The article argues that while Environmental (E) aspects of ESG have gained significant attention through climate disclosures and carbon-related reporting, the Social (S) and Governance (G) pillars remain equally important yet underemphasized. It highlights that the Social pillar focuses on fair treatment of workers, supply chain ethics, diversity, community impact, human rights, employee wellbeing, and consumer protection, supported in India by labour codes, CSR obligations under the Companies Act, and Business Responsibility and Sustainability Reporting (BRSR) requirements. The Governance pillar is presented as the mechanism that transforms ESG commitments into accountability through ethical leadership, board independence, transparency, whistleblower systems, audit oversight, and data governance, backed by SEBI regulations, the Companies Act, NFRA oversight, and the Digital Personal Data Protection Act. The article concludes that sustainable institutions require all three pillars—Environmental, Social, and Governance—to function together, as trustworthiness arises from being enlightened, empathetic, and ethical simultaneously.

E is Enlightened

What About S and G?

CMA Tarun Marimganti, B.Com, FCMA,DISSA

Fellow Member, ICMAI

| E

Enlightened The planet’s ledger is open. Science made the invisible visible. This pillar found its voice. |

S

Empathetic Behind every supply chain is a human being. Empathy is the discipline of accounting for people. |

G

Ethical Governance is one question: are we doing the right thing when nobody is watching? |

INTRODUCTION

Environmental disclosure has found its moment. Climate targets, carbon credits, TCFD-aligned reports — the E in ESG is scrutinised, scored, and increasingly regulated. But a framework built on three pillars cannot stand on one.

Social and Governance — the Empathetic and the Ethical — remain the underdiscussed half of every ESG report. This article argues that S and G are not supporting pillars. They are co-equal obligations — with their own measurement architecture, their own Indian regulatory backing, and their own capacity to create or destroy institutional value.

| S — Empathetic

Social capital is the most underpriced asset on any balance sheet. |

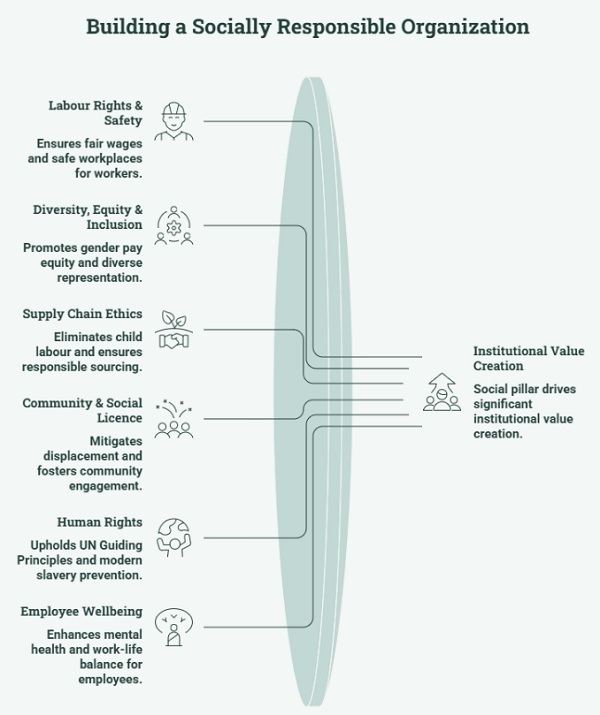

Every organisation operates through people — its workers, its suppliers, its communities. The Social pillar asks whether that relationship is fair, safe, and dignified. Not as a moral aspiration, but as a measurable, reportable, auditable obligation.

| Social failures are not slow-burning like climate risk. They are sudden — a labour strike, a supply chain scandal, a community displacement that revokes the social licence to operate. |

What S Actually Measures

| Theme | What It Covers |

| Labour Rights & Safety | Fair wages, safe workplaces, ILO Core Labour Standards, freedom of association. |

| Diversity, Equity & Inclusion | Gender pay equity, representation at all levels, anti-discrimination enforcement. |

| Supply Chain Ethics | Child labour elimination, forced labour audits, responsible sourcing (SA8000, OECD). |

| Community & Social Licence | Local employment, displacement mitigation, CSR effectiveness, consultation. |

| Human Rights | UN Guiding Principles; modern slavery; conflict-affected operations. |

| Employee Wellbeing | Mental health, healthcare access, ESOP, work-life balance. |

| Consumer Protection | Data privacy, product safety, responsible marketing, accessibility. |

Key Metrics

| Type | Metric |

| Quantitative | Lost Time Injury Frequency Rate (LTIFR) and fatality count |

| Quantitative | Gender ratio: Board, senior management, total workforce |

| Quantitative | Employee turnover rate and average training hours per year |

| Quantitative | % of supply chain audited for labour standards |

| Qualitative | Grievance mechanism: existence, confidentiality, resolution rate |

| Qualitative | CSR expenditure allocation and measurable community outcomes |

Indian Regulatory Backbone

INDIA | S FRAMEWORK

|

| G — Ethical

Governance is the enforcement mechanism for everything ESG promises. |

Governance is not procedure. It is the answer to one question asked quietly in every boardroom: are we doing the right thing when nobody is watching? Ethics is not a value statement on the wall. It is the structure of accountability that makes the question answerable.

| Every major corporate collapse — Satyam, IL&FS, Enron — was a Governance failure at its core. Without G, E and S are unenforceable promises. |

What G Actually Measures

| Theme | What It Covers |

| Board Composition & Independence | Director independence; diversity of expertise; separation of Chairman and CEO; succession planning. |

| Executive Remuneration Alignment | Pay-for-performance; CEO-to-median-worker ratio; ESG-linked KPIs; clawback provisions. |

| Anti-Corruption & Ethics | ABAC policies; code of conduct; ethics training coverage; violations history. |

| Financial Transparency | Auditor independence and rotation; audit committee effectiveness; RPT oversight. |

| Shareholder Rights | Voting structure; minority shareholder protection; takeover transparency. |

| Cybersecurity & Data | Cyber risk Board oversight; breach protocols; DPDP Act 2023 compliance. |

| ESG Oversight at Board Level | Dedicated ESG committee; ESG-linked executive incentives; assured integrated reporting. |

Key Metrics

| Type | Metric |

| Quantitative | % of independent directors on the Board |

| Quantitative | Women directors as % of total Board strength |

| Quantitative | CEO-to-median-employee pay ratio |

| Quantitative | Board meeting attendance rate (%) |

| Qualitative | Whistleblower mechanism: existence, confidentiality, resolution tracking |

| Qualitative | Related party transaction disclosure quality and Audit Committee oversight |

| Qualitative | Auditor independence: rotation schedule and non-audit fee ratio |

Indian Regulatory Backbone

INDIA | G FRAMEWORK

|

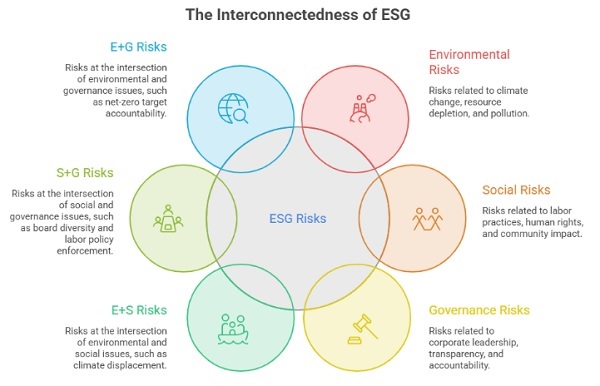

WHERE THE PILLARS MEET

The most consequential ESG risks live at the boundaries between pillars — not within any single one.

| E + S | Climate displacement falls hardest on vulnerable communities. Just Transition — moving to clean energy without destroying livelihoods — is where environmental responsibility and social equity become inseparable. |

–

| S + G | Board diversity is both a governance metric and a social equity one. Labour policy is set in boardrooms. Governance structures determine whether social commitments are enforced or ignored. |

–

| E + G | Net-zero targets without Board-level accountability and audited milestones are not commitments. They are greenwashing. G is what converts an E aspiration into an E obligation. |

CONCLUSION

CONCLUSION

E found its language because science made its consequences visible. S and G deserve the same clarity. The worker whose safety is ignored, the community whose water is diverted, the whistleblower whose complaint is buried — these are not soft issues. They are material risks with financial, legal, and reputational consequences.

| Enlightened without Empathetic is a company that saves the planet but exploits its people. Enlightened without Ethical is a company that announces targets it has no intention of meeting. |

–

| The Definitive Test

E — Enlightened: Are you honest about your impact on the planet? S — Empathetic: Are you fair to the people your organisation touches? G — Ethical: Are your structures accountable when nobody is watching? If the answer to all three is yes — you are not just ESG-compliant. You are trustworthy. |

******

About the Author: CMA Tarun Marimganti is a Fellow Member of the Institute of Cost Accountants of India (FCMA), practising as a Cost Accountant at Tarun Marimganti & Associates, Hyderabad.

Disclaimer: The views expressed in this article are the personal views of the author and are intended solely for informational and academic purposes. This article does not constitute professional advice, legal opinion, or a substitute for specific consultation. Readers are advised to evaluate the facts of their particular case independently and seek appropriate professional advice before acting on the basis of this article. The author and the firm shall not be responsible for any loss or consequences arising from reliance on the contents of this article.