Case Law Details

DCIT Vs Paramount Propbuild Pvt. Ltd. (ITAT Delhi)

The Income Tax Appellate Tribunal (ITAT), Delhi, dismissed the Revenue’s appeal and upheld the order of the Commissioner of Income Tax (Appeals) [CIT(A)] deleting the addition of ₹6.25 crore made under Section 68 of the Income Tax Act on account of unsecured loans received by the assessee from four lender companies.

The case arose from a search and seizure operation conducted under Section 132 in the Paramount, Gulshan and Ajnara Group on 11 March 2011. During the assessment proceedings for Assessment Year 2011-12, the Assessing Officer (AO) made an addition of ₹6.25 crore under Section 68, alleging that the assessee had failed to establish the identity of the lenders, the genuineness of the loan transactions, and the creditworthiness of the four lending companies. The AO also noted that summons issued to the lenders were returned unserved.

Before the CIT(A), the assessee filed additional evidence under Rule 46A, explaining that sufficient opportunity had not been provided during assessment proceedings. The documents included copies of the lenders’ PAN cards, confirmations, income tax returns, audited financial statements, Memorandum of Association, certificates of incorporation, board resolutions, loan sanction letters, foreclosure letters, and bank statements. The CIT(A) forwarded these documents to the AO for comments on both admissibility and merits. While the AO objected to the admission of the additional evidence, no adverse comments were made on the merits or authenticity of the documents in the remand report. The CIT(A) therefore admitted the evidence and proceeded to examine the transactions.

The CIT(A) found that all four lenders were Non-Banking Financial Companies (NBFCs), possessed PAN, maintained bank accounts, filed returns with the Registrar of Companies and Income Tax Department, maintained audited financial statements, and continued to remain active. The loans had been received through banking channels in September 2010 and repaid through banking channels in October 2010, well before the search conducted in March 2011 and prior to any notice issued under Sections 153A or 143(2). The CIT(A) also examined the financial position of the lenders and noted that each had substantial net worth during Financial Year 2009-10, ranging from over ₹20 crore to ₹37 crore, which was sufficient to advance the loans. The lenders also continued to have substantial net worth in later years. Based on these facts, the CIT(A) held that the assessee had discharged the burden of proving the identity, genuineness, and creditworthiness of the lenders and deleted the addition.

Before the Tribunal, the Revenue argued that the assessee had failed to produce the lenders during assessment proceedings and that the additional evidence should not have been admitted. The assessee submitted that the CIT(A) had correctly admitted the evidence, the AO had not disputed it on merits in the remand report, and all transactions were genuine banking transactions involving NBFCs.

The Tribunal observed that the Revenue failed to rebut the factual findings recorded by the CIT(A). It noted that the loans were repaid within a month through banking channels, the lenders possessed adequate financial capacity, and the AO had not questioned the merits of the additional evidence. The Tribunal also relied on the Gujarat High Court decision in PCIT v. Ojas Tarmake (P.) Ltd., which held that where loans are received and repaid through banking channels during the same year, deletion of the addition under Section 68 is justified. Finding no infirmity in the CIT(A)’s order, the Tribunal upheld the deletion of the addition of ₹6.25 crore and dismissed the Revenue’s appeal.

FULL TEXT OF THE ORDER OF ITAT DELHI

The present appeal is filed by Revenue against the order dated 02.08.2024 by Ld. Commissioner of Income Tax (A), National Faceless Appeal Centre (“NFAC”), Delhi [“Ld.CIT(A)”] in Appeal No. NFAC/2010-11/10108566 passed u/s 250 of the Income Tax Act, 1961 [“the Act”] arising out of assessment order dated 28.03.2013 passed u/s 143(3)/153A of the Act pertaining to Assessment Year 2011-12.

2. Brief facts of the case are that a search and seizure action was carried out u/s 132 of the Act in the case of M/s. Paramount, Gulshan & Ajnara Group of cases on 11.03.2011. The assessee company being part of the Group, its office was also searched. The assessee company was engaged in the business of development of residential and commercial projects in Uttar Pradesh. The assessee filed its return of income on 25.09.2011, declaring total income of INR 9,14,95,371/-. This being the year of search, notices u/s 143(2) was issued, followed by notices u/s 142(1) of the Act which were issued from time to time. The AO by alleging that assessee had purchased the goods which remained unverified and accordingly, made the addition of INR 22,18,88,782/-. Besides this, addition of INR 6,25,00,000/- was made u/s 68 on account of loans taken from Four parties by alleging that the assessee has failed to prove the genuineness of the transactions and creditworthiness of the lenders.

3. Aggrieved by the said order, assessee preferred appeal before Ld.CIT(A) who vide order dated 02.08.2024, allowed the appeal of the assessee.

4. Aggrieved by the said order, Revenue is in appeal before the Tribunal by taking various Grounds of appeal mentioned in the appeal memo.

5. Both the Grounds of appeal raised by the Revenue are with respect to the deletion of addition of INR 6,25,00,000/- made u/s 68 of the Act on account of undisclosed loans.

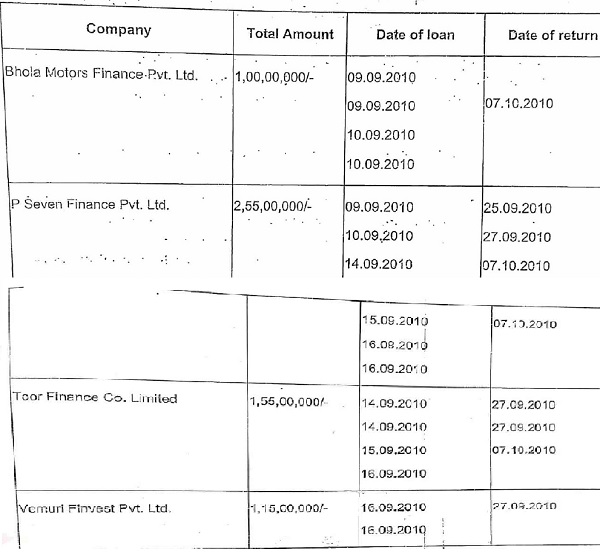

6. Before us, Ld.CIT DR for the Revenue submits that AO at page 4 of the assessment order has discussed this issue in detail wherein it is observed by the AO that certain documents were found and seized during the course of search indicating that assessee has taken loans during the year under appeal from four parties mentioned as below:-

| i. | Bhola Motor Finance (P) Limited | INR 1.00 crore |

| ii. | P. Seven General Finance (P) Ltd. | INR 2.55 crore |

| iii. | Toor Finance Company Limited | INR 1.55 crore |

| iv. | Vemuri Finvest (P.) Ltd. | INR 1.15 crore |

7. As per Ld. CIT DR for the Revenue, the AO had issued summons to these parties however, the notices issued returned back unserved. Therefore, identity and genuineness of the transactions and creditworthiness of the lenders remained unexplained. Ld.CIT DR submits that though all the companies are group companies of the assessee however, despite of giving notices, none of them appeared before the AO as well as before Ld. CIT(A) nor any compliance was made. Before ld. CIT(A), assessee has filed certain details of these parties as additional evidences. Ld. CIT DR submits that Ld. CIT(A) as admitted the additional evidences by ignoring the fact that despite of sufficient opportunities provided by the AO, no details whatsoever were filed therefore, AO has rightly made the addition and the same deserves to be restored.

8. On the other hand, Ld.AR for the assessee submits that during the appellate proceedings, assessee has filed additional evidences which are discussed by Ld.CIT(A) at pages 27 to 29 and admitted the same. He drew our attention to the observations made by Ld.CIT(A) in para 2 at page 18 of the order wherein Ld.CIT(A) has observed that AO in his Remand Report has not controverted the additional evidences filed by the assessee under Rule 46A nor rebutted the same on merits. Ld.AR further submits that loans taken were rapid during the year itself and entire transactions of loans were much before the search carried out in the case. As per ld. AR, all the transactions were carried out through banking channel and lender companies are NBFCs. With respect to the identity and genuineness of the transactions and creditworthiness of the lenders, assessee has filed their PAN, bank statements, filing return to ROC, financial statements etc. which have not been doubted by the AO in the Remand Report. Ld. AR submits that Ld.CIT(A) after considering these facts, has deleted the additions made by AO and requested for the confirmation of the same.

9. Heard the contentions of both parties at length and perused the material available on record. It is observed that though during the course of assessment proceedings, assessee has not filed details with respect to the lender companies however, during the course of appellate proceedings, assessee has filed all the relevant details as additional evidence in order to establish the identity and creditworthiness of the lender companies and genuineness of the transactions. The details so submitted are as under:-

i. Copy of PAN of lenders;

ii. Copy of confirmations of lenders;

iii. Copy of acknowledgement of ITR of lenders;

iv. Audited financial statement of lenders;

v. Copy of Memorandum of Associate and certification of incorporation of lenders;

vi. Copy of Board resolution and copy of foreclosure of leans issued by the lenders.

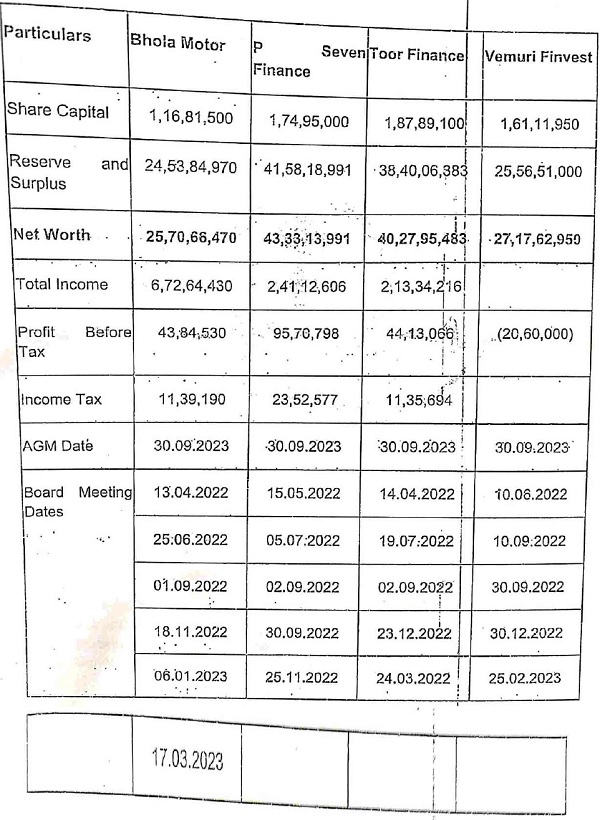

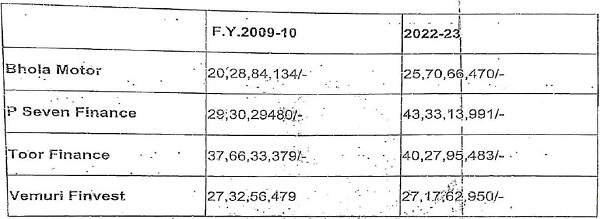

10. It is further observed that all these details were sent to the AO for his comments on merits however, the AO in the Remand Report, has not doubted the same and had not made adverse comments. It is further observed that all the transactions were carried out through banking channel and all the loans taken were paid during the month of October, 2010 as tabulated by Ld.CIT(A) in its order at page 29 & 30. Ld. CIT(A) while deleting the addition at page 27 to 37, has discussed about the merits of the documents filed by the assessee and further at page 35 of the order, has discussed the net worth of the lender companies according to which all the lenders have net worth of more than INR 25 crores. This net worth was of financial year 2023-24 however, at page 36 of the order of Ld.CIT(A) has further tabulated the net worth comparison of the lender companies in FYs 2009-10 & 2022-23 as per which all the four lender companies are having sufficient net worth even in FY 2009-10. Considering these facts, Ld. CIT(A) has deleted the additions made by the AO.

11. The relevant findings of Ld.CIT(A) as contained at page 27 to 37 of ld. CIT(A) are reproduced as under:-

FINDINGS:

1. “The appellant had moved an application under Rule 46A for admission of additional evidence before the CIT(Appeal)-III on the grounds they it was not given any sufficient opportunity during the assessment proceedings to prove the identity, creditworthiness and genuineness of the transaction from the four lenders.

i. The CIT (Appeal) had forwarded the appellant’s application along with documents to the AO for his comments both on merits as well as on law, vide his office letter No. CIT(A)-III/ 2013-14/517 Dated 17.02.2014.

ii. The AO had submitted a remand report dated 15.04.2014 in which the AO has simply stated that since sufficient opportunity was given to the appellant during the assessment proceedings, therefore the additional evidence should submitted should not be entertained and no report was given on merits.

iii. The CIT (Appeal) in this regard in his order had held that the evidence submitted by the appellant went to the root of the issue and the documents were of such nature which per se was not in the nature of additional document but in nature of supporting documents to decide the issue in the appellant’s hand. After considering the fact that only one questionnaire dated 08.11.2012 had been issued by the AO and thereafter no query had been raised in the assessment proceedings with regard to the above issue, the CIT (Appeal) had held that the appellant’s case even otherwise also fell within the category of circumstances mentioned in Rule 46A (i)(d) and therefore the documents by the appellant were accepted and taken on record.

iv) From the above it is clear that the CIT (Appeal) had duly forwarded the Additional evidences filed under Rule 46A by the appellant to the AO to provide his comment both on:

1. Facts &

2. On Merits

The CIT (Appeal) in his order has stated that assessing Officer had offered no comments on merits of the Additional evidences filed by the appellant, other than that they must not be admitted on the grounds that sufficient opportunity had been provided to the appellant. The CIT (Appeal) had duly considered this argument in his order and had given a finding that only one questionnaire dated 8.11.2012 had been issued to the appellant and therefore the case even otherwise fell within the category of circumstances mentioned in Rule 46A(i)(d).

Thus, from the facts of the case, it is seen that the additional evidences had been duly provided to the Assessing Officer to give his comments both on facts and merits under Rule 46A, but the Assessing Officer has not provided any comments on merits to rebut the additional evidence produced by the appellant or had contravened it in any other way. Therefore, there is no adverse comment by the AO against the additional evidence filed by the appellant, despite the fact that he was given due opportunity to examine the same as per the provisions of Rule 46A and provide comments on the facts and merits of the submission.

Therefore, in view of the above mentioned facts, the Additional evidences filed by the appellant are accepted under Rule 46A.

2. From the perusal of the record, it is seen that the entire loan from the four lender companies were taken in September, 2010 and repaid in October, 2010 through banking channels. The confirmations in this regard are placed on record.

The details of the loan taken and returned back by the appellant are as below:

i. From the assessment order, it is seen that the search and seizure operation in the case of M/s. Paramount had been carried out on 11/03/2011. Subsequently, the assessment order for the A.Y. 2011-12, which pertains to the year of the search, was passed on 28/03/2013 u/s. 153A r.w.s 143(3).

ii. Further from the facts as discussed above, it is seen that both the acceptance and return of loan had taken place much before the search was conducted on the appellant company or before the issue of any notice u/s. 153A or 143(2).

iii) The appellant has relied upon the following decision in this regard:

– PCIT vs. Ojas Tarmake (P.)Ltd., (2023)1556 taxman.com 75, High Court of Gujarat.

– PCIT vs.Neotech Education Foundation, (2023) 292 taxman 199, High Court of Gujarat.

– PCIT vs. Ambe Tradecorp (P.) Ltd., (2023) 290 taxman 471, High Court of Gujarat.

– PCIT vs. Overtop Marketing (P.) Ltd., (2023) 148 taxmann.com 94, High Court of Culcutta.

– Pr. CIT vs. Hi-Tech Residency (P.) Ltd., (2018) 257 taxman 335 (SC).

– Pr. CIT vs. Hi-Tech Residency (P.) Ltd., (2018) 257 taxman 390 (Del).

– CIT vs. Real Time Marketing Pvt. Ltd., (2008) 306 ITR 0035 (Del).

– CIT vs. Jai Kumar Bakliwal, (2014) 366 ITR 0217 (Raj).

– Aravali Trading Co. vs. ITO, (2010) 187 Taxman 0338 (Raj). – CIT vs.Metachem Industries, 245 ITR 160, High Court of Madhya Pradesh.

– Nemi Chand Kothari vs. CIT &Anr., (2003) 264 ITR 0254 (Gau).

– CIT vs. Shri Ram Narain Goel, (1997) 224 ITR 0180 (P &H).

In the case of PCIT vs. Ojas Tarmake (P.) Ltd., (2023) 1556 taxman.com 75, High Court of Gujarat, the Hon’ble High Court has held that

“Section 68 of the Income-tax Act, 1961-Cash credit (Unsecured loan)-Assessment Year 2013-14- During the assessment proceedings it was noted that assessee had shown particulars of unsecured loan received during the relevant assessment year Assessing Officer issued letter under section 133(6) in creditors of unsecured loans Thereafter, Assessing Officer made addition with respect to unsecured loan on ground that assessee failed to discharge onus of liability as laid down under section 68-On appeal, Commissioner (Appeals) held additions on ground that assessee failed to produce any of creditors before Assessing Officer-Whether since Tribunal found on facts that amount of loan received by assessee was returned to loan party during the year itself and all transactions were carried out through banking channels, no error of law committed by Tribunal by deleting addition made under section 68- Held, yes [Paras 3 and 4] [In favour of assessee]”

In the case of PCIT vs. Neotech Education Foundation, (2023)292 taxman 199, High Court of Gujarat, the Hon’ble High Court has held that

“Section 68 of the Income-tax Act, 1961-Cash credit (Unsecured loan)-Assessment Year 2014-15-Assessee-company was running on educational institution-During year; a survey operation was carried out at premises of one NEF during which certain incriminating materials were found reflecting that assessee had received loan amount for purchase of land for construction of an educational campus-Assessing Officer made addition under section 68 on account of said loan amount treating it as unexplained-It was noted that Commissioner (Appeals) had observed that assessee had discharged its onus by furnishing necessary details such as a copy of PAN, bank details and ITR etc. in support of identity and creditworthiness of creditors and genuineness of transaction-He further noted that payment of loan to assessee as well as repayment of loan and interest by assessee were made by account payee cheques-Further, both lower authorities had concurrently held that initial burden of proof even if not discharged by assessee at level of Assessing Officer but every transaction was explained by production of documents by assessee before Commissioner (Appeals) where now remand report were called for- Where; on facts, impugned addition on account of loan amount made by Assessing Officer was to be deleted-Held, yes [Paras 9 to 11] [In favour of assessee]”

In view of the discussions in the above Paras, facts and evidences on record and the case laws as cited above, it is apparent that the receipt and repayment of the loan had taken place through banking channels and also before the issue of any notice or the search on the appellant. The loan appears as a regular loan transaction and does not appear as some questionable arrangement, being very transient, having being taken & returned in less than a month on its own.

3. The appellant has submitted that the correspondence could be served upon through Postal authorities (India Post) on the lender companies at the addresses as derived from the Master data of these companies available on MCA portal.

The submissions made by the appellant are relevant to the present date and the present addresses of the four lender companies. However, they present irrefutable evidence towards the facts that these companies are not non-existent. They are active and operational even on date. The fact that the correspondences have been through the Postal Authorities (India Post) further, lends credence to the contention of the appellant that these companies exist even on date, and these companies are at the same time making compliances to the required statutory regulations. These submissions considered with the other facts and evidences placed on record and as have been discussed in prior paras, by the appellant provide supporting evidence towards the facts that the correspondences through postal authorities could be served on the appellant even on date, and therefore, these companies are active and existent.

4. The lender companies are Non Banking Finance Companies (NBFC).They are having PAN, Bank accounts, filing Returns to RoC, filing their tax returns, filing their Audited accounts, paying taxes, holding annual general meetings and Board of Directed meetings as has been discussed in prior Paras.

Further, the appellant had submitted before the CIT(A)-III, New Delhi, its detailed submissions in this regard at para 4.4, 4.5, 4.6, 4.7 & 4.8, which have also been discussed in detail in prior paras.

The appellant has further also submitted that the master data of these companies had been extracted from the portal of the Ministry of Corporate Affairs and correspondences through the postal authorities(India Post) could be made even in the current year at the registered addresses as provided in the portal of MCA.

Therefore, from the above submissions of the appellant and after considering all the facts and evidences on record, I find that the appellant has discharged its onus regarding the Identity of the four lenders i.e., M/s Bhola Motor Finance Pvt. Ltd., M/s P Seven General Finance (P.) Ltd.,M/s Toor Finance Company Ltd. & Vemuri Finvest Pvt. Ltd.

4.1 The appellant had taken loans from the above four mentioned lender companies. The loans were taken through banking channels and returned back through the banking channels. The appellant had submitted the relevant documents in this regard. The same were the:

a) Copy of PAN of the lender

b. Copy of confirmation from the lender

c. Copy of acknowledgement of the ITR of the lender

d. Copy of audited statement of the lender

e. Copy of MOA & incorporation certificate of the lender

f. The copy of loan sanction letter from the lender

g. Copy of Board resolution of the lender

h. Copy of foreclosure letter from the lender

Besides this, the appellant has given the copy of his bank statements where the receipt and return of the loan is clear. It is seen from the same that the loans from all the four lenders have been taken in September, 2010 and returned back in October, 2010. The details of these have been discussed in prior paras.

Therefore, from the above submissions of the appellant and after considering the facts and evidences on record, I find that the appellant has discharged its onus regarding the genuineness of the transactions made by the appellant with the four lenders i.e., M/s Bhola Motor Finance Pvt. Ltd., M/s P Seven General Finance (P.) Ltd.,M/s Toor Finance Company Ltd. & Vemuri Finvest Pvt. Ltd.

4.2 The Assessing Officer in his assessment order has raised no questions on the creditworthiness of the lenders. However, the appellant in his submissions made before the CIT (Appeal)-III, New Delhi had furnished the details regarding the creditworthiness of the lenders.

These details submitted for the F.Y. 2009-10 were as below:

– The copy of audited financial statements of the M/s Bhola Motors where the net worth has been shown at Rs. 20 Crores.

– The copy of audited financial statements of the M/s P Seven General Finance (P.) Ltd where the net worth has been shown at over Rs. 29 Crores.

– The copy of audited financial statements of the M/s Toor Finance Company Ltd. where the net worth has been shown at Rs. 37 Crores.

– The copy of audited financial statements of the Vemuri Finvest Pvt. Ltd. where the net worth has been shown at Rs. 27 Crores.

Further, as supporting evidence the appellant has submitted the audited accounts of the lenders, even for the FY 2022-23 to establish that the lenders were genuine parties, who continued to operate and remain in business even till date and still remained their creditworthiness.

The details of the lenders submitted by the appellant for the F.Y. 2022-23 is as below:

Thus the appellant has submitted that these four lender companies have continued to file their returns, meet statutory compliances and even on date have the creditworthiness.

The net worth of the companies for the F.Y. 2009-10 and 2022-23 can be briefly summarized as below:

Thus, what is evident is that the company had enough net worth to advance loans to the appellant company in the F.Y. 2010-11. The loans taken in September, 2010 had already been returned back in October, 2010. The fact that the lender companies, which are NBFCs, continue to have their net worth in the F.Y. 2022-23, and remain active and operational, lends credence to the fact that the lender companies did have creditworthiness to make loans to appellant company. It is pertinent to point out that the same had never even been questioned by the Assessing Officer in his assessment order for the relevant A.Y. 2011-12.

Therefore, from the above submissions of the appellant and after considering the facts and evidences on record, I find that appellant has discharged its onus regarding the creditworthiness of the four lenders i.e., M/s Bhola Motor Finance Pvt. Ltd., M/s P Seven General Finance (P.) Ltd.,M/s Toor Finance Company Ltd. & Vemuri Finvest Pvt. Ltd.

5. To conclude, it is clear from the facts and after considering all the evidences that have been submitted, that the appellant has been able to discharge the burden regarding the Identity, Genuineness & Creditworthiness of the lender parties as required u/s 68 of the I.T.Act, and therefore no addition in this regard is warranted. Hence, in my considered opinion and after taking into account all the facts and evidences as discussed above, the appeal of the appellant is allowed and the addition made of Rs. 6,25,00,000/-made u/s 68 of the I.T. Act, 1961 is deleted.

12. Before us, the Revenue has failed to controvert the findings given by Ld.CIT(A) which are made after appreciating the facts and details filed by the assessee and further by considering the facts that the lender companies are NBFCs and loans taken by the assessee were repaid within a short period of time of one month which fact has not been doubted by the Revenue. Further the Hon’ble Gujarat high court in the case of PCIT vs. Ojas Tarmake (P.) Ltd. (supra) has held as under :

“Section 68 of the Income-tax Act, 1961-Cash credit (Unsecured loan)-Assessment Year 2013-14- During the assessment proceedings it was noted that assessee had shown particulars of unsecured loan received during the relevant assessment year Assessing Officer issued letter under section 133(6) in creditors of unsecured loans Thereafter, Assessing Officer made addition with respect to unsecured loan on ground that assessee failed to discharge onus of liability as laid down under section 68-On appeal, Commissioner (Appeals) held additions on ground that assessee failed to produce any of creditors before Assessing Officer-Whether since Tribunal found on facts that amount of loan received by assessee was returned to loan party during the year itself and all transactions were carried out through banking channels, no error of law committed by Tribunal by deleting addition made under section 68- Held, yes [Paras 3 and 4] [In favour of assessee]”

13. It is further observed that all the Four lender companies are having sufficient net worth of more than INR 20 crores in FY 200910 to grant the loan to the assessee to the extent of INR 6.25 crores in toto.

14. In view of these facts and overall discussion made herein above and by respectfully following the judgements of various Hon’ble High Courts as relied upon the ld. CIT(A), we find no infirmity in the order of Ld.CIT(A) which is hereby, upheld. All the grounds of appeal of the Revenue are thus, dismissed.

15. In the result, appeal filed by the Revenue is dismissed.

Order pronounced in the open Court on 17.04.2026.

Author Bio