Implications of the J&K High Court Judgment on Value Addition Criteria for Refund Computation under the GST Budgetary Support Scheme (BSS)

J&K High Court held GST Budgetary Support refunds be based on fixed value addition rates under Notification 01/2010-CE, not actual higher rates.

The recent judgment by the Honourable Jammu & Kashmir High Court on the application of value addition principles for refund calculations under the GST Budgetary Support Scheme (BSS) has generated considerable attention within the industry and tax administration. This ruling addresses the critical issue of whether refunds should be computed based on a manufacturer’s actual value addition or limited to standardized value addition rates prescribed in the erstwhile Notification No. 01/2010-C.E. The Court’s interpretation carries significant ramifications, raising complex questions about compliance, refund eligibility, and procedural safeguards under the scheme. This discussion explores the practical and legal challenges posed by the judgment, as well as its broader implications for stakeholders involved in claiming budgetary support under the GST framework

Before delving into the subject matter, we will discuss a brief overview of the provisions of the Budgetary Support Scheme under GST.

The budgetary support (BSS) under GST refers to a scheme provided by the Government of India to support eligible industrial units located in certain special category states like Jammu & Kashmir, Uttarakhand, Himachal Pradesh, and the Northeastern States including Sikkim.

The GST Council, in its meeting on 30.09.2016, noted that existing indirect tax exemptions under Central or State incentive schemes would not continue under GST, requiring units to pay GST. However, it allowed Central and State Governments to provide budgetary support. Consequently, the Central Government decided to offer partial reimbursement of GST paid by eligible units, limited to its share of CGST and/or IGST after devolution to States, to alleviate hardships from the withdrawal of prior exemptions.

The notification dated 5th October 2017 (‘BSS Notification’) by the Ministry of Commerce & Industry, Department of Industrial Policy & Promotion, introduces the Scheme of Budgetary Support under GST Regime for eligible manufacturing units located in Jammu & Kashmir, Uttarakhand, Himachal Pradesh, and North Eastern States including Sikkim.

Key points:

- The scheme replaces earlier excise duty exemption/refund benefits that ceased from 1st July 2017 due to GST implementation.

- It targets units that were previously eligible under specific Central Excise exemption notifications but now must pay GST.

- Budgetary support is offered as a partial reimbursement of GST paid (specifically 58% of Central tax and 29% of Integrated tax paid after utilizing input tax credits), limited to the Central Government’s share post-devolution to States.

- The scheme applies from 1st July 2017 and continues for the residual period of the original eligibility (up to 10 years from commencement of production), valid till 30th June 2027.

- Eligible goods, units, and input criteria are clearly defined, with measures to prevent misuse, including inspections and audits.

- Claims for reimbursement are to be filed quarterly, with disbursements from the budgetary allocation of DIPP.

- Recovery mechanisms and penalties apply for fraudulent claims or non-compliance.

- The scheme is a goodwill measure with no direct relation to erstwhile excise schemes but supports units through the GST transitional period.

Overall, the scheme facilitates continued industrial promotion in these special category states by mitigating the impact of GST on units losing earlier excise exemptions.

Upliftment of economically & geographically disadvantaged regions

- The scheme aims to make these units competitive and promote industrial growth in economically disadvantaged regions by compensating them for the tax liabilities under GST that replaced earlier exemptions.

- It is estimated that total number of 4284 eligible units located in the State(s) of Jammu & Kashmir, Uttarakhand, Himachal Pradesh and North Eastern States including Sikkim will benefit from the above scheme.

- The total budgetary support approved by the government for this scheme was around Rs. 27,413 crore for the period from July 1, 2017, to March 31, 2027.

Determination of the amount of budgetary support

To avail the benefit of this scheme, eligible units must first utilize the input tax credit of Central and Integrated taxes, paying any remaining liability in cash. If this condition is not met, the sanctioning officer will reduce the budgetary support by the amount of unused input tax credit. The 58% reimbursement rate is based on the current 42% tax devolution to States as recommended by the 14th Finance Commission.

The amount of GST budgetary support for beneficiaries (eligible industrial units) is calculated as the sum total of:

- 58% of the Central Goods and Services Tax (CGST) paid in cash, which is the amount debited from the cash ledger account maintained by the unit under CGST Act, after utilizing the input tax credit (ITC) of CGST and Integrated GST (IGST).

- 29% of the Integrated Goods and Services Tax (IGST) paid in cash, paid through debit in the cash ledger account maintained under the IGST Act, after utilizing input tax credits of CGST and IGST.

If inputs are procured from a registered person operating under the Composition Scheme, the amount of budgetary support is reduced proportionately by the percentage value of such inputs out of the total inputs procured.

Formulaically, it can be described as:

- Budgetary support = (58% of CGST paid in cash after ITC utilization) + (29% of IGST paid in cash after ITC utilization) – proportionate reduction for inputs from Composition scheme suppliers.

The payment of these taxes must be made in cash after fully utilizing the available input tax credit to be eligible for the support. The eligible unit must apply for the support quarterly, and the claim undergoes inspection and sanction by the authorities before disbursal.

This scheme compensates for the central tax cash component paid by units in specified special category states to continue their incentive support under GST.

In summary, the budgetary support under GST is a grant-like refund mechanism to continue incentivizing industrial units in special category states that lost excise duty exemptions due to GST implementation, allowing them to claim partial refund on the central tax components they pay in cash under GST.

The CGST/IGST to be taken into above account should be paid on value addition

Verification of Value addition under Budgetary support

Value addition under the Budgetary Support Scheme (BSS) refers to the increase in value of goods as a result of the manufacturing process carried out by an eligible unit. It is a key factor in determining the admissible budgetary support amount.

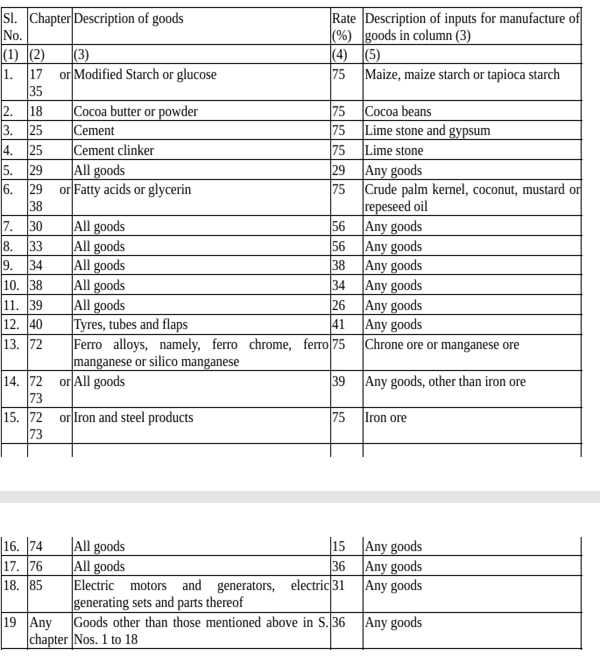

Specifically, para 5.8 of the BSS notification dated 5th October 2017 defines value addition as any change in the physical object that transforms it into a new or different article or alters its chemical composition or structure. The scheme includes a table prescribing standard rates of value addition for different categories of specified goods.

Explanation: For calculation of the value addition the procedure specified in notification no 01/2010-CE dated 06.02.2010 of the Department of Revenue as amended from time to time shall apply mutatis-mutandis.

The calculation method and standards for value addition draw on the procedure specified in an earlier notification (No. 01/2010-CE dated 06.02.2010), which was used for excise duty exemptions before GST will apply.

In the erstwhile 01/2010 notification, the option was available for eligible manufacturers to apply for fixation of special rates if actual value addition is greater than prescribed rates

If Actual value addition is greater than prescribed rate- No option for ‘special rates’

The amount of budgetary support is linked to the tax paid on this value addition. Para 5.8 of the BSS notification provides that if the actual GST paid on the value addition exceeds the GST amount calculated based on the standard value addition rates in the table, the claim undergoes verification.

The same was also referred in Para 9 of department Circular No.1060/9/2017 CX dated 27.11.2017 which clarifies that the eligible unit shall also indicate the value addition achieved by it in respect of each category of specified goods and where the value addition is higher than the limit provided in the table under the said para, the sanction of the claim shall be after verification of the value addition

It is also pertinent to note that Para 5.3 of BSS Notification states that the limitations, conditions, and prohibitions in the Department of Revenue’s notifications existing before 01.07.2017 shall continue to apply under this scheme. However, provisions for determining special rates under those exemption notifications shall not apply to the eligible manufacturers Therefore, no option was available for eligible manufacturers to apply for fixation of special rates for calculation of budgetary support amount.

J&K Cement Corporation vs. Union of India (2025) 174 taxmann.com 228 (Jammu & Kashmir and Ladakh)

The judgment by the Honourable Jammu & Kashmir High Court concerning the value addition used for calculating refunds under the GST Budgetary Support Scheme (BSS) has unleashed a complex set of challenges, giving rise to substantial interpretational and practical issues.

The Court held that budgetary support must be restricted to the value addition rates prescribed under the erstwhile Notification No. 01/2010-C.E. dated 06.02.2010, which fixed predetermined value addition percentages for various goods. This ruling means that refunds cannot be granted based on a manufacturer’s actual or claimed value addition if it exceeds those specified rates. Instead, the refund calculation under the BSS is capped at these official prescribed rates, effectively disregarding any actual higher value addition.

This interpretation excludes the provision for fixation of a ‘special rate’ for actual higher value addition that existed under the previous Central Excise regime but was explicitly removed from the BSS terms. The Court’s decision thus enforces strict adherence to the historical value addition rates, limiting refunds to those levels.

However, the scheme itself contains provisions (notably Para 5.8 of the BSS) which contemplate verification processes when actual GST paid on value addition exceeds the prescribed rates, potentially allowing some refund claims beyond the fixed table rates after due verification. This aspect, including Circular No. 1060/9/2017-CX (dated 27 November 2017), which requires refund sanction after verification in case of higher value addition, was not factored into the Court’s ruling. This omission raises concerns regarding the scope for legitimate claims above the fixed rates once verified by authorities.

The ruling, therefore, creates uncertainty and the potential for extensive litigation concerning which value addition should be considered—fixed prescribed rates or actual manufacturer-specific rates. It threatens to limit budgetary support strictly to the conservative predetermined benchmarks, undermining claims based on actual operational efficiencies or higher value addition.

Furthermore, since the BSS lacks limitation periods for recovery actions on refunds granted beyond prescribed rates, units sanctioned refunds based on actual value addition may face retrospective recovery demands with significant financial implications.

In professional terms, this judgment signals a stringent, scheme-compliant approach mandating that budgetary support refunds be calculated only on officially notified value addition rates, rejecting reliance on actual manufacturer-specific value addition unless subjected to and cleared by verification. The decision has far-reaching impacts on the administration and claim practices under the BSS, potentially increasing compliance risks and protracted disputes, calling for urgent clarifications to balance industrial promotion objectives with strict regulatory adherence.

This judicial interpretation underscores the critical need for clarity in policy execution to avoid undermining ease of doing business and to prevent inadvertent conflict between statutory provisions, verification mechanisms, and judicial rulings in the GST refund domain.

****

( the views expressed in this article are strictly personal and author of this article can be reached at [email protected])