Case Law Details

Delhi International Cargo Terminal Pvt. Ltd. Vs DCIT (ITAT Mumbai)

Mumbai ITAT: Typographical Error in Tax Audit Report Cannot Deny PF Deduction if Contribution Was Actually Paid Within Due Date

The Mumbai ITAT held that a mere typographical error in the Tax Audit Report cannot justify disallowance of employees’ Provident Fund (PF) contribution under section 36(1)(va) where the evidence establishes that the contribution was in fact deposited within the statutory due date. In this case, the tax auditor mistakenly reported the date of deposit as 11.01.2022 instead of the correct date 05.01.2023, leading CPC to make a disallowance of ₹6,65,674 while processing the return under section 143(1). The Tribunal noted that the incorrect date itself demonstrated a clerical mistake, as it preceded the relevant accounting period, and the PF challans clearly proved that the payment was made on 05.01.2023, before the due date of 15.01.2023.

The Tribunal further observed that the assessee had produced the PF challans and supporting documents before the appellate authority, but these were not properly considered. Since there was no actual delay in remittance, the Supreme Court’s decision in Checkmate Services (P.) Ltd. v. CIT (448 ITR 518) was held to be inapplicable. The matter was restored to the Assessing Officer only for the limited purpose of verifying the challans, with a direction to allow the deduction upon verification. The issue relating to unabsorbed depreciation was also restored to the Assessing Officer for fresh consideration. Accordingly, the appeal was allowed for statistical purposes.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

The instant appeal of the assessee filed against the order of the Ld. Commissioner of Income Tax-Appeals ADDL/JCIT(A), Panaji [for brevity the “Ld. CIT(A)”], order passed under section 250 of the Income Tax Act 1961 (for brevity ‘the Act’) for Assessment Year 2023-24, date of order 22.01.2026. The impugned order emanated from the order of the CPC, Bengaluru (for brevity the ‘Ld. AO’) order passed under section 143(1) of the Act date of order 27.03.2024.

2. The brief facts of the case is that the assessee filed the return by declaring total income nil and carrying on business of Inland Container Deport (ICD) and related Logistic Services. The assessee’s return was processed u/sec. 143(1) of the Act and the total income was determined amount to Rs.6,65,940/- against the return total income of nil. During the processing of the return the Ld. AO disallowed a sum of Rs.6,65,940/- claimed deduction u/sec. 36(1)(va) of the Act on basis of the tax audit report where a chart was prepared showing due date of payment of provident fund dues and actual date of payment of provident fund for the item mentioned in Serial No.28 amount to Rs.6,65,674/-. The due date for depositing sum received from employees as PF contribution for month of December 2022 was correctly mentioned 15.01.2023 but the date of actual payment was erroneously stated as 11.01.2022 which is 369 days before the due date. Instead of actual date of payment was 05.01.2023. There was typographical error made by the Tax Auditor where the amount was paid on 05.01.2023 that is 10 days before the due date. The assessee challenged the impugned assessment order before the Ld. CIT(A). But the Ld. CIT(A) rejected the appeal and uphold the additions. Being aggrieved assessee filed an appeal before us.

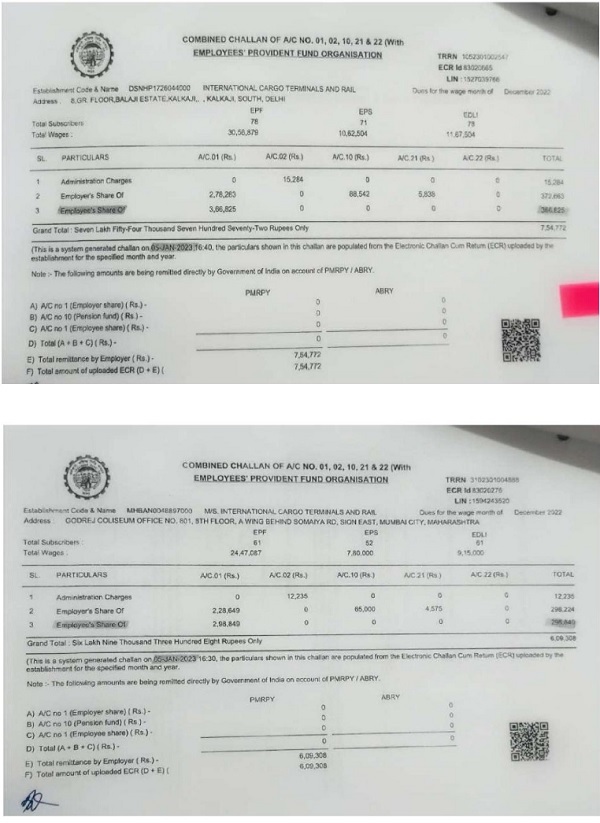

3. The Ld. AR argued and filed a paper book comprising pages 1 to 62 which has been placed on record. The Ld. AR submitted that the addition of Rs. 6,65,674/- made under section 36(1)(va) of the Act is factually incorrect and arose solely due to a typographical error in the Tax Audit Report. It was contended that, in the audit report, the date of deposit of employees’ contribution to Provident Fund for the month of December 2022 was inadvertently mentioned as 11.01.2022 instead of the correct date, 05.01.2023. The due date for remittance of the said contribution was 15.01.2023, and the payment was actually made on 05.01.2023, well within the prescribed due date. The Ld. AR drew attention to the PF challans placed on record evidencing the payment of Rs. 6,65,674/- (Delhi: Rs. 3,66,825/- and Mumbai: Rs. 2,98,849/-) on 05.01.2023. It was argued that the erroneous date mentioned in the audit report is self-evidently a clerical mistake, as the stated date precedes even the commencement of the relevant accounting period. Accordingly, since the employees’ contribution was duly deposited within the prescribed time limit, the disallowance made under section 36(1)(va) is unsustainable in law and deserves to be deleted.

4. The Ld. AR invited our attention in APB page 4 and 5 where the alleged challans related to Employees’ PF contribution amount to Rs.3,66,825/- and Rs.2,98,849/- which are enclosed herewith. The copies of the challans are reproduced as below:

5. The Ld. DR argued and contended that the assessee had made the mistake during filing of the TAR (Tax Audit Report). The Auditor has made the mistake for mentioning the due date which is 369 days before from the date of the payment of the challans. Due to this specific error the Ld. AO had added back the alleged amount with the total income of the assessee. During the appellate proceeding the assessee was not able to submit the relevant documents and challans before the Ld. CIT(A) and accordingly the addition was confirmed. The relevant part of the appellate order in page no.28 is reproduced as below:

“On careful perusal of the records, it is observed that:

1. The adjustment has been made strictly on the basis of data furnished by the appellant itself in the Tax Audit Report, which forms part of the return of income.

2. During the appellate proceedings, the appellant failed to furnish any documentary evidence, such as:

-

- copy of PF challan,

- bank statement evidencing payment, or

- confirmation from the PF authorities, to substantiate its claim that the payment was made within the due date,

- Copy of audit report.

3. Mere assertion that the error was typographical, without supporting primary evidence, cannot be accepted, especially when the statutory audit report clearly reflects a delayed payment.

4. It is a settled principle of law that onus lies on the appellant to substantiate the claim made in the return of income. In the absence of documentary proof, the claim remains unverified and unsubstantiated.

5. The CPC is empowered to make adjustments u/s 143(1)(a) where there is inconsistency between the return and the audit report. In the present case, the adjustment is strictly in accordance with law and within the scope of section 143(1).”

6. We have heard the rival submissions and perused the material available on record. The assessee claimed deduction under section 36(1)(va) of the Act in respect of employees’ contribution towards Provident Fund. The dispute pertains to a sum of Rs. 6,65,674/-, comprising payments of Rs. 3,66,825/- and Rs. 2,98,849/-, which were remitted through two separate challans on 05.01.2023. It is observed that the Tax Auditor, while furnishing the Tax Audit Report, inadvertently mentioned the date of payment as 11.01.2022 instead of the actual date of payment, i.e., 05.01.2023. The Ld. AR submitted that during the appellate proceedings, the assessee had furnished all relevant documentary evidence vide letter dated 02.01.2025, copies of which are placed at pages 1 to 3 of the APB. The corresponding PF challans and the response filed through the e-proceeding portal are also placed at pages 4 to 7 of the APB. However, without taking cognizance of these documents, the Ld. CIT(A) proceeded on the assumption that no supporting evidence had been furnished by the assessee. Upon examination of the record, we find merit in the contention of the assessee. The error in mentioning the date of payment as 11.01.2022 is clearly a clerical and typographical mistake committed by the Tax Auditor, particularly when the said date precedes the relevant period itself. The challans evidencing payment of Rs.3,66,825/- and Rs.2,98,849/-, aggregating to Rs.6,65,674/-, have been placed before us and form part of the certified paper book. The same were also furnished before the Ld. CIT(A). Therefore, there remains no factual dispute that the employees’ contribution was deposited on 05.01.2023, well before the statutory due date prescribed under the relevant Provident Fund provisions. Consequently, the ratio laid down by the Hon’ble Supreme Court in Checkmate Services (P.) Ltd. v. CIT reported in (2022) 448 ITR 518 (SC) would have no application to the facts of the present case, as there is no delay whatsoever in the remittance of the employees’ contribution.

7. In view of the foregoing discussion, we find that there is no default on the part of the assessee in depositing the employees’ contribution to Provident Fund within the prescribed due date and, therefore, no violation of section 36(1)(va) of the Act can be attributed to the assessee. However, in the interest of verification, we restore the matter to the file of the Ld. AO for the limited purpose of verifying the challans evidencing payment of the aforesaid amount. Upon such verification, the deduction claimed by the assessee under section 36(1)(va) shall be allowed in accordance with law. Needless to state, the assessee shall be afforded a reasonable opportunity of being heard during the set-aside proceedings.

The assessee has also raised grounds relating to the claim of unabsorbed depreciation of earlier years. Since the adjudication of the said issue is consequential in nature, the same is also restored to the file of the Ld. AO for fresh consideration in accordance with law.

Accordingly, the appeal of the assessee is allowed for statistical purposes.

8. In the result, the appeal of the assessee bearing ITA No.3138/Mum/2026 is allowed for statistical purpose.

Order pronounced in the open court on 24th day of June 2026.

Author Bio