Case Law Details

Star Tradecom Private Limited Vs ITO (ITAT Kolkata)

The appeal before the ITAT Kolkata arose from an order of the National Faceless Appeal Centre for Assessment Year 2009-10. During the appellate proceedings, the assessee raised an additional legal ground challenging the validity of the reassessment proceedings. The assessee contended that the reassessment initiated through a notice under Section 148 and completed under Sections 147/143(3) was invalid because no statutory notice under Section 143(2) had been issued or served. It further argued that since the reassessment order itself was non est, the subsequent revisionary proceedings under Section 263 based on that assessment were also liable to be quashed.

The Tribunal admitted the additional ground, observing that it involved a pure question of law and that all relevant facts were already available on record, making further factual verification unnecessary. It held that a legal issue may be raised before an appellate authority for the first time even if it was not urged before the lower authorities. In support of this conclusion, the Tribunal referred to the decisions in Jute Corporation of India Ltd., National Thermal Power Co. Ltd., and Britannia Industries Ltd..

The assessee had originally filed its return of income, which was processed under Section 143(1). Subsequently, the Assessing Officer reopened the assessment under Section 147 by issuing a notice under Section 148 on the ground that income relating to miscellaneous expenses had escaped assessment. A reassessment order under Sections 147/143(3) was thereafter passed determining a higher total income.

Later, the Commissioner exercised revisionary jurisdiction under Section 263 after holding that the reassessment order was erroneous and prejudicial to the interests of the Revenue because adequate enquiries had nt been conducted regarding the identity and creditworthiness of shareholders and the genuineness of share capital transactions amounting to ₹5.07 crore. The assessment was set aside with directions to conduct fresh enquiries. In the consequential proceedings, notices issued under Sections 142(1) and 131 remained unserved, and the Assessing Officer ultimately treated the share application money as unexplained cash credit under Section 68.

The Tribunal observed that throughout the original reassessment proceedings, the assessee had consistently requested the Assessing Officer to furnish the notice issued under Section 143(2), asserting that it had never been served. According to the assessee, no such notice had ever been issued. The Tribunal also noted that the assessee had sought information through an RTI application and that the Assessing Officer replied that the records relating to issuance of the notice under Section 143(2) were not available. On these facts, the Tribunal concluded that the reassessment had been completed without issuance of the mandatory notice under Section 143(2).

The Tribunal relied extensively on the judgment of the Calcutta High Court in Principal Commissioner of Income-tax v. Oberoi Hotels (P.) Ltd., which applied the Supreme Court’s ruling in ACIT v. Hotel Blue Moon. The High Court held that issuance of notice under Section 143(2) is mandatory whenever the Assessing Officer seeks to make an assessment different from the return filed, including in reassessment proceedings. It further held that failure to issue such notice results in the reassessment proceedings being quashed and that Section 292BB only cures defects in service of notice and does not dispense with the mandatory requirement of issuing the notice itself.

Applying these principles, the Tribunal held that the reassessment framed under Sections 147/143(3) without issuance of notice under Section 143(2) was bad in law and a nullity. Since the reassessment order itself was invalid, the Principal Commissioner could not validly invoke revisionary jurisdiction under Section 263 on the basis of such an assessment. Accordingly, the Tribunal allowed the additional ground raised by the assessee and held that the revisionary proceedings were unsustainable.

FULL TEXT OF THE ORDER OF ITAT KOLKATA

This is an appeal preferred by the assessee against the order of the National Faceless Appeal Centre, Delhi (hereinafter referred to as the “Ld. CIT(A)”] dated 23.12.2022 for the AY 2009-10.

2. The assessee has raised additional ground, which is extracted as under:-

“3. For that the reopening proceedings carried out vide issuance of notice under section 148 of the I. T Act on 16.12.2010 and thereafter proceedings completed on17.03.2011, are bad-in-law and non-est based on decision in ACIT vs. Hotel Blue Moon, (2010) 321 ITR 362 (SC) since statutory notice under section 143(2) of the I.T Act was not issued and served to the Appellant company and, therefore, since the subject matter of the revisionary proceedings i.e. assessment order dated 17.03.2011 is nullity, bad-in-law and non-est, therefore, revisionary proceedings under section 263 cannot be carried out on the basis of such non-est assessment and the same deserves to be quashed”

3. After hearing the rival contentions and perusing the material on record, we find that the assessee has raised the above additional ground of appeal challenging the jurisdiction of the AO to make addition. In our opinion the issued raised in the additional ground is a purely a legal issue qua which all the facts are available in the appeal folder and no further verification of facts are required from any quarter whatsoever. In our considered view the assessee is at liberty to raise any legal issue before any appellate authority for the first time even when the same has not been raised before the lower authorities. The case of the assessee is squarely coverd by the decisions of the Apex court in the case of i) Jute Corporation of India Ltd. Vs CIT in 187 ITR 688 , ii) National Thermal Power Co. Ltd v. CIT [1998] 229 ITR 383 and also by the decision of Hon’ble Calcutta High Court in PCIT vs. Britannia Industries Ltd. [2017] 396 ITR 677 (Cal). Therefore, we are inclined to admit the same for adjudication.

4. The facts in brief are that the assessee filed the return of income on 11.07.2009, declaring total income at 1714/-, which was duly processed u/s 143(1) of the Income-Tax Act, 1961 (hereinafter referred to as “the Act”). Subsequently, the case of the assessee was reopened u/s 147 of the Act by issuing notice u/s 148 of the Act on 16.12.2010, on the basis of information that income under the head miscellaneous expenses to the tune of 126,870/- had escaped assessment within the meaning of Section 147 of the Act. Accordingly, the assessment u/s 147/ 143(3) of the Act was framed vide order dated 17.03.2011, determining the total income at 150,480/-.

5. Thereafter, on examination of the assessment record, the Commissioner of Income Tax KOL-III, Kolkata held that assessment order was erroneous in so far as prejudicial to the interest of the Revenue on the ground that requisite enquiries were not done regarding the identity and creditworthiness of the shareholders and genuineness of the transactions through which the introduction of share capital to the tune of 5,07,00,000/- was made during the financial year. Accordingly, the show cause notice u/s 263 of the Act was issued to the assessee to explain as to why the assessment should not be set aside. Ultimately the order u/s 263 of the act was passed on 05.03.2013, setting aside the assessment with a direction to re-frame the assessment after conducting through enquires. Thereafter, notice u/s 142(1) of the Act was issued on 10.02.2014, by the Id. AO fixing the case on 20.02.2014, calling for various details of the shareholders but the same was unserved. Further summons were issued u/s 131 of the Act by Speed Post to the directors of the assessee company fixing the hearing on 12.03.2014, and the same were also unserved. Finally, share application money raised by the assessee was added as unexplained money u/s 68 of the Act to the income of the assessee. Now the assessee has taken up the additional ground which has been admitted by us hereinabove.

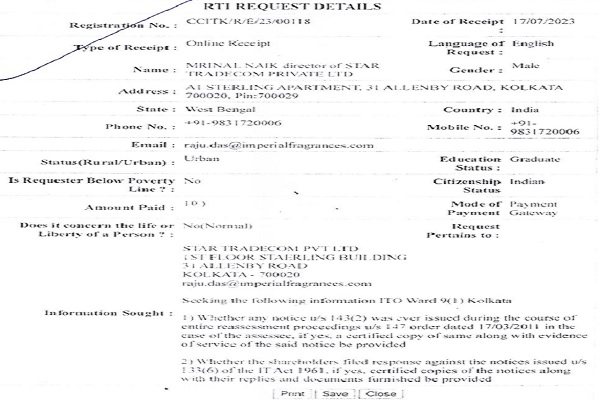

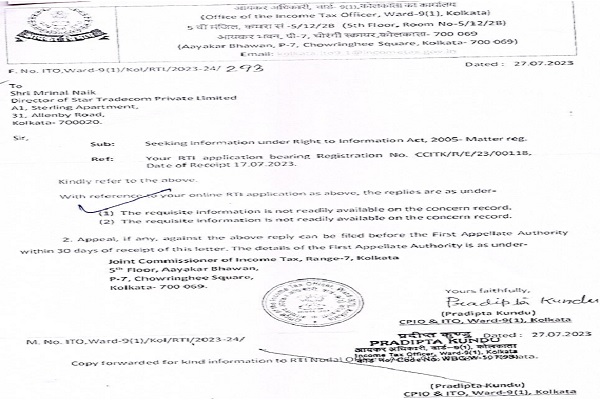

6. After hearing the rival contentions and perusing the materials available on record, we find that the assessee has been requesting the AO throughout the original assessment proceedings, which culminated in passing the order u/s 147/ 143(3) of the Act dated 17.03.2011, to supply the notice u/s 143(2) of the Act as the same was not served on the assessee. But the same was never supplied to the assessee. accordingly to the assessee the notice u/s 143(2) was never issued. Therefore , the assessment framed by the AO sans notice u/s 143(2) of the Act is bad in law and nullity. The assessee has obtained information from the AO by filing RTI application and the Id. AO replied that the requisite information / details qua issuance of notice u/s 143(2) of the Act were not available in the records. We note that the assessee has asked for the notice issued u/s 143(2) of the Act and also responses against the notice u/s 133(6) of the Act in the RTI application. For the sake of ready refence, the RTI application and reply of the Id. AO are extracted below:-

—

—

7. Therefore, in our opinion the assessment framed by the Id. AO u/s 147/ 143(3) of the Act on 17.03.2021, is bad in law and nullity. The case of the assessee find support from the decisions of Hon’ble High Court in case of Principal Commissioner of Income-tax vs. Oberoi Hotels (P.) Ltd. [2018] 96 taxmann.com 104 (Calcutta)/[2018] 409 ITR 132 (Calcutta)[22-06-2018], wherein it has held as under:-

“1. The Court – The substantial questions of law that have arisen are in the context of reassessment proceedings initiated under Section 147 of the Income Tax Act, 1961 pursuant to a notice under Section 148 thereof.

2. The Appellate Tribunal has quashed the entire reassessment proceedings on the assessee’s assertion that no notice under Section 143(2) of the Act was issued by the Assessing Officer before undertaking the reassessment. The judgment of the Appellate Tribunal is founded primarily on the ratio decidendi in the Supreme Court judgment Asstt. CIT v. Hotel Blue Moon [2010] 188 Taxman 113/321 ITR 362. The Revenue is in appeal and says that in view of Section 292BB of the Act, the ground could not have been urged by the assessee before the Appellate Tribunal, particularly, as the assessee participated in course of the reassessment, the objections of the assessee as to the reassessment were considered by the Assessing Officer and it was not pointed out by the assessee prior to the reassessment being completed that no notice under Section 143(2) of the Act had been issued to him in respect of the reassessment. In the alternative, the Revenue says that if a notice under Section 143(2) is deemed to be mandatory so that in the absence thereof the subsequent order of assessment (or reassessment) has to be annulled, the matter must be restored to the stage where a notice under Section 143(2) of the Act may be issued for completing the assessment or reassessment, as the case may be. In such circumstances, the following substantial questions of law arise:

| “1. | Whether the failure to issue a notice under Section 143(2) of the Act in course of reassessment proceedings would vitiate the reassessment proceedings altogether? |

| 2. | What is the effect in view of Section 292BB of the Act when a notice under Section 143(2) of the Act is not issued at all?” |

3. The Supreme Court judgment in Hotel Blue Moon has first to be referred to since such judgment still holds the field. In course of a block assessment when the Assessing Officer repudiated the return filed by the assessee but failed to issue any notice under Section 143(2) of the Act within the prescribed period of time, the Supreme Court held, at paragraph 15 of the judgment, inter alia, as follows:—

“15. … But section 143(2) itself becomes necessary only where it becomes necessary to check the return, so that where block return conforms to the undisclosed income inferred by the authorities, there is no reason, why the authorities should issue notice under section 143(2). However, if an assessment is to be completed under section 143(3) read with section 158 BC, notice under section 143(2) should be issued within one year from the date of filing of block return. Omission on the part of the assessing authority to issue notice under section 143(2) cannot be a procedural irregularity and the same is not curable and, therefore, the requirement of notice under section 143(2) cannot be dispensed with …”

4. It is evident that the dictum of the Supreme Court in Hotel Blue Moon is that a notice under Section 143(2) is mandatory if the return as filed is not accepted and an assessment order is to be made at variance with the return filed by the assessee. It is also evident that the issue is not limited to block assessment but would apply to every case where a notice under Section 143(2) of the Act is necessary. In the judgment and order of the Appellate Tribunal impugned herein dated May 14, 2015, the Tribunal noticed a judgment of this Court of April, 8, 2014 rendered in ITAT 149 of 2013 (CIT v. Humboldt Wedag India (P.) Ltd.) where this Court had expressed an opinion that when an order of assessment was passed in course of reassessment under Section 143(3) of Act, “The omission could have been a reason for setting aside the order of assessment, but that could not have been a reason, in the facts and circumstances of this case, for nullifying the exercise under section 147 of the Income Tax Act.”

5. Such view taken by this Court in Humboldt Wedag India Pvt. Ltd. was without noticing the Supreme Court judgment in Hotel Blue Moon. The relevant Bench also did not take into consideration a previous order of this Court of April 4, 2013 when the reassessment proceedings were quashed merely on the ground that no notice under Section 143(2) of the Act was issued to the assessee before making the reassessment. It is necessary to see the short order of April, 4, 2013 passed in ITAT 27 of 2013 (CIT v. I. S. Leather):

“Admittedly, no notice under section 143(2) of the I.T. Act was issued to the assessee before making the re-assessment. The learned Tribunal, relying on the judgment in the case of ACIT v. Hotel Bluemoon reported in (2010) 321 ITR 362 (SC) and the judgment in the case of CIT v. C. Palaniyappan, reported in (2006) 284 ITR 257 (Madras), opined that the re-assessment was without jurisdiction and was, therefore, quashed. It is against this order that the revenue has come up. “We find no infirmity in the order under challenge. The appeal is as such dismissed.”

6. The Revenue has sought to rely on a Madras High Court judgment Areva T & D India Ltd. v. Asstt. CIT [2007] 165 Taxman 123/294 ITR 233 where the view taken was that “the non-issuance of a notice under section 143(2) of the Act, will not make the reassessment nullity in law, which is validly initiated under section 148 of the Act”. However, such judgment of the Madras High Court was noticed and discussed in a later judgment of the same Court Sapthagiri Finance & Investments v. ITO [2012] 25 taxmann.com 341/210 Taxman 78 (Mad.) (Mag.). It was held therein that the view taken in Areva T & D India Ltd was no longer good law in view of the Supreme Court judgment in Hotel Blue Moon. The assessee has also relied on another unreported judgment of the Madras High Court of November 19, 2014 in Tax Case (Appeal) 766 of 2014 N. Ahamed Ali v. ITO [2012] 25 taxmann.com341/210 Taxman 78 (Mad.) (Mag.) where it was held that a notice under Section 143(2) of the Act was mandatory and the judgment in Areva T & D India Ltd was not good law.

7. Section 148 of the Act permits the issuance of a notice in certain circumstances when it is discovered that income has escaped assessment and sub-section (1) thereof mandates a return to be filed upon an assessee being served a notice under such provision, whereupon “the provisions of this Act, shall, so far as may be, apply accordingly as if such return were a return required to be furnished under Section 139.”

8. Section 143 of the Act pertains to assessment and in its opening words refers to a return being made under Section 139 of the Act or in response to a notice under Section 142 (1) of the Act. At the time relevant for the assessment that was undertaken by the Assessing Officer after a notice under Section 148 of the Act had been issued, Section 143(2) in its then form had two clauses and a proviso after Clause (ii) that precluded a notice under Clause (ii) being served beyond a particular period. Further, Section 153 (2) of the Act directs an order of assessment, reassessment or recomputation to be made under Section 147 of the Act within a particular period. The relevant periods, both in terms of the proviso to Section 143(2) of the Act and in terms of Section 153 thereof, have expired. As noticed by the Supreme Court in Hotel Blue Moon (supra) and is quoted above, the time is of some significance and notices can no longer be issued after the expiry of the period mandated therefor nor can proceedings be continued after the time limit set therefor by the statute.

9. In the light of the above discussion, particularly taking into consideration the law laid down by the Supreme Court in Hotel Blue Moon (supra), it is inescapable that the issuance of a notice under Section 143(2) of the Act is mandatory if the Assessing Officer seeks not to accept any part of the return as furnished by the assessee or make an assessment order contrary thereto and, even in course of reassessment proceedings, such notice cannot be dispensed with.

10. One of the arguments put forth on behalf of the Revenue is that in course of reassessment proceedings once a notice is issued under Section 148 of the Act, the assessee is made aware of what part of the income or on what count the assessee’s income is perceived to have escaped attention. It is submitted that in such a scenario, the requirement of a notice under Section 143(2) may be somewhat diluted, if not unnecessary. Apart from the fact that such argument cannot be countenanced in the light of the dictum in Hotel Blue Moon (supra), it is evident that an assessment under Section 143(3) of the Act is consequent upon a hearing and the production of evidence on such points on which the Assessing Officer may harbour doubts and are indicated in his notice under Section 143(2) of the Act. Section 143(3) of the Act contemplates an assessment undertaken by the Assessing Officer upon material being produced by the assessee on grounds which are indicated by the Assessing Officer in his notice under Section 143(2) of the Act in respect whereof the Assessing Officer may have misgivings or may disagree with the return filed by the assessee. Implicit in the wording of Section 143(3) of the Act is the indispensability of a notice under Section 143(2) thereof.

11. Apropos the second question framed above, it is necessary that Section 292BB of the Act be noticed in its entirety:

“292BB Notice deemed to be valid in certain circumstances –

Where an assessee has appeared in any proceeding or cooperated in any inquiry relating to an assessment or reassessment, it shall be deemed that any notice under any provision of this Act, which is required to be served upon him, has been duly served upon him in time in accordance with the provisions of this Act and such assessee shall be precluded from taking any objection in any proceeding or inquiry under this Act that the notice was-

a. not served upon him; or

b. not served upon him in time; or

c. served upon him in an improper manner:

Provided that nothing contained in this section shall apply where the assessee had raised such objection before the completion of such assessment or reassessment.”

12. Even if the provision does not carry a non-obstante clause, since Section 292BB is a provision of general application, it would be applicable in all situations; but only in so far as it proclaims to operate. Section 292BB of the Act, read in the context of several provisions of the Act which mandatorily require notices to be issued in divers situations, cannot be said to have dispensed with the issuance of such notices altogether. Section 292BB must be understood to cure any defect in the service of the notice and not authorise the dispensation of a notice when the appropriate interpretation of a provision makes the notice provided for thereunder to be mandatory or indispensable.

13. This is not a case where the assessing officer says that a notice had been issued and there is a contradiction thereof by the assessee. It is evident that the assessee carried the objection before the Commissioner (Appeals) and the Commissioner brushed aside the objection on the ground that it was a technicality without addressing the issue or applying his mind to such aspect of the matter. Further, it is evident from the order impugned passed by the Appellate Tribunal that no notice under Section 143(2) of the Act had, in fact, been issued in this case. In such a situation, where a notice that is mandatorily required to be issued is found not to have been issued, Section 292BB of the Act has no manner of operation.

The two substantial questions of law are answered accordingly as follows:

1. If the time for issuance of the notice under Section 143(2) of the Act has expired or the time for completing the reassessment proceedings under Section 153(2) of the Act has run out, the failure to issue such notice under Section 143(2) of the Act would result in the entire proceedings, including any order of assessment, to be quashed.

2. Section 292BB of the Act does not dispense with the issuance of any notice that is mandated to be issued under the Act, but merely cures the defect of service of such notice if an objection in such regard is not taken before the completion of the assessment or reassessment.

In addition, it is held that in the light of the Supreme Court dictum in Hotel Blue Moon (supra), the view expressed in Humboldt Wedag India (P.) Ltd. (supra) is per incuriam and, as such, not good law.

ITAT 152 of 2015 and GA 3671 of 2015 are disposed of.

There will be no order as to costs.”

8. Therefore, we find merit in the contention of the assessee that the revisionary jurisdiction cannot be invoked u/s 263 of the Act by the PCIT on an invalid assessment order as stated above. Consequently, the additional raised by the assessee is allowed.

9. So far as raising the issue in collateral proceedings is concerned, we are of the view that the issue of invalidity can be raised in the collateral proceedings by the assessee even though the order concerned passed by the authorities have not been challenged before the appellate authority. The case of the assessee find support from the following decisions. In defense of his arguments, the Id. AR stated that the consequential proceedings would be invalid and the assessee can challenge the validity of the assessment framed in the co- lateral/consequential proceedings. The case of the assessee is squarely covered by the decisions of Hon’ble Calcutta High Court in case of Keshab Narayan Banerjee Vs. CIT [1999] 238 ITR 694 (Calcutta)/[1999] 156 CTR 109 (Calcutta) and M/s Classic Flour & Food Processing Pvt. Ltd. Vs. CIT, Kolkata in ITA no. 764 to 766/KOL/2024 vide order dated 05.04.2017, Concord Infra Projects Pvt. Ld. Vs. PCIT in ITA No. 174/KOL/2021 vide order dated 13.10.2024. In all the above decisions it has been held that the assessee is within its legitimate and lawful right to challenge the assessment framed u/s 147 of the Act even in the collateral proceeding as has been held in the aforesaid decisions.

10. In the result, the appeal of the assessee is allowed.

Order pronounced on 16.06.2026.

Author Bio