Monetary policy remained accommodative in 2019-20. The repo rate was cut by 110 basis points in four consecutive Monetary Policy Committee meetings in the financial year due to slower growth and lower inflation. However, it was kept unchanged in the fifth meeting held in December 2019. Liquidity conditions were tight for initial two months of 2019-20; but subsequently it has remained comfortable. The financial flows to the economy however, remained constrained as credit growth declined for both banks and Non-Banking Financial Corporations. The Gross Non Performing Advances ratio of Scheduled Commercial Banks has remained unchanged at 9.3 per cent between March and September 2019 and increased slightly for the Non-Banking Financial Corporations from 6.1 per cent to 6.3 per cent. Capital to Risk-weighted Asset ratio of Scheduled Commercial Banks increased from 14.3 per cent to 15.1 per cent between March 2019 and September 2019. Nifty50 and S&P BSE Sensex indices, reached record high closing of 12,355 and 41,952 respectively during 2019-20 (upto January 16, 2020). The resolution under IBC has been much higher as compared to previous resolution channels. Amount recovered as percentage of amount involved was 49.6 per cent in 2017-18 and 42.5 per cent in 2018-19. The proceedings under IBC take on average about 340 days, including time spent on litigation, in contrast with the previous regime where processes took about 4.3 years.

MONETARY DEVELOPMENTS DURING 2019-20

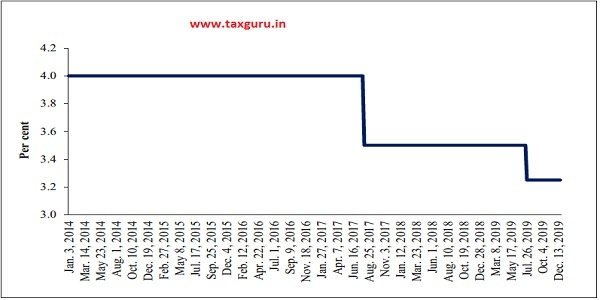

4.1 Monetary policy during 2019-20 was conducted under the revised statutory framework, which became effective from June 27, 2016. As on end January 2020, five meetings of the Monetary Policy Committee (MPC) have been held in financial year 2019-20. In the first four meetings, the MPC decided to cut the policy repo rate changing the stance of monetary policy from neutral to accommodative. The repo rate was reduced by 110 basis points (bps) from 6.25 per cent in April 2019 to 5.15 per cent in October 2019 (Table 1). MPC’s decision was guided by low inflation and the need to strengthen domestic growth by spurring private investment in the economy.

4.2 In its fifth bi-monthly monetary policy statement in December 2019, MPC decided to keep the repo rate unchanged at 5.15 per cent, underlining the rising consumer price inflation as one of the reasons. MPC also signaled its intention to wait until effective monetary policy transmission happens.

Various high frequency indicators along with surveys conducted by the Reserve Bank indicated a weakening of both domestic and external demand conditions; hence the real GDP projections were revised downwards to 5 per cent for 2019-20.

Table 1: Revision in Policy Rates

| Effective Date | Repo Rate (per cent) |

Reverse Repo Rate (per cent) |

Bank Rate/ MSF Rate* (per cent) |

Cash Reserve Ratio (per cent of NDTL) |

Statutory Liquidity Ratio (per cent of NDTL) |

| 04-04-19 | 6.00 | 5.75 | 6.25 | 4.00 | 19.25 |

| 06-06-19 | 5.75 | 5.50 | 6.00 | 4.00 | 19.00 |

| 07-08-19 | 5.40 | 5.15 | 5.65 | 4.00 | 18.75 |

| 04-10-19 | 5.15 | 4.90 | 5.40 | 4.00 | 18.50** |

| 05-12-19 | 5.15 | 4.90 | 5.40 | 4.00 | 18.50 |

| 04-01-20 | 5.15 | 4.90 | 5.40 | 4.00 | 18.25 |

Source: RBI.

Notes: NDTL is Net Demand and Time Liabilities.

*: Bank Rate was aligned to MSF rate with effect from February 13, 2012.

**: See RBI notification dated December 5, 2018 to reduce in SLR to 18 per cent in phases, viz., w.e.f. January 5, 2019 –

19.25 per cent; April 13, 2019 – 19.00 per cent; July 6, 2019 – 18.75 per cent; October 12, 2019 -18.50 per cent; January

4, 2020 – 18.25 per cent; and April 11, 2020 – 18.00 per cent.

Table 2: Year on Year (YoY) Change in Monetary Aggregates as on end March of each year (per cent)

| Items | 2013-14 | 2014-15 | 2015-16 | 2016-17* | 2017-18 | 2018-19 | 2019-20# |

| Currency in Circulation | 9.2 | 11.3 | 14.9 | -19.7 | 37 | 16.8 | 11.9 |

| Cash with Banks | 10.7 | 12.4 | 6.6 | 4.2 | -2.1 | 21.4 | 15.8 |

| Currency with the Public | 9.2 | 11.3 | 15.2 | -20.8 | 39.2 | 16.6 | 11.8 |

| Bankers’ Deposits with the RBI | 34 | 8.3 | 7.8 | 8.4 | 3.9 | 6.4 | 17.1 |

| Demand Deposits | 7.8 | 9.8 | 11 | 18.4 | 6.2 | 9.6 | 13.1 |

| Time Deposits | 14.9 | 10.7 | 9.2 | 10.2 | 5.8 | 9.6 | 9.8 |

| Reserve Money (M0) | 14.4 | 11.3 | 13.1 | -12.9 | 27.3 | 14.5 | 13.2 |

| Narrow Money (M1) | 8.5 | 11.3 | 13.5 | -3.9 | 21.8 | 13.6 | 12.5 |

| Broad Money (M3) | 13.4 | 10.9 | 10.1 | 6.9 | 9.2 | 10.5 | 10.4 |

Source: RBI.

Notes: * March 31, 2017 over April 1, 2016 (barring M0, CIC, and Bankers’ Deposits with the RBI).

# As on December 2019.

4.3 During 2018-19, the growth rates of monetary aggregates witnessed reversion to their long-term trend after experiencing unusual behavior in 2016-17 due to demonetisation and again in 2017-18 due to the process of remonetisation.

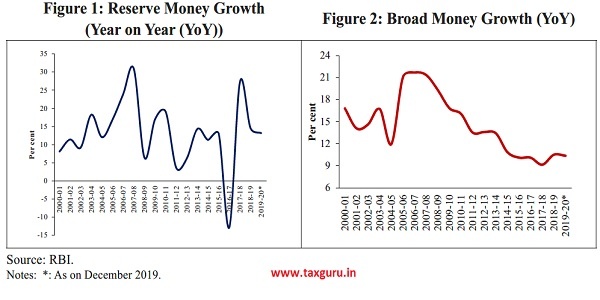

4.4 The growth of reserve money as on December 2019 was 13.2 per cent (Table 2 and Figure 1). On the component side, the expansion in reserve money was led by Currency in Circulation (CIC) (Table 2). From the sources side, expansion in M0 during 2019-20 so far (as on December 27, 2019) was contributed mainly by RBI’s Net Foreign Assets (NFA) as against Net Domestic Assets (NDA) during the previous year. Within NDA, while net RBI credit to the Government has contributed to the expansion in M0, it has been at a lower magnitude vis-à-vis last year. Among other sources, RBI’s claims on banks decreased, indicating surplus liquidity conditions in 2019-20 so far (discussed in more detail in the next section).

Figure 3: Deposits Growth (YoY)

Figure 3: Deposits Growth (YoY)

Source: RBI.

Note: Figures for December 2019 are as of December 20.

4.5 Broad money (M3) growth has been on declining trend since 2009 (Figure 2). However, since 2018-19 it has picked up marginally, mainly driven by the growth in aggregate deposits and stands at 10.4 per cent as on December 2019. Note that this is far below average growth of 14.9 per cent from 2000-01 to 2018-19 (Figure 2). From the component side, the expansion in M3 so far during the year is attributable to aggregate deposits, which recorded a higher growth of 10.1 per cent as on December 20, 2019 as compared with 9.2 per cent a year ago. Growth in both, time deposits and demand deposits picked up in 2019-20 and was higher in December 2019 as compared to December 2018 (Figure 3). On the sources side, banks’ credit to the government mainly contributed to M3 expansion.

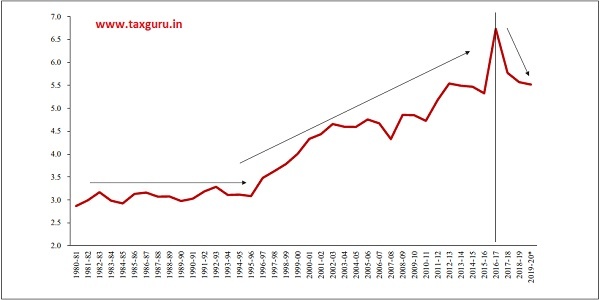

4.6 Between mid- 1990’s to 2016-17, the money multiplier (measured as a ratio of M3/M0) was mostly increasing; however, it has been declining since 2017-18. Money Multiplier recorded a slight decline in 2019-20 as well (Figure 4).

Figure 4: Money Multiplier (M3/M0)

Source: RBI.

Note:*: As on December 2019.

LIQUIDITY CONDITIONS AND ITS MANAGEMENT

4.7 Systemic liquidity in 2019-20 has been largely in surplus since June 2019 (Figure 5). Durable liquidity injection was undertaken through four Open Market Operations (OMOs) purchase auctions and one US$ 5 billion buy/sell swap auction, all conducted during first quarter of 2019-20. Moreover, the Reserve Bank’s forex operations augmented the domestic rupee liquidity in contrast to absorption last year. Furthermore, the Statutory Liquidity Ratio (SLR) has been reduced by 25 bps each in four steps effective April 13, 2019, July 6, 2019, October 12, 2019 and January 4, 2020 respectively, to 18.25 per cent of Net Demand and Time Liabilities (NDTL) of banks, in accordance with the roadmap announced in December 2018 with a view to aligning the SLR with the Liquidity Coverage Ratio (LCR). Other factors creating surplus liquidity are moderation in currency demand after two years of high demand following demonetisation.

Figure 5: Daily Liquidity Management

Source: Net liquidity injected data from Money Market Operation, RBI

4.8. April and May were the only two months in 2019-20 (upto January 2020) when liquidity was in deficit due to restrained government spending and high demand for cash. The unwinding of Government of India cash balances – a regular feature every year in April – was much lower in the current year due to the imposition of the model code of conduct during elections restraining government spending. RBI conducted a US$/Rs. buy/sell swap auction of US$ 5 billion for a tenor of three years in April, thereby injecting Rs. 34,874 crore, and two OMO purchase auctions in May amounting to Rs. 25,000 crore. The increased spending by the government, net forex purchases by the RBI and return of currency to the banking system combined with the two OMO purchase auctions amounting to Rs. 27,500 crore conducted by the Reserve Bank resulted in surplus liquidity in June. Liquidity has remained in surplus despite some episodes of forex sales in July and August.

Figure 6: Policy Corridor and Call Rate

Source: RBI.

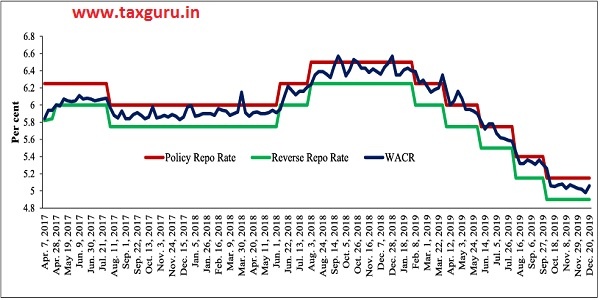

4.9 Comfortable liquidity situation is also evident in the Weighted Average Call Money Rate (WACR) being mostly been close to the repo rate within the Liquidity Adjustment Facility (LAF) corridor (Figure 6).

4.10 With a view of moving further towards harmonization of the effective liquidity requirements of banks with LCR a roadmap was given in April 2019 to increase the Facility to Avail Liquidity for LCR by 50 bps in four steps to reach 15 per cent of NDTL by April 2020. Thus, by April 1, 2020, the total High Quality Liquid Assets carve out from SLR would be 17.0 per cent of NDTL of banks.

DEVELOPMENTS IN THE G-SEC MARKET

4.11 During the first half of 2019-20, the 10-year benchmark G-Sec yield mostly softened (Figure 7), tracking subdued crude oil prices, surplus liquidity, and four consecutive policy rate cuts amounting to 110 bps.

4.12 In first quarter of 2019-20, initially from April to mid-May 2019, 10-year benchmark yield hardened marginally on account of rise in crude oil prices. Thereafter, it largely followed a downward trend. The primary drivers for the softening of yield may be attributed to change in monetary policy stance of the U.S. Fed (on global growth concerns and ongoing trade tensions), easing of liquidity condition of the banking system, consecutive policy rate cuts by the RBI along with change of stance from neutral to accommodative. Additionally, benign crude oil prices aided the sentiment. Transfer of RBI surplus to the Government, accommodative stance by MPC, significant and sustained surplus liquidity, also, capped further upside in yields.

4.13 The softening of the benchmark yield continued during early period of second quarter of 2019-20 amidst expectation of another rate cut on the back of slowing economy. Thereafter, the yield started to harden on the back of news of launch of a new 10-year security and unexpected rise in crude oil prices. After the December 2019 MPC meeting where policy repo rates were kept unchanged, the 10 year G-Sec yields went up and stood at 6.8 per cent on December 16, 2019.

4.14 “Special Open Market Operation” by Reserve Bank of India, which means purchase of long term securities and simultaneous sale

Figure 7: 10-Year Benchmark G-Sec Yield

Source: CCIL.

of short term securities helped bring down the yield slightly on 10 year G-Secs. This is expected to bring down the term premium by reducing the differential between the long and short term bond yields. The first round of sale and purchase worth `10,000 crore was done on December 23, 2019. The second and third round was on December 30, 2019 and January 6, 2020 respectively for the same amount. This led to a slight decline in the yield of 10-year G-Sec. The 10-year benchmark bond (6.45% GS 2020) yield closed at 6.8 per cent on December 16, 2019 and declined to 6.6 per cent on December 20, 2019 and 6.5 per cent on January 2, 2020. However, the yield on 10-year benchmark bond drifted up again and stood at 6.63 per cent on January 15, 2020.

BANKING SECTOR

4.15 Gross Non Performing Advances (GNPA) ratio (i.e. GNPAs as a percentage of Gross Advances) of Scheduled Commercial Banks remained flat at 9.3 per cent at end September 2019, as was at end March 2019. Similarly their Restructured Standard Advances (RSA) ratio remained unchanged at 0.4 per cent during the same period. The Stressed Advances (SA) ratio of Scheduled Commercial Banks (SCBs) followed suit by remaining flat at 9.7 per cent as at end-September 2019. GNPA ratio of Public Sector Banks (PSBs) was unchanged at 12.3 per cent while stressed advances ratios increased from 12.7 per cent at end March 2019 to 12.9 per cent at end September 2019.

4.16 Capital to risk-weighted asset ratio (CRAR) of SCBs increased from 14.3 per cent to 15.1 per cent between March 2019 and September 2019, largely due to improvement in CRAR of PSBs. SCBs’ Return on Assets (RoA) recovered from (-) 0.1 per cent to 0.4 per cent during H1 of 2019-20, while their Return on Equity (RoE) recovered from (-) 1.6 per cent to 4.1 per cent during the same period. However, many PSBs have continued to record negative profitability ratios since March 2016, mainly on account of provisioning requirements.

MONETARY TRANSMISSION

4.17 Transmission of monetary transmission has been weak in 2019 on all three accounts: Rate Structure, Quantity of Credit, and Term Structure.

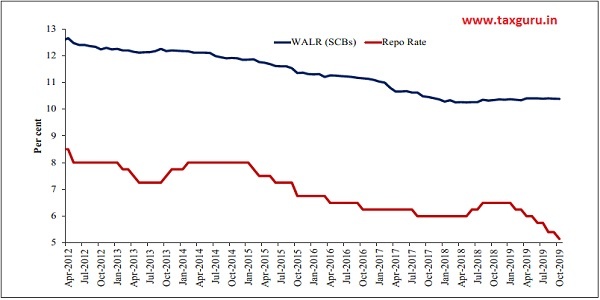

(a) Rate Structure: The Weighted Average Lending Rate (WALR) of SCBs has not

Figure 8: Weighted Average Lending Rate on outstanding loans and Repo rate

Source: RBI.

declined at all in 2019 despite reduction of repo rate by 135 bps since January 2019 (Figure 8). WALR on outstanding rupee loans of SCBs was 10.38 per cent in January 2019 and 10.40 per cent in October 2019. The monetary transmission has been slightly better for fresh loans. WALR on fresh loans of Public Sector Banks reduced by 47 bps and that of Private Sector Banks reduced by 40 bps from January to October 2019. However, even this has been much less than the repo rate cut of 135 bps (in 2019).

4.18 The credit spread (difference between repo rate and WALR) is at the highest level in this decade. WALR on outstanding loans of SCBs is 525 bps higher than the repo rate, suggesting that there has been no transmission

Figure 9: Credit spread

Source: RBI.

Note: Blue means CRR cut, Red denotes Repo hike, Green denotes Repo cut.

Credit spread is defined as difference between repo rate and WALR on outstanding loans.

Figure 10: Saving Deposit Rate

Source: RBI.

of the cut in repo rate to lending rates of the banks in 2019. (Figure 9).

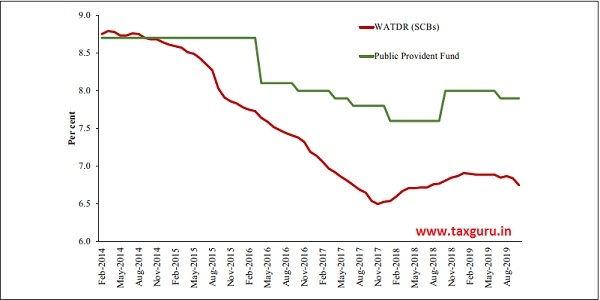

4.19 There has been a reduction in the saving deposit rate by 25 bps in 2019 (Figure 10). The term deposit rate which is more important has seen a decline of only 16 bps from January 2019 to October 2019. An important limiting factor seems to be the rate on small savings scheme like Public Provident Fund (PPF). In 2014, the Weighted Average Term Deposit Rate (WATDR) was same as PPF, however the gap between them is 115 bps at end October 2019 (Figure 11). It is unlikely that the term deposit rates can decline without a decrease in administered rates on schemes like these.

(b) Term structure

4.20 RBI’s monetary easing and LAF liquidity has had some impact on short term interest rates. However, this impulse is not feeding through to longer term maturities. Since the beginning of the year, the yields on short term government securities (364 days T-bill) have declined much faster than that

Figure 11: Term Deposit Rate of SCBs and rate of interest on Public Provident Fund

Source: RBI and Ministry of Finance.

Figure 12: Bond yields (per cent)

Source: CCIL.

of long term Government securities (10-year G-sec). Infact, after August 2019 the yield on 10-year G-Sec have not declined much, barring the small decline after Special Open Market Operation by RBI (details in previous section) (Figure 12).

(c) Credit Growth

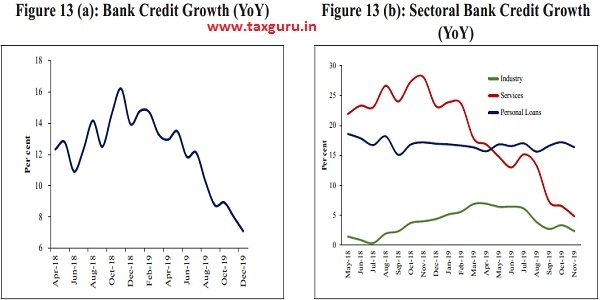

4.21 Despite a decrease in policy rates, the credit growth in the economy has been declining since the beginning of this year. Bank Credit growth (YoY) moderated from 12.9 per cent in April 2019 to 7.1 per cent as on December 20, 2019. The credit growth has been moderating from December 2018, when it was 13.9 per cent (Figure 13(a)). The moderation in credit growth was witnessed across all the major segments of non-food credit, except personal loans, which continued to grow at a steady and robust pace during 2019-20 so far (data available till November 2019). The moderation was led by a sharp deceleration in credit growth to the services sector. Credit growth to industry has been very low in the recent months (Figure 13(b)). The main contributor to this slowdown has been a negative growth of credit to Micro, Small and Medium Enterprises and Textiles (Table 3).

Source: RBI.

Table 3: Growth in Industry-wise Deployment of Bank Credit by Major Sectors (YoY, per cent)

| Item | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Nov-19# |

| Non Food Credit | 8.6 | 9.1 | 8.4 | 8.4 | 12.3 | 7.2 |

| Industry | 5.6 | 2.7 | -1.9 | 0.7 | 6.9 | 2.4 |

| Micro & Small | 9.1 | -2.3 | -0.5 | 0.9 | 0.7 | -0.1 |

| Medium | 0.4 | -7.8 | -8.7 | -1.1 | 2.6 | -2.4 |

| Large | 5.3 | 4.2 | -1.7 | 0.8 | 8.2 | 3.0 |

| Textiles | -0.1 | 1.9 | -4.6 | 6.9 | -3.0 | -6.1 |

| Infrastructure | 10.5 | 4.4 | -6.1 | -1.7 | 18.5 | 7.0 |

Source: RBI.

Note: Data are provisional and relate to select banks which cover about 90 per cent of total non-food credit extended by all

scheduled commercial banks.

# as on November 22, 2019.

Box 1: Major Policy Changes related to Banking Regulations

1. Permitting One-time Restructuring of Existing Loans to MSMEs Classified as ‘Standard’ without a Downgrade in the Asset Classification

A one-time restructuring of existing loans to MSMEs that were in default but with asset classification as ‘standard’ as on January 1, 2019, was permitted without an asset classification downgrade. The scheme is available to MSMEs qualifying with objective criteria including, inter alia, a cap of Rs. 25 crore on the aggregate exposure of banks and NBFCs as on January 1, 2019. The restructuring will have to be implemented by March 31, 2020 and an additional provision of 5 per cent will have to be maintained in respect of accounts restructured under this scheme.

2. Bank Lending to Infrastructure Investment Trusts (InvITs)

It was decided to permit banks to lend to InvITs, subject to certain safeguards which include a Board approved policy on exposures to InvITs, assessment of all critical parameters including sufficiency of cash flows at InvIT level, overall leverage of the InvITs and the underlying SPVs to be within the leverage permitted under the Board approved policy, monitoring of performance of the underlying SPVs on an ongoing basis and lending to only those InvITs where none of the underlying SPVs are facing ‘financial difficulty’.

3. Resolution of Stressed Assets

Reserve Bank released the new Prudential Framework for Resolution of Stressed Assets. The fundamental principles underlying the regulatory approach for resolution of stressed assets are as under:

(i) Early recognition and reporting of default in respect of large borrowers by banks, FIs and NBFCs;

(ii) Complete discretion to lenders with regard to design and implementation of resolution plans, subject to the specified timeline and independent credit evaluation;

(iii) Harmonised framework for resolution of stressed assets, in supersession of all earlier resolution schemes (S4A, SDR, 5/25, etc.);

(iv) A system of disincentives in the form of additional provisioning for delay in implementation of resolution plan or initiation of insolvency proceedings;

(v) Withdrawal of asset classification dispensations on restructuring. Future upgrades to be contingent on a meaningful demonstration of satisfactory performance for a reasonable period;

(vi) For the purpose of restructuring, the definition of ‘financial difficulty’ to be aligned with the guidelines issued by the Basel Committee on Banking Supervision; and,

(vii) Signing of inter-creditor agreement (ICA) by all lenders to be mandatory, which will provide for a majority decision making criteria.

4. External Benchmark Based Lending

As the transmission of policy rate changes to the lending rate of the banks under the current MCLR framework was not satisfactory, guidelines were issued to banks on September 4, 2019 mandating banks w.e.f. October 1, 2019 to link all new floating rate personal or retail loans and floating rate loans to MSE to an external benchmark as under:

a) Benchmarks: The banks are free to choose one of the several benchmarks from Repo Rate, 3 Months or 6 Months Treasury Bill yield and any other benchmark market interest rate published by the Financial Benchmark India Private Ltd (FBIL).

b) Spread: Banks are free to decide the spread over the external benchmark. However, credit risk premium may undergo change only when borrower’s credit assessment undergoes a substantial change, as agreed upon in the loan contract. Further, other components of spread including operating cost could be altered once in three years.

c) Reset of interest rates: The interest rate under external benchmark shall be reset at least once in three months.

5. Revised guidelines on compensation of Whole Time Directors/Chief Executive Officers/Material Risk Takers and Control Function Staff for all Private Sector Banks (including LABs, SFBs, PBs, WOS, and foreign banks) to be effective from April 01, 2020:

a) Substantial portion of compensation e. at least 50 per cent should be variable (Earlier no threshold was prescribed)

b) Employee Stock Ownership Plans (ESOPs) to be included as a component of Variable Pay as share-linked instruments. (Earlier excluded)

c) Variable Pay is to be capped at 300 per cent of Fixed Pay (Earlier Variable Pay was capped at 70 per cent of Fixed Pay but did not include ESOPs/share-linked instruments)

d) Minimum 50 per cent of Variable Pay is to be via non-cash component (such as ESOPs). (Earlier no specific proportion was prescribed)

e) Mandating a compulsory deferral mechanism for Variable Pay, regardless of quantum of variable pay (Earlier it was mandated only beyond a specified threshold)

f) Mandating imposition of malus in case of divergence in NPA/provisioning beyond RBI prescribed threshold for public disclosure. (New addition)

g) Quantitative and Qualitative criteria are being prescribed for identification of Material Risk Takers (New addition).

NON-BANKING FINANCIAL SECTOR (NBFC)

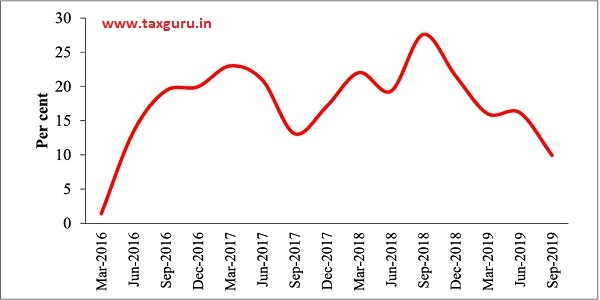

4.22 After growing very fast in 2017-18 and in first half of 2018-19, the sector has decelerated sharply since then. The growth of loans from NBFCs declined from 27.6 per cent in September 2018 and 21.6 per cent in December 2018 to 9.9 per cent at end September 2019 (Figure 14).

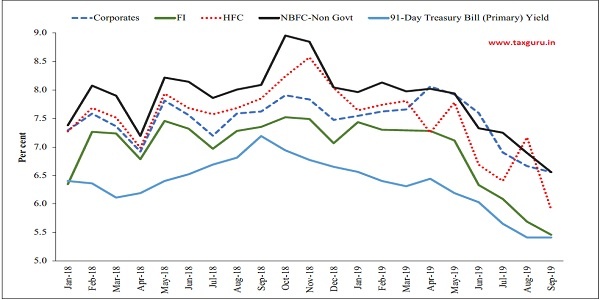

4.23 The balance sheet of the NBFC sector grew by 17.9 per cent from ` 26.18 lakh crore to ` 30.85 lakh crore during 2018-19. This growth was on top of a growth of 21.3 per cent recorded during 2017-18 despite concerns over NBFCs. The third quarter of 2018-19 witnessed liquidity stress. The cost of funds for NBFCs declined by March 2019 and further by September 2019, as reflected in the 3-month CP discount rate1 (Figure 15).

Figure 14: Growth in Loans and advances by NBFCs (YoY)

Source: RBI.

Note: 1. Data pertains to deposit taking NBFCs and Non-Deposit Taking Systematic Important NBFCs including Government Companies.

2. Data from June 2018 onwards is provisional.

Figure 15: Category wise 3-Month CP Rate2

Source: RBI.

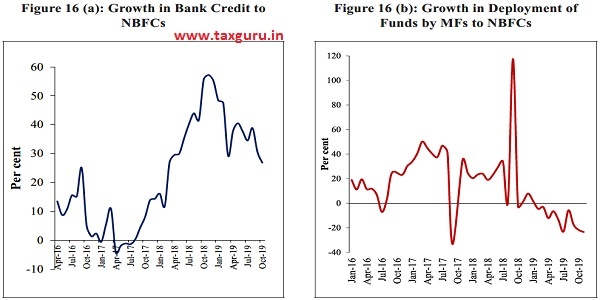

4.24 There is an observable shift in the sources of funding of NBFCs. Bank borrowings increased from Rs.5.62 lakh crore in October 2018 to Rs.7.13 lakh crore in October 2019 i.e. a growth of 26.8 per cent (Figure 16 (a)). However, this growth is much lower as compared to end October 2018. Deployment of credit by mutual funds to NBFCs has been contracting since October 2018 (Figure 16 (b)).

4.25 The market borrowings increased from Rs.10.4 lakh crore to Rs.10.5 lakh crore during September 2018 to September 2019. Among the instruments of market borrowing, the share of Commercial Papers decreased by 31.2 per cent from September 2018 to September 2019, while the share of Non-Convertible Debentures (NCDs) increased by 7.7 per cent from Rs. 8.61 lakh crore to Rs. 9.27 lakh crore in the same period.

4.26 As against the regulatory requirement of 15 per cent, the Capital to risk weighted assets ratio (CRAR) of NBFC sector remained at 19.5 per cent at end March 2019 and end September 2019. The gross NPAs ratio of NBFC sector increased from 5.8 per cent at end March 2018 to 6.1 per cent at end March 2019 and further increased marginally to 6.3 per cent at end September 2019. The net NPAs ratio marginally increased from 3.3 per cent in March 2018 to 3.4 per cent in March 2019 and remained same as on September 2019. The Return on Assets (RoA) of the sector decreased to 1.5 per cent as on March 2019 from 1.6 per cent as on March 2018. Further, the Return on Equity (RoE) moderated to 6.6 per cent as on March 2019 from 6.9 per cent as on March 2018.

Source: SEBI & RBI (Sectoral deployment of bank credit by major sectors)

Note for figure 16(a)

1. This data includes HFCs as well.

2. Data are provisional and relate to select banks which cover about 90 per cent of total non-food credit extended by all scheduled commercial banks.

Box 2: Major Policy Changes related to Non-banking Financial Regulation /Supervision

In the aftermath of the IL&FS event, several measures were undertaken to strengthen the regulation and supervision of the NBFC sector, as set out below.

1. Amendment to the RBI Act, 1934 to Strengthen the Regulation and Supervision of the NBFC Sector vesting additional powers with the Reserve Bank to:

a. Raise the minimum net owned fund requirement for NBFCs up to Rs. 100 crore (from existing Rs. 2 crore);

b. Remove Director of an NBFC from the office (other than Government companies);

c. Supersede the Board of Directors of NBFC (other than Government companies);

d. Remove or debar statutory auditor from exercising the duties as auditor of any of the RBI regulated entities;

e. Resolve NBFCs through amalgamation, reconstruction, splitting the viable and non-viable businesses in separate units;

f. Direct an NBFC to annex its financial statements such as statements and information relating to the business or affairs of any group company of the NBFC and to cause an inspection or audit to be made of any group company of an NBFC and its books of account.

g. To increase the quantum of penalties that the Reserve Bank may impose.

2. Eligible NBFC-ND-SIs as Authorised Dealers (ADs) – Category II: The Reserve Bank allowed non-deposit taking systemically important NBFC-ICCs to obtain AD-Category II license, effective April 16, 2019, in order to increase accessibility and efficiency of the services extended to the members of the public for their day-to-day non-trade current account transactions. Eligible NBFCs will have to satisfy certain conditions and seek specific permission from the Reserve Bank.

3. Liquidity Risk Framework for NBFCs: All non-deposit taking NBFCs with asset size of ` 100 crore and above, systemically important Core Investment Companies and all deposit taking NBFCs irrespective of their asset size, shall adhere to the set of liquidity risk management guidelines:

a) Granular maturity buckets and tolerance limits,

b) Liquidity risk monitoring tools/ metrics to capture strains in liquidity position,

c) Adoption of “stock” approach to liquidity, in addition to structural & dynamic liquidity,

d) Extension of principles of sound liquidity risk management to aspects like off-balance sheet and contingent liabilities, intra-group fund transfers, etc., and

e) Introduction of Liquidity Coverage Ratio (LCR) for all non deposit taking NBFCs (excluding Core Investment Companies, Non-operating Financial Holding Companies Standalone Primary Dealers and Type-I NBFCs) with asset size Rs. 5,000 crore and above and all deposit taking NBFCs irrespective of size to maintain sufficient High Quality Liquid Assets (HQLA) to survive any acute liquidity stress. The LCR will be progressively increased to 100 per cent by December 1, 2024.

4. Review of Limits for NBFC-Micro Finance Institutions (NBFC-MFIs): The household income limits for borrowers of NBFC-MFIs have been raised from the current level of Rs.1,00,000 for rural areas and Rs.1,60,000 for urban/semi urban areas to Rs.1,25,000 and Rs.2,00,000, respectively, along with increase in lending limit from Rs.1,00,000 to Rs. 1,25,000 per eligible borrower effective November 8, 2019.

Housing Finance Companies: The regulation of Housing Finance Companies (HFCs) has been transferred by Government of India from National Housing Bank (NHB) to the RBI with effect from August 9, 2019.

DEVELOPMENTS IN CAPITAL MARKET

Primary Market

A. Public Issue

4.27 The total money raised by public and rights issue increased to Rs.73,896 crore in the year 2019-20 (up to December 31, 2019) from Rs. 44,355 crore in the corresponding period last year. In the same period in 2018-19, the Primary market resource mobilisation through public and rights issues had declined as compared to 2017-18.

Equity

4.28 The resource mobilisation through public issue (equity) decreased in April-December 2019 compared to the similar period for previous year, continuing with the declining trend of last year. During April-December 2019, 47 companies mobilized Rs. 10,895 crore through public equity issuance compared to 103 companies raising Rs. 13,947 crore in April-December 2018, indicating a decrease of 21.9 per cent over the period. On the other hand, resource mobilization through rights issues (equity) during April-December 2019 increased sharply with resource mobilization of Rs. 51,255 crore, as compared to Rs. 1,843 crore in the corresponding period of last year (Table 4).

Table 4: Primary Market Resource Mobilisation through Public and Rights Issues

| Issue Type | 2016-17 (upto Dec 31, 2016) | 2017-18 (upto Dec 31, 2017) | 2018-19 (upto Dec 31, 2018) | 2019-20 (upto Dec 31, 2019) | ||||

| No of issues | Amount (Rs. crore) | No of issues | Amount (Rs. crore) | No of issues | Amount (Rs. crore) | No of issues | Amount(Rs. crore) | |

| Public Issue (Equity) | 70

|

24,515

|

134

|

64,141

|

103

|

13,947

|

47

|

10,895

|

| Rights Issue (Equity) | 5

|

1,297

|

14

|

4,522

|

6

|

1,843

|

11

|

51,255

|

| Public Issue (Debt) | 12 | 27,161 | 4 | 3,896 | 15 | 28,565 | 27 | 11,746 |

| Total Public Issue | 87 | 52,973 | 152 | 72,559 | 124 | 44,355 | 85 | 73,896 |

Source: SEBI.

Debt

4.29 Resource mobilization through issuance of debt securities to public declined significantly to Rs. 11,746 crore raised through 27 issues during April-December 2019, as compared to Rs. 28,565 crore through 15 issues in the corresponding period of the previous year.

B. Private Placement

4.30 During 2019-20 (up to December 31, 2019), Indian corporates preferred private placement route to gear up the capital in the corresponding period in previous year. Rs. 6.29 lakh crore was raised through 1,520 issues in April-December 2019 through private placements, as compared to Rs. 5.3 lakh crore through 2,006 issues in the corresponding period of previous year (Table 5).

Equity

4.31 There were 225 issues which raised Rs. 1.79 lakh crore through private placement of equity securities in April-December 2019, compared to 335 issues which raised Rs. 1.57 lakh crore in April-December 2018. Out of the 225 issues, there were 9 qualified institutional placement (QIP) allotments and 216 preferential allotments which raised Rs. 34,029 crore and Rs. 1.45 lakh crore, respectively, during April-December 2019, as compared to 11 QIPs allotments and 324 preferential allotments which raised Rs. 6,958 crore and Rs. 1.50 lakh crore, respectively, in April-December 2018.

Debt

4.32 Further, the resource mobilization through private placement of corporate bonds stood at Rs. 4.50 lakh crore during April-

Table 5: Primary Market Resource Mobilisation through Private Placements

| Issue Type | 2016-17 (upto Dec 31, 2016) | 2017-18 (upto Dec 31, 2017) | 2018-19 (upto Dec 31, 2018) | 2019-20 (upto Dec 31, 2019) | ||||

| No of issues | Amount (Rs. crore) | No of issues | Amount (Rs. crore) | No of issues | Amount (Rs. crore) | No of issues | Amount (Rs.crore) | |

| QIPs Allotment (Equity) | 14 | 4,395 | 37 | 57,711 | 11 | 6,958 | 9 | 34,029 |

| Preferential Allotment (Equity) | 299 | 30,224 | 307 | 40,668 | 324 | 1,49,921 | 216 | 1,45,404 |

| Private Place- ment of Bonds | 2,662 | 4,78,974 | 1,943 | 4,60,061 | 1,671 | 3,73,375 | 1,295 | 4,49,939 |

| Total Private Placement | 2,975 | 5,13,593 | 2,287 | 5,58,440 | 2,006 | 5,30,254 | 1,520 | 6,29,372 |

Source: BSE, NSE, MSEI and SEBI.

December 2019, as compared to Rs. 3.73 lakh crore during April-December 2018.

Mutual Fund Activities

4.33 There was a net inflow of Rs. 1.9 lakh crore into the mutual funds industry during April-December 2019 as compared to a net inflow of Rs. 0.8 lakh crore for the corresponding period in last year. The net Assets Under Management (AUM) of all mutual funds increased by 18.4 per cent to Rs. 26.3 lakh crore at the end of December 31, 2019 from Rs. 22.2 lakh crore at the end of December 31, 2018 (Table 6).

INVESTMENT BY FOREIGN PORTFOLIO INVESTORS (FPIs)

4.34. There were net inflows to the tune of Rs. 0.81 lakh crore on account of the FPIs in the Indian capital market during April-December 2019, as compared to net outflows of Rs. 0.94 lakh crore during April-December 2018. The total cumulative investment by FPIs (at the acquisition cost) increased by 7.8 per cent to US$ 259.5 billion as on December 31, 2019 from US$ 240.1 billion as on December 31, 2018 (Table 7).

MOVEMENT OF INDIAN BENCHMARK INDICES

4.35. India’s benchmark indices, namely, Nifty 50 and S&P BSE Sensex, reached record highs during 2019-20 (upto January 16, 2020). The S&P BSE Sensex, the benchmark index of Bombay Stock Exchange (BSE), reached an all-time high closing of 41,952 on January 14, 2020, witnessing an increase of 7.9 per cent from 38,871 level on April 1, 2019. Nifty 50 index reached an all time high closing at 12,355 on January 16, 2020 (Figure 17).

Table 6: Mobilization of Funds by Mutual Funds

| Period | No. of Folios (crore) | Gross Mobilization (Rs. lakh crore) | Redemption (Rs. lakh crore) | Net Inflows (Rs. lakh crore) | Net AUM at the end of the period (Rs. lakh crore) |

| 2018-19 (upto December 31, 2018) | 8.03 | 139.30 | 138.50 | 0.80 | 22.20 |

| 2019-20 (upto December 31, 2019) | 8.71 | 134.30 | 132.50 | 1.90 | 26.30 |

Source: NSDL.

Table 7: Investment by Foreign Portfolio Investors

| Year/Month

|

Gross Purchase (Rs.crore) | Gross Sales (Rs. crore) | Net Investment (Rs. crore) | Net Investment (US $ mn.) | Cumulative Net Investment (US $ mn.) |

| 2018-19 (upto December 31, 2018) | 11,78,809 | 12,72,988 | -94,179 | -13,442 | 2,40,171 |

| 2019-20 (upto December 31, 2019) | 13,79,888 | 12,99,141 | 80,746 | 11,465 | 2,59,579 |

Source: NSDL.

Figure 17: Movement of Indian Benchmark Indices

Source: BSE and NSE.

Box 3: Benefits of Enabling Bilateral Netting for Financial Contracts in India

A bilateral netting agreement enables two counterparties in a financial contract to offset claims against each other to determine a single net payment obligation due from one counterparty to the other. Similarly, a multilateral netting agreement allows counterparties to offset claims against each other through a Central Counterparty (CCP) in a clearing house. Under instances of default, including insolvency, dissolution or winding-up of counterparty, close-out netting enables the non-defaulting counterparty to prematurely terminate the financial contract and sum the mutual claims to determine a single net amount due from one counterparty to the other.

At present, there are legal provisions for multilateral close-out netting for financial transactions intermediated through a CCP, such as the Clearing Corporation of India Limited (CCIL), under the Payment and Settlement Systems (Amendment) Act (2015). However, bilateral netting for financial contracts is not permitted in India. This negatively impacts banks and other financial market participants via several channels:

(i) In the absence of bilateral netting, RBI’s regulations require banks to measure credit exposure to a counterparty for OTC derivative contracts based on gross marked-to-market (MTM) exposure instead of net MTM exposure. This increases credit risk for financial market participants, especially in the event of insolvency of a counterparty, which could then raise systemic risk.

(ii) In implementing the Basel III regulatory reforms3, RBI requires banks to calculate regulatory capital requirements for OTC derivative transactions based on gross MTM exposure to a counterparty instead of net MTM exposure. This forces banks to hold more regulatory capital than what would be required under bilateral netting. According to RBI estimates, bilateral netting arrangements could have helped 31 major banks participating in India’s OTC derivatives market save about ` 22.58 billion in regulatory capital during FY2017-18.

(iii) The RBI’s current proposal for implementing global OTC derivatives market reforms4 requires financial institutions to exchange margin5(collateral) with counterparties for OTC derivative transactions based on gross counterparty exposure instead of net counterparty exposure. Implementation of this reform going forward would force banks to divert more capital towards collateral requirements than what would be required if bilateral netting is permitted. According to CCIL estimates, banks and primary dealers would have had to hold about `98 billion of additional capital as margin6 as of March 2018 if margin regulations were implemented.

(iv) Higher regulatory capital burden makes trading activity for financial contracts more capital intensive, translating into higher cost of transaction. This discourages market participation by banks and primary dealers, affecting market liquidity and market development in terms of depth. This is one of the major factors hindering activity in India’s Credit Default Swaps (CDS) market (RBI Report of Working Group on Development of Corporate Bond Market in India, 2016).

Global regulatory bodies such as the Financial Stability Board (FSB) and the Basel Committee on Banking Supervision have supported the use of close-out netting due to its positive impact on financial stability. At present, major jurisdictions such as the U.S., U.K., Australia, Canada, Japan, France, Germany, Singapore and Malaysia have legal provisions in place for netting agreements.

Hence, establishing a legal framework for bilateral close-out netting in India would help: (a) reduce credit risk and regulatory capital burden for banks, freeing up capital for other productive uses; (b) reduce hedging costs and liquidity needs for banks, primary dealers and other market-makers, thereby encouraging participation in the OTC derivatives market to hedge against risk. Increased market participation in the CDS market would also provide an impetus for corporate bond market development; (c) establish an efficient recovery mechanism for financial contracts under instances of default by a counterparty; and (d) adhere to India’s G20 and FSB commitment to implement global regulatory reforms in the OTC derivatives market.

INSURANCE SECTOR

4.36. Internationally, the potential and performance of the insurance sector are generally assessed on the basis of two parameters, viz., insurance penetration and insurance density. The measure of insurance penetration and density reflects the level of development of insurance sector in a country. While insurance penetration is measured as the percentage of insurance premium to GDP, insurance density is calculated as the ratio of premium to population (measured in US$ for convenience of international comparison).

4.37. The insurance density in India which was US$ 11.5 in 2001, reached to US$ 74 in 2018 (Life- US$ 55 and Non-Life – US$ 19). The comparative figures for Malaysia, Thailand and China during the same period were US$ 518, US$ 385 and US$ 406 respectively. Penetration

Box 4: Defined Contributory Pension Scheme: National Pension System

The New Pension Scheme, now renamed as National Pension System (NPS) was introduced by the Government on December 22, 2003 and it was made mandatory for Central Government employees (except armed forces) who join service w.e.f. January 1, 2004. The Scheme was extended to the State Governments and as of now 28 State Governments have notified NPS for their employees. The Scheme was extended to all citizens of the country on voluntary basis from May 2009.

Till September 30, 2019, a total of around 3.06 crore subscribers (including Atal Pension Yojana) have been enrolled under NPS. Assets Under Management (AUM) which includes the returns on the corpus, under the NPS have witnessed an increase from Rs.3.18 lakh crore as on 31st March 2019 to Rs.3.71 lakh crore as on September 30, 2019, registering an increase of 16.71 per cent. The APY has a total of 1.78 crore subscribers and AUM of Rs.8,743 crore as on September 30, 2019 (Table 1).

Table 1: Number of Subscribers, Corpus and Assets Under Management under NPS/APY (As on 30th September 2019)

| Sector | Number of Sub- scribers | Contribution*(Rs. Crore) | Asset Under Management (Rs.Crore) | |||

| Absolute | % | Absolute | % | Absolute | % | |

| Central Government | 18,31,307 | 14 | 75,504 | 28 | 1,07,409 | 30

|

| Central Autonomous Bodies (CAB) | 1,94,419 | 2 | 12,796 | 5 | 17,294 | 5

|

| State Government | 38,56,844 | 30 | 1,26,668 | 46 | 1,68,547 | 46

|

| State Autonomous Bodies | 7,01,274 | 5 | 17,229 | 6 | 18,412 | 5 |

| Corporate | 9,68,019 | 8 | 28,307 | 10 | 36,580 | 10 |

| Unorganised Sector | 9,25,810 | 7 | 10,986 | 4 | 10,777 | 3 |

| NPS Lite | 43,39,836 | 34 | 2,624 | 1 | 3,631 | 1 |

| Total | ,28,17,509 | 100 | 2,74,115 | 100 | 3,62,650 | 100 |

| APY | 11,78,21,441 | 7,927 | 8,743 | |||

| Total | 3,06,38,950 | 2,82,042 | 3,71,393 | |||

Source: CRA Report

Note: *Matched and Booked.

Within the government, Uttar Pradesh has maximum number of subscribers followed by Madhya Pradesh, Rajasthan, and Maharashtra. The largest Assets under Management are with Rajasthan followed by Uttar Pradesh, Madhya Pradesh and Maharashtra (Table 2).

Table 2: Geographical Coverage under NPS (Govt Sector)

| Sl. No. | State Govt. | Total No. of Subscribers | Contribution (Rs. Crore) | AUM (Rs. Crore) |

| 1. | Andhra Pradesh | 1,85,951 | 7,946.11 | 10,408.51 |

| 2. | Arunachal Pradesh | 17,411 | 406.50 | 485.19 |

| 3. | Assam | 1,55,251 | 5,296.16 | 6,814.88 |

| 4. | Bihar | 1,68,073 | 5,423.78 | 7,297.47 |

| 5. | Chandigarh** | 10,968 | 630.45 | 836.18 |

| 6. | Chhattisgarh | 2,96,468 | 7,317.75 | 9,428.50 |

| 7. | Goa | 32,450 | 1,394.32 | 1,756.79 |

| 8. | Gujarat | 2,17,338 | 7,331.63 | 9,531.89 |

| 9. | Haryana | 1,71,028 | 6,807.18 | 9,071.93 |

| 10. | Himachal Pradesh | 93,260 | 3,865.18 | 4,716.86 |

| 11. | J & K | 1,22,831 | 3,541.61 | 4,525.77 |

| 12. | Jharkhand | 1,08,136 | 4,226.41 | 5,814.52 |

| 13. | Karnataka | 2,40,767 | 8,304.64 | 11,426.90 |

| 14. | Kerala | 1,25,480 | 2,164.48 | 2,558.24 |

| 15. | Madhya Pradesh | 4,87,695 | 12,703.13 | 16,465.36 |

| 16. | Maharashtra | 3,14,158 | 12,019.46 | 14,936.13 |

| 17. | Manipur | 41,973 | 971.69 | 1,252.80 |

| 18. | Meghalaya | 14,554 | 333.18 | 411.49 |

| 19. | Mizoram | 7,985 | 211.56 | 250.44 |

| 20. | Nagaland | 21,073 | 402.80 | 476.23 |

| 21. | Odisha | 1,64,378 | 4,406.22 | 5,662.72 |

| 22. | Puducherry** | 13,207 | 729.50 | 970.02 |

| 23. | Punjab | 1,82,190 | 6,740.35 | 8,931.20 |

| 24. | Rajasthan | 4,81,493 | 16,897.74 | 22,118.90 |

| 25. | Sikkim | 15,344 | 443.08 | 577.30 |

| 26. | Telangana | 1,53,764 | 5,449.12 | 7,372.21 |

| 27. | Uttarakhand | 80,962 | 4,005.84 | 5,410.68 |

| 28. | Uttar Pradesh | 6,26,116 | 13,800.19 | 17,280.20 |

| 29. | Tamil Nadu* | 187 | 18.25 | 20.75 |

| 30. | Tripura | 652 | 3.76 | 4.47 |

| 31. | West Bengal* | 330 | 23.47 | 34.09 |

| Total | 45,51,473 | 1,43,815.54 | 1,86,848.62 |

Source: PFRDA.

Note: *: Executed agreement with CRA and NPS trust only for All India Service officer.

**: Status included under the State Government.

Major steps taken during FY 2019-20

It has been decided to introduce the following options for Central Government NPS subscribers (change in the Pension Funds or investment pattern is allowed in respect of incremental flows only):

a. Choice of Pension Fund: As in the case of subscribers in the private sector, the Government subscribers shall also be allowed to choose any one of the pension funds including Private sector pension funds. They could change their option once in a year. However, the current provision of combination of the Public-Sector Pension Funds will be available as the default option for both existing as well as new Government subscribers.

b. Choice of Investment pattern: Government employees may exercise one of the following choices of Investment Pattern twice in a financial year :

- The existing scheme in which funds are allocated by the PFRDA among the three Public Sector Undertaking fund managers based on their past performance in accordance with the guidelines of PFRDA for Government employees shall continue as default scheme for both existing and new subscribers.

- Government employees who prefer a fixed return with minimum amount of risk shall be given an option to invest 100 per cent of the funds in Government securities.

- Government employees who prefer higher returns shall be given the options of the following two Life Cycle based schemes:

> Conservative Life Cycle Fund with maximum exposure to equity capped at 25 per cent.

> Moderate Life Cycle Fund with maximum exposure to equity capped at 50 per cent.

for Life insurance has declined from 2011, whereas for the non-life insurance has increased consistently and is 2.74 percent for Life Insurance and 0.97 per cent for Non-Life insurance in 2018 (Table 8 and 9). Globally insurance penetration and density were 3.31 per cent and US$ 370 for the life segment and 2.78 per cent and US$ 312 for the non-life segment respectively in 2018.

4.38. During 2018-19, the gross direct premium of Non-Life insurers was Rs.1.69 lakh crore, as against Rs.1.51 lakh crore in 2017-18, registering a growth of 12.47 per cent. Motor and health segments primarily helped the industry report this growth. Life insurance industry recorded a premium income of Rs.5.08 lakh crore in 2018-19 as against Rs.4.59 lakh crore in the previous financial year, registering a growth of 10.75 per cent.

While renewal premium accounted for 57.68 per cent of the total premium received by the life insurers, new business contributed the remaining 42.32 per cent.

INSOLVENCY AND BANKRUPTCY CODE

Important Developments

4.39. Three years into operation, the regime under the Insolvency and Bankruptcy Code (IBC) boasts of a strong ecosystem, comprising the Adjudicating Authority, the IBBI, three insolvency professional agencies, 11 registered valuer organisations and 2,374 registered valuers7 and 2,911 insolvency professionals (as on December 31, 2019). The debtors and

Table 8: Penetration in Life Insurance

| Particulars | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| Insurance Penetration (in per cent) | 3.40 | 3.17 | 3.10 | 2.60 | 2.72 | 2.72 | 2.76 | 2.74 |

| Insurance Density (in US$) | 49.0 | 42.7 | 41.0 | 44.0 | 43.2 | 46.5 | 55.0 | 55.0 |

Table 9: Penetration in Non-Life Insurance

| Particulars | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| Insurance Penetration (in per cent) | 0.70 | 0.78 | 0.80 | 0.70 | 0.72 | 0.77 | 0.93 | 0.97 |

| Insurance Density (in US$) | 10.0 | 10.5 | 11.0 | 11.0 | 12.0 | 13.2 | 18.0 | 19.0 |

Source: SwissRe, Sigma various issues.

creditors alike are initiating the processes under the Code with 2,542 corporates, some of them having very large nonperforming assets account, and undergoing corporate insolvency resolution process. Upto September 2019, about 743 of them have completed the process yielding either resolution or liquidation and 498 corporates have commenced voluntary liquidation process8. Out of the 562

Corporate Insolvency Resolution Process (CIRPs) initiated in October-December 2019, 132 are under liquidation, and 14 have been already settled (Table 10). As on end December 2019, `1.58 lakh crore were realizable in cases resolved (Table 11).

4.40. These cases have been filed under various sectors. 41.2 per cent of the cases admitted by NCLT for CIRP are in

Table 10: Quarterly trends of cases

| Quarterly trends of cases | April-Jun 2019 | July-Sep 2019 | Oct-Dec 2019 |

| Total No. of CIRPs initiated/admitted during the quarter | 300 | 565 | 562 |

| Total No. of cases in which resolution plan has been approved during the quarter | 27 | 32 | 30 |

| Total No. of cases withdrawn during the quarter | 24 | 18 | 5

|

| Total No. of cases settled during the quarter | 22 | 24 | 14

|

| Total No. of cases under liquidation during the quarter | 96 | 153 | 132

|

| Category wise distribution (Financial creditor, Operational Creditor, Corporate Debtor) of all the admitted cases in which CIRP has been initiated. | Financial Creditor-129 Operational Creditor- 154 Corporate Debtor-17 | Financial Creditor-265 Operational Creditor-291 Corporate Debtor-9 | Financial Creditor-245 Operational Creditor-301 Corporate Debtor-16 |

Source: IBBI.

Table 11: Realisable value for cases resolved under Corporate Insolvency Resolution Processes (Amount in ` Crore)

| April-June 2019 | July- September 2019# | October- December 2019## | |

| Overall realisable value by Financial Creditors and Operational Creditors in cases resolved | 7,331.90 | 27,534.48 | 1,900.52 |

| Total realisable value till the end of respective quarters | 1,28,095.16 | 1,55,861.99 | 1,57,762.51 |

Source: IBBI.

Note: # : Data of 1 case awaited.

## : Data of 8 cases awaited.

Cases are included as per the date of NCLT orders rather than date of final payment.

manufacturing sector followed by 19 per cent in Real Estate, Renting and Business Activities sector (Table 12).

4.41. The Government has been proactively addressing the issues that come up in implementation of the reform. Since its enactment in 2016, the Code has been amended three times, within a short span of time, mainly to streamline the processes and address any lacuna to ensure proper operationalizing of the provisions of the Code.

4.42. The first amendment introduced section 29A, which deals with the provision introduced to bar promoters from bidding for their own companies. It prevented defaulters from regaining control of their companies at a cheaper value. The second amendment introduced section 12A to provide creditors option to withdraw insolvency application within 30 days of filing the petition. The amendment also stated that home buyers shall be treated as financial creditors to give home buyers a voice in the insolvency proceedings as they, also provide funding for projects by making advance payments, and to discourage real estate developers from defaulting on commitments not only to banks but also to their customers. The third amendment primarily focused upon the revival of a CD by ensuring timely admission and completion

Table 12: Sector-wise breakup of the total cases admitted by NCLT for CIRP during the quarter

| Sector* | April-Jun 2019 | July-Sep 2019 | Oct-Dec 2019 |

| Extraterritorial organizations and bodies | 1 | 4 | 3 |

| Agriculture, Hunting and Forestry | 9 | 18 | 15 |

| Construction | 28 | 64 | 65 |

| Education | 2 | 1 | 2 |

| Electricity, Gas And Water Supply | 7 | 23 | 22 |

| Financial Intermediation | 4 | 6 | 5 |

| Health And Social Work | 3 | 5 | 9 |

| Hotels And Restaurants | 8 | 12 | 12 |

| Manufacturing | 125 | 208 | 232 |

| Mining and Quarrying | 2 | 5 | 5 |

| Other Community, Social And Personal Service Activities | 4 | 5 | 7 |

| Others | 4 | 8 | 8 |

| Real Estate, Renting And Business Activities | 62 | 125 | 109 |

| Transport, Storage And Communications | 8 | 22 | 12 |

| Wholesale And Retail Trade; Repair Of Motor Vehicles, Motorcycles And Personal And Household Goods | 33 | 59 | 55 |

| Fishing | 0 | 0 | 1 |

| Grand Total | 300 | 565 | 562 |

Source: IBBI.

Note: *The distribution is based on the CIN of Corporate Debtors (CDs) as per the National Industrial Classification 2004.

of the resolution process. The amendment ensures that 14 days period deadline given to the NCLT for admitting or rejecting a resolution application shall be strictly adhered to. The amendment further specifying the mandatory time frame of 330 days to complete the Corporate Insolvency Resolution Process (CIRP) without exception, tries to instill discipline amongst the stakeholders to avoid inordinate delays in the insolvency resolution process. The Government also reaffirms its stance as a facilitator in the third amendment by specifically making a resolution plan binding on the Central Government, State Governments or a local authority to whom debt in respect of payment of dues is owed.

4.43. IBBI has conceptualized a 24-month Graduate Insolvency Programme. There are 2,911 Insolvency Professionals registered as on December 31, 2019 (Table 13). The Indian Institute of Corporate Affairs commenced the first batch of GIP on July 1, 2019.

4.44. The resolution under IBC has been much higher as compared to other processes. As per the data provided in Report on Trend and Progress of Banking in India 2018-19, the amount recovered as a percentage of amount involved in 2017-18 and 2018-19 has been much higher as compared to Lok Adalat, DRTs etc (Table 14). The Code provides a timeline of 330 days to conclude a CIRP. This push has meant that proceedings under the Code take on average about 340 days, including time spent on litigation, in contrast with the previous regime where processes took about 4.3 years.

Table 13: Insolvency Professionals registered as on December 31, 2019

| City / Region | Indian Institute of Insolvency Professionals of ICAI | ICSI Institute of Insolvency Professionals |

Insolvency Professional Agency of Institute of Cost Accountants of India |

Total |

| New Delhi | 355 | 223 | 60 | 638 |

| Rest of Northern Region | 287 | 161 | 46 | 494 |

| Mumbai | 340 | 114 | 31 | 485 |

| Rest of Western Region | 208 | 89 | 29 | 326 |

| Chennai | 113 | 72 | 11 | 196 |

| Rest of Southern Region | 288 | 153 | 43 | 484 |

| Kolkata | 169 | 34 | 16 | 219 |

| Rest of Eastern Region | 50 | 18 | 5 | 73 |

| Total Registered | 1,810 | 864 | 241 | 2,915 |

| Cancellations | 1 | 3 | 0 | 4 |

| Registered as on 31st December 2019 | 1,809 | 861 | 241 | 2,911 |

Source: IBBI.

Table 14: NPAs of SCBs recovered through various channels

Amount in Rs.crore

|

Recovery Channel |

2017-18 | 2018-19(P) | ||||||

| No. of cases referred | Amount involved | Amount re covered* | Col. (4) as percent of Col. (3) | No. of cases referred | Amount involved | Amount re covered* | Col. (8) as per cent of Col. (7) | |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| Lok Adalats | 3317897 | 45728 | 1811 | 4.0 | 4080947 | 53506 | 2816 | 5.3 |

| DRTs | 29345 | 133095 | 7235 | 5.4 | 52175 | 3066499 | 10574 | 3.5 |

| SAR FAESI Act | 91330 | 81897 | 26380 | 32.2 | 248312 | 289073 | 41876 | 14.5 |

| IBC | 704@ | 9929 | 4926 | 49.6 | 1135@ | 166600 | 70819 | 42.5 |

| Total | 3439276 | 270631 | 40352 | 14.9 | 4382569 | 815678 | 126085 | 15.5 |

Source: Report on Trend and Progress of Banking in India 2018-19 (which sourced from Off-site returns, RBI and IBBI).

Notes: P : Provisional.

* : Refers to the amount recovered during the given year, which could be with reference to the cases referred during the given year as during the earlier year.

DRTs: Debt Recovery Tribunals; SARFAESI Act: The Securitisation and Reconstruction of Financial Assets and Enforcement of Securities Interest Act, 2002.

@ : Cases admitted by National Company Law Tribunals (NCLTs).

Figures relating to IBC for 2017-18 and 2018-19 are calculated by adding quarterly numbers from IBBI newsletters.

CHAPTER AT A GLANCE

> Monetary policy remained accommodative in 2019-20.

> The repo rate was cut in four out of five meetings held in 2019-20 (till December). The repo rate has been cut by 110 bps in 2019-20 so far.

> Bank credit growth slowed down in 2019-20 and stands at 7.1 per cent (YoY) as of December 20, 2019, as compared to a growth of 12.9 per cent in April 2019.

> The growth (YoY) of loans from NBFCs declined from 27.6 per cent in September 2018 and 21.6 per cent in December 2018 to 9.9 per cent at end September 2019.

> Gross NPA ratio of SCBs remained unchanged at 9.1 per cent between March and September 2019.

> Systemic liquidity has been largely in surplus in 2019-20. Weighted Average Call Money Rate remeined mostly close to repo rate within the Liquidity Adjustment Facility (LAF) corridor.

> Nifty 50 and S&P BSE Sensex indices reached record high closing of 12,355 and 41,952 respectively during 2019-20 (upto January 16, 2020).

> The total money raised by public issue and rights increased to Rs.73,896 crore in 2019-20 (up to December 31, 2019) from Rs. 44,355 crore in the corresponding period last year. Rs.6.29 lakh crore was raised through private placements in 2019-20 (up to December 31, 2019) as compared to Rs.5.3 lakh crore in the corresponding period of previous year.

> As on end December 2019, Rs. 1.58 lakh crore were realizable in cases resolved under Corporate Insolvency Resolution Processes. The proceedings under IBC take on average about 340 days, including time spent on litigation, in contrast with the previous regime where processes took about 4.3 years.

Notes:-

1. Data for September 2019 is provisional.

2. Data for September 2019 is provisional.

3. The post-crisis G20 and Basel reforms in the OTC derivatives market require non-centrally cleared derivative transactions to be subject to higher capital requirements relative to transactions intermediated through a CCP.

4. The post-crisis G20, Basel and International Organization of Securities Commissions (IOSCO) reforms in the OTC derivatives market require counterparties to exchange ‘margin’ (collateral) for non-centrally cleared derivative transactions.

5. There are two types of margins based on two kinds of counterparty exposure in OTC derivative transactions. Variation margin protects a counterparty from current exposure based on the MTM value of the derivative at any point in time. Initial marginprotects a counterparty from potential future exposure due to changes in the MTM value of the derivative contract during the time it takes to close out and replace the position in the event of default by the counterparty.

6. These estimates are for initial margin. Capital needs would be much higher if variation margin estimates are included.

7. Data as on September 30, 2019, published in IBBI Quarterly Newsletter for the quarter July-September, 2019.

8. Data as on September 30, 2019, published in IBBI Quarterly Newsletter for the quarter July-September, 2019.