Case Law Details

Kanta Devi Jalan Vs DCIT (ITAT Delhi)

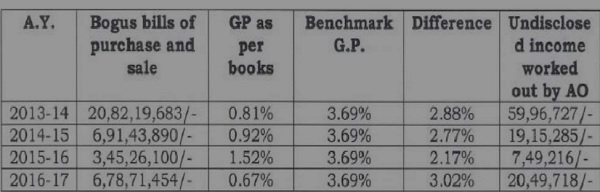

Summary: The Income Tax Appellate Tribunal (ITAT), Delhi, partly allowed the assessee’s appeals for Assessment Years 2013-14 to 2016-17 concerning additions made on alleged bogus purchase and sale transactions. The Assessing Officer had treated transactions with certain alleged dummy concerns as accommodation entries, rejected the books of account under Section 145(3), and estimated additional gross profit (GP) at 2.88% by adopting the highest GP rate of AY 2019-20. The Tribunal observed that the assessee’s sales had been accepted, transactions were routed through banking channels, and the assessee had furnished VAT registration documents and bank account details establishing the identity and creditworthiness of the parties. At the same time, the Tribunal held that the assessee was still required to establish the genuineness of the purchases and the source of funds. Finding the AO’s adoption of the AY 2019-20 GP rate excessive and unrelated to the relevant years, the ITAT restricted the addition to 1% GP, clarifying that the relief should not be treated as a precedent.

Core Issue. The principal issue before the Tribunal was whether the entire addition made on account of alleged bogus purchases could be sustained where the sales declared by the assessee had been accepted, the purchases were supported by banking transactions, VAT registration documents and bank account details of the suppliers, but the assessee could not fully establish the genuineness of the purchases. The Tribunal also considered the reasonableness of adopting the gross profit rate of AY 2019-20 for estimating income pertaining to AYs 2013-14 to 2016-17.

Facts. The assessee, engaged in the business of trading in food grains and pulses, was subjected to search proceedings under section 153A. During assessment, the Assessing Officer relied upon information received from the Investigation Wing that certain suppliers were accommodation entry providers controlled by an alleged entry operator. Holding that purchases from such parties were unverifiable, the Assessing Officer rejected the books under section 145(3). Since the corresponding sales were accepted, the Assessing Officer estimated the profit element embedded in the alleged bogus purchases by adopting the highest gross profit rate of 3.69% declared by the assessee in AY 2019-20 and made additions for AYs 2013-14 to 2016-17. The CIT(A) affirmed the additions.

Findings of the ITAT. The Tribunal observed that the assessee was engaged in a trading business and that the Revenue had accepted the sales declared by the assessee. It held that such sales could not have been effected without corresponding purchases. The Tribunal further noticed that the transactions had been carried out through banking channels and that the assessee had furnished VAT registration particulars and bank account details of the suppliers, thereby establishing their identity to a considerable extent. It also observed that the Assessing Officer had not brought any material on record to establish that the documentary evidence produced by the assessee was false or fabricated.

However, the Tribunal held that proving the genuineness of purchases also required the assessee to satisfactorily explain the source and genuineness of the payments made for such purchases. The primary burden to establish the allowability of expenditure continued to rest upon the assessee and that burden had not been completely discharged. Accordingly, the Tribunal held that some estimation of profit was justified instead of deleting the addition in its entirety.

While considering the quantum of estimation, the Tribunal found that the Assessing Officer had wrongly adopted the gross profit rate of AY 2019-20, which reflected a substantially different business model and product mix from the years under appeal. The Tribunal observed that the assessee’s declared gross profit during AYs 2013-14 to 2016-17 ranged only between 0.67% and 1.52%. In these circumstances, adoption of the enhanced gross profit rate of 3.69% was held to be arbitrary and excessive.

Balancing the facts of the case, the Tribunal restricted the addition by estimating the profit element at 1% of the impugned purchases, holding that such estimation was fair, reasonable and broadly in line with the assessee’s historical margins. The Tribunal, however, clarified that the direction was rendered on the peculiar facts of the case and should not be treated as a precedent for other cases.

Accordingly, the additions for AYs 2013-14 to 2016-17 were restricted to 1% of the disputed transactions and all the appeals were partly allowed.

Cases Relied Upon. The Tribunal considered the principles laid down by the Supreme Court in CIT v. Odeon Builders Pvt. Ltd., Andaman Timber Industries v. CCE, and the decision of the Allahabad Bench of the Tribunal in Jai Bajrang Gur Bhandar v. ITO.

Ratio Decidendi. Where sales are accepted and corresponding purchases are supported by banking channels and contemporaneous commercial documents, the entire purchases cannot ordinarily be disallowed merely because the suppliers are alleged accommodation entry providers. Nevertheless, the burden of establishing the genuineness of the expenditure continues to rest upon the assessee. In such circumstances, only the profit element embedded in the disputed purchases can be brought to tax, and the estimation must be based upon the assessee’s own historical gross profit and surrounding facts rather than an unrelated year’s higher margin.

FULL TEXT OF THE ORDER OF ITAT DELHI

1. The assessee has filed appeals against the order of the Learned Commissioner of Income-tax (Appeals)-30, Delhi [“Ld. CIT(A)”, for short] dated 24.01.2023 for the Assessment Years 2013-14 to 2016-17.

2. Since the issues are common and the appeals are connected, hence the same are heard together and being disposed off by this common order. We take up the assessee’s appeal being ITA No.807/Del/2023 for AY 2013-14 as lead case to adjudicate the issues under consideration raising following concise grounds of appeal :-

“1. That the grounds raised in the Appeal before CIT-(A) was not disposed by passing speaking order.

2. That the comment/remand report not taken from Revenue in view of the grounds raised in Appeal before CIT-A.

3. That Panchnama is invalid, bad in law, void, without jurisdiction, barred by limitation, and was not produced for signatures of Assessee by the Authorized officer.

4. Annexure J, Annexure-S and Annexure-O not provided to assessee at the time of search & seizure.

5. That Assessing officer fails to bring on record that the Search party can consider any person (even he holds no authorization in writing from assessee) as authorized representative of assessee.

6. The Panchnama is not correct as authorized officer is having the warrant of authorization dated 01.11.201 and search was conducted on 01.11.2018.

7. The Panchnama is not correct as authorized officer stated in the Panchnama that search party reach for search at 3.54 A.M and Search started at 3.55 A.M.

8. That Assessing officer fails to bring on record, under what circumstances search party leaked the information to Mr. Mukesh to arrived at the search place in late night i.e.at 3.54 A.M. on 01.11.2018.

9. That Assessing officer fails to bring on record, under what circumstances search party search the locker before sun arises.

10. That assessee has prove the identity and creditworthiness of parties from whom purchase and sale made by assessee.

11. That assessee has prove the identity and creditworthiness of parties from whom purchase and sale made by assessee by submitting the Bank Account details.

12. That Assessing officer fails to bring on record that VAT registration granted by concerned VAT Department in violation of VAT Act and rules and procedures prescribed by State Govt.

13. That Assessing officer fails to bring on record that bank accounts of parties to whom assessee deals were opened by the Banks in violation of RBI Guidelines.

14. That Assessing officer fails to bring on record, that the documents filed by assesses to establish the genuineness of the purchases were bogus false.

15. That the assesses filed documents to establish the genuineness of the purchases.

16. That Assessing Officer fails to bring on record any material evidence to show that the purchases/sales were bogus.

17. That without affording the assessee any opportunity to cross examine those witnesses.

18. That the AO failed to cause any enquiry to be made to establish his suspicions that the said purchases/sales are bogus,

19. That the AO failed to bring on record that the assessee booked bogus sale/purchase and money is received back by assessee in cash from these parties.

20. That the A.O. has taken the net profit ratio of AY 2019-20 for making the addition pertaining to income of AY 2013-14 to AY 2016-17 which have no relation /linkage with the transaction made in the 2019-2020.

21. In view of non compliance of instructions issued by CBDT by the Ld. A.O. while passing the said order. Hence the order passed by the learned A.O. is bad, both in the eye of law and on the facts.

22. The assessment order is illegal, void, and arbitrary, without jurisdiction, barred by limitation, bad-in -law. Hence the assessment order is arbitrary, wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.”

3. Brief facts of the case are, the original return under section 139 of the Income-tax Act, 1961 (for short ‘the Act’) was not filed by assessee for the year under consideration. Thereafter, search u/s 132 of Act was conducted on 31.10.2018 to 17.12.2018 at the business premises of M/s Faqir Chand Lockers and Vaults Private Limited. During the course of search, it was found that there were 300 lockers in the name of different persons mostly belonging to nearby business entities. Among these lockers, one locker No. 183 was allotted in the name of Shri Ved Prakash Agarwal (assessee herein), accordingly a search warrant was issued in the name of the assessee on the premise Locker No 183 at M/s Faqir Chand lockers and Vaults Private Limited 6704A, Khari Baoli, Chandni Chowk, Delhi, in the name of Shri Vikash Jalan and the same was executed on 01.11.2018. Assessment jurisdiction over the assessee was transferred by the Pr. Commissioner of Income Tax. Delhi-15, New Delhi vide order u/s 127 of Income Tax Act, 1961.

4. A notice u/s 153A of the Act was issued on 28.09.2020 requiring the assesses to furnish the return of income for the year under consideration being one of the six assessment years preceding the assessment year in which search was conducted within 15 days of service of the said notice. In response to the notice, assessee e-filed return on 28.12.2020 declaring income of Rs.3,42,430/-. Notices u/s 143(2) and 142(1) along with a questionnaire were issued and served on the assessee. In response, the assessee filed his submissions which were examined and placed on record.

5. The Assessing Officer observed that as per the information received, asearch operation was conducted by the Investigation Wing at the business premises of Sh. Hitesh Jain, prop. M/s Mittersain Rajesh Kumar, Kamal on 23.05.2017. During the search proceedings, some incriminating documents like loose papers, blank signed cheque books, laptop data were seized from the premises of Hitesh Jain. During the course of search operation, he admitted that he was involved in providing accommodation entries through the various dummy / paper concerns by issuing bogus bills in lieu of certain commission and no actual sale / purchase had been taken place. AO observed that assessee has received accommodation entries from the dummy/paper concern which are detailed at page 2 of the assessment order as under :-

| Sr. No. | Name of Dummy / paper concerns of Hitesh Jain | Amount credited in the bank account of dummy concerns by the assessee during the F.Y. 2012-13 |

Amount debited by the bank account of dummy concerns by the assessee during the F.Y. 2012-13 |

| 1 | M/s. Gagan Enterprises | Rs.2,68,18,435/- | Rs.8,00,000/- |

| 2 | M/s. Raghuveer Singh Davinder Kumar | Rs.7,87,15,170/- | Rs.5,00,000/- |

| 3 | M/s. Gurudev Trading Company | Rs.4,41,63,372/- | Rs.6,20,000/- |

| 4 | M/s. Aggarwal Trading Co. | Rs.1,40,29,193/- | |

| 5 | Shree Shiva Agro Traders | Rs.4,06,93,513/- |

6. After examining the information received, AO issued notice u/s 133(6) dated 13.03.2020 to the assessee directing to file the ITR, Balance Sheet, P&L A/c and Ledger accounts of above dummy concerns. In compliance to the notice, assesses did not submit any reply. Subsequently, notices u/s 153A of the Act were issued to the assessee on 28.09.2020 and prior to issuance of notice u/s 153A, proceedings u/s 148 of the Act were initiated and notice u/s 148 of the Act could not be issued due to unprecedented situation i.e. lockdown in the country caused by COVID-19 pandemic.

7. Further vide letter dated 24.06.2021, ld. AR of the assessee submitted that consequent to the death of Shri Ved Prakash Aggarwal (the assessee), his wife Mrs. Kama Devi Jalan is the legal heir of the deceased and the new proprietor of M/s Om Bhandar.

8. During the course of assessment proceedings, AO observed that the assessee had made payments to certain parties towards purchase of goods and received amounts from parties on account of sale of goods. These parties were apparently dummy parties controlled by one Shri Hitesh. Jain, an admitted entry operator. Since the assessee had booked bogus purchases, vide notice dated 06-04-2021 issued u/s 142(1), the issue was confronted to the assessee. In response to the above, the assessee submitted his reply vide his submission dated 28.06.021 which is recorded by the AO in the assessment order. However, the above submissions of the assessee were considered by the AO and found not tenable.

9. Further AO observed that the assessee was not able to justify that the assessee has transacted with the bogus parties controlled by the abovesaid entry operator. The mere fact that payments have been made through account payee cheque cannot, in any way, paint a bogus transaction with colours of genuineness. AO relying on the decisions of Hon’ble courts observed that mere payment by account payee cheque cannot establish that the transaction was genuine.

10. Further AO observed that the assessee has not made purchases from the above-bogus parties. However, at the same time, since the goods claimed to have been purchased from these bogus parties have been sold, it is clear that the assessee has purchased goods from some other party whose details are not on record. AO further observed that it appears that assessee had made purchases from grey market.

11. He observed that to the extent of purchases made by the assessee from the bogus parties and the corresponding sales made out of such purchases, the books of accounts of the assessee are not clear and do not give true and correct picture of the accounts of the assessee. Accordingly, he further observed it is not possible for him to rely upon the sanctity of such books for the purpose of computing the total income of the assessee and invoking the powers provided u/s 145(3) of the Act, he rejected the books of accounts of the assessee. Accordingly, he observed that accounts of the assessee are incorrect and are incomplete, therefore, true profit cannot be deduced from such accounts and details furnished. Thus, he rejected the books of accounts of the assessee to the extent of the bogus purchases and corresponding sales.

12. AO further observed the details of GP rates for the AYs 2013-14 to 2019- 20 which are tabulated as under:

| Assessment Years | Declared GP Rate (in % ) |

| 2013-14 | 0.81 |

| 2014-15 | 0.92 |

| 2015-16 | 1.52 |

| 2016-17 | 0,67 |

| 2017-18 | 2.92 |

| 2018-19 | 2.77 |

| 2019-20 | 3.69 |

13. From a perusal of the above table, AO noted, that the highest declared GP rate in the case of the assessee was for AY 2019-20 and assessee has declared G.P. of 0.81% on the total turnover for the year under consideration, hence, he calculated the GP @ 2.88% (G.P. 3.69 % – 0.81%) and added on the entire bogus transaction of Rs.20,82,19,683/-. Accordingly, he made addition of Rs.59,96,727/-. (i.e. bogus purchases and sales of Rs.20,82,19,683/- @ GP rate of 2.88%).

14. Aggrieved with the above order, assessee preferred an appeal before the ld. CIT (A) and filed detailed submissions. Ld. CIT (A), after going through the detailed submissions, sustained the addition made by the AO.

15. Aggrieved with the above order, assessee is in appeal before us.

16. At the time of hearing, ld. AR of the assessee submitted as under :-

1. The present appeal arises against the order passed by the Ld. Assessing Officer, which has been confirmed/partly confirmed by the Ld. CIT(A) without properly appreciating the facts and legal position. The assessment order is illegal, arbitrary, and passed in violation of principles of natural justice and settled law.

2. That the comment/remand report not taken from Revenue in view of the grounds raised in Appeal before CIT-(A)

3. That Panchnama is invalid and defective, bad in law, void, without jurisdiction, barred by limitation, was not produced for signatures of Assessee by the Authorized officer.

That Panchnama is invalid as the same is not produced for signatures by the assessee by the Authorized officer. Accordingly, the said Panchnama should not be read / given any weightage as said panchnama are nonest in the eye of law.

Therefore the said order is nonest under the eyes of law. Hence on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

4. Annexure J, Annexure-S and Annexure-O not provided to assessee at the time of search & seizure. Any addition without providing material is unsustainable.

5. That Assessing officer fails to bring on record that the Search party can consider any person (even he holds no authorization in writing from assessee) as authorized representative of assessee. Mr. Mukesh is treated as authorized representative of assessee even he did not hold any authorization in writing from assessee at that time to appear/present before the authorized officer on behalf of assessee at the time of search and sign the Panchnama. Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

6. The Panchnama is not correct as authorized officer is having the warrant of authorization dated 01/11/201 and search was conducted on 01/11/2018 and not in the year 201 as stated in warrant and Panch certified in the panchnama that panchnama is correctly recorded. Therefore the said order is nonest under the eyes of law. Hence on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio

7. The Panchnama is not correct as authorized officer stated in the Panchnama that search party reach for search at 3.54 A.M and Search started at 3.55 A.M. and in the intervening one minute, the warrant of authorization was read in English and Hindi by Authorized officer and personal search was also taken and Panch certified in the panchnama that panchnama is correctly recorded. Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

8. That Assessing officer fails to bring on record, under what circumstances search party leaked the information to Mr. Mukesh to arrived at the search place in late night i.e.at 3.54 A.M. on 01.11.2018 as search place is not the residential premises or any office premises but the locker place and no one is allowed to operate lockers in late night hours i.e. at 3.54 A.M. as search warrant are confidential in nature and search party is not permitted to disclose the details of search to any one until search party reaches the search place. Therefore the said assessment order is nonest under the eyes of law.

Hence on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

9. That Assessing officer fails to bring on record, under what circumstances search party search the locker before sun arises. As search can be started only after sun arises and there is no meteorological department (Mausam Vibhag) report that on 01/11/2018 at 3.54 A.M. sun arises. Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

10. That assessee has prove the identity and creditworthiness of parties from whom purchase and sale made by assessee by submitting the VAT registration documents as VAT registration is granted by State Government under VAT ACT only after verifying the credentials of prospective Dealers in compliance of procedures prescribed under the VAT Act. Therefore the additions is not sustainable under the law and on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio. No defect has been pointed out by the AO, hence, no addition is justified.

11. That assessee has prove the identity and creditworthiness of parties from whom purchase and sale made by assessee by submitting the Bank Account details as in India bank account can be opened and operated only when same is KYC complied and comply the RBI guidelines. Therefore the additions is not sustainable under the law and on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

12. That Assessing officer fails to bring on record, that VAT registration granted by concerned VAT Department in violation of VAT Act and rules and procedures prescribed by State Govt. Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is arbitrary, wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

In reference to the point 9, 10 & 11 he relied on the following decision:

Commissioner Of Income Tax 7 vs M/S Odeon Builders Pvt. Ltd. on 21 August, 2019

………

13. That Assessing officer fails to bring on record that bank accounts of parties to whom assessee deals were opened by the Banks in violation of RBI Guidelines. Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is arbitrary, wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

14. That Assessing officer fails to bring on record, that the documents filed by assessee such as copies of purchase bills, copies of purchase/ sale invoices, tax invoices in respect of the purchases/Sale, extracts of stock ledger showing entry/exit of the materials purchased, copies of bank statements to show that payment for such purchases were made through regular banking channels, etc., to establish the genuineness of the purchases were bogus /false. Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is arbitrary, wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

15. That the assessee had filed the copies of purchase bills, copies of purchase/ sale invoices, challan cum tax invoices in respect of the purchases/sales, extracts of stock ledger showing entry/exit of the materials purchased, copies of bank statements to show that payment for such purchases were made through regular banking channels, etc., to establish the genuineness of the purchases. Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is arbitrary, wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

16. That Assessing Officer fails to bring on record any material evidence to show that the purchases/sales were bogus. Mere reliance by the Assessing Officer on information obtained from the Dy. Director (Investigation) Panipat on CRIU, Insight portal of Department or the statements of persons made before the said authorities would not be sufficient to treat the Purchases/sales as bogus and thereafter to make addition. Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

17. That the sworn statement of parties before Dy. Director (Investigation) Panipat on CRIU ,Insight portal of Department/authorities, without affording the assessee any opportunity to cross examine those witnesses in this regard or the fact that these parties did not respond to notice under section 133(6) of the Act, would not in itself suffice to treat the purchases/sale as bogus and make the addition. If the AO doubted the genuineness of this said purchases, it was incumbent upon him to cause further inquiries in the matter to ascertain the genuineness or otherwise of the transactions.Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

Commissioner Of Income Tax 7 vs M/S Odeon Builders Pvt. Ltd. on 21August, 2019

………

Similarly

M/S Andaman Timber Industries vs Commr. Of Central Excise,Kolkata on 2 September, 2015

18. That the AO failed to cause any enquiry to be made to establish his suspicions that the said purchases/sales are bogus, and the documentary evidence brought on record to establish the genuineness of the purchase/sale transactions by the assessee is false, wrong and bogus. The AO has merely relied on information from investigation wing without conducting independent verification. Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

19. That after identity and genuineness established by the assessee from identification and creditworthiness, the burden shifts to the department. And all the addition is based on suspicion. That the AO failed to bring on record that the assessee booked bogus sale/purchase and money is received back by assessee in cash from these parties as no documentary evidence bought by the A.O. on record for the same. Therefore the said assessment order is nonest under the eyes of law. Hence on this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

20. That the A.O. has adopted GP of unrelated year of AY 2019-20 for earlier years for making the addition pertaining to income of AY 2013-14 to AY 2016-17 because the assessment orders were passed for the period pertaining to 2013-14 to 2016-17 and average gross profit ratio was (0.98%) whereas the Ld. A.O. arbitrately and using the pick and choose policy took the GP of Assessment year 2019-20. In the year 2019-20 major trading was Pulses and there was negligible trading of Rice while in the AY 2013-14 to 2015-16 trading of rice was 24% to 40% which can be verified from the trading A/c of the respective year. It is pertaining to entioned here that the transaction made i 2019-20 have no relation/linkage with the transaction of AY 2013-14 to 2016- 17. Further the Ld. A.O not has brought on record the reasons for taking the GP of 2019-20 which itself shows that the Ld. A.O has not followed procedures a s Ld. A.O. is duty bound to disclosed the same on the office records. In the view of the above stated facts and submiss ion it is humbly requested to that the assessment order be set a sided as the same is arbitrary, wrong, baseless.

1. GPTakenforadditionofAY2019-20(due tohigherin6 year s)3.69% instead of addition pertain to 2013-2014:-

In the FY 2010-11 the GP was 0.76%

In the FY 2011-1 the GP was 0.91%

That, therefore the GP data of previous year’s asked in t e previous date of hearing is provided.

2. Year-wise % of sale of Rice (As rice was purchased from alleged parties)

| Sr.No. | AY | % of Rice | % of Pules & other |

GP Ratio |

| 01 | 2012-13 | 86% | 14% | 0.92% |

| 02 | 2013-14 | 14.80% | (0.412%)Pule (84.75%)Chan a | 0.81% |

| 03 | 2014-15 | 24% | 76% (Pules+ Channa) | 0.92% |

| 04 | 2015-16 | 40% | 58% (Pules + Channa) | 1.52% |

| 05 | 2016-17 | 5% | 93% (Pules +

Channa+Moong +Matar+Lobiya) |

0.67% |

| 06 | 2017-18 | 16% | 82% (Pules + Channa+Moong +Matar+Lobiya ) |

2.92% |

| 07 | 2018-19 | 1.20% | 98.80% (Pules + Channa+Moong) | 2.77% |

| 8 | 2019-20 | 0% | 99.93%

(Masoor+Rajma |

3.69% |

Case Law:-

ITAT, ALLAHABAD BENCH, ALLAHABAD in ITA No.137/Alld/2023 A.Y.2017-18 Jai Bajrang Gur Bhandar, Mutthiganj, Allahabad, U.P. vs. Income Tax Officer, Ward-1(2), Allahabad.

21. In view of non compliance of instructions issued by CBDT by the Ld.A.O. while passing the said order. Hence the order passed by the learned A.O. is bad, both in the eye of law and on the facts.

That the said order has being passed by the Ld. A.O. without going through the contents of Sections of the Income Tax Act, 1961, circulars issued by the CBDT deliberately, intentionally and without application of mind by overriding their jurisdictions in excess of his duties and responsibilities and hence the said order is not sustainable under the eyes of law. In view of this ground alone the assessment order is wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.

22. The assessment order is illegal, void, arbitrary, without jurisdiction, barred by limitation, bad-in –law. Hence the assessment order is arbitrary, wrong, baseless and liable to be quash/set-aside as the same is void-ab-initio.”

17. On the other hand, ld. DR of the Revenue relied on the findings of the lower authorities.

18. Considered the rival submissions and material placed on record. We observed that the assessee has made transactions with five parties, details of which are given above in the table, have not responded to the notices u/s 133(6) of the Act, therefore, the AO could not verify the genuineness of the purchases. We further observed that the assessee is engaged in trading business and sales were accepted against the purchases and without purchases, the assessee could not have achieved the sales. Further we observed that the AO has fully accepted the sales declared by the assessee. We further observed that all the transactions are discharged through banking channels.

19. Further we observed that the assessee has proved the identity and creditworthiness of parties from whom purchase and sales made by assessee by submitting the VAT registration documents as VAT registration is granted by State Government under VAT ACT only after verifying the credentials of prospective Dealers in compliance of procedures prescribed under the VAT Act.

20. We further observed that assessee has proved the identity and creditworthiness of parties from whom purchase and sale made by assessee by submitting the Bank Account details as in India, bank account can be opened and operated only when same is KYC complied and comply the RBI guidelines.

21. Further we also observed that the assessee is engaged in a trading business and it had declared margin during AYs 2013-14 to 2016-17 are in the range of 0.67% to 1.52% whereas the Assessing Officer had adopted the profit declared in the AY 2019-20. It was submitted before us that the profit declared in that year had different business model, the same cannot be adopted for the year under consideration.

22. However, we observed that the genuineness of the purchases would inter alia also include explanation with regard to the source for paying for such purchases. Explaining the source of purchases would be one of the prime considerations for concluding whether the purchases have been made from accounted or unaccounted sources and to test the veracity of transaction being only accommodation entry. It is well settled and undisputed that the onus of proving any genuineness of the expenditure claimed as deduction is on the assessee. The primary onus is on the assessee to discharge his burden to prove the purchases, which an assessee has claimed as a deduction under the Income Tax Act for arriving at the taxable income.

23. In view of our above discussion and detailed submissions of the ld. AR which are reproduced above, we observed that applying of GP 2.88% of the bogus purchases is excessive, thus it is deemed appropriate in the larger interest of justice and in all fairness that we restrict it to GP 1% which is line with the average gross profit declared by the assessee of 0.67% to 1.52% during the period i.e. AYs 2013-14 to AY 2016-17 and would be just and proper with a rider that the same shall not be treated as a precedent. Necessary computation shall follow as per law. We order accordingly and the grounds raised by the assessee are partly allowed.

24. In the result, the appeal filed by the assessee for AY 2013-14 is partly allowed.

25. Since the facts in AYs 2014-15, 2015-16 and 2016-17 are exactly similar to Assessment Year 2013-14, our above findings in AY 2013-14 are applicable mutatis mutandis in Assessment Years 2014-15, 2015-16 and 2016-17. Accordingly, the appeals filed by the Revenue for AYs 201415, 2015-16 and 2016-17 are partly allowed.

26. To sum up : all the appeals filed by the assessee are partly allowed.

Order pronounced in the open court on this 24th day of June, 2026

Author Bio