Foreign Trade Policy 2015-20 and other schemes provide promotional measures to boost India’s exports with the objective to offset infrastructural inefficiencies and associated costs involved to provide exporters a level playing field.

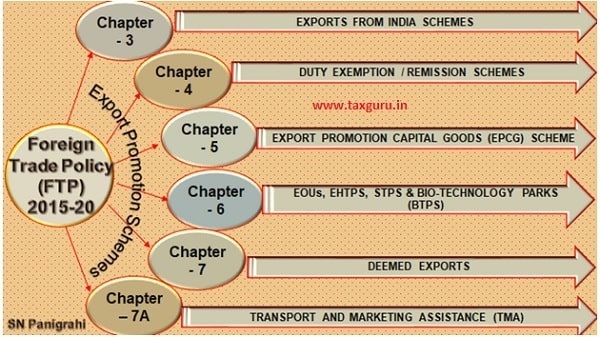

At present there are multiple export promotion schemes as per FTP – 2015-20, as shown below, but none of the schemes meets all the genuine requirements of the exporters and completely off-setting various types of hidden costs associated with the Exports. Exporters are also not fully able to avail all the export benefits entitled to them, because of procedural formalities and ignorance. Therefore, making Indian Exports Uncompetitive.

There are also uncertainty and confusion over continuity of most of the schemes in view of recent withholding of WTO panel, that India’s Export Subsidy Programs Violate WTO Pact, as a result, exporters are unable to plan for the longer period.

US Challenged Indian Export Promotion Schemes in WTO

A WTO Dispute Settlement Panel has upheld a US Complaint that Export Subsidy Program provided by the Indian Government Violated Provisions of the Trade Body’s Subsidies and Countervailing Measures (SCM) pact. The Ruling, which has been shared with the two parties in the dispute, will be released to all the WTO members around 10th October, 2019.

The three-member dispute settlement panel comprising Jose Antonio S. Buencamino, Leora Blumberg and Serge Panatier has stuck down Indian Export Promotion Schemes on the grounds that India is not entitled to provide such subsidies because its per Capita National Product (GNP) has crossed $ 1,000 per annum.

In 2018, the US complained that India’s Export-Related Programs violated Article .1(a) of WTO’s Subsidies and Countervailing Measures (SCM) Agreements. Under Article 3.1, Developing Countries with per Capita Gross National Product (GNP) of US$ 1,000 per annum are not entitled to provide Export subsidies that are Contingent upon Export Performance.

US that had claimed that India offered illegal export subsidies and “thousands of Indian companies are receiving benefits totaling over $7 billion annually from these programs”.

According to a WTO notification in 2017, India crossed the per-capita GNI threshold for three straight years through 2015 — to $1,178 in 2015 from $1,051 in 2013.

India has maintained that in 2015 it had announced it would discontinue Export Subsidies soon. Subsequently, the government made another announcement in 20017 that it would end the Export Subsidies. Despite these pronouncements, the government has continued with Export Subsidies. India has argued that as countries that were already above $1,000 were given eight years to adjust to the new regime, it should also get similar time to change its exports policy.

After the Panel’s Report made public, India will have a month to Challenge the Ruling before an Appellate Body, the Highest Court for Global Trade Disputes. If the Appellate Body upholds the Panel’s Ruling, India will be required to Discontinue the Existing Export Promotion Schemes within a mutually-agreed-upon (with the US, in this case) time frame, which is often a year.

WTO Subsidies and Countervailing Measures (SCM)

WTO SCM Agreement contains a definition of the term “subsidy”. The definition contains three basic elements:

(i) a financial contribution

(ii) by a government or any public body within the territory of a Member

(iii) which confers a benefit.

All three of these elements must be satisfied in order for a subsidy to exist.

In order for a financial contribution to be a subsidy, it must be made by or at the direction of a government or any public body within the territory of a Member. Thus, the SCM Agreement applies not only to measures of national governments, but also to measures of sub-national governments and of such public bodies as state-owned companies.

A financial contribution by a government is not a subsidy unless it confers a “benefit.”. Article 14 of the SCM Agreement provides some guidance with respect to determining whether certain types of measures confer a benefit.

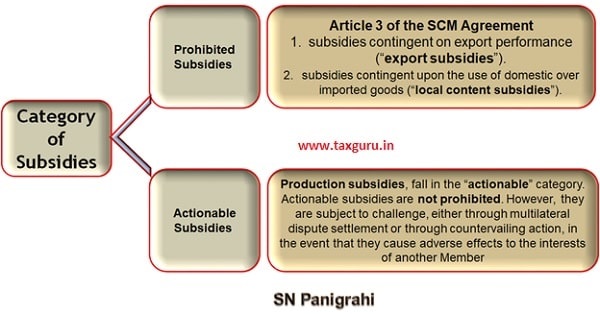

Categories of Subsidies

The SCM Agreement creates two basic categories of subsidies: those that are prohibited, those that are actionable (i.e., subject to challenge in the WTO or to countervailing measures). All specific subsidies fall into one of these categories.

Prohibited subsidies

Two categories of subsidies are prohibited by Article 3 of the SCM Agreement.

The first category consists of subsidies contingent, in law or in fact, whether wholly or as one of several conditions, on export performance (“export subsidies”). A detailed list of export subsidies is annexed to the SCM Agreement.

The second category consists of subsidies contingent, whether solely or as one of several other conditions, upon the use of domestic over imported goods (“local content subsidies”).

These two categories of subsidies are prohibited because they are designed to directly affect trade and thus are most likely to have adverse effects on the interests of other Members.

Actionable subsidies

Most subsidies, such as production subsidies, fall in the “actionable” category. Actionable subsidies are not prohibited. However, they are subject to challenge, either through multilateral dispute settlement or through countervailing action, in the event that they cause adverse effects to the interests of another Member.

There are three types of adverse effects.

First, there is injury to a domestic industry caused by subsidized imports in the territory of the complaining Member. This is the sole basis for countervailing action.

Second, there is serious prejudice. Serious prejudice usually arises as a result of adverse effects (e.g., export displacement) in the market of the subsidizing Member or in a third country market. Thus, unlike injury, it can serve as the basis for a complaint related to harm to a Member’s export interests.

Finally, there is nullification or impairment of benefits accruing under the GATT 1994. Nullification or impairment arises most typically where the improved market access presumed to flow from a bound tariff reduction is undercut by subsidization.

Countervailing Measures

Part V of the SCM Agreement sets forth certain substantive requirements that must be fulfilled in order to impose a countervailing measure, as well as in-depth procedural requirements regarding the conduct of a countervailing investigation and the imposition and maintenance in place of countervailing measures. A failure to respect either the substantive or procedural requirements of Part V can be taken to dispute settlement and may be the basis for invalidation of the measure.

Substantive rules

A Member may not impose a countervailing measure unless it determines that

1. there are subsidized imports, injury to a domestic industry, and

2. a causal link between the subsidized imports and the injury.

As previously noted, the existence of a specific subsidy must be determined in accordance with the criteria in Part I of the Agreement.

Continuing with present Export Promotion Schemes, which falls under the term Subsidy, may attract Countervailing measures in the hands of Importing Countries, thereby makes our Export uncompetitive.

US Pressure Tactics:

The ruling comes at an Opportune time for Washington, which is pilling pressure on New Delhi to open the Indian market for Medical Products, particularly Stents and Knee Implants, Dairy Items and other products, as part of an interim trade deal.

US could now use the dispute panel’s findings to put moral pressure on India to extract greater market access for the above products.

Export Promotion Schemes that could be Affected

The Programs that could be affected are Export Oriented Units Scheme, Electronic Hardware Technology Parks Scheme, Merchandize Exports from India (MEIS), Export Promotion Capital Goods (EPCG) Scheme, Special Economic Zones (SEZ) and Duty Free Import Authorization (DFIA) Scheme

Testing Time for Many Agriculture Export Schemes

The US has questioned subsidies provided to rice and wheat, while Brazil, Australia and Guatemala have gone a step further and have initiated disputes against India’s sugarcane subsidies.

Three more countries, Thailand, Costa Rica and the Russian Federation have joined the dispute as third parties. The complainants argue that India has substantially increased production-related subsidies for sugarcane provided by both the Central and State governments and, as a result, the country has breached its commitment to limit sugarcane subsidies.

The complainants also argue that the Central and State governments provide subsidies for exporting sugar, which it cannot under the AoA rules, since these subsidies were notified to the WTO.

Other Export Promotion Schemes are also being Challenged:

The US and Australia have raised doubts about India’s new farm sector support scheme, Transport and Marketing Assistance (TMA) announced in March this year, at the World Trade Organization (WTO) saying it was trade distorting and perhaps, inconsistent with global norms.

The “Transport and Marketing Assistance” (TMA) for specified agriculture products scheme aims to provide assistance for the international component of freight and marketing of agricultural produce which is likely to mitigate disadvantage of higher cost of transportation of export of specified agriculture products due to trans-shipment and to promote brand recognition for Indian agricultural products in the specified overseas markets.

The Scheme would be applicable for a period as specified from time to time. Presently the Scheme would be available for exports effected from 1.3.2019 to 31.03.2020

This is the latest scheme to come under attack along with the Pradhan Mantri Kisan Samman Nidhi (PM-KISAN) scheme that has been questioned by New Zealand even though Australia and the European Union have supported it.

New Foreign Trade Policy Should be in-line with WTO Norms

In backdrop of Severe Challenges in WTO, the government is recasting the incentives to make them compliant with global trade rules. The Commerce Ministry wants to make incentives compliant with WTO trade rules.

The Commerce Ministry will soon come out with a new foreign trade policy, which provides guidelines and incentives for increasing exports for the next five financial years 2020-25

The Commerce Ministry has also floated a cabinet note for a new export incentives scheme — Rebate of State and Central Taxes and Levies (RoSCTL) — that would be compliant with the WTO norms.

The RoSCTL scheme is available for exports of garments and made-ups. It would now be proposed to extend it to all exports in a phased manner.

The new scheme would replace the existing MEIS, which was challenged by the US last year in the WTO. It would ensure refund of all un-rebated central and state levies and taxes imposed on inputs that are consumed in exports of all sectors.

Major un-rebated levies are: state VAT/ central excise duty on fuel used in transportation, captive power, farm sector, mandi tax, duty of electricity, stamp duty on export documents, purchases from unregistered dealers, embedded CGST and compensation cess coal used in the production of electricity.

“The thrust of the new foreign trade policy would be to boost exports of goods and services which are bought in large values by the world and where India has strong competitiveness. The launch of the new foreign trade policy will also include the state of art information technology (IT) systems with end-to-end integration with all agencies.

These measures may ease out Export related Procedural Hardships and encourage exports.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST & Foreign Trade Consultant, Practitioner, Corporate Trainer & Author.

Available for Corporate Trainings & Consultancy

Can be reached @ snpanigrahi1963@gmail.com

Author Bio