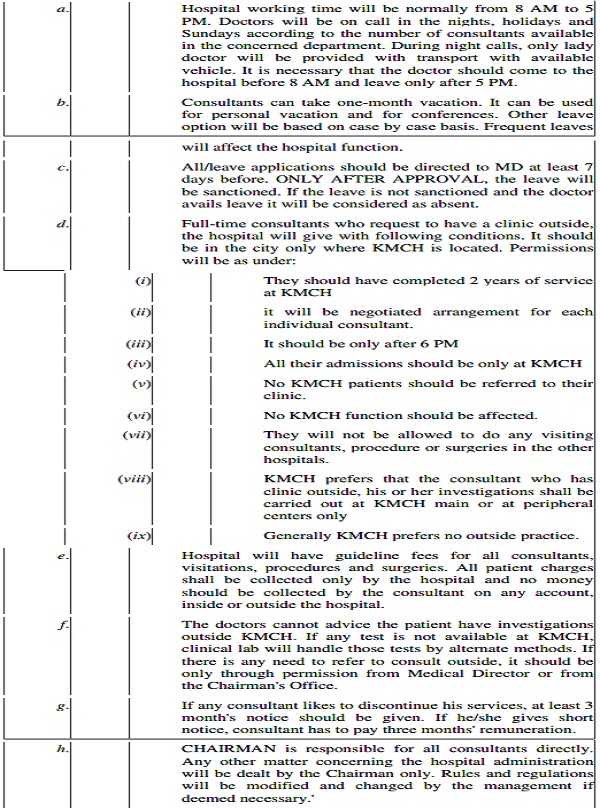

34. There are no differences that emanate from a perusal of the impugned orders and the references to the agreements and contracts are in standardized terms. The clauses extracted in WP.No.14515 of 2022 are thus taken to be representative of the agreement entered into by KMCH in the cases of all the petitioners. The clauses, as extracted in impugned order dated 12-4-2022 in W.P.No.14515 of 2022, read as follows:

** ** **

10. Also on perusal of the Revised Guidelines for practice of Medicines at M/s.KMCH, the following points reveal the existence of employer-employee relationship:

35. On the basis of the above clauses, the officer has come to the conclusion that KMCH exercises total control over the doctors in regard to their timings of work, holidays, call duties based on the exigencies of work, termination, entitlement to private practice, increments and other service rules.

36. The key distinction in this regard is between a contract for service and one of service, and depends on several factors. The regulations, restrictions, guidelines and control exercised in regard to logistical and administrative functions of the workforce are not unique to a hospital and I am hard-pressed to identify any establishment that does not exercise some degree of control over the administrative and logistical functioning of the workforce, be they salaried or otherwise.

37. Such a situation would, in fact, be extremely undesirable, if not leading to a situation of anarchy. No management would risk running an organization where the workforce comes and goes when they chose without any control exercise in areas of their functionality. Then again, the policy to permit private practice, does not, by itself, determine the existence or otherwise of a master-servant relationship. In facts, the terms as extracted as part of the impugned order reveal that the consultants are entitled to practice privately subject to certain regulatory conditions by the hospital.

38. To my mind, what is vital is that the professionals discharge their professional duties and functions in a free and fully independent fashion without any interference from the hospital management. Though it is expected that there would be regular quality control measures, this would not lead to the inference that there is control exercised over the discharge of professional functions.

39. That apart, some of the petitioners have also submitted that they have availed medical insurance to insulate them from patient/patient family claims, and this is a responsibility they carry solo.

40. In the case of Sushilaben Indravadan Gandhi (supra), the Apex Court dealt with the claim of insurance by the wife of a deceased doctor who had been attached to the Rotary Eye Institute/R3 in that case. The deceased had been travelling in a mini bus owned by R3 which had turned turtle leading to his injury and subsequent demise. The claim for insurance by his wife had initially been rejected on the ground that he was in the employ of R3 as on the date of the accident, as a result of which the limitation of liability provision in favour of the New India Assurance Company Limited would kick in.

41. The question that arose for consideration was as to whether the contract entered into by the deceased with R3 was a contract of service in which case a liability would be capped to an extent of Rs. 50,000/- or whether it was a contract for service in which case, the liability would be unlimited.

42. The Apex Court discusses several judgments rendered in the context of the Industrial Disputes Act as to whether persons who supplied goods or services in several capacities could be said to ‘in the employ’ of the employer.

43. In Dharangadhara Chemical Works Ltd. State of Saurashtra AIR 1957 SC 264, the Court held that the prima facie test for determination of a master-servant relationship is the right of the master to supervise and control the work done by the servant in the matter of not just in directing what work is to be done but also the manner in which he shall execute the work.

44. So too in the case of Mersey Docks and Harbour Board Coggins & Griffith (Liverpool) Ltd. 1947 AC 1 (HL). To quote Lord Uthwatt, ‘The proper test is whether or not the hirer had authority to control the manner of execution of the act in question’.

45. In Chintaman Rao State of M.P. AIR 1958 SC 388, the Hon’ble Supreme Court held that Sattedars and their coolies were not workers within the meaning of Section 2(1) of the Factories Act and in Birdhichand Sharma v. First Civil Judge AIR 1961 SC 644, the Court found that persons working in a beedi factory were workers under the Factories Act.

46. In Shankar Balaji Waje State of Maharashtra AIR 1962 SC 517, upon a consideration of the facts involved, the Supreme Court preferred to apply the judgment in the case of Chintaman Rao (supra), holding in favour of the worker.

47. In C. Dewan Mohideen Sahib & Sons v. Industrial Tribunal, AIR 196 SC 370, the Court examined the sample agreement that was produced before the Court in coming to the conclusion that the workers were employees of the contractors.

48. In Silver Jubilee Tailoring House Chief Inspector of Shops & Establishments [1974] 3 SCC 498, the question that arose was as to whether there was a relationship of employer and employee, between a tailoring shop and those employed by the owner of the shop for stitching. The provisions of Section 2(14) of the Andhra Pradesh (Telengana Area) Shops and Establishments Act, 1951 defined a person ’employed’ as in the case of a shop, a person wholly or principally employed therein in connection with the business of the shop.

49. The judgments of English and American Courts in Cassidy Ministry of Health [1951] 1 All ER 574 (CA), Montreal v. Montreal Locomotive Works Ltd. [1947] 1 DLR 161, Bank Voor Handel en Scheepvaart N.V. v. Slatford [1952] 2 All ER 956 , U.S. v. Silk (1947 SCC Online US SC 97, Market Investigations Ltd. v. Minister of Social Security [1969] 2 QB 173 were discussed.

50. In the aforesaid judgments, the Courts had looked into the test of control of the manner of work and in Cassidy’s case (supra), the Court pointed out that the test of control was not universal, pointing out there were many instances in contracts of services where the master cannot control the manner in which the work is to be done, such as in the case of a captain of a ship. Thus, to apply the test of control in the case of skilled employments to decide whether there is relationship of master-servant, would be unreal and would not result in a proper conclusion.

51. In the case of Montreal Locomotive Works Ltd. (supra), the Court felt that in complex business and industrial conditions one would have to apply a test involving control, ownership of the tools, risk of loss and other relevant tests.

52. In Slatford case (supra), the Court looked into whether the person concerned was ‘part and parcel of the organization’ and in the case of Silk (supra), the Court opined that the test was not merely the common law test of ‘power of control’ where the persons concerned could be said to be employees ‘as a matter of economic reality’.

53. The important considerations were degree of control, opportunities of profit or loss, investment in facilities, permanency of relations and the skill required to carry out the operations.

54. The question in Silver Jubilee Tailoring House (supra), was ultimately decided holding that the individuals were employees, since the equipment upon which they sewed were supplied by the shop and supervision was exercised by the employer, who had the right to reject substandard work.

55. In Hussainbhai Alath Factory Thozhilali Union [1978] 4 SCC 257, applying the test of economic reality of control of the employer over the workers’ subsistence, skill and continued employment, the question was answered holding that the persons were direct employees of the owner. The argument that they were only employed with the contractor and not the employer, was rejected.

56. Thus the question of whether there was ‘right of control’ by the employer would depend on the facts in each case and on the terms of the contracts between the parties.

57. In Indian Banks Assn. Workmen of Syndicate Bank [2001] 3 SCC 36 the deposit collectors employed by specific banks were held entitled to be treated as workmen. In General Manager, Indian Overseas Bank v. WorkmenAll India Overseas Bank Employees Union [2006] 3 SCC 729, the question that arose was whether the Bank who employed jewel appraisers were workmen for the purpose of Industrial Disputes Act. The terms of employment of regular employees and jewel appraisers were compared and the comparison is extracted below:

|

Regular employees |

|

| 1 | Subject to qualification and age prescribed |

| 2 | Recruitment through employment exchange/Banking Service Recruitment Board |

| 3 | Fixed working hours |

| 4 | Monthly wages. |

| 5 | Subject to disciplinary control |

| 6 | Control/supervision is exercised not only with regard to the allocation of work, but also the w carried out |

| 7 | Wages are paid by the Bank |

| 8 | Retirement age |

| 9 | Subject to transfer |

| 10 | While in employment cannot carry on any other occupation |

58. Based upon the comparison as above, the Court held that the jewel appraisers are not employees of the Bank. The English Court of Appeal in English Province of Our Lady of Charity 2013 QB 732, was concerned with the question as to whether the Roman Catholic Church would be vicariously liable in a claim brought for damages alleging that a lady, when resident in a children’s home operated by a Roman Catholic order of nuns, had been sexually abused by a priest.

59. The judgment made reference to several English judgments and the tests laid out therein to decide the question of ‘Hallmarks of the relationship of employer and employee’, referring inter alia to the four indicia of a contract of service being (a) The master’s power of selection of his servant; (b) the payment of wages or other remuneration; (c) the master’s right to control the method of doing the work; and (d) the master’s right of suspension or dismissal.

60. In Lee Ting Sang Chung Chi-Keung 1990 2 AC 374 (PC), the Court referred to the ‘fundamental’ test determined by Cooke, J in Market Investigations Ltd Minister of Social Security [1969] 2 QB 173, being’..is the person who has engaged himself to perform these services performing them as a person in business on his own account?’ If the answer was ‘yes’, then the contract is a contract for services. If the answer is ‘no’, then the contract is a contract of service.

61. After a detailed discussion of the above cases, the Apex Court, in the case of Sushilaben Indervandan Gandhi (supra), examined the contract between the deceased and R3 as follows:

34. Looked at in this light, let us now examine the agreement between Dr. Alpesh Gandhi and the Respondent No. 3. The factors which would lead to the contract being one for service may be enumerated as follows:

34.1 The heading of the contract itself states that it is a contract for service.

34.2 The designation of Dr. Gandhi is an Honorary Ophthalmic Surgeon.

34.3 INR 4000 per month is declared to be honorarium as opposed to salary.

34.4 In addition to INR 4000 per month, Dr. Gandhi is paid a percentage of the earnings of the Respondent No. 3 from out of the OPD, Operation Fee component of Hospitalization Bills, and Room Visiting Fees.

34.5 The arbitration clause which speaks of disputes arising in the course of the tenure of this contract will be referred to the Managing Committee of the Institute, the decision of the Managing Committee being final, is also a clause which is unusual in a pure master-servant relationship.

34.6 The fact that the appointment is contractual – for 3 years – and extendable only by mutual consent, is another pointer to the fact that the contract is for service, which is tenure based.

62. As against the above factors, the distinguishing factors noted were as follows: 34.7 The fact that termination of the contract can be by notice on either side would again show that the parties are dealing with each other more as equals than as master-servant.

34.8 Clause XI of the agreement also makes it clear that the earlier appointment that was made of Dr. Gandhi would cease the moment this contract comes into existence, Dr. Gandhi no longer remaining as a regular employee of the Institute.

35. As against the aforesaid factors which would point to the contract the contract being a contract for service, the following factors would point in the opposite direction:

35.1 The employment is full-time. Dr. Gandhi can do no other work, and apart from the seven types of work that Dr. Gandhi is to perform under clause IV, any other assignment that may get created in the course of time may also be assigned to him at the employer’s discretion.

35.2 Dr. Gandhi is to work on all days except weekly offs and holidays that are given to him by the employer. However, what is important is that though governed by the leave rules of the Institute as in vogue from time to time, Dr. Gandhi will not be entitled to any financial benefit of any kind as may be applicable to other regular employees of the Institute under clause V.

35.3 Dr. Gandhi will be governed by the Conduct Rules of the Institute as invoked from time to time and as applicable to regular employees of the Institute.

63. On balance, the Court held that factors that would render the contract, one for service, outweighed the facts pointing in the opposite direction, and concluded as follows:

36. If the aforesaid factors are weighed in the scales, it is clear that the factors which make the contract one for service outweigh the factors which would point in the opposite direction. First and foremost, the intention of the parties is to be gathered from the terms of the contract. The terms of the contract make it clear that the contract is one for service, and that with effect from the date on which the contract begins, Dr. Gandhi shall no longer remain as a regular employee of the Institute, making it clear that his services are now no longer as a regular employee but as an independent professional. Secondly, the remuneration is described as honorarium, and consistent with the position that Dr. Gandhi is an independent professional working in the Institute in his own right, he gets a share of the spoils as has been pointed out hereinabove. Thirdly, he enters into the agreement on equal terms as the agreement is for three years, extendable only by mutual consent of both the parties. Fourthly, his services cannot be terminated in the usual manner of the other regular employees of the Institute but are terminable on either side by notice. The fact that Dr. Gandhi will devote full-time attention to the Institute is the obverse side of piece-rated work which, as has been held in some of the judgments hereinabove, can yet amount to contracts of service, being a neutral factor. Likewise, the fact that Dr. Gandhi must devote his entire attention to the Institute would not necessarily lead to the conclusion that de hors all other factors the contract is one of service. Equally important is the fact that it is necessary to state Dr. Gandhi will be governed by the Conduct Rules and by the Leave Rules of the Institute, but by no other Rules. And even though the Leave Rules apply to Dr. Gandhi, since he is not a regular employee, he is not entitled to any financial benefit as might be applicable to other regular employees. Equally, arbitration of disputes between Dr. Gandhi and the Institute being referred to the Managing Committee of the Institute would show that they have entered into the contract not as master and servant but as employer and independent professional. A conspectus of all the above would certainly lead to the conclusion, applying the economic reality test, that the contract entered into between the parties is one between an Institute and an independent professional.

64. At paragraph 43, the Court summarised its findings as follows:

The question that arises before us is as to whether the expression “employment” is to be construed widely or narrowly – if widely construed, a person may be said to “employed” by an employer even if he is not a regular employee of the employer. However, the wider meaning that has been canvassed for by the insurance company cannot possibly be given, given the language immediately before, namely, “in the course of”, thereby indicating that the “employment” can only be that of a person regularly employed by the employer.

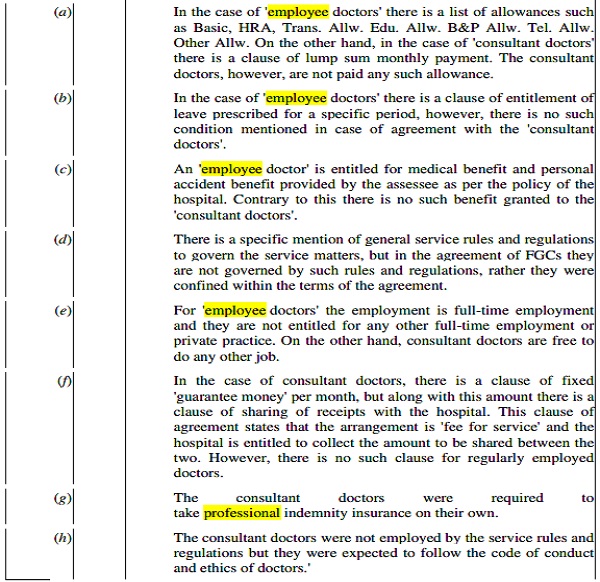

65. In the case of Escorts, the hospital had two categories of Doctors e. Employee Doctors and Retainer/Consultant Doctors. The terms were different from one category to another. The differences has been set out by way of a tabulation extracted below:—

| Sl. No | As per Agreement | Employee Doctors (Agreement @ pg 170) | Retainer/Consultant Doctors (Agreement @ pg 150) |

| 1 | Term | Whole time employment-not restricted for a fixed term | Fixed Term defined in agreement-renewable based on mutual consent |

| 2 | Remuneration | Salary plus following employment benefits:

– House Rent Allowance – Education Allowance – Special Allowance – Medical Reimbursement – Leave Travel assistance – Performance linked bonus |

Consolidated Retainership Fee |

| Also entitled to performance linked bonus | N.A. | ||

| Also entitled to Terminal benefits:

– Provident Fund – Gratuity |

N.A. | ||

| 3 | Exclusively | Doctors employed on whole-time basis with the Hospital- complete restriction on any other work for remuneration (part-time/full-time) in any other trade or business | Partly restricted-Doctors not to engage in employment with other hospitals; however, no restriction on private practice |

| 4 | Transfer/Posting | Transfer and posting of doctors at the sole discretion of the Hospital |

N.A. |

| 5 | Retirement | Retirement Age prescribed under the agreement @ 58 years | N.A. |

| 6 | Leave | Eligible for privilege, sick and casual leaves as applicable for respective category | N.A. |

| 7 | Intellectual Property rights | Any IPR developed by the doctor to be the sole property of the Hospital | N.A. |

| 8 | Insurance | N.A. | Professional Indemnity Insurance obtained by Doctors on their own account @ pg. 135 |

| 9 | ITR | Remuneration treated as ‘Salary’ by Doctors | Remuneration treated as ‘Professional Fee’ by Doctors @ pgs.143 & 146 |

66. The question that arose was, as regards the taxability of the remuneration paid to the Retainer Doctors, whether salary or income from profession. Upon going through the differences in the terms governing the two categories of Doctors, the High Court allowed the appeal of the hospital holding the same to be an exercise of profession. What weighed substantially with the Court was the absence of control exercised by the hospital.

67. On the aspect of ‘consultancy’ by the professionals, the Court stated thus:

’15. ‘Consultancy charges’ in the ordinary sense means providing of expert knowledge to a third party for a fee. It is a service provided by a professional advisor. These consultant Doctors are rendering professional services as and when they are called upon to attend the patients.

Profession implies any vocation carried by an individual or a group of individuals requiring predominantly intellectual skill, depending on individual characteristic of person(s) pursuing with the vocation, requiring specialized and advance education or expertise. Consultancy charges are paid to the Doctors towards rendering their professional skill and expertise which are purely in the nature of professional charges. Assessee Company has no control over the Doctors engaged by them with regard to treatment of patients.

16. Mere providing of non-competition clause in the agreement shall not invalidate the nature of profession. It is common that the doctors are rendering their professional services as visiting doctors in different hospitals. Imposing a condition of bar to private practice is to make use of the expertise, skill of a doctor exclusively to the assessee-company i.e., to get the attention and focus of the professional skill and expertise only to the patients of the assessee-company and to discourage doctors from transferring patients to their own clinics or any other hospital. This condition imposed by the assessee-company would not alter the nature of professional service rendered by the doctors. Tribunal also held that none of the doctors are entitled to gratuity, PF, LTA and other terminal benefits. Considering all these aspects at length a detailed, well reasoned order is passed by the Tribunal on this issue which we may not find fault with.’

Several other judgments were also discussed, many that find reference in the judgment of the Supreme Court in Sushilaben’s Indravandan Gandhi’s case (supra).

68. The Gujarat High Court in Apollo Hospital International Ltd.’s case (supra), considered the nature of remittances made to full-time resident Doctors in Apollo Hospital International Limited. Professional Tax and Provident Fund were being

The conclusion of the Tribunal to the effect that the income of the Consultant Doctors should be treated as professional income was confirmed.

69. In the case of Grant Medical Foundation (supra), the Bombay High Court also considered a similar case involving two categories of doctors. Neither category was entitled to provident fund or terminal benefits. Both categories were free to carry on private practice, but the private patients were to be treated only from the premises of the assessee hospital. There was a difference in the manner of remuneration as well, fixed in the case of the full-time doctors and variable in the case of the consultants.

70. The Bench also noticed the insistence of that hospital management, that facilities provided for investigation, consultation and diagnostics be utilised to the optimum. As regards the incorporation of fixed timings and hours, the Bench opined that such regulations were only a measure of ensuring that the medical practitioner was obliged to devote time and energy wholeheartedly to the hospital.

71. In conclusion, the issue was decided in favour of the hospital, the Court clarifying that their concurrence did not mean that professionals could never be employees or that there could never be a master-servant relationship in the case of a professional. Such a finding would depend upon the attending facts and circumstances, terms and conditions of engagement and on an examination on a case-to-case basis.

72. In the case of CIT (TDS) IVY Health and Life Sciences (P) Ltd., [2015] 63 taxmann.com 362/[2016] 236 Taxman 292/380 ITR 342, the Punjab and Haryana High Court considered the taxability of payments to doctors falling within a single category, and who worked on fixed timings. The doctors were not entitled to private practice, attended the hospitals on call and received a fixed salary. They are not entitled for Leave Travel concession, concession in medical treatment of relatives, Provident Fund, Leave Encashment, Retirement benefits such as gratuity and are subject to the rules and regulations of the hospitals.

73. The terms read as follows:

’16.Additionally, we may notice the terms of the agreement on the basis of which the Assessing Officer had issued show cause notice to the assessee which read thus:—

“(i) The second party shall be associated exclusively with M/s.IVY Hospital as full-time consultant and shall not associate himself with any other hospital.

(ii) the second party shall be paid professional charges for services rendered by him in IVY Hospital as under with a minimum guarantee of Rs. ..per month subject to TDS deductions as per Act, the minimum guarantee amount shall be paid to the second party for a period of 12 months from the date of joining. The same shall be revised at the end of 12 months.

| (a) | 70% of the OPD charges | |

| (b) | Visiting charges in ward/private room as mutually settled between the two parties. | |

| (c) | 15% of the investigation done of IVY Hospital. |

(iii) the second party shall not do practice at any other place and would be associated exclusively with IVY hospital. The second party shall not operate or admit patient in any other hospital except at IVY Hospital.”‘

Considering the above, the stand of the assessee was accepted.

74. In Manipal Health Systems (P) Ltd., (supra), the Karnataka High Court considered and applied the ‘intention test’ to decide in favour of the assessee, noting that the income of the Doctor was variable and concluding that there was no employee and employer relationship between the parties.

75. The Andhra Pradesh High Court, in Yashoda Super Speciality Hospital (supra), by way of a short judgment accepted the case of the Doctors. They also concluded that the embargo placed upon private practice would not change the basic character of the relationship between the doctor and the hospital. An agreement is expected to contain both prohibitory as well as facilitatory clauses, and must be read as a whole, and in balance.

76. The overwhelming precedent is thus in favour of the doctor/hospitals, and I note close identity in the agreement before me with those in the aforesaid cases. All petitioners before me hold specialisations in different fields of medicine and a tabulation of their specialisations is set out below:

| S.No. | W.P.No. | CONSULTANT |

| 1. | 15268 of 2022 | Anaesthesiologist |

| 2. | 14592 of 2022 | Anaesthetist |

| 3. | 15289 of 2022 | Nephrologist |

| 4. | 15304 of 2022 | Dental Surgeon |

| 5. | 12692 of 2022 | Neuro and Cardiovascular Radiologist |

| 6. | 15079 of 2022 | Dermatologist |

| 7. | 14810 of 2022 | Pulmonologist |

| 8. | 14829 of 2022 | Anaesthetist |

| 9. | 14897 of 2022 | Urologist |

| 10. | 14993 of 2022 | Radiologist |

| 11. | 14979 of 2022 | Radiologist |

| 12. | 15082 of 2022 | Physician |

| 13. | 15084 of 2022 | Transfusion Medicine |

| 14. | 15281 of 2022 | General and Laparoscopic

Surgeon |

| 15. | 15276 of 2022 | Paediatrician and

Neonatologist |

| 16. | 14515 of 2022 | Oncologist |

| 17. | 15317 of 2022 | General Surgery |

| 18. | 15365 of 2022 | Gastroenterologist |

| 19. | 15386 of 2022 | Cardiac Anaesthesia |

| 20. | 15452 of 2022 | Orthopaedic Surgeon |

| 21. | 15448 of 2022 | Orthopaedic Surgeon |

| 22. | 15458 of 2022 | Plastic Surgeon |

| 23. | 15721 of 2022 | Internal Medicine |

| 24. | 15995 of 2022 | Intensivist |

| 25. | 19632 of 2022 | Head of Critical Care

Department |

| 26. | 19637 of 2022 | Critical Care Medicine |

| 27. | 19634 of 2022 | Intensivist |

| 28. | 15384 of 2022 | Radiologist |

| 29. | 15455 of 2022 | Psychiatrist |

| 30. | 15388 of 2022 | Neurologist |

| 31. | 14833 of 2022 | Neuro Surgeon and Spine |

77. The agreements in the present cases reveal the following terms:

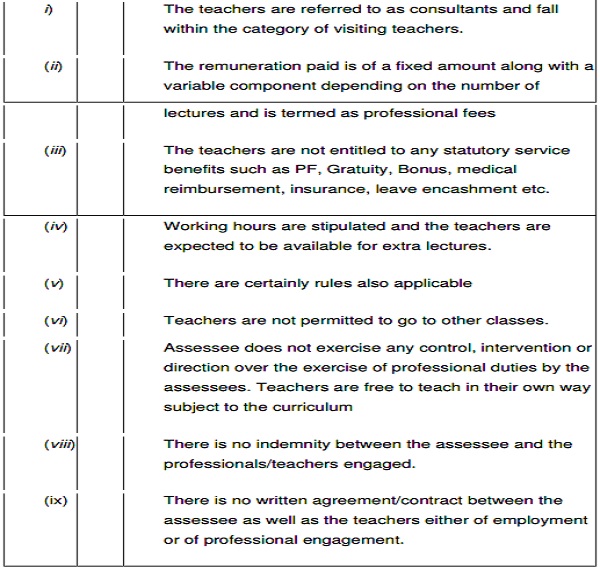

| (i) | The doctors are referred to as consultants and fall within the | |

| category of visiting consultants/full-time consultants, as against part-time and special category consultants who also attend the hospital. | ||

| (ii) | The remuneration paid is of a fixed amount along with a variable component depending on the number of patients treated, and is termed as ‘salary’. | |

| (iii) | The consultants are not entitled to any statutory service benefits such as PF, Gratuity, Bonus, medical reimbursement, insurance, leave encashment etc. | |

| (iv) | Working hours are stipulated as 8 a m to 5 p m and the consultants are expected to be available on call in the night. | |

| (v) | They are permitted a month’s vacation and leave on a case-to-case basis and depending on need. | |

| (vi) | Private practice is permitted in the case of both categories, upon the satisfaction of certain conditions, such as service of 2 years in the hospital and other conditions extracted as part of the impugned order at paragraph 12 above. | |

| (vii) | The hospital does not exercise any control, intervention or direction over the exercise of professional duties by the petitioners. | |

| (viii) | The petitioners are wholly responsible for professional indemnity insurance and the hospital does not indemnify the doctors from any manner of claims. |

78. The intention of the parties appears to engage in a relationship of equals. The hospital, on the one hand, and the professional, on the other, engage in a relationship where the former provides the administrative infrastructure and facilities and the latter, the professional skill and expertise to result in a mutual rewarding result.

79. Then again, the fact that the remuneration paid is variable, and the doctors are not entitled for any statutory benefits also points to the absence of an employer-employee relationship. The mere presence of rules and regulations do not, in my considered view, lead to a conclusion of a contract of service. Rules and regulations are necessary to ensure that the workplace functions in a streamlined and disciplined fashion. Thus, mere existence of an agreement that indicates some measure of regulation of the service of the doctors, cannot lead to a conclusion that they are salaried employees.

17. Thus respectfully following the decision of the honourable madras High Court and in view of the above facts it is clear that the above decision of the honourable madras High Court squarely covered the issue in favour of the assessee holding that where the identical terms and conditions, these teachers could not be held to be the employees of the assessee and tax deduction at source could have been forced under section 192 of the act. Therefore we do not find any infirmity in assessee treating them as professional and deducting tax at source on their payment under section 194J of the act.

18. Accordingly the order passed by the learned AO under section 201 (1)/201 (1A) treating the assessee as assessee in default for short deduction of tax at source holding that the salary payment is made by the assessee to all these teachers rejecting the claim of the assessee that those consultant where taxes deducted at source under section 194J of the act and Order of the ld CIT (A) confirming the same are not sustainable and hence quashed.

19. In the result appeal filed by the assessee is allowed.

20. Stay petition is dismissed as infructuous.

Order pronounced in the open court on 16th June, 2026.

Author Bio