Case Law Details

Akhil Maheshwari Vs Commissioner of Customs (CESTAT Kolkata)

The appeals challenged an order that absolutely confiscated gold bars and imposed penalties on the appellants under the Customs Act, 1962.

The case arose after officers of the Directorate of Revenue Intelligence (DRI), Kolkata, acting on intelligence, intercepted Shri Anil Kumar Yadav on 9 August 2020 while he was boarding the New Delhi–Howrah COVID-19 AC Special Train at Howrah Railway Station. During a personal search, officers recovered four rectangular gold bars and twelve small cut pieces of gold weighing 3,651.3 grams and valued at ₹2,07,75,897, concealed in a cloth belt tied around his waist. As he could not produce documents supporting lawful possession or transport of the gold, the gold and two mobile phones were seized on the belief that the gold was of foreign origin and smuggled.

In his voluntary statement, Shri Anil Kumar Yadav stated that he had travelled to Kolkata on the instructions of Shri Akhil Maheshwari to transport the gold. He further stated that a person known as “Mr. Goldy” handed over the gold to him and that he intended to carry it from Kolkata to Meerut. He was subsequently arrested.

Later, Shri Nikhil Maheshwari claimed ownership of the seized gold by submitting job work challans issued by M/s Pooja Jewellers along with the firm’s gold register. M/s Pooja Jewellers was a proprietorship concern owned by Smt. Pooja Maheshwari, who had authorised Shri Akhil Maheshwari to act on behalf of the firm.

A show cause notice was issued proposing confiscation of the gold and penalties on Shri Anil Kumar Yadav, Shri Akhil Maheshwari, and Shri Nikhil Maheshwari. In their reply, the appellants stated that M/s Pooja Jewellers was a registered business engaged in dealing with gold and that the seized gold had been lawfully purchased through valid tax invoices. They produced GST invoices, GST returns, stock registers, purchase registers, banking transaction details, and job work challans. They explained that the gold had been purchased under valid invoices, melted into bar form for manufacturing ornaments, and sent to Kolkata for job work before being intercepted during transportation back to Meerut.

The adjudicating authority nevertheless ordered absolute confiscation of the gold under Sections 111(b) and 111(d) of the Customs Act, 1962, and imposed penalties of ₹20 lakh each on the three noticees. The Commissioner (Appeals) upheld the order, leading to the present appeals.

Before the Tribunal, the appellants argued that the difference between the CRCL test report showing 99.6% purity and the purchase invoices mentioning 99.5% purity could not justify rejection of their claim. They contended that they had discharged the burden of proof under Section 123 of the Customs Act by producing documentary evidence establishing lawful procurement and movement of the gold.

The Tribunal found that there was no dispute regarding the recovery of the gold from Shri Anil Kumar Yadav. However, it noted that the ownership of the gold had been claimed by M/s Pooja Jewellers and that the appellants had produced purchase registers, purchase invoices, GST returns, and job work challans showing that the gold formed part of the firm’s stock.

The Tribunal observed that the gold was duty-paid, GST had been paid, and the transactions were reflected in the books of accounts. It held that the adjudicating authority had discarded these documents without proper consideration. The Tribunal concluded that the appellants had discharged the burden cast upon them under Section 123 of the Customs Act.

It further noted that the gold did not bear any foreign-origin markings and that the case involved a town seizure. The appellants had also produced documents supporting lawful procurement of the gold, and these formed part of the record. In these circumstances, the Tribunal held that it could not be concluded that the gold was of foreign origin or smuggled.

Accordingly, the Tribunal held that the gold was not liable for confiscation. Since confiscation itself was unsustainable, the penalties imposed on the appellants also could not survive.

The Tribunal set aside the impugned order, directed the authorities to release the seized gold to the appellants, and allowed all three appeals with consequential relief.

FULL TEXT OF THE CESTAT KOLKATA ORDER

The appellants are in appeals against the impugned order wherein the gold bars have been absolutely confiscated and various penalties were imposed on the appellants.

The facts of the case are that the DRI, Kolkata, on the basis of intelligence, intercepted Shri Anil Kumar Yadav on 09.08.2020 at about 16.15 hrs, while he was on board to travel by New Delhi–Howrah Covid-19 AC Special Train No. 02302 at Coach B5, Berth No. 60, at Platform No. 09 of Howrah Railway Station.

2.1 DRI officers asked Shri Anil Kumar Yadav whether he was carrying any gold with him and on his affirmation, he was offered to be present for the purpose of search at DRI Office at 8 Ho Chi Minh Sarani, Kolkata–700071.

2.2 On personal search of Shri Anil Kumar Yadav, a white-green checked cloth belt was found tied around his waist, from which 04 (Four) pieces of rectangular shaped gold bars and 12 small cut pieces of gold, totally weighing 3651.3 grams, valued at Rs. 2,07,75,897/-, were recovered.

2.3 As Shri Anil Kumar Yadav could not produce any licit documents in support of possessing, carrying, transporting or dealing with the said gold, the same were seized on reasonable belief that the said gold is of foreign origin and smuggled one. Two mobile phones recovered from the possession of Shri Anil Kumar Yadav were also seized.

2.4 Shri Anil Kumar Yadav in his voluntary statements dated 09.08.2020 stated, inter alia, that as per instruction of Shri Akhil Maheshwari he had come to Kolkata by New Delhi-Howrah (02302) COVID-19 AC Special on 09.08.2020 to carry the gold.

2.5 Shri Anil Kumar Yadav also stated that a person known as Mr. Goldy handed over him the said gold and he came back to Howrah Station to board (02301) New Delhi-Howrah COVID-19 AC Special which was scheduled for departure at 04:45 PM to carry the same from Kolkata to Meerut.

2.6 Shri Anil Kumar Yadav was arrested on 09.08.2020 and produced before the Chief Metropolitan Magistrate, Kolkata on 10.08.2020.

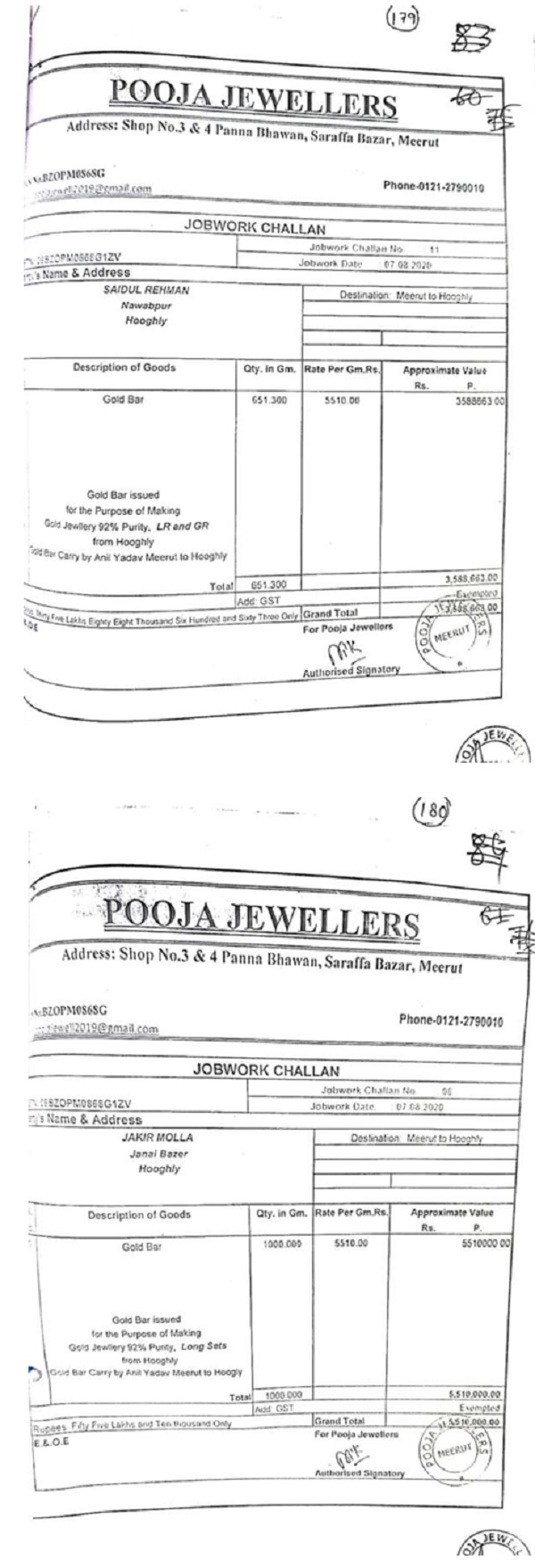

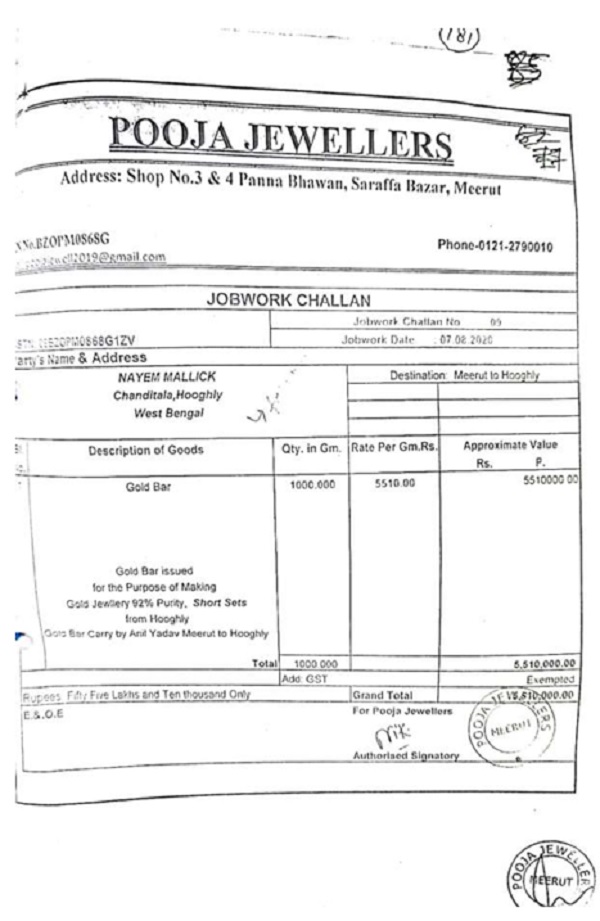

2.7 On 25.09.2020 Shri Nikhil Maheshwari vide a letter addressed to the Assistant Commissioner (Preventive), CC(P), WB, Kolkata, claimed the ownership of the seized gold by submitting “Jobwork Challan” No. 11, 10, 08, 09 all dated 07.08.2020 issued by POOJA JEWELLERS, Shop No. 3 & 4, Panna Bhawan, Saraffa Bazar, Meerut. Shri Nikhil Maheshwari also submitted the register for gold maintained by POOJA JEWELLERS.

2.8 The proprietor of POOJA JEWELLERS is Smt. Pooja Maheshwari, w/o Shri Akhil Maheshwari and Smt. Pooja Maheshwari has authorized Shri Akhil Maheshwari to act on behalf of her for the firm.

2.9 After due process, the department issued Show Cause Notice dated 03.01.2021 to Shri Anil Kumar Yadav, Shri Akhil Maheshwari and Shri Nikhil Maheshwari with a proposal to confiscate the seized gold along with imposition of penalty upon the noticees.

2.10 In the written reply dated 15.04.2024, Shri Akhil Maheshwari and Shri Nikhil Maheshwari submitted the following:

(i) That Shri Akhil Maheshwari and Shri Nikhil Maheshwari are the authorized signatory of M/s POOJA JEWELLERS, registered under proper trade license and the said firm is engaged in purchase and sale of gold and gold items. As the business activity of the firm is managed by Akhil Maheshwari, he has made the claim for the seized gold on behalf of the firm.

(ii) That the goods were not of foreign origin but were rather locally procured under licit invoices. In corroboration of the claim, he had submitted GST invoice, GST returns, stock registers, purchase registers, banking transaction details and job work challan.

(iii) that the seized gold was purchased by the firm under proper invoices and later on melted into bar forms for the purpose of crafting them into ornaments. Accordingly, 3651.300 gms of gold was given to Shri Anil Kumar Yadav for getting the task executed from job workers at Kolkata. However, when Shri Anil Kumar Yadav was on his way back to Meerut, the subject goods were arbitrarily intercepted and seized.

2.11 The case was adjudicated by the Additional Commissioner, CC(P), WB by way of absolute confiscation of the seized gold under the provision of Section 111(b) and 111(d) of the Customs Act, 1962 and imposition of penalty of Rs. 20 Lakh each on Shri Anil Kumar Yadav, Shri Akhil Maheshwari & Shri Nikhil Maheshwari.

2.12 Being aggrieved the said Order-in-Original, the appellant filed appeal before the Commissioner of Customs (Appeals) and Commissioner of Customs (Appeals) vide order dated 31.10.2025 rejected their appeal.

2.12 Being aggrieved with the said Order-in-Appeal dated 31.10.2025, the appellants are before us.

3. The ld. Counsel for the appellants submits that purity of seized gold bars as per CRCL test report is 99.6%, whereas, the tax invoices produced by the appellants, the purity of the gold bar is mentioned as 99.5%. The same cannot, by itself, be treated as a valid ground to reject the claim of lawful procurement. He further submits that the appellants have duly complied with the burden of proof by furnishing the documentary evidence including tax invoices and job work challans which corroborates the lawful procurement and movement of the gold. In support of his contention, he relies on the following case laws :

(i) Om Sai Trading reported in [2020 (372) E.L.T. 542 (Pat) ;

(ii) Madhukar Sonaba Bhagat reported in [2019(368) E.L.T. 990 (Tri.-Kolkata)] ;

(iii)Sri Samir Kumar Roy & Others v. CC (Prev.) West Bengal – [2001 (135) E.L.T. 1036 (T)] ;

(iv) Ajit Bhosle reported in 2020 (374) E.L.T. 814 (Tri.-Kolkata);

3.1 He therefore submits that Ratio of the above case laws are squarely applicable in the present case. He, therefore, prays for setting aside the impugned order by allowing their appeals with consequential benefits.

4. Heard the ld. A. R. for the Revenue, who has justified the impugned order.

5. Heard both the parties and considered the submissions.

6. We find that the facts are not in dispute that the appellant, Shri Anil Kumar Yadav, was intercepted on 09.08.2020 at about 04.15 pm, who was boarding train from Howrah Station and he was carrying four pieces of gold bars and 12 small cut pieces of gold totally weighing 3651.3 grams. Although, Shri Yadav was not having any licit documents in support of possessing the said gold. In his statement, he stated that he came to Howrah on the instruction of Shri Akhil Maheshwari to carry the gold and Shri Nikhil Maheshwari, who was the partner of M/s Pooja Jewellers, claimed the ownership of the gold. In fact, M/s Pooja Jewellers was the proprietorship concern owned by Smt. Pooja Maheshwari wife of Shri Akhil Maheshwari. Shri Akhil Maheshwari was authorised to act on behalf of Smt. Pooja Maheshwari for the firm.

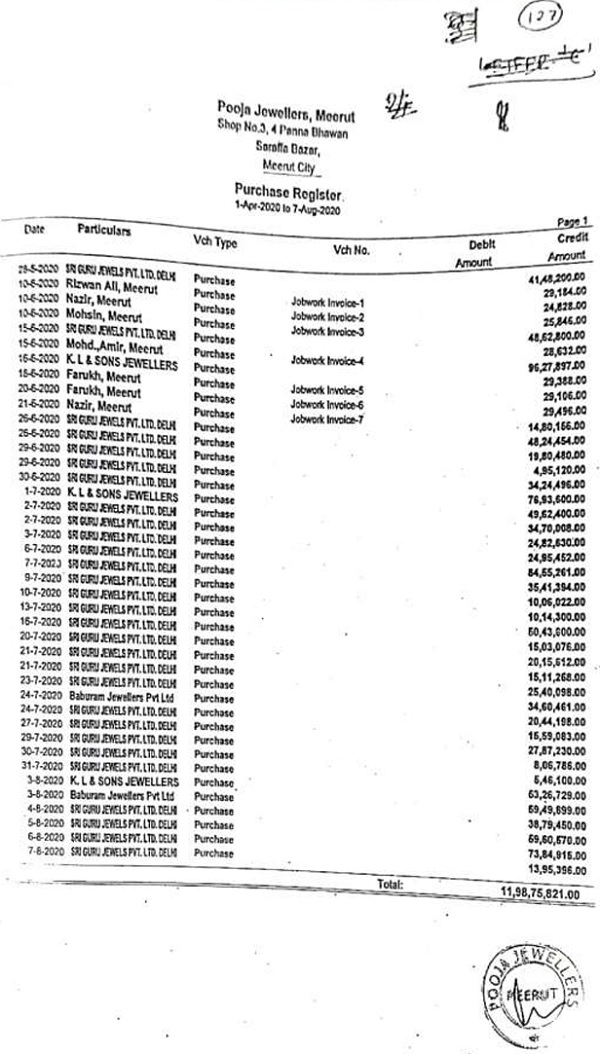

7. In support of their ownership of the gold, they produced the purchase register, which is extracted below :

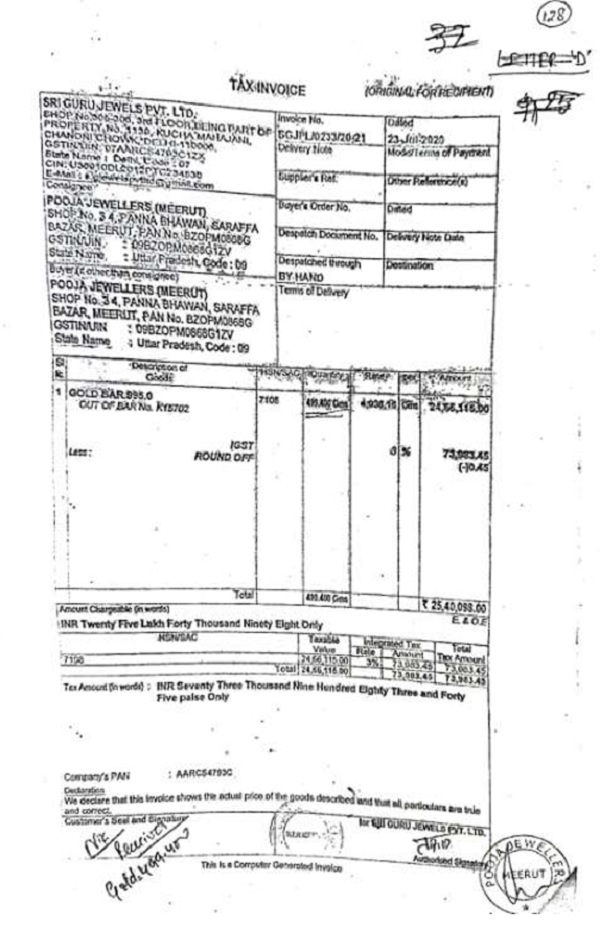

which shows that the appellants were having the impugned gold in stock and also filed the purchase invoice for procuring the said gold. For better appreciation of facts, one of the Invoice is extracted below :

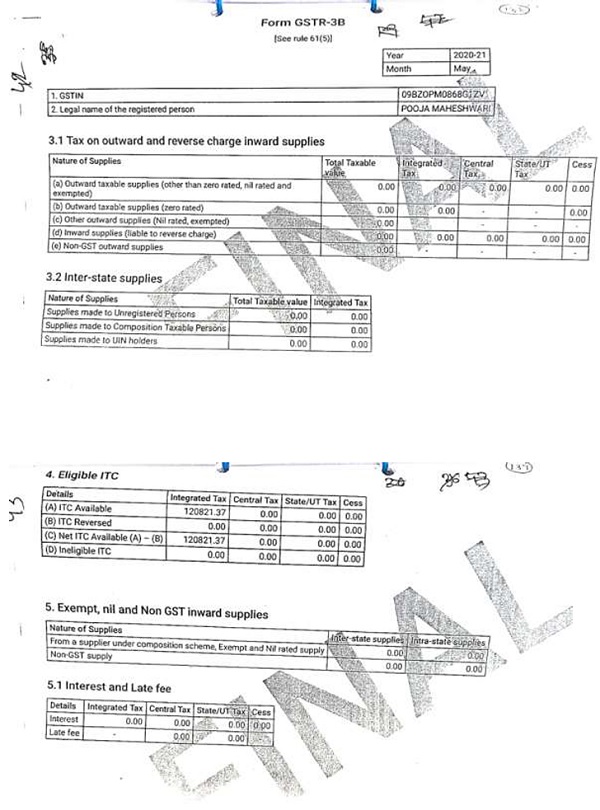

8. Further, the appellants have filed their GST Returns in Form GSTR-3B. For better appreciation of facts,the same are extracted herein below:

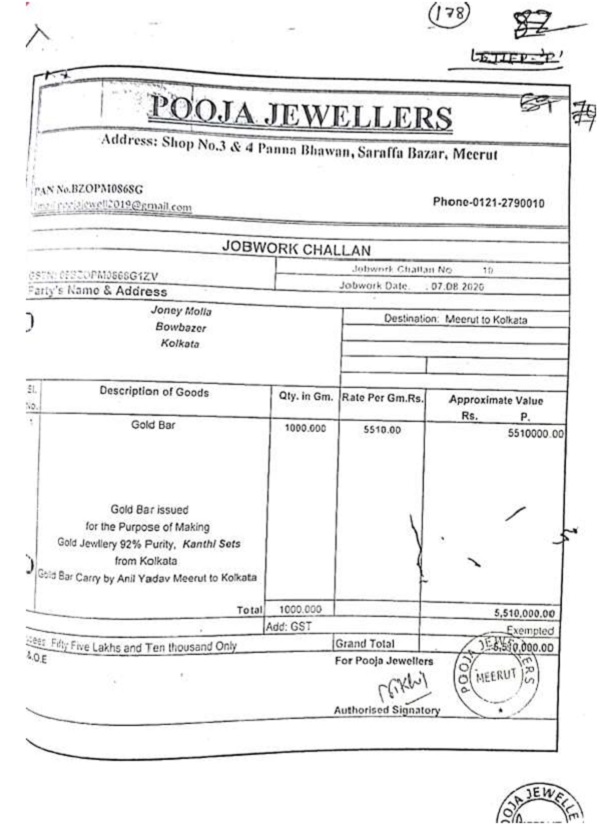

9. Further, we find that the Job work Challans were also produced during the course of adjudication. For better appreciation of facts, the same are extracted below :

–

–

10. As the gold in question is duty paid and GST Returns have been filed by the appellants and produced the purchase register thereof, which has been discarded by the adjudicating authority. In that circumstances, the evidences produced by the appellants are required to be considered by the adjudicating authority. The appellants have been able to discharge their onus under Section 123 of the Customs Act, 1962.

11. Moreover, we find that the gold in question is not having any foreign origin marking on the gold and it is the case of town seizure. Moreover, the purity of gold 99.6% and the documents for procuring the said gold have been produced by the appellants and the same has been brought on record.

12. In that circumstances, the gold in question is not liable for confiscation.

13. We further take note of the fact that on the production of the documents by the appellants for procuring the gold on payment of GST and the same has been recorded in the Books of Accounts. In that circumstances, it cannot be said that the gold in question is of foreign origin being smuggled one.

14. Therefore, the gold cannot be confiscated. Consequently, no penalties can be imposed on the appellant.

15. In view of this, we direct the authorities below to release of gold in question to the appellant as the appellants have discharged their onus under Section 123 of the Customs Act, 1962.

16. In the result, the impugned order is set aside and all the three appeals are allowed with consequential relief, if any.

(Pronounced in the open court on 18.06.2026)

Author Bio