Case Law Details

General Agencies (Kolkata) Pvt. Ltd. Vs Commissioner of Customs (Appeals) (CESTAT Kolkata)

The Customs, Excise and Service Tax Appellate Tribunal (CESTAT), Kolkata allowed the appeal filed by General Agencies (Kolkata) Pvt. Ltd. and set aside penalties imposed under Sections 112(a) and 114AA of the Customs Act, 1962.

The appellant had imported Kerosene Generator Sets by classifying the goods under CTH 85023990 and filed Bills of Entry dated 25.08.2020 and 26.10.2021. Along with the Bills of Entry, the appellant submitted all relevant documents, including Emission Certificates issued by Envirotech East Pvt. Ltd., an empanelled laboratory authorized by the Ministry of Environment. After verification of the Bills of Entry and accompanying documents, including the environmental certificates, Customs authorities permitted clearance of both consignments for home consumption.

On 19.01.2023, a Show Cause Notice was issued alleging that the goods were correctly classifiable under CTH 85022090 instead of CTH 85023990. The notice also alleged that the environmental certificate did not comply with the applicable notification because it was not issued in the prescribed “Type Approval” form. The adjudicating authority reclassified the goods and imposed penalties of Rs. 15 lakh under Section 112(a)(i) and Rs. 25 lakh under Section 114AA of the Customs Act. The Commissioner (Appeals) upheld the order, leading to the present appeal.

The appellant submitted that the applicable environmental standards were contained in Notification GSR 535(E) dated 07.08.2013 and that Envirotech East Pvt. Ltd. was an authorized testing agency under the Ministry of Environment’s notification dated 15.11.2018. The appellant argued that the emission certificate issued by Envirotech, together with the manufacturer’s quality report containing technical specifications, demonstrated compliance with the prescribed environmental requirements. It contended that Customs had examined all documents at the time of import and allowed clearance only after verification. According to the appellant, the only allegation in the Show Cause Notice was that the certificate was not in the prescribed “Type Approval” format, which by itself could not justify penalties, particularly under Section 114AA, as the certificate had been issued by a duly authorized agency.

The appellant further submitted that the value of both consignments was approximately Rs. 39 lakh and the customs duty involved was about Rs. 11 lakh, making the penalties imposed disproportionate even if any contravention were assumed.

The Revenue argued that Notification GSR 535(E) specifically required a Type Approval Certificate. It submitted that the certificate produced by Envirotech did not contain details regarding noise levels and therefore failed to satisfy the notification. According to the Revenue, failure to fulfil the prescribed conditions justified the penalties.

After examining the records, the Tribunal found that Envirotech East Pvt. Ltd. was a duly notified agency authorized to conduct tests and issue certificates. It also noted that the emission certificate had been submitted along with the Bills of Entry and accepted by Customs without objection at the time of assessment. The Show Cause Notice was issued more than two years after clearance of the first consignment and more than one year and three months after clearance of the second consignment, with the only objection being that the certificate was not in the “Type Approval” form.

The Tribunal observed that the relevant notification requiring a Type Approval Certificate was already within the knowledge of Customs authorities when the consignments were assessed. Despite examining the certificates and other documents, Customs did not raise any objection before granting clearance. The Tribunal held that if Customs failed to detect any deficiency at the time of import, the importer was entitled to entertain a bona fide belief that the certificate issued by an authorized agency satisfied the notification requirements.

The Tribunal further observed that even if the allegation was that the goods did not comply with environmental requirements, issuing a Show Cause Notice after the goods had already been cleared and sold could not prevent any alleged pollution. It described the matter as a case where the Revenue had failed to detect the alleged deficiency despite having access to all relevant documents at the time of import.

Regarding the Revenue’s submission that the certificate lacked noise level details, the Tribunal referred to the manufacturer’s technical specifications, which indicated a maximum noise level of 71 dBA, well below the maximum permissible limit of 86 dBA prescribed in the notification.

The Tribunal found no evidence that the appellant had attempted to suppress or conceal any material facts. It held that the appellant had acted bona fide by submitting all relevant documents, including the emission certificate issued by an authorized agency. The Tribunal concluded that the failure to identify the absence of a Type Approval Certificate at the time of assessment was attributable to the Revenue and not to any concealment or false declaration by the importer.

Holding that the requirements for imposing penalties under Sections 112(a) and 114AA were not satisfied, the Tribunal set aside both penalties. The appeal was allowed with consequential relief, if any, in accordance with law.

FULL TEXT OF THE CESTAT KOLKATA ORDER

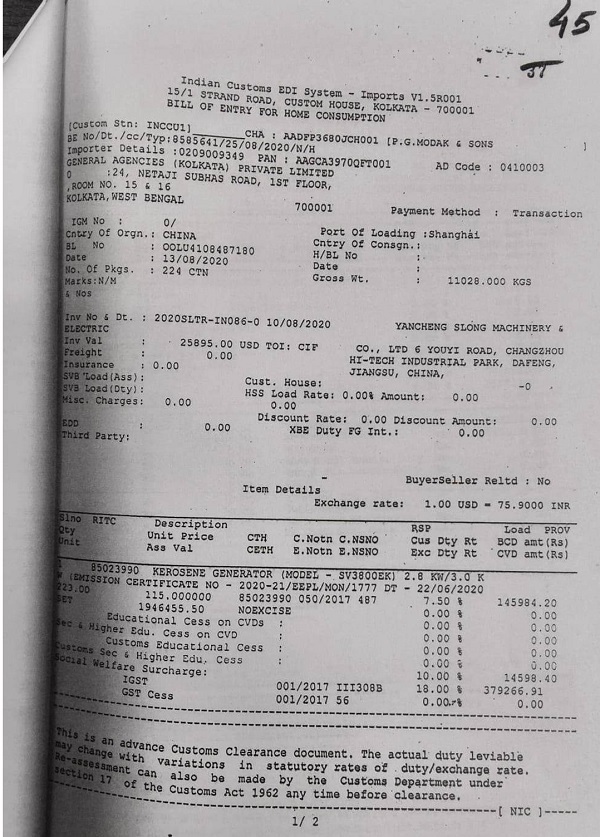

The appellant imported „Kerosene Generator Sets‟ adopting CTH 85023990 for classification of the imported goods, for which Bill of Entry No. 8585641 dated 25/08/2020 was filed. They also enclosed all the relevant documents alongwith Emission Certificate issued by Envirotech East Pvt. Ltd. [Envirotech for short] laboratory, Ministry of Environment. Similarly one more consignment was imported on 26.10.2021 and along with all the documents including the Emission Certificate[Environment Certificates] were submitted.After due verification of the Bills of Entry and the other documents including the Environment Certificates, the Customs officers allowed the consignment to be cleared for home consumption. Subsequently, on 19.01.2023 a Show Cause Notice was issued alleging that the classification is required to be done under CTH 85022090 instead of CTH 85023990. The Show Cause Notice also alleged that the certificate issued was not in conformity with the conditions given under the Notification. After due process, the Adjudicating Authority held that the goods are required to be classified under CTH 85022090. He also imposed a penalty of Rs. 1500000 under Section 112(a)(i) and Rs. 25,00,000/- under Section 114AA of the Customs Act, 1962.Being aggrieved, the appellant filed their appeal before the Commissioner (Appeal) who has dismissed the same. Therefore, the appellant is before the Tribunal.

2. The Ld. Advocate appearing on behalf of the appellant makes the following submissions.

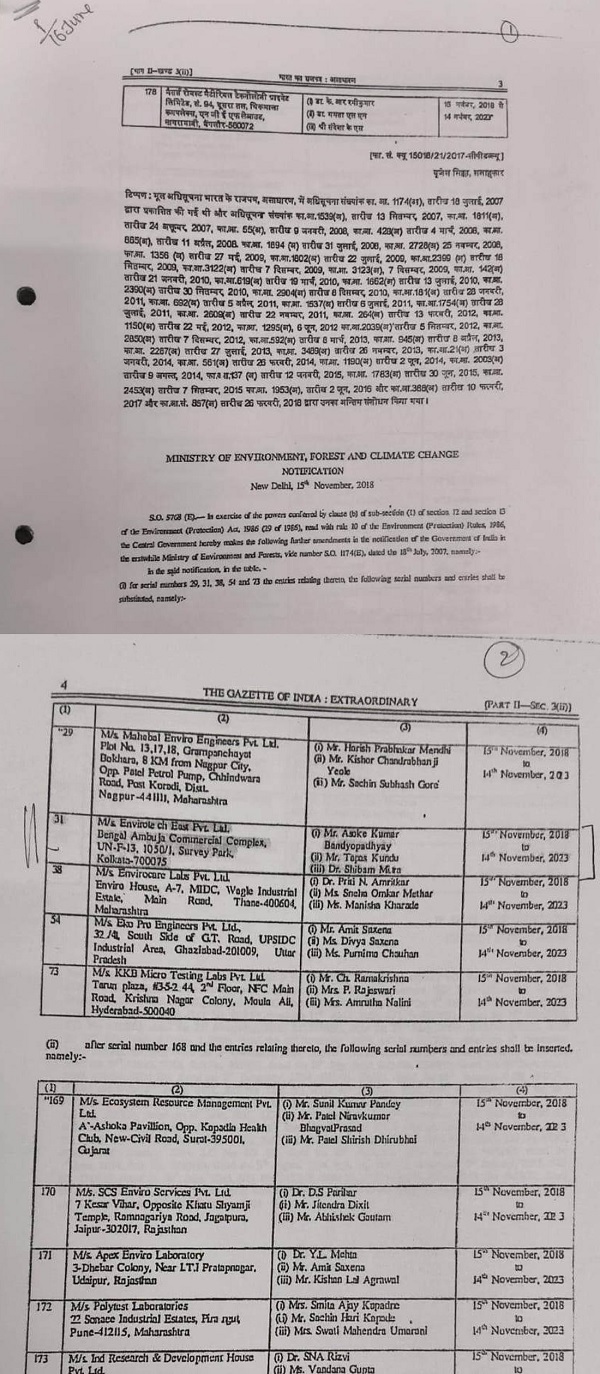

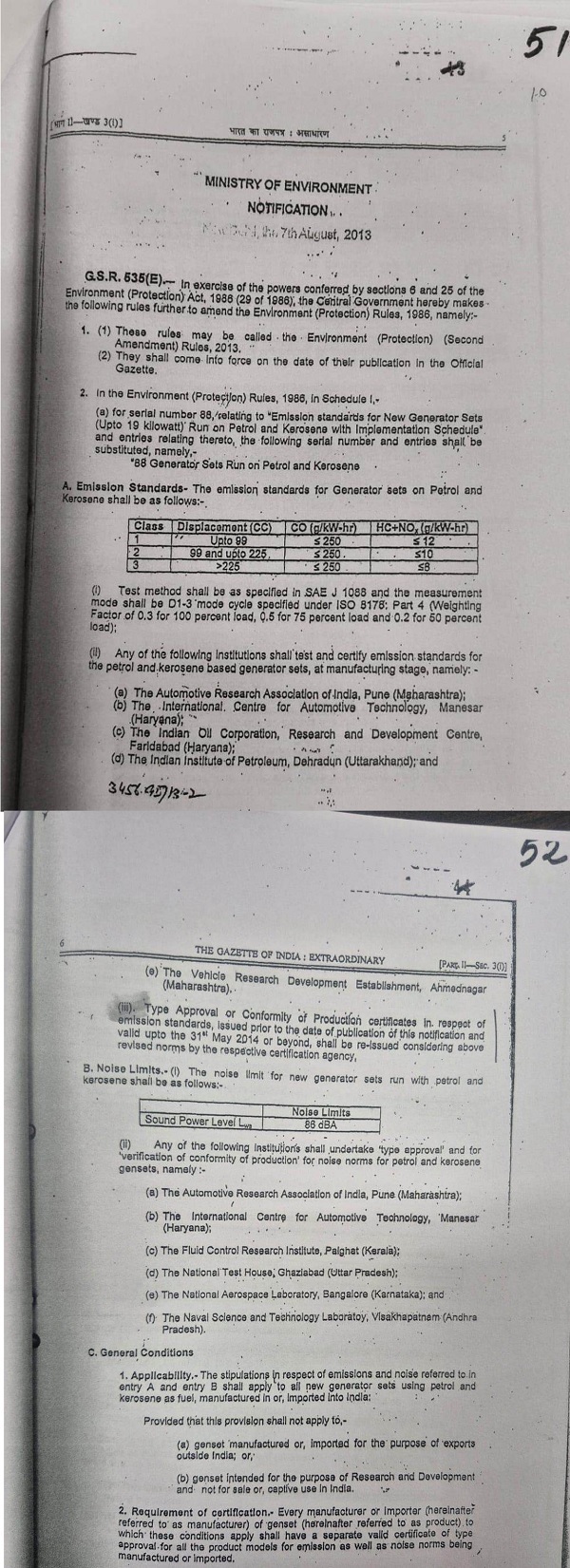

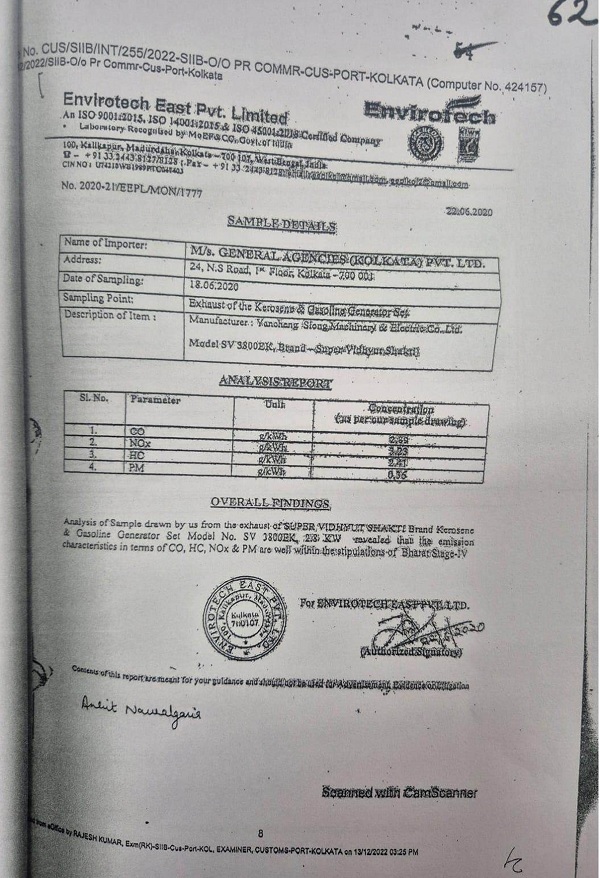

3. With reference to the relevant Notification issued by Ministry of Environment is GSR 535 (E) dated 7th August, 2013, he takes us through to page no. 51 & 52 of the appeal paper book. He submits that the “Emission standards” and the noise level standards are specified in this notification. He then takes us to Notification dated 15.11.2018 giving details of the empanelled firms which are authorized to take up the necessary tests and to issue the environment certificate. He points out that the certificate in respect of the goods imported by the appellant, have been issued by the M/s. Envirotech East Pvt. Ltd., who are listed at Sl No. 31 of the Notification dated 15.11.2018. He also takes us through to the certificate issued by this firmon closed at Page 62 of the appeal book.

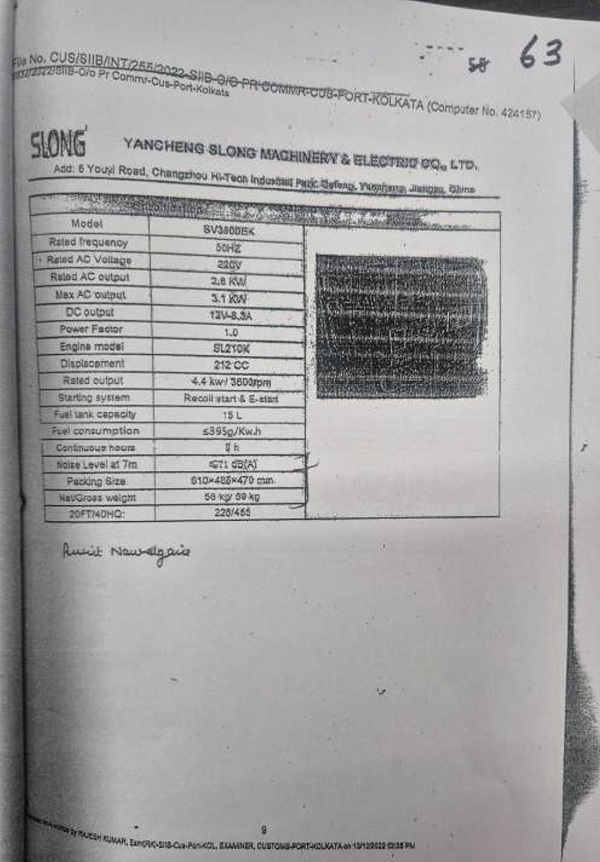

4. He submits that the certificate issued was submitted alongwith other documents to the Customs officials at the time of imports. Only after thorough verification of all the documents, the Bills of Entry were assessed and the goods allowed to be cleared. He also submits that apart from filing the certificate from Envirotech, they have also submitted the Quality Report issued by the manufacturer Yancheng Slong Machinery & Electric Co. Ltd. [enclosed at Page 63 of the appeal book], wherein all the technical specifications have been given.

5. He submits that a harmonious reading of the Notifications and Certificate issued by the Envirotech and Technical Specification certified by the manufacturer would clarify that the imported goods meet all the conditions set under notification No. GSR 535(E) dated 07.08.2013. As per him the Revenue has gone on to issue the Show Cause Notice only on the ground that “Type Approval” certificate, as specified in the Notification dated 7.8.2013, was not issued by Envirotech. Taking this ground, the appellant has been imposed with the penalty of Rs. 15,00,000/- under Section 112 (a)(i) of the Customs Act, 1962 and penalty of Rs. 25,00,000/- under Section 114AA of the Customs Act, 1962. He submits that the non-providing of the „Type Approval‟ on its own would not make the appellant to suffer the penalty under Section 114AA, as the appellant has provided the Certificate issue by the duly authorized agency by the Ministry of Environment.

6. He takes us through the value involved in the consignments which is to the extent of about Rs. 39,00,000/- in respect of both the consignments and the total Custom Duty involved is for about Rs. 11,00,000/-.

7. Considering these facts, even as the appellant submits that no penalty was required to be imposed, without prejudice to this stand, they submit that the penalties imposed disproportionate to the alleged contravention and the Customs Duty involved. He prays that the appeal may be allowed.

8. The Ld. Authorized Representative submits that the Notification dated 07.08.2013 specifies that Type Approval Certificate has to be obtained by the importer. He points out that the appellant failed to provide the Certificate on “type approval” basis. He submits that the certificate issued by Envirotech to does not contain any details of Noise Levels. As per the Notification if the Noise level is 86dBA, the Gen Sets would not meet the Environment specifications.. As the conditions set in the Notification has not been fulfilled, he justifies the penalties imposed on the appellant.

9. Heard both sides and perused the Appeal papers and documents submitted.

10. It would be important to go through some of the documents submitted by the appellant, which are extracted below:

11. The above document clarifies that M/s Envirotech East Pvt. Ltd., is duly notified to carried out tests and issue the Certificate.

12. The extract of the above Bill of Entry show the appellant has filed Emission Certificate No.2020021/EEPL/Mon/1777 dt 22.6.2020 at the time offering the imported consignment for inspection / Bill of Entry clearance.

13. The above documents forming part of Notification No. GSR 535(E) dated 7thAugust 2013, specifies the technical details which should be tested and certified. It is also seen that the Notification specifies that „Type Approval‟ Certificate should be issued. The maximum Noise Level has been specified as 86 dBA

14. This is the certificate issued by duly authorized agency Envirotech. Admittedly, this Certificate was enclosed along with the Bills of Entry and submitted to Customs officials along with other documents. After more than 2 years from the date of clearance of the first consignment and after more than 1 year 3 months from the date of clearance of the second consignment, the SCN has been issued. The only ground taken in the SCN is about non-providing of the Certificate in „Type Approval‟ form. Admittedly, the Certificate has been issued by the authorized agency Envirotech. After the Certificate issue was issued and presented before the Customs Officials, no objection was raised about the same not being in the nature of „Type Approval‟. The Notification dated 7th August 2013, was very much within the knowledge of the Customs Officials. But still no objection was raised. Even if for a moment it is taken that this has resulted in allowing a polluting Genset to be cleared out of the Customs area, we do not see as how this act of issuing the SCN could prevent the pollution, when the goods have been sold long back in the market. This is a classic case of the Revenue failing to prevent the clearance even after going through the Certificate. The appellant would have entertained Bonafide belief that when the Certificate is issued by an Authorize agency like Envirotech, they would have followed all the norms required under the Notification.

15. This is the Technical Specification of the Genset given by the manufacturer.

16. Revenue had access to all these documents. Only after verifying the Certificates issued by Envirotech, and other documents presented by the appellant, the goods were released for home consumption by the Customs Authorities.

17. At the time of hearing, the Ld. A R submits that one important test which has not been carried out by Envirotech towards the dBA. However, when we go through the product specification given by the Manufacturer [reproduced above], the maximum permitted dBA by the manufacturer is less than or equal to 71 dBA, which is much less than the Noise level of 86 dBA mentioned in the Notification.

18. Considering the factual details discussed above, we do not find that any attempt was made by the appellant to suppress or conceal any facts. They have acted in a Bonafide way.

19. Section 112(a) and 114AA read as under:

112. Penalty for improper importation of goods, etc.

(a) Any person, who, in relation to any goods, does or omits to do any act which act or omission would render such goods liable to confiscation under section 111, or abets the doing or omission of such an act,

114AA. Penalty for use of false and incorrect material.

If a person knowingly or intentionally makes, signs or uses, or causes to be made, signed or used, any declaration, statement or document which is false or incorrect in any material particular, in the transaction of any business for the purposes of this Act, shall be liable to a penalty not exceeding five times the value of goods.

20. As per our discussions in the earlier paragraphs, the appellant has acted with Bonafide intention, submitting all the documents, Emissions Certificate issued by a duly authorized agency at the time of imports. The error of non-detection of the Type Approval certificate at the time of the import is on the part of the Revenue, rather than it being any act of concealment on the part of the appellant. Therefore, we hold no case has been made out against the appellant to impose penalties under Section 112(a) and Section 114AA

21. Accordingly, we set aside the penalties imposed on the appellant.

22. The appeal stands allowed. The appellant would be eligible for consequential relief, if any as per law.

(Pronounced in open court on 19.06.2026)

Author Bio