Presently AS 4 deals only with Events occurring after the Balance Sheet date. Even though the Standard’s name starts with contingencies, all the paragraphs related to ‘contingencies’ have been withdrawn by The Institute of Chartered Accountants of India. From 1-4-2004, contingencies are dealt by AS-29 – “Provisions, Contingent Liabilities and Contingent Assets”. Before we start the main discussion, you need to understand the sequence of approval of financial statements in case of companies.

Financial Year is the period for which accounting records are prepared, summarized and analyzed. On the end of financial year Final Accounts are prepared to know the outcome of financial activity during the accounting year management has the primary responsibility to prepare final accounts. After preparation of final accounts audit is done to establish true and fair view of the financial statements. Audited financial statements are then accepted by the Board of directors/partners in their meetings.

Period from end of the financial year to the date of meeting of Board of directors is called period after balance sheet date.

Substantive Rule 1 : Preparation and presentation of financial statements is the responsibility of the management of the entity. Financial statements are approved by the Board of Directors in case of a company; in case of partnership firm, managing partners approve the financial statements, etc.

What is Approval of Financial Statement: Approval of Financial Statements means that, the books of account of the financial year are closed. Subsequent to approval of financial statements, that income or expenditure should be recorded in next year as a prior period item.

(Prior Period items are part of AS 5)

Example 1 A factory is painted in March 2023, and the painter submitted the bill in April 2023. The accountant of the company did not make a provision for the expense as on 31-3-2024.

FY 2022-23 financials are approved on 30-9-2023.

a) Can the accountant record the JE for the painting expenses in FY 2015-16 OR should he record in 2016-17? And (b) If the bill is received after 30-09-2016 what would be the treatment?

Solution:

(a) The expense is incurred during FY 2022-23 and it should be recognised as an expense in the same year. Information of the expense is received before the date of approval of financial statements; hence the entity should recognise the transaction as on the balance sheet date i.e. in FY 2022-23.

(b) If the bill is received after 30th Sep., 2016, it should be recognised as a prior period expense in FY 2023-24 as per AS 5. Refer AS 5 – Prior period expense for further information.

2. Definitions from the Accounting Standard :

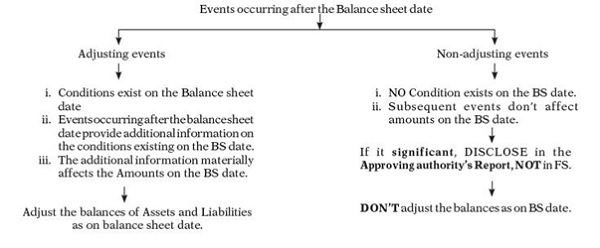

Events occurring after the balance sheet date: These are significant events, which occur between the balance sheet date and financial statements approval date. These significant events can be favourable or unfavourable to the entity.

What Significant events Means – Material events, which can influence the economic decisions of the users of financial statements.

The whole discussion in this standard is whether the events occurring after the balance sheet date should be recorded as on balance sheet date OR in the next financial year.

Events occurring after the balance sheet date are classified into two i.e. adjusting events and non-adjusting events; let us understand this concept from the below picture:

The primary objective of the standard is to ensure the completeness, that all the transactions and related information should be updated in financial statements.

Example 2: While preparing the financial statements for the year ended 31-3-2024, P Ltd. made a provision for doubtful debts @ 5% on accounts receivables balance. In Feb., 2024, a debtor for ` 2 lakh had suffered heavy loss due to an earthquake. The loss of debtor was not covered by any insurance policy. In April, 2024, the same debtor became insolvent. Financial statements are approved on 30-9-2024. Discuss the accounting treatment as per AS 4 in the financial statements ended 31st March, 2018.

Solution: On 31st March, 2024, the financial position of the debtor was not good and such condition existed on the balance sheet date. The entity may or may not be sure of the position on the balance sheet date. The subsequent event of insolvency is confirming the financial position of the debtor. So it is an adjusting event and it requires an adjustment to accounts receivable balance by way of making provision for doubtful debts for the entire amount.

5% provision may be as per the accounting policy of the company and the above provision should be made in addition to the existing provision.

Example 3 : Continuing with the above question – The accounts receivable balance is 2 lakh as on 31-3-2024. But earthquake took place in April 2024 and the debtor became insolvent in May 2024. Discuss the accounting treatment as per AS 4.

Solution: The debtor’s financial position was good as on 31-3-2024 and the subsequent conditions are entirely different from the balance sheet date condition i.e. no condition exists. Hence it is a NON-adjusting event and it doesn’t require any adjustment to assets as on 31-3-2024. P Ltd. should provide for doubtful debts during the next FY i.e. 2024-25. Board of Directors can disclose the same in their report, if it is material to X Ltd.

Example 4: Continuing with the above question – There was no balance of accounts receivable as on 31-3-2024 and P Ltd. sold goods in April 2024 and earthquake took place in May 2024 and the debtor became insolvent in July 2024. Discuss the accounting treatment as per AS 4.

Solution: It is a non-adjusting event and doesn’t require any adjustment to assets as on 31-3-2018.

P Ltd. should provide for doubtful debts during the next FY i.e. 2024-25. Board of Directors can disclose the same in their report, if it is material to P Ltd

Example 5: A company has filed a legal suit against the debtor from whom 15 lakh is recoverable as on 31.3.2025. The chances of recovery by way of legal suit are not good as per legal opinion given by the counsel in April, 2025. Can the company provide for full amount of 15 lakhs as provision for doubtful debts? Discuss.

Solution: As per AS 4, assets and liabilities should be adjusted for events occurring after the balance sheet date that provide additional evidence to assist the estimation of amounts relating to conditions existing at the balance sheet date.

In the given case, subsequent information is giving more clarity that the balance as on the balance sheet date is not recoverable hence it is appropriate to make a provision for doubtful debts. Therefore, provision for doubtful debts should be made for the year ended on 31st March, 2025.

Example 6. P Ltd. invested 100 lakh in Q Ltd. in April 2025 but the negotiations had started in Jan. 2025. As per AS 4 – In which financial year X Ltd. should account for the investment?

Solution: Negotiations don’t amount to conditions. As there are no conditions existing on the balance sheet date, it is a non-adjusting event and doesn’t require any adjustment to assets as on31-3- 2025 i.e. it should record the investments only in 2025-26.

Investment planning of 100 lakh in April, 2025 in the acquisition of another company should be disclosed in the Director’s Report to enable users of financial statements to make proper evaluations and decision.

Example 7: P Ltd. purchased a building for 50 lakh in Jan. 2025, and the agreement to purchase was concluded in Jan. 2025. P Ltd’s financial year ends on 31st March. In the month of April 2025, the same building is registered in the name of P Ltd. In which financial year P Ltd. should account for the building?

Solution: Looking at the substance of the transaction, the agreement was concluded in Jan. 2025 and registration is required for security purpose. The subsequent registration is confirming the agreement. So the building should be recorded in 2024-25 only.

Example 8: X Ltd. Holds current investments as on 31-3-2025. Cost of investments is 50 lakh and fair market value is 55 lakh (on 31-3-2025) and the company measured it at 50 lakh as per AS 13 (i.e. Cost or FMV whichever is less). Financial statements are approved by BODs on 30-09-2025. Due to subsequent market conditions the value of investments fell down to 40 lakh. Whether X Ltd. needs to value the investments at 50 lakh or 40 lakh on 31-3-2025? Discuss.

Solution: Market conditions on 31st March are different from 30th Sep. market conditions. The value of investments as on 30th Sep. does NOT affect the conditions on 31st March. Hence it is a non-adjusting event and there is no need to adjust the balance on 31-3-2018 and the value of investments will continue at `50 lakh

If the approving authority wants to disclose non-adjusting events in their report, they should disclose the following information: a.Nature of the events; b.Estimation of the financial effect; and c. If it is not possible to estimate, disclose the fact that such estimation cannot be made.

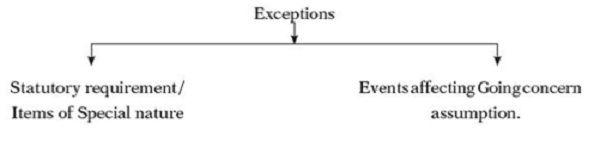

Exceptions to the general rule:

Even though it is a non-adjusting event it should be adjusted as on balance sheet date. There are two exceptions to the rule of adjusting events:

1.If it is a legal requirement OR it is of special nature;

2. If events occurring after the balance sheet date affects the Going Concern Assumption of the entity.

Example 9: On 31-08-2024, the Board of Directors of P Ltd. proposed dividend of 8% for FY 2023-24. Financials of 2023-24 are approved by BoD on 30-09-2024. Discuss the accounting treatment of the proposed dividend as per AS 4.

Solution: Proposed dividend is an event occurring after the balance sheet date. The company DOESN’T have any liability to pay dividend on balance sheet date. The reason being dividend will be a liability to the company only when it is approved by the members of company in the General Meeting. As there are NO conditions existing as on 31-3-2024, the subsequent proposal for dividend is a NON-adjusting event, as per the Schedule III proposed dividend information should be disclosed in the notes on accounts separately

Example 10: After the closure of financial year i.e. 31-3-2025, there was a severe earthquake. The company lost its building and major plant and the extent of loss is beyond repair. The company doesn’t have adequate funds to replace the same. Discuss your views based on AS 4.

Solution: The subsequent event of earthquake occurred after the balance sheet and no condition exists on balance sheet date. It is a non-adjusting event. Even though the above event occurred after the BS date, the event materially affects the solvency of the company and it indicates clearly that the company is not a going concern. Even though it is not an adjusting event, as per AS 4 – Company has to prepare the financial statements on 31-3-2025 on NRV basis (liquidation basis) and any gain or loss should be transferred to P&L.

Example 11: P Ltd. financial statements of 2023-24 are approved by the BoD on 30-09-2024 & financial statements are adopted by the AGM on 15-10-2024. On 30-11-2024, the company identified an expenditure (omission of expense) which is relating to 2023-24. How to deal with the expenditure? Discuss.

Solution: Once the financial statements are approved by the BoD and adopted by the AGM, the expenditure of 2024-25 will be recognised in the P&L of 2024-25 as a prior period expense (omission of expense) as per AS 5. Refer AS 5 for detailed discussion

Some More problems related with event after balance sheet date:

Problem. 1 A company deals in Petroleum products. The sale price of petroleum is fixed by the Government. After the balance sheet date, but before the finalization of the company’s accounts, the Government unexpectedly increased the price retrospectively. Can the company account for additional revenue at the close of the year?

Solution: As per AS-4, the unexpected increase in the sale price of petrol by the Government after the balance sheet date cannot be regarded as an adjusting event as it doesn’t represent a condition existing as on the balance sheet date. Hence revenue (due to increase in sales price) should be recognized only in the subsequent year with proper disclosure.

Problem No. 2 A Company follows April-March as its financial year. The company recognizes cheques dated 31st March or before, received after the balance sheet date but before approval of FS by debiting cheques in hand a/c & crediting Debtors a/c. The cheques in hand are shown in the balance sheet as an item of Cash & Cash equivalents. All cheques in hand are presented to bank in the month of April & are also realized in the same month in normal courses after deposit in the Bank. What treatment is correct as per AS-4?

Solution: Even if the cheques bear the date 31st March or before, the cheques received after 31st March do not represent any condition existing as on 31st March. It means, it is not an asset under the control of the entity as on the balance sheet date. Hence, there is no situation/condition exist as on 31st March. Considering this, collection of cheques after the balance sheet date is NOT an adjusting event. So recognising these as cheques in hand is not consistent with AS-4. Moreover, the collection of cheques after the balance sheet date does not represent any material change or commitments affecting the financial position of the enterprise and therefore no disclosure in the Director’s Report are necessary.

Problem No. 3 Company entered into a construction contract to lay a pipeline before 31-3-2024. Financial statements for that year were finalized on 15-5-2024. While doing grounding work it met a rocky substance for which it had to incur an additional `50 crore on 16-5-2024. Should company make provision? If yes, in which year should it be making 2023-24 or 2024-25?

Ans: The Company’s financial statements were finalized on 15-5-2024. But it discovered that it has to expend an additional 50 crore only on 16-5-2024, therefore it does not amount to an event occurring after the balance sheet date.

The company has to make a provision in the financial year 2018-19 i.e. in the next financial year.

Problem No. 4 P Limited Company closed its accounting year on 30.6.2024and the accounts for that period were considered and approved by the board of directors on 20th August, 2024. The company was engaged in laying pipe line for an oil company deep beneath the earth. While doing the boring work on 1.9.2024 it had met a rocky surface for which it was estimated that there would be an extra cost to the tune of ` 80 lakhs. You are required to state with reasons, how the event would be dealt with in the financial statements for the year ended 30.6.2024.

Ans: In this case the incidence, which was expected to push up cost, became evident after the date of approval of the accounts. So, it is not an ‘event occurring after the balance sheet date’. However, this may be mentioned in the Report of Approving Authority i.e. Board of Director’s report.