Case Law Details

Lekh Raj Vs DCIT (ITAT Delhi)

The Income Tax Appellate Tribunal (ITAT), Delhi allowed six appeals filed by the assessee for Assessment Years (AYs) 2013-14 to 2017-18 and 2019-20 against the orders of the Commissioner of Income Tax (Appeals) dated 12.03.2025. Since all the appeals arose from the same search proceedings, the Tribunal heard them together and treated AY 2013-14 as the lead case.

The appeals challenged, among other issues, the assumption of jurisdiction under Section 153C, the validity of the assessments framed under Section 153C read with Section 143(3), and the protective addition of ₹44,89,000 under Section 68. The assessee also contended that the additions were made without incriminating material, without granting an opportunity for cross-examination, and in violation of the principles of natural justice.

The Tribunal noted that a search and seizure operation under Section 132 was conducted in the case of Navin Mahipal Group on 16.09.2019, during which certain documents relating to the assessee were found and seized. Consequently, proceedings under Section 153C were initiated for AYs 2010-11 to 2019-20, and a notice dated 30.09.2021 was issued. The Tribunal observed that, apart from registered sale deeds, no other documents relating to the assessee were seized. A consolidated satisfaction note for all assessment years was recorded by the Assessing Officer on 28.09.2021. Thereafter, the Assessing Officer passed an order under Section 153C read with Section 143(3) on 30.03.2023, making a protective addition of ₹44,89,000 under Section 68 in respect of amounts credited to the assessee’s bank account. The CIT(A), in ex parte proceedings, dismissed the appeals in their entirety.

Before the Tribunal, the assessee argued that AY 2013-14 was an unabated assessment year and that no incriminating material had been found during the search to justify an assessment under Section 153C. It was submitted that the registered sale deeds seized during the search merely evidenced legally executed transactions and could not be regarded as incriminating material. Reliance was placed on the Supreme Court’s decision in Abhisar Buildwell, wherein it was held that no addition can be made under Section 153C in respect of completed or unabated assessments in the absence of incriminating material.

The assessee further contended that the satisfaction note was recorded only on 28.09.2021, after the amendments introduced by the Finance Act, 2021. It was argued that where the satisfaction note is recorded after 01.04.2021, assessments in the case of a non-searched person cannot be framed under Section 153C, and proceedings, if any, must instead be taken under Sections 147 and 148. Reliance was placed on the Delhi High Court’s decision in PCIT v. Ojjus Medicare (P.) Ltd. and the Tribunal’s decision in Geetanjali Bhayana v. DCIT.

The Department supported the orders of the lower authorities and sought dismissal of the appeals.

After considering the rival submissions, the Tribunal observed that the satisfaction note in the assessee’s case was admittedly recorded on 28.09.2021. It referred to the first proviso to Section 153C(1), under which, for a person other than the searched person, the relevant date is the date on which the seized material is received by the Assessing Officer having jurisdiction over such other person. The Tribunal noted that the CIT(A) had presumed 21.01.2021, the date of transfer of jurisdiction under Section 127, as the date on which the seized material was handed over. However, the Tribunal held that there was no material on record to support such an assumption. Relying on the Delhi High Court’s judgment in Ojjus Medicare (P.) Ltd., it held that where the actual date of handing over the seized material is not available, the date of recording the satisfaction note becomes the relevant date. Accordingly, 28.09.2021 was treated as the date on which the seized material was received by the Assessing Officer.

The Tribunal then examined the amendment to Section 153C introduced by the Finance Act, 2021, which inserted sub-section (3) with effect from 01.04.2021. It noted that, in view of the amendment, Section 153C would not apply in relation to searches or requisitions covered by the amended provision, and therefore notices issued under Section 153C after 01.04.2021 in the case of a non-searched person were unsustainable. Applying the amended provision and the law laid down by the Delhi High Court in Ojjus Medicare (P.) Ltd., the Tribunal held that the notice issued under Section 153C and the assessment order passed under Section 153C were without jurisdiction and liable to be quashed.

With regard to the remaining five assessment years (AYs 2014-15 to 2017-18 and 2019-20), both parties agreed that the facts were identical to those in AY 2013-14. The Tribunal held that the common satisfaction note dated 28.09.2021 applied equally to all these years. Following its findings for AY 2013-14, the Tribunal quashed the assessment orders for all the remaining assessment years as well. Accordingly, all six appeals were allowed.

FULL TEXT OF THE ORDER OF ITAT DELHI

1. These six appeals by the assessee are directed against the orders of the Commissioner Income Tax (Appeals) for the Assessment Years 2013-14 to 2017-18 & 2019-20, respectively. The impugned orders for the respective assessment years are of even date i.e. 12.03.2025. Since, the facts germane to the issues stem from the same search, these appeals are taken up together for adjudication and are decided by this common order.

2. For the sake of convenience, appeal of the assessee in ITA No. 3181/Del/2025 for A.Y. 2013-14, is taken up as lead case, hence the facts are narrated from the said appeal.

ITA No. 3181/Del/2025; A.Y. 2013-14

3. The assessee in the appeal has raised following grounds of appeals:

“1. That the Appellant denies his liability to be assessed at total income of Rs. 46,57,000/- as against the returned income of Rs. 1,68,000/- and accordingly denies his liability to pay tax, interest demanded thereon.

3. That having regard to the facts and circumstances of the case, the Ld. Commissioner of Income Tax (Appeals) [‘Ld. CIT(A)’] has erred in law and on facts in confirming the action of the Ld. Assessing Officer [‘Ld. AO’] in assuming jurisdiction u/s 153C of the Income Tax Act, 1961, for framing the assessment for the impugned assessment year, without satisfying the mandatory jurisdictional conditions prescribed under the said provision, rendering the entire assessment bad in law and liable to be quashed.

3. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law and on facts in confirming the action of Ld. AO in framing the impugned assessment order u/s 153C r.w.s. 143(3) is bad in law and against the facts and circumstances of the case.

4. That having regard to the facts and circumstances of the case, the Ld. CIT(A) has erred in law and on facts in confirming the action of the Ld. AO in making a protective addition of Rs. 44,89,000/- under section 68 of the Act, in respect of the amount credited in the bank accounts of the assessee, as per para 5.5 of the order, without bringing on record any incriminating material and without appreciating the submissions and evidences placed on record.

5. That having regard to the fact and circumstances of the case, the Ld. CIT(A) has further erred in law and on facts in confirming the said additions by recording incorrect facts and findings, without providing the opportunity of cross-examination, and without observing the principle of natural justice, thereby rendering the addition bad in law and liable to be deleted.

6. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law and on facts in not reversing the action of Ld. AO in charging interest under sections 234A, 234B, 234C and 234D of Income Tax Act, 1961.

7. That the Appellant craves the leave to add, modify, amend or delete any of the grounds of appeal at the time of hearing and all the above grounds are without prejudice to each other.”

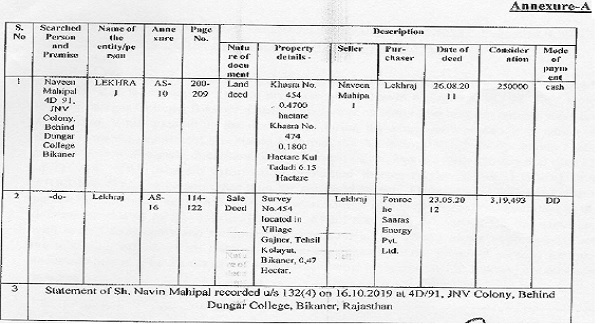

4. Facts of the case in brief as emanating from the records are: A search and seizure operation u/s 132 of the Income Tax Act, 1961 [hereinafter referred to as, “the Act”] was carried out in the case of Navin Mahipal Group on 16.09.2019. During the course of search certain documents pertaining to the assessee were found and seized.

Accordingly, assessment proceedings u/s 153C of the Act for A.Y. 201011 to 2019-20 were initiated in the case of the assessee. Notice u/s 153C dated 30.09.2021 was issued to the assessee. The seized documents pertaining to assessee were :

Apart from aforementioned sale deeds, no other document was seized during the search pertaining to the assessee. Consolidated satisfaction for A.Y. 2010-11 to 2019-20 for initiating proceedings u/s 153C r.w.s. 143(3) of the Act were recorded by the AO of the assessee on 28.09.2021. The AO vide assessment order dated 30.03.2023 passed u/s 153C r.w.s. 143(3) of the Act made protective addition of RS. 44,89,000/- u/s 68 of the Act in respect of the amount received by the assessee, in his bank account. Aggrieved by the assessment, the assessee filed appeal before the CIT(A) inter-alia assailing validity of assessment proceedings as well as, addition on merits. The First Appellate Authority in ex-parte proceedings dismissed appeal of the assessee in toto. Hence, the present appeal.

5. Ms. Monika Ghai, Advocate, appearing on behalf of the assessee submits that the assessment in the case of assessee is liable to be quashed as A.Y. 2013-14 is a case of unabated assessment and no incriminating material was found during the course of search at the place of searched person pertaining to the assessee. She submitted that the Hon’ble Supreme Court of India in the case of Abhisar Buildwell [2023] 454 ITR 212 (SC) has held that in the case of completed/unabated assessment, in the absence of any incriminating material, the Assessing Officer cannot make addition u/s 153C of the Act. The AO can assume jurisdiction u/s 153C of the Act in the year of unabated assessment only where any incriminating material is seized during search. She asserted that, it is evident from assessment order that addition made by the AO is not based on any incriminating material found during the course of search in the case of Navin Mahipal Group. The only documents that were seized pertaining to the assessee were registered sale deeds of land and that too executed during F.Y. 2011-12 and 2012-13. The said sale deed cannot partake the character of incriminating material as they are evidence of legally executed transaction. Thus, the Ld. Counsel prayed for quashing the assessment and allowing appeal of the assessee.

5.1 Ms. Ghai, further submits that the assessment is also liable to be quashed for the reason that the assessment proceedings were completed u/s 153C of the Act, though the satisfaction note in the case of assessee was recorded only on 28.09.2021. The provisions of section 153C of the Act were amended by the Finance Act, 2021 and, as per the amended provisions, where the satisfaction note is recorded after 01.04.2021, the assessment in the case of non-searched person cannot be made u/s 153C of the Act. After 01.04.2021, the assessment in the case of non-searched person can only be made u/s 148 r.w.s. 147 of the Act. To support her submissions, she placed reliance on the decision rendered in the case of PCIT Vs. Ojjus Medicare(P.) Ltd. [2024] 465 ITR 101 (Delhi) and the decision of Tribunal in the case of Geetanjali Bhayana Vs. DCIT 181 Taxmann.com 95 Delhi (Trib.).

6. Per contra, Ms. Richa Gaharwar, CIT(DR), representing the department vehemently defending findings of the CIT(A), prayed for dismissing appeal of the assessee and upholding the impugned order.

7. We have heard submissions made by rival sides and have examined the orders of authorities below. We have also considered the decision on which ld. Counsel for the assessee has vehemently placed reliance to buttress her arguments. The assessee in appeal has assailed validity of the assessment order passed u/s 153C r.w.s. 143(3) of the Act. It is an undisputed fact that addition has been made in the hands of the assessee on protective basis consequent to search in the case of Navin Mahipal Group on 16.09.2019. The satisfaction note in case of the assessee was drawn by the AO on 28.09.2021. As per the first proviso to section 153C(1), the date of search in the case of person other than the searched person shall be the date on which books of account or documents or assets seized or requisitioned by the Assessing Officer having jurisdiction over such other person are received by the AO of other person. Thus, in the case of a person other than the searched person, the relevant date would be the date on which relevant documents or seized material is received by the AO of the person other than the searched person. The CIT(A) in Para 14 of the impugned order has recorded that:

“it does not emanate from record as to when the seized material was handed over to AO, it is seen that the case of the appellant was centralised u/s 127 of the Act from Faridabad to New Delhi on 21.01.2021. Therefore, the date 21.01.2021 may be taken as the date on which the material was handed over to the AO, that is to say, that the material was handed over to the AO in F.Y. 2020-21.”

We are of the considered view that in absence of specific date of handing over the seized material to AO of the assessee, the date of issue of order u/s 127 of the Act has been wrongly assumed by the CIT(A) as the date on which seized material was received by the AO of assessee. The Hon’ble Jurisdictional High Court in the case of PCIT vs. Ojjus Medicare(P.) Ltd (supra) has held that where the date of handing over of documents is not available, date of issuance of satisfaction note by the Assessing Officer u/s 153C of the Act would be pertinent for the purpose of first proviso to section 153C of the Act. In the present case, the AO had recorded satisfaction on 28.09.2021. Since, the date of handing over of seized material is not emanating from the records, the date of recording of satisfaction i.e., 28.09.2021 shall be considered as the date of receiving seized material by the AO of the assessee.

8. Section 153C was amended by the Finance Act, 2021 with effect from 01.04.2021 whereby sub-section(3) was inserted. The relevant subsection is reproduced hereinbelow:

“(3) Nothing contained in this section shall apply in relation to a search initiated under section 132 or books of account, other documents or any assets requisitioned under section 132A on or after the 1st day of April, 2021.”

By virtue of above amendment to section 153C, no assessment u/s 153C can be made in the case of other person under section 153C of the Act if the date of search falls beyond 01.04.2021. As a corollary, any notice issued for making assessment u/s 153C of the Act in the case of a non-searched person after 01.04.2021 would be no-nest.

9. Thus, applying the amended provisions of section 153C of the Act and the law explained by the Hon’ble Jurisdictional High Court in the case of Ojjus Medicare(P.) Ltd. (supra), to facts of the instant case, we find that the notice u/s 153C of the Act issued by the AO to assessee and thereafter, assessment order passed u/s 153C is unsustainable and is liable to be quashed on the ground of jurisdiction. We hold accordingly.

10. In the result, impugned order is set-aside and appeal of the assessee is allowed.

ITA No. 3182/Del/2025 [A.Y. 2014-15],

ITA No. 3183/Del/2025 [A.Y. 2015-16],

ITA No. 3184/Del/2025 [A.Y. 2016-17],

ITA No. 3185/Del/2025 [A.Y. 2017-18],

ITA No. 3186/Del/2025 [A.Y. 2019-20].

11. Both sides are unanimous in stating that the facts in these five appeals are identical to ITA No. 3181/Del/2025 [A.Y. 2013-14]. Therefore, submissions made for A.Y. 2013-14, would equally hold good for the remaining five assessment years.

12. We find that in all these five Assessment Years i.e., A.Y. 2014-15 to 2017-18 & 2019-20, the assessments have been made u/s 153C of the Act, whereas common satisfaction for all the aforesaid assessment years was recorded on 28.09.2021. Facts being pari-materia to A.Y. 2013-14, our findings in appeal of the assessee for A.Y. 2013-14 would mutatis mutandis apply to appeals for A.Y. 2014-15 to 2017-18 & 2019-20. For parity of reasons, the assessment orders for aforesaid A.Ys. are quashed.

13. In the result, the appeals of the assessee are allowed.

14. To sum up, ITA No. 3181/Del/2025 [A.Y. 2013-14], ITA No. 3182/Del/2025 [A.Y. 2014-15], ITA No. 3183/Del/2025 [A.Y. 2015-16], ITA No. 3184/Del/2025 [A.Y. 2016-17], ITA No. 3185/Del/2025 [A.Y. 2017-18] and ITA No. 3186/Del/2025 [A.Y. 2019-20] are allowed.

15. Order pronounced in the Open Court on Monday the 30th day of March, 2026.

Author Bio