New Income-tax Compliance to travel abroad

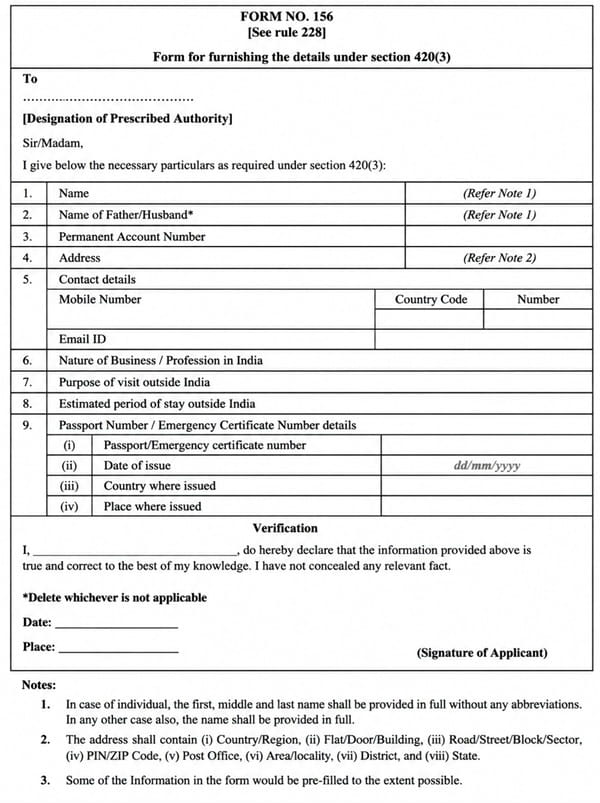

Are you planning to travel abroad after April 1, 2026? If so, you should be aware of certain mandatory compliances you must complete before going to the airport under the New Income-tax Law, 2025 — Section 420(3) and Income-tax Rule 228. From April 1, 2026, every resident citizen of India who holds a PAN and is leaving India temporarily or permanently must, subject to the exceptions notified, submit information online to the Income-tax Department using the new pre-filled Form No. 156. This marks a distinct shift from earlier provisions, which required intimation to the tax department only in specific cases of foreign travel.

This form is not a tax clearance certificate. Persons who do not have a PAN — for example, students, retired senior citizens, or those who have never had taxable income — cannot file this form. Failure to file may cause immigration problems, potentially serious consequences, and travel delays; therefore, this form has now become essential for international travel. Understandably, many taxpayers are confused due to this change. To address the ambiguity, the department has issued a set of FAQs on Income Tax Form 156 (Earlier Form 30C): Form for furnishing the details under section 420(3) of Income Tax Act, 2025, which forms one of the source for this write up.

It is pertinent to note that while the rules originally required online filing of Form 156, the online facility is currently not operational as the necessary software is not yet ready. Accordingly, as clarified in the FAQs, the form is to be submitted manually until the online system is enabled. Since this is a new compliance requirement and implementation remains incomplete due to technical constraints, rigorous follow-up by the department and government is still pending. Further, no penalty provisions have been introduced in the rules so far for non-compliance. It is a fact that many travellers who have left India and subsequently returned were not questioned by the immigration authorities. However, this may be attributed to the fact that the compliance requirement is relatively new and the operational mechanism for its effective implementation is not yet fully in place. Once the online submission system becomes fully operational, it is expected that stricter monitoring and enforcement will be carried out, particularly in cases involving individuals with significant tax liabilities. In any event, taxpayers will have little choice but to comply, as they will be required to carry the acknowledgement of submission of Form No. 156 while travelling. As international travel becomes increasingly common, awareness of this new requirement will be essential for smooth and hassle-free overseas travel.

What information is mandatory?

If a taxpayer has a PAN, they must complete the remaining fields in the pre-filled Form 156 online via the Income-tax Department’s e-filing portal. The taxpayer must provide their PAN, the purpose of the foreign visit, and the estimated duration of stay abroad. It has been clarified that the form cannot be filed without a PAN. The form does not apply to individuals with no taxable income in India. In such cases, and where there is no PAN, they must instead file Form 157 (the tax clearance certificate), which is also mandatory. While filling personal details, fields for Aadhaar or mobile number may be left blank because only the PAN is mandatory to complete Form 156. Aadhaar is no longer required in personal details; it can be provided if available. The Income-tax Department recommends providing a mobile number to ensure quick communication and verification.

What documents are required to file Form 156?

The person leaving India must provide their passport and PAN number. However, if a passport is not available, an emergency certificate issued by the passport-issuing country must be produced. Once Form 156 is submitted and an acknowledgment is received, no changes to the form will be allowed; therefore taxpayers are expected to ensure all details are accurate before uploading. It has also been clarified that there is no need to attach proof of tax payment with the form.

What is the process to file Form 156?

This form must be filed electronically through the Income-tax Department’s e-filing portal and includes the following steps:

- Registration: Individuals must register on the e-filing portal using a valid active PAN.

- Submitting Form 156: After registration, the taxpayer must log in to the e-filing portal and submit Form 156 electronically. The form is not yet available on the site but will be released soon.

- Verification: Depending on the taxpayer’s profile, the form can be verified using a pre-validated bank or demat account, an electronic verification code (OTP) generated via net banking or ATM (as per bank), or a Digital Signature Certificate (DSC).

Last year the Income-tax Department clarified that a tax clearance certificate is not required for every foreign travel. Subsequently, the simple streamlined form was notified as Notification No. 198(E) dated March 20, 2026. Under this system, the Income-tax Department will issue notices only to a limited number of taxpayers who do require a tax clearance certificate; only those persons will be required to obtain the certificate, and only then will they be permitted to travel abroad. It is not fully clear whether a taxpayer who files the form but does not receive such a notice will still be allowed to travel. However, it is clear that an ordinary taxpayer does not need a tax clearance certificate.

Conclusion

A Significant Change for International Travellers

The Income-tax Department had earlier clarified that a Tax Clearance Certificate is not required for every person travelling abroad. Consistent with that approach, the Central Government has introduced the simplified Form 156 through Notification No. 22/2026-Income Tax [G.S.R. 198(E)] dated 20 March 2026.

While the requirement does not impose any additional tax burden, it introduces a new reporting obligation for eligible residents undertaking international travel. Accordingly, taxpayers planning foreign visits after 1 April 2026 should ensure timely compliance to avoid any last-minute inconvenience.

FAQs – New Income Tax Form 156 Mandatory for Foreign Travel

Q1. Who is required to file Form 156 before travelling abroad?

Answer: From 1 April 2026, every resident Indian citizen holding a PAN and leaving India temporarily or permanently must submit Form 156 under Section 420(3) of the Income-tax Act, 2025 and Rule 228, unless covered by a notified exception.

Q2. Is Form 156 the same as a Tax Clearance Certificate?

Answer: No. Form 156 is only an information-reporting form and is not a Tax Clearance Certificate. The Income-tax Department has clarified that only a limited category of taxpayers who receive a specific notice will be required to obtain a Tax Clearance Certificate before travelling abroad.

Q3. What information and documents are required for filing Form 156?

Answer: Form 156 requires details such as the taxpayer’s PAN, purpose of foreign travel, and estimated duration of stay abroad. The taxpayer must also provide passport details or, if a passport is unavailable, an emergency certificate issued by the passport-issuing country. No proof of tax payment is required to be attached.

Q4. Can Form 156 be filed without a PAN or modified after submission?

Answer: No. A valid PAN is mandatory for filing Form 156. Once the form is submitted and an acknowledgement is generated, the details cannot be modified, so taxpayers should verify all information carefully before submission.

Q5. Is the online filing facility for Form 156 currently available?

Answer: Although the law provides for electronic filing through the Income-tax Department’s e-filing portal, the online facility is not yet operational. Until it is enabled, the department has clarified that Form 156 should be submitted manually in accordance with the FAQs issued by the Income-tax Department.