Case Law Details

Smapath Raj Sunil Kumar Jain Vs DCIT (ITAT Hyderabad)

The Income Tax Appellate Tribunal (ITAT), Hyderabad, dismissed the assessee’s appeal and upheld the addition of ₹3.75 crore made on account of unexplained excess stock of gold found during a survey under Section 133A of the Income-tax Act. The Tribunal held that unsupported gold deposit agreements produced after the survey, along with subsequent payment of interest to alleged depositors, were insufficient to explain the excess stock discovered during the survey.

The assessee, proprietor of a jewellery business, was subjected to a survey on 11.03.2020. During the survey, physical gold stock of 44,882.656 grams was found against book stock of 26,497.255 grams, resulting in excess physical stock of 18,385.401 grams. The assessee initially stated that the stock required reconciliation because ornaments contained stones and other metals and were not of 24-carat purity. However, considering the discrepancies, he voluntarily offered additional income of ₹5 crore during the survey. Subsequently, while filing the return of income, the assessee offered only ₹1.25 crore, claiming that 13,613 grams of the excess stock represented gold received from 15 persons under “gold deposit agreements.”

The Assessing Officer rejected the explanation, observing that the gold deposit agreements appeared to be an afterthought. Most agreements were executed on the same day in February 2020, were not produced during the survey, and there was no evidence that such a gold deposit practice had existed in earlier years. The AO also noted that the assessee had himself valued the excess stock during the survey and therefore rejected the argument that valuation by a registered valuer was necessary. Accordingly, the AO added the balance amount of ₹3.75 crore, being the difference between the ₹5 crore offered during the survey and the ₹1.25 crore disclosed in the return. The Commissioner (Appeals) confirmed the addition after holding that the gold deposit agreements were unsupported by contemporaneous evidence and failed to establish the genuineness of the claimed deposits.

Before the Tribunal, the assessee argued that the addition was based solely on the survey statement, which had been validly retracted, and relied on the Supreme Court decision in CIT v. S. Khader Khan Son and CBDT instructions discouraging reliance on confessional statements obtained during surveys. The assessee also contended that the reconciliation supported by agreements from 15 depositors, their identities, and subsequent payment of interest established the genuineness of the transactions. It was further argued that the Department ignored the issues relating to embedded stones, varying purity of gold ornaments, and the absence of valuation by a registered valuer.

The Tribunal observed that there was no dispute regarding the existence of excess physical stock of 18,385.401 grams. It noted that the assessee had initially admitted the discrepancy and later sought to explain 13,613 grams through gold deposit agreements produced nearly two years after the survey. The Tribunal found that no such agreements were discovered during the survey, no corresponding entries existed in the books of account on the survey date, and the assessee failed to establish that any similar gold deposit scheme had been followed in earlier years. It held that merely filing agreements, affidavits, and evidence of subsequent payment of interest did not establish the genuineness of the claimed gold deposits.

Addressing the reliance on Khader Khan Son and CBDT Circulars, the Tribunal held that the principles laid down in those authorities apply where additions are based solely on statements recorded during a survey. In the present case, however, the addition was supported by corroborative evidence in the form of unexplained excess physical stock found during the survey. Therefore, the addition was not based merely on the survey statement but on tangible evidence coupled with the assessee’s failure to provide a satisfactory explanation. The Tribunal concluded that the Assessing Officer had rightly made the addition of ₹3.75 crore, the Commissioner (Appeals) had correctly confirmed it, and no interference was warranted. Accordingly, the appeal filed by the assessee was dismissed.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

This appeal filed by the assessee is directed against the order of the Commissioner of Income Tax (Appeals), Visakhapatnam-3, dated 10.12.2025, and pertains to assessment year 2020-21.

2. The assessee has raised the following grounds of appeal:

1. The order of the learned Commissioner of Income-tax (Appeals) is bad in law, contrary to facts and unsustainable, and is liable to be set aside. The learned CIT(A) erred in confirming the addition of Rs. 3,75,00,000/- made by the Assessing Officer on account of alleged excess stock, without appreciating the facts, evidence and explanations placed on record by the appellant

2. The authorities below erred in relying upon the statement recorded during survey under section 133A, ignoring the fact that such statements have no evidentiary value in law and that the appellant had validly and promptly retracted the same. The learned CIT(A) failed to appreciate that no addition can be made solely on the basis of a survey statement, without any corroborative material OR evidence, as laid down by the Hon’ble Supreme Court in CIT v. S. Khader Khan Son.

3. The learned CIT(A) erred in upholding the rejection of the stock reconciliation and gold deposit agreements submitted by the appellant, without bringing any material on record to disprove the genuineness of the said evidences.

4. The authorities below erred in making the addition without obtaining any valuation of stock by a registered valuer, and the alleged excess stock was determined on estimation and conjectures, which is not permissible in law.

5. The CIT(A) erred in disregarding the CBDT Circular F.No.286/2/2003 IT(Inv.) dated10.03.2003 and Instruction F.No.286/98/2013 IT(Inv.II) dated 12.12.2014, which clearly direct that confessions during survey without supporting evidence should not be relied upon.

6. The learned CIT(A) erred in sustaining a high-pitched assessment, ignoring the fact that the appellant is a tax-audited assessee with regularly maintained books of account and no defects were pointed out therein. The addition of Rs.3,75,00,000/- is arbitrary, excessive and based on surmises and conjectures, and therefore liable to be deleted.

7. The learned CIT(A) erred in confirming the levy of consequential interest and initiation of penalty proceedings, which are purely consequential and unsustainable once the addition itself is deleted.

8. The appellant craves leave to add, alter, amend OR withdraw any of the above grounds at the time of hearing of the appeal.

3. The brief facts of the case are that the assessee, Shri Sampath Raj Sunil Kumar, Proprietor of M/s. Sunil Jewellers is engaged in the business trading in jewellery and gold filed his return of income (RoI) for AY 202021 on 31.03.2021 admitting total income of Rs.2,57,58,180/-. In this case, a survey u/s.133A of the Income Tax Act, 1961 was conducted on 11.03.2020. During the course of survey, physical inventory of stock of gold has been taken and compared with stock available as per the books inventory which resulted in excess physical stock of 18385.401 grams. During the course of survey, a sworn statement was recorded from the assessee on 11.03.2020 and he was asked to explain excess physical stock found during the course of survey, for which, the assessee arrived at net closing book stock as on 11.03.2020 26,497.255 grams. Once again, the assessee was asked to clarify the difference between physical stock which was at 44,882.656 grams as against the book stock at 26,497.255 grams. The assessee admitted that there is a difference of excess physical stock 18,385.401 grams. However, stated that the same needs to be reconciled and arrived at correct stock figures. Further, there are stones and other materials embedded in gold ornaments which need to be removed and also the purity is not ’24’ carat but its purity is ’18’ carat or 916 KDM. However, considering the fact that, there are certain discrepancies in the stock, offered additional income of Rs.5 Crs. over and above the regular income for AY 2020-21. Subsequently, during post survey enquiry, the assessee has furnished reconciliation along with books of accounts and claimed that he has received ‘gold deposit agreements’ from ’15’ customers/interested parties and received gold ornaments to the tune of 13,613 grams and in respect of balance quantity, offered additional income of Rs.1.20 Crs and disclosed in return of income filed for the year under consideration.

4. The case was selected for scrutiny and during the course of assessement proceedings, the AO noticed that the assessee has retracted his deposition made on 11.03.2020 with regard to voluntary offerings of additional income of Rs.5 Crs. and therefore, called upon the assessee to file relevant reconciliation, explaining excess physical stock found during the course of survey. In response, the assessee submitted reconciliation and claimed that, he has received gold deposit of 13,613 grams from ’15’ customers, for which, the assessee has furnished agreements from the parties indicating the quantity of gold ornaments received from them and claimed that the unreconciled value of Rs.1.25 Crs. has been offered to tax and paid relevant tax.

5. The AO after considering the relevant submissions of the assessee and also by taking note of physical stock found during the course of survey observed that, the subsequent retraction of deposition given by the assessee along with ‘gold deposit agreements’ claimed to have been entered into with ’15’ persons is only an afterthought but has not any substance going by the agreements entered into with various persons in a single day i.e. on 12.02.2020. The AO further noted that, at the time of survey, assessee has not been able to explain excess stock found during the course of survey and also admitted additional income by noticing the discrepancy, however, the subsequent argument that he has received 13,613 grams from ’15’ persons is only an afterthought without any valid evidences. The AO further noted that the assessee neither furnished ‘gold deposit agreements’ at the time of survey nor proved that this practice had existed in the earlier Financial Years also. The AO had also rejected the arguments of the assessee for valuation of gold jewelry and observed that the assessee himself has arrived at value of excess stock found during the course of survey and therefore, observed that without proper valuation, addition can’t be made is also incorrect. Therefore, rejected the arguments of the assessee and made addition of Rs.3.75 Crs. Towards additional income offered during the course of survey but not admitted in return of income (RoI) filed by the assessee. The relevant observations of the AO are as under:

5. However, during the course of assessment proceedings, the assessee has retracted his deposition made on 11.03.2020 as above. With regard to excess stock found and offer of additional income of Rs.5 crores, the assessee has stated that ” voluntary offer of additional income of Rs.5 crs to buy peace with the department is not correct as there is a clear reconciliation of physical stock and the valuation of stock was also not valued properly, hence the figures arrived at 4.00 am by the department in sworn statement is contradictory and not tenable as the closing stock arrived in between the financial year without reconciliation is not permitted in law and spirit”.

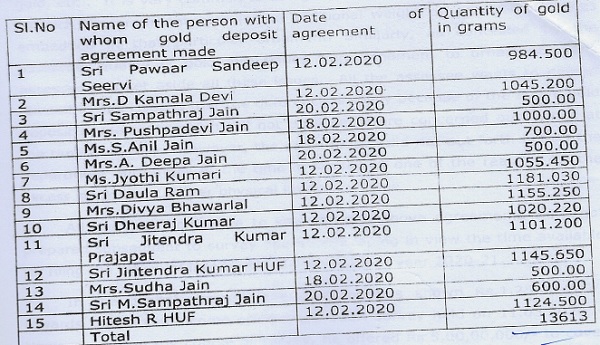

5.1 In this regard, the assessee has furnished gold deposit agreements from 15 customers / interested parties, the details of which are as under :

From the above, it can be seen that all the agreements have been made in the month of February, 2020. Further, majority of agreements have been made in a single day i.e. on 12.02.2020. As the survey was conducted on 11.03.2020 and last date for filing the return of income for the assessment year 2020-21 was sufficiently available at his disposal, the assessee has enough time to fabricate all the above agreements.

5.2 In the sworn statement, the assessee had deposed that “, there are stones and other metals embedded in the gold ornaments which needs to be removed from the gross weight before arriving at the net weight. Further, the purity of gold is not 24 carat. They consist of 18 carat and 916 gold. The URD gold is also not of pure gold and suffers from alloy mix.”. In this regard, the assessee has not contested even for a single gram of gold that was excess calculated on account of stones embedded in gold ornaments, quality of gold, etc. It is very common to use gold ornaments embedded with stones as such the ornament gains some additional weight on account of stones embedded in that particular ornament. Similarly, as contested by the assessee, quality of gold also varies from ornament to ornament. The assessee has set aside all these issues. All the assessee wants to defend himself in this issue is that the difference is solely because of the above gold deposit agreements which did not produce before concerned authorities at the time of survey. However, the same reason did not put forth before the department authorities at the time of survey as one of the reasons for the excess stock found as per physical inventory made.

6. All the facts contribute to say that the above agreements were got prepared subsequent to survey operation keeping in view the time available for filing the return of income for the assessment year 2020-21.

In the capital account, the assessee has shown Rs.1,25,00,000/-towards “additional income offered u/s 133A survey held on 11.03.2020” However, during the course of survey, he offered Rs.5,00,00,000/- to cover up the discrepancies in the excess stock found. Therefore, the difference of Rs.3,75,00,000 (Rs.5,00,00,000 minus Rs. 1,25,00,000) has been added to the income returned.

6. Aggrieved by the assessement order, the assessee preferred an appeal before the Ld.CIT(A). Before CIT(A), the assessee has reiterated his arguments made before the AO and submitted that the AO made addition towards difference in value of physical stock found during the course of survey without proper valuation of jewellery and by removing stones and other metals embedded in the jewellery and also considering the purity of gold ornaments. The assessee further submitted that the AO ignored reconciliation submitted by the assessee in light of ‘gold deposit agreements’ entered into with ’15’ persons in respect of 13,613 grams of gold ornaments. The assessee further submitted that additions can’t be made purely on the survey statement without any corroborative evidence. In this regard, relied upon the decision of the Hon’ble Supreme Court in the case of CIT v. S Khader Khan Son reported in [2012] 254 CTR 228 (SC).

7. The Ld.CIT(A) after considering the relevant submissions of the assessee and also taken note of reasons given by the AO to make additions towards additional income offered during the course of survey but not admitted in the RoI observed that, there is no dispute with regard to the fact that during the course of survey excess stock to the tune of 18,385.401 grams of gold was found, for which, there was no explanation from the assessee. It is also an admitted fact that the assessee voluntarily admitted additional income of Rs.5 Crs. in respect of excess stock found during the course of survey. However, the subsequent arguments of the assessee that after reconciliation, he is able to identify 13,613 grams of gold towards ‘gold deposit agreements’ entered into with `15′ persons is only an afterthought without any evidences. Further, the assessee had also failed to prove the existence of ‘gold deposit agreements’ in the earlier Financial Years. In the absence of any explanation with regard to genuineness of ‘gold deposit agreements’, the AO has rightly rejected the explanation of the assessee and made additions towards additional income offered during the course of survey in respect of excess stock found in respect of gold ornaments. Therefore, rejected the explanation of the assessee and sustained the additions made by the AO. The relevant findings of the Ld.CIT(A) are as under:

6. DECISION:

6.1 I have carefully examined the assessment order, the written submissions filed through ITBA and the detailed arguments advanced by Sri K.P. Gangi Reddy, Chartered Accountant and learned Authorised Representative of the appellant. The learned AR placed reliance on CBDT Circulars on retraction, the decision of the Hon’ble Supreme Court in CIT v. S. Khader Khan Son, 254 CTR 228 (SC), and many judicial precedents to contend that no addition can be made based solely on a survey admission. The AR further argued that (i) the admission stood retracted, (ii) the AO failed to value the gold through a registered valuer, (iii) the AO ignored the 15 gold depositors through whom 13.613 kg was allegedly explained, and (iv) the AO did not invoke any specific provision while making the addition. All submissions and judicial precedents relied upon by him have been duly considered.

6.2 The factual position emerging from the records is as follows. A survey u/s 133A was conducted on 11-03-2020 at the appellant’s premises where physical stock of 44,882.656 grams was inventoried as against book stock of 26,497.255 grams, resulting in an excess stock of 18,385.401 grams. During survey, the appellant stated that owing to presence of embedded stones and other metals, varying purity of gold in different ornaments the net weight would be from the gross weight. However, considering the stock discrepancies, he offered Rs. 5 crores as additional income.

During assessment proceedings, in response to notice u/s 142(1), the appellant submitted a fresh reconciliation (point 9), attributing 13.613 kg of the excess stock to gold deposited by 15 individuals as “Loan Gold included in physical stock” and offered the balance of 4772 grams as income. The AO, after examining the agreements produced in support of “Loan Gold”, found them to be created post-survey, unsupported by books or contemporaneous evidence, and accordingly treated the balance Rs. 3.75 crore as unexplained investment in excess stock.

6.3 Although the appellant has as many as 14 grounds, they ultimately converge on a few core objections which require adjudication. The first is that the addition cannot survive because the admission made during survey was later retracted, and therefore no reliance can be placed on it. The second objection concerns the absence of valuation by a registered valuer, which according to the appellant renders the survey figures unreliable. The third and most substantial contention is that the excess stock stood explained through the Gold Deposit Scheme involving 15 individuals who contributed 13.613 kg before the survey. Though not mentioned in the original grounds, the Ld AR through written submissions and oral arguments contended that the assessment is vitiated because the Assessing Officer has not expressly invoked the specific statutory provision under which the addition is made. These objections form the crux of the dispute and are discussed in the following paragraphs.

6.4 At the outset, it is a crucial and undisputed fact that 18,385.401 grams of excess gold existed at the time of survey. The appellant has never disputed the quantitative difference either during survey or during assessment. The voluntary disclosure made during survey and the subsequent attempt to explain the difference through 15 depositors both acknowledge the existence of excess physical stock. Therefore, the argument that the addition is based on “mere admission” is factually incorrect. Even without the admission, the existence of undisclosed stock is a primary incriminating fact, permitting the AO to invoke section 69B.

Once this foundational fact is established, the narrative naturally shifts to whether the explanation offered-i.e., the Gold Deposit Scheme-is credible. During survey, when specifically questioned about sources such as URD gold, customers’ gold or personal gold, not a single mention was made about any gold loan depositors. Even examination of financial statements filed during appeal proceedings shows that no such scheme existed prior to February 2020 or after February 2020. The loan agreements-submitted only during assessment almost after two years of survey-are identically drafted, executed on three days (12-02-2020, 18-02-2020 and 20-02-2020), and was absent in the books on the date of survey. No depositor was produced; no confirmations were filed; no proof of delivery of gold was furnished during the course of survey except for the self-serving agreements during assessment. These factors cumulatively indicate that the explanation is an afterthought.

The conduct of the appellant also fails the tests laid down by the Hon’ble Supreme Court in Sumati Dayal v. CIT, 214 ITR 801 (SC), and CIT v. Durga Prasad More, 82 ITR 540 (SC), which require the Assessing Authority to apply the test of human probabilities. A sudden influx of 13.6 kg of gold from 15 persons within nine days, for a scheme never heard of before or after, without a single entry in books on the date of survey, is inconsistent with human conduct and business probabilities. This finding is further supported by Samaddar Brothers vs. Commissioner of Income-tax [2023] 148 taxmann.com 453 (Calcutta)/[2023] 292 Taxman 323 (Calcutta) [13-02-2023], where explanations created post-survey were rejected, and Pavankumar M. Sanghvi vs. Income-tax Officer [2018] 97 taxmann.com 398 (SC)/[2018] 258 Taxman 160 (SC) [01-05-2018] (SLP dismissed), where post-survey documents were held unreliable. Similarly, Commissioner of Income-tax vs. Kuwer Fibers (P.) Ltd. [2017] 77 taxmann.com 345 (Delhi) [20-10-2016] and Neeraj Agrawal vs. Deputy Commissioner of Income-tax [2023] 152 taxmann.com 632 (Allahabad – Trib.)/[2023] 103 ITR(T) 398 (Allahabad – Trib.) [14-03-2023] held that explanations not supported by books cannot be accepted. These apply directly to the present facts.

Accordingly, the first two limbs of the appellant’s arguments-retraction and valuer-stand answered. The retraction becomes irrelevant once the appellant himself accepts excess stock and attempts to explain it through depositors. The valuer objection is misplaced because the issue pertains to quantity, not to the value of the ornaments.

6.5 The appellant’s reliance on CIT v. S. Khader Khan Son, 254 CTR 228 (SC), is misplaced. The present addition is not based on the survey admission but on the undisputed physical excess stock. The ratio in Khader Khan applies only where an addition is made solely on the basis of a survey statement without corroboration. In the present case, the addition is founded on a tangible, quantified discrepancy, with the appellant’s explanation found unsatisfactory. Once the appellant chose to furnish a reconciliation in response to notice of the AO under section 142(1), the retraction ceased to have any consequence.

6.6 As regards the argument that the AO did not invoke a specific section, the nature of the addition clearly corresponds to section 69B, and it is well-settled that omission to mention the precise section does not vitiate the assessment when the factual foundation is clear.

6.7 Having considered all submissions, documents and case law, I hold that the appellant has failed to discharge the burden of explaining stock difference of 13.613kg gold and the genuineness of the claimed 15 gold depositors is unsupported by contemporaneous evidence, not reflected in books, inconsistent with the conduct at the time of survey, contrary to normal business practices, and fails the tests of human probabilities as laid down in Sumati Dayal and Durga Prasad More. Payment of interest to such claimed deopositors and deducting TDS on such interest subsequently would not make the unexplained admitted excess stock explained. Accordingly, the addition of Rs. 3,75,00,000 is confirmed and the related grounds are dismissed.

8. Aggrieved by the order of Id. CIT(A), the assessee is now in appeal before the Tribunal.

9. The Ld. Counsel for the assessee submitted that the Ld.CIT(A) erred in sustaining the additions made by the AO towards additional income offered during the course of survey for Rs.3.75 Crs. without appreciating the fact that the assessee has reconciled the excess stock by filing relevant details including ‘gold deposit agreements’ from ’15’ persons along with their identity towards genuineness and creditworthiness. The Ld. Counsel for the assessee further submitted that the addition can’t be made solely on the basis of survey statement as held by the plethora of judicial precedents, including the decision of the Hon’ble Supreme Court in the case of Khader Khan Son (supra). In the present case, the AO made addition only on the basis of survey statement without considering the reconciliation filed by the assessee along with evidences. The assessee has furnished relevant ‘gold deposit agreements and also filed particulars of those parties. Further, the assessee has also paid interest on gold loans taken from ’15’ persons in the subsequent Financial Years. Therefore, the AO ought to have accepted the explanation of the assessee and not made addition towards difference amount only on the basis of survey statement.

10. The Ld. Counsel for the assessee further submitted that the AO had not even considered the arguments of the assessee right from the beginning including from the date of survey where assessee has made a clear statement for incorrect valuation of gold by the AO. Further, the AO ignored arguments of the assessee and taken value of gold at ’24’ carat purity, even though, the assessee claimed that the gold ornaments found during the course of survey contain stones and other metals and also purity of gold was not ’24’ carat but ’18’ carat and 916 KDM category. The Ld. Counsel for the assessee submitted that the CBDT vide Circular F.No.286/2/2003-IT(Inv) dated 10.03.2003 specifically directed officers to not obtain confession during search/survey proceedings without supporting evidence. In the present case, the AO had taken confession statement from the assessee and by ignoring retraction filed by the assessee has made addition without any supporting evidence. Therefore, he submitted that the additions made by the AO should be deleted.

11. The Ld.SR-AR for Revenue, on the other hand, supporting the order of the Ld.CIT(A) submitted that there is no dispute with regard to the fact that there was excess physical stock of gold ornaments to the tune of 18,385.401 grams and the assessee has failed to explain the excess stock found during the course of survey. It is also an admitted fact that the assessee had voluntarily admitted additional income of Rs.5 Crs. but to cover up various discrepancies including excess stock found during the course of survey. Further, subsequent retraction of deposition in light of ‘gold deposit agreements’ from ’15’ persons is only an afterthought without any supporting evidences. Further, the assessee has failed to prove existence of such claim either in the previous Financial Year or in the subsequent Financial Years. Therefore, the explanation offered by the assessee in respect of 13,613 grams of gold in light of ‘gold deposit agreements’ after a period of two years from the date of survey can’t be accepted. Further, the AO has not made addition only on the basis of statement recorded from the assessee and it is further supported by the excess stock found during the course of survey which is clear evidence of undisclosed income of the assessee. The AO and the Ld.CIT(A) after considering relevant facts has rightly sustained the additions made by the AO, and therefore, he submitted that the additions made by the AO and sustained by the Ld.CIT(A) should be upheld.

12. We have heard both the parties, perused the materials available on record and had gone through orders of the authorities below. There is no dispute with regard to the fact that during the course of survey u/s.133A of the Act on 11.03.2020, excess physical stock of gold ornaments to the tune of 18,385.401 grams was found which couldn’t be explained by the assessee with relevant details. In fact, the department found at the business premise of the assessee, physical stock of 44,882.656 grams of gold as against the book stock of 26,497.255 grams, resulting into difference of excess physical stock 18,385.401 grams and the same was not explained by the assessee. Although, the assessee claimed that the same needs to be reconciled and arrived at correct stock figures by removing metals and stones embedded in the gold ornaments, by considering the purity of gold is not ’24’ carat, but the assessee voluntarily admitted additional income of Rs.5 Crs. to buy peace and to end protracted litigation with the Department. Further, while filing RoI for the year under consideration, the assessee had only admitted additional income of Rs.1.25 Crs. towards excess stock found during the course of survey and claimed that the remaining balance of Rs.3.75 Crs. in respect of 13,613 grams of gold was reconciled in light of ‘gold deposit agreements’ with ’15’ persons/interested persons. Therefore, it is necessary for us to examine the reasons given by the AO to make addition of Rs.3.75 Crs. towards additional income offered during the course of survey but not admitted in the RoI, in light of above facts.

13. Admittedly, the assessee has not disputed excess stock of 18,385.401 grams of gold, when compared to physical stock and book stock. It is also an admitted fact that the assessee couldn’t explain the difference and offered additional income of Rs.5 Crs. over and above the regular income for the Financial Year 2019-20 relevant to AY 2020-21. However, the assessee came out with a new explanation and claimed that after reconciliation, he found that 13,613 grams of gold pertains to ‘gold deposit agreements’ entered into with ’15’ persons and the same should be excluded or considered while arriving at excess tock found during the course of survey. To support this argument, the assessee filed affidavit of 15 parties along with agreements and claimed that they have deposited gold ornaments with them, for which, the assessee has paid interest in the subsequent Financial Year. We find that the assessee has taken this argument for the first time nearly two years after the date of survey that too at the time of assessement proceedings. Further, at the time of survey, there was no such agreement found by the Department, nor the assessee has furnished any agreements to explain the excess stock found during the course of survey. There was no entry in the books of accounts maintained by the assessee for his business with respect to gold loan agreements. Further, the assessee has not filed any proof to establish that similar scheme had existed in the past. Therefore, in our considered view, in the absence of any proper explanation with regard to ‘gold deposit agreements merely by filing agreements along with affidavit, the explanation offered by the assessee for 13,613 grams of gold can’t be accepted. In our considered view, mere payment of interest in the subsequent Financial Year doesn’t prove the genuineness of gold deposit agreement entered into by the assessee with above parties. Since the assessee has not made this claim at the time of survey and also the ‘gold deposit agreements’ are not supported by further evidences, in our considered view, reconciliation filed by the assessee for explaining 13,613 grams of gold can’t be accepted. Therefore, in our considered view, the explanation of the assessee for explaining 13613 gms of gold jewellery cannot be accepted.

14. Having said so, let us come back to the arguments of the assessee in light of certain judicial precedents including the decision of the Hon’ble Supreme Court in the case of Khader Khan Sons (supra) and also the decision of the Hon’ble Supreme Court in the case of Pullangode Rubber Produce Co. Ltd. v. State of Kerala reported in [1973] 91 ITR 18 (SC). There is no dispute with regard to the ratio laid down by the Hon’ble Supreme Court in the above two cases to the effect that no addition can be made only on the basis of survey statement without any corroborative evidences. This fact is also strengthened by the Circular issued by the CBDT vide Circular F.No.286/2/2003-IT(Inv) dated 10.03.2003, where the CBDT specifically directed the officers to not to obtain confession during survey proceedings without supporting evidences. But, fact remains that in the present case, additions made by the AO is not only on the basis of sworn statement recorded from the assessee at the time of survey but further supported by the corroborative evidences in the form of excess physical stock of gold ornaments found during the course of survey which was not explained by the assessee. Therefore, in our considered view, the arguments of the Ld. Counsel for the assessee in light of above decisions does not hold good and contrary to the facts available on record. Therefore, we are of the considered view that the AO has rightly made additional income offered during the course of survey but not admitted RoI towards excess stock found during the course of survey for Rs.3.75 Crs. The Ld.CIT(A) after considering relevant facts has rightly sustained the additions made by the AO. Thus, we are inclined to uphold the findings of the Ld.CIT(A) and dismiss the appeal filed by the assessee.

15. In the result, appeal filed by the assessee is dismissed.

Order pronounced on the 19th day of June, 2026, in Hyderabad.

Author Bio