Case Law Details

CIT Vs Ernst And Young U.S. LLP (Delhi High Court)

Summary: The Delhi High Court, in CIT Vs Ernst And Young U.S. LLP, held that reimbursements made by Indian EY entities to the US entity for seconded employees constituted Fee for Technical Services (FTS) under Article 12 of the India–USA DTAA, as the secondment arrangement satisfied the “make available” test by transferring technical knowledge and skills enabling Indian employees to perform the work independently. The Court also held that the foreign entity remained the real employer because it retained the power to terminate the employees, continued their social security coverage, and the employees returned to the US after the secondment. Rejecting the argument that cost-to-cost reimbursement or TDS deduction by the Indian entity prevented taxation, the Court ruled that the absence of a markup did not by itself exempt the payments from tax. On the question of whether the receipts qualified as exempt “professional services” under Article 15 of the DTAA, the Court found that the ITAT had not adequately examined the nature of the services and remanded the issue for fresh consideration. The ruling highlights that Global Capability Centres (GCCs) and multinational companies should carefully review secondment agreements, determine the real employer based on the substance of the arrangement, separately evaluate professional services under the DTAA, and consider the transfer pricing implications of payments to foreign related parties.

Delhi High Court Ruling on Cross-border Secondment of employees

Why Employee secondment matters for Global Capability Centres (GCC) & MNCs in India

Cross border secondment is commonly used by Global Capability Centres (GCC) & MNCs in India by their foreign holding companies:

- To train employees on technical skills

- To facilitate technology implementation

- To deploy employees for project execution

- To ensure applicability of global standards in their Indian group of Companies

Background of the Case

Ernst & Young U.S. L.L.P. (‘EY US’ hereinafter) is based in the United States of America and is a member of the Ernst & Young (EY) network

There are three EY entities which operate in India (EY India), they are as under:-

(i) EY GBS (India) Pvt Ltd.

(ii) EY Global Delivery Services India LLP (EYGDS) and;

(iii) Ernst & Young LLP.

EY US has sent some employees on secondment to EY India for imparting technical skills to its Indian employees. EY India has reimbursed the cost of those employees to EY US on cost to cost basis on account of secondment of employees.

Employment offered by the EY India entities is for a limited period of time of 2-3 years, and on completion of their tenure, the said employees were repatriated back to the EY US.

However, for the convenience purpose, these employees are receiving salaries from EY US in their US account. Further, such costs shall be reimbursed by EY India to EY US.

However, these employees shall be on the payroll of EY India. Further, TDS is also deducted by EY India as per Income Tax Act, 1961.

Issues before the Court

Issue A: Whether cost to cost reimbursement on account of secondment of employees constitutes as FTS as per the provisions of section 9(1)(vii) as well as under Article 12 of the India-USA Double Taxation Avoidance Agreement(DTAA)

Issue B: Whether the fees received by EY US from EY India fall within the Article 12(5)(e) of India-USA DTAA exclusion (i.e., qualify as ‘professional services’ under Article 15 India-USA DTAA), thereby exempting them from Indian tax

Ernst & Young stand

EY US has entered into a deputation agreement with EY India under which employees shall be seconded to EY India which states that during the deputation, employees shall become employees of EY India.

EY India has discharged their TDS obligation under Section 192 of the Act to pay taxes to the Indian Authorities, resulting in the issuance of the requisite TDS certificate to the employees

The amounts having already been taxed at the hands of their seconded employees employed in India, the same cannot be subject to double taxation again through the assessee company i.e., EY US

Conditions of ‘make available’ does not satisfy. Therefore the payments made by EY India to EY Us does not qualify for Fee for technical services under Article 12(4)(b) of the DTAA.

EY US has rendered services to the Indian establishments which were “professional services” within the meaning of Article 15(2) of the DTAA and therefore such payments are in fact covered under Article (12)(5)(e) and not taxable in India

Revenue Stand

Since the services rendered by the EY US to EY India entities was with regard to technical knowledge, experience, skill, know-how or the processes which come within the meaning of Article 12(4)(b) of the DTAA and therefore should be taxable as FTS under Article 12 of the DTAA.

Seconded employees shall be treated as Employees of EY US only as these employees continue to contribute to social security benefits in US through EY US. The seconded employees also cannot opt out from contributing to the social security benefits in USA

Further, EY India does not have right to terminate the contracts with Employees. That right still remains with EY US. After the expiry of 2-3 years, employees shall go back to US to work with EU US. Therefore, employer employee relationship between EY US & employees still exist.

Revenue has relied on the judgement of Centrica India Offshore (P) Limited v. CIT, 2014:DHC:2172-DB, wherein the Court has held that amounts reimbursed by Indian entities to an overseas company in terms of a secondment agreement amounted to FTS and are liable to tax in India

Delhi High Court ruling

Issue A: Payments made by EY India to EY US treated as ‘Fee for Technical Services’ under Article 12 of the DTAA.

Hon’ble Court held that conditions ‘make available’ clause of DTAA is being satisfied as per the agreement entered between EY India & EY US. Technical skills were imparted by Seconded employees to Indian employees to imbibe the culture of EY Group and implement its policies/standards on the EY India. Once the process and policies are imbibed / retained, there is no need for the secondee personnel to work again with the EY India entities, as the employees of the EY India entities can apply the same by themselves.

Further, EY India cannot terminate the employees as such authority is not available with it. Once the work in India is completed, employees shall go back to join EY US. There is no employer-employee relationship exists between EY India & sceconded employees.

EY US continue to be the ultimate employer of these employees.

With the fulfilment of conditions of ‘make available’ clause, payment made by EY India to EY shall be treated as ‘Fee for Technical Services’ under Article 12 of the DTAA.

Issue B: Professional Receipts

Hon’ble High Court has held that ITAT has not delineated the actual services provided by the EY US to its Indian clients or discussed whether such services could be included in the definition. It merely noted the qualifications of the employees of the EY US and held that they would come within the ambit of the definition of professional services provided under Article 15(2).

The merit and effect of the finding of fact by the AO that the services are in the nature of technical services and consultancy have neither been discussed nor distinguished by the ITAT.

The court declined to interpret Article 15(2) definitively & remanded back the matter to ITAT ITRAT for fresh consideration on this matter.

Key Legal Principles highlighted by the Court

- Make available clause- Where technical knowledge, experience, skill, know-how or processes are transferred in such a manner that the Indian personnel are able to perform the work independently thereafter, the & “make available” condition under the DTAA may be regarded as satisfied.

- Professional Service bifurcation- Article 15 does not provide blanket exemption to all types of services. Each individual services needs to be checked separately.

- Substance over Form: The key consideration is identifying the real employer of the seconded employees. If the employees continue their employment relationship with the foreign entity, remain covered under its social security and employee benefit schemes, and the foreign employer retains overall supervision and control, the overseas entity may still be regarded as the actual employer.

- No Tax Shield for Companies: Simply recovering the exact employee cost without adding any markup does not, by itself, provide a tax advantage or exemption to the companies involved.

Important Points for GCCs and MNCs to Keep in Mind after This Decision

1) Review your Deputation agreement

2) Evaluate who qualifies as the real employer based on the substance of the arrangement rather than the contractual description alone

3) Professional receipts line wise categorised mandatory to check applicability of Article 15 of DTAA

4) Transfer Pricing application on payments made to foreign related parties

FULL TEXT OF THE JUDGMENT/ORDER OF DELHI HIGH COURT

CM APPL No.75760/2025(condonation of delay) in ITA 715/2025

1. For the reasons stated in the application, the delay of 21 days in filing the appeal stands condoned.

2. The application stands disposed of.

ITA 423/2025; ITA 424/2025; ITA 715/2025; ITA 753/2025; & ITA 760/2025

3. These appeals filed by the Revenue under Section 260A of the Income Tax Act, 1961 (the Act) relate to different Assessment Years (AY) from 2018-19 upto 2022-23.

4. We must state here that these appeals involve identical questions of law however they diverge on facts. ITA 424/2025 pertains to AY 2021-22 wherein the assessee filed its return of income on 22.12.2021 declaring a total income of Rs.67,74,750/- and claimed the refund of TDS amount of Rs.3,01,41,850/- as exempt income and offered its income to tax as per Section 115A of the Act. The Assessing Officer (AO) passed a Draft Assessment Order (DAO) proposing to make an addition of Rs.18,28,95,723/- to the income of the assessee on account of payment received by the assessee with respect to seconded employees in India and Rs.30,73,50,907/- on account of receipts from professional services. The AO in the DAO had bifurcated the amounts under different heads; (i) first being the amount calculated to be reimbursed as costs with respect to seconded employees being Rs.18,28,95,723/-; and (ii) the amounts which were receipts from India based clients for services performed in and from the USA amounting to Rs.65,20,12,778/-, which services were examined and the amount of Rs.30,73,50,907/- was found to be not falling under the exemption clause, under Article 12(5) (e) of the India-USA Double Taxation Avoidance Agreement (DTAA).

5. The assessee had filed objections to the DAO before the Dispute Resolution Panel (DRP), and the DRP vide order dated 10.08.2023 rejected the contentions of the assessee and upheld the additions made by the AO in the DAO. Consequently, the final assessment order was passed, as per the directions of the DRP. The Income Tax Appellate Tribunal (ITAT) allowed the appeal filed by the assessee and set aside the assessment order. The issue which arises in this appeal is whether the payment received by the assessee on account of secondment of employees would be taxable as Fees for Technical Services (FTS) under Article 12 of the DTAA and whether the receipts for services rendered in and from the USA fall under the exemption of Article 12(5)(e) of the DTAA.

6. The challenge in ITA 423/2025 pertains to the AY 2019-20 for which the ITAT has held that the sum of Rs.50,99,38,561/- to be cost to cost reimbursement on account of secondment of employees as FTS under Section 9(1) (vii) of the Act as well as Article 12 of the DTAA. During the AY 2019-20 the assessee filed its return of income on 30.08.2019 declaring a total income of Rs.32,73,620/- and claiming Rs.1,06,40,79,637/- as exempt income and offered its income to tax as per Section 115A of the Act. The AO passed a DAO proposing to make addition of Rs.50,99,38,561/- to the income of the assessee on account of payments received by the assessee with regard to its seconded employees in India. The assessee filed objections to the DAO before the DRP. The DRP vide order dated 24.05.2022 rejected the contention of the assessee and upheld the addition made by the AO in the DAO.

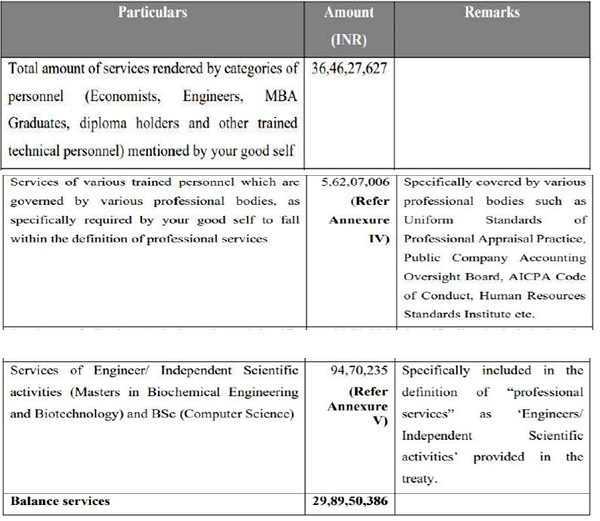

7. The next set of appeals being ITA 715/2025, 760/2025 and 753/2025, have been heard separately, after we reserved the orders in ITA 423/2025 and 424/2025. This Court had framed questions of law vide order dated 17.12.2025 in ITA No.753/2025 and order dated 18.12.2025 in ITA 760/2025. The ITA No.715/2025 pertains to the AY 2020-21 wherein the assessee filed its return of income on 22.03.2021 declaring a total income Rs.67,19,060/- and claiming refund of TDS amounting to Rs.8,15,73,480/-as exempt income and offered its income to tax as per Section 115A of the Act read with provisions of Article 12 of the DTAA. The AO added Rs.68,02,25,664/- as taxable income on account of payments received by the assessee with regard to seconded employees. Furthermore, the AO has also made addition of Rs.29,89,50,386/- on account of receipts for services held to be taxable as FTS.

8. ITA 760/2025 relates to AY 2022-23 wherein the AO has made addition of Rs.13,94,26,424/- as cost to cost reimbursement on account of seconded employees and also an amount of Rs.97,78,94,279/- on account of receipts for the services rendered in and from the USA.

9. ITA 753/2025 pertains to AY 2018-19 wherein the AO has made addition of Rs.24,05,12,955/- on account of cost to cost reimbursement in respect of seconded employees and Rs.3,82,22,932/- for receipts from professional services rendered from the USA held to be taxable as FTS.

10. In ITA No.715/2025 this Court had not framed any questions of law, however, based on the arguments advanced by the learned counsel for the parties, this Court admits the appeal and frames following questions of law for consideration:-

A. Whether on the facts and in the circumstances of the case and in law, the ITAT is erred in holding that sum of Rs.68,02,25,664/- as cost to cost reimbursement on account of secondment of employees should not be treated as FTS as per the provisions of section 9(1)(vii) as well as under Article 12 of the India-USA Double Taxation Avoidance Agreement (DTAA)?

B. Whether on the facts and in the circumstances of the case and in law, the ITAT has erred in appreciating the application of “Make available” clause, in the case of assessee, which is necessary for holding Rs. 29,89,50,386/-as FTS as per Article 12 of India-USA DTAA?

C. Whether on the facts and in circumstances of the case and in law, the ITAT was justified in holding that the assessee falls within the meaning of Article 12(5)(e) of the India-USA DTAA?

11. A summary of the prayers and questions of law framed in these appeals are tabulated as under for convenience:

| Particulars | AY | Prayers | Questions of law framed along with date of order |

| ITA 753/2025 arising from ITAT ITA No.1254/Del/ 2025 against Assessment Order dated 18.12.2024 | 2018-19 | (a) To formulate the Substantial Questions of Law mentioned in Para 3 of the Memo of Appeal;

(a) To formulate any other Substantial Questions of (a) To set aside the impugned order dated 31.07.2025 of the ITAT in ITA No.1254/Del/2025. |

Vide order dated 17.12.2025

(A) Whether on the facts and in the circumstances of the case and in law, the ITAT is erred in holding that sum of Rs.24,05,12,955/- as cost to cost reimbursement on account of secondment of employees should not be treated as FTS as per the provisions of section 9(l)(vii) of the Income Tax Act, 1961 as well as under Article 12 of the India- USA Double Taxation Avoidance Agreement (DTAA)? (B) Whether in the facts of |

| ITA 423/2024 arising from ITAT ITA No.2332/Del/ 2022 against Assessment Order dated 27.07.2022 | 2019-20 | (a) To formulate the Substantial Questions of Law mentioned in Para 3 of the Memo of Appeal;

(b) To frame any other Substantial Questions of Law which may arise from the impugned order dated 20.06.2023; (c) To set aside the impugned order dated 20.06.2023 of the Hon’ble ITAT in ITA No. 2332/DEL/2022; |

Vide order dated 29.10.2025

A. Whether on the facts and in the circumstances of the case and in law, the Hon’ble ITAT is erred in holding that sum of Rs.50,99,38,561/- as cost to cost reimbursement on account of secondment of employees should not be treated as FTS as per the provisions of section 9(1)(vii) as well as under Article 12 of the India- USA Double Taxation Avoidance Agreement(DTAA) ? B. Whether on the facts and in the circumstances of the case and in law, the Hon’ble ITAT has erred in appreciating the application of “Make available” clause, in the case of assessee, which is necessary for holding Rs.50,99,38,561/- as FTS as per Article 12 of India- USA DTAA? |

| ITA 715/2025 arising from ITAT ITA No.2168/Del/ 2023 against Assessment Order dated 30.05.2023 | 2020-21 | (a) To frame the Substantial Questions of Law mentioned in Para 3 of the Memo of Appeal;

(b) To frame any other Substantial Questions of Law which may arise from the impugned order dated 19.05.2025; (c) To set aside the impugned order dated 19.05.2025 of the ITAT in ITA No.2168/Del/2023. |

A. Whether on the facts and in the circumstances of the case and in law, the ITAT is erred in holding that sum of Rs.68,02,25,664/- as cost to cost reimbursement on account of secondment of employees should not be treated as FTS as per the provisions of section 9(1)(vii) as well as under Article 12 of the India- USA Double Taxation Avoidance Agreement (DTAA)?

B. Whether on the facts and in the circumstances of the case and in law, the ITAT has erred in appreciating the application of “Make available” clause, in the case of assessee, which is necessary for holding Rs. 29,89,50,386/-as FTS as per Article 12 of India- USA DTAA? C. Whether on the facts and in circumstances of the case and in law, the ITAT was justified in holding that the assessee falls within the meaning of Article 12(5)(e) of the India-USA DTAA? |

| ITA 424/2024 arising from ITAT ITA No.3253/Del/ 2023 against Assessment Order dated 19.09.2023 | 2021-22 | (a) To formulate the Substantial Questions of Law mentioned in Para 3 of the Memo of Appeal;

(b) To frame any other Substantial Questions of Law which may arise from the impugned order dated 07.08.2024; (c) To set aside the impugned order dated 07.08.2024 of the Hon’ble ITAT in ITA No.3253/DEL/2023; |

Vide order dated 30.10.2025 A. Whether on the facts and in the circumstances of the case and in law, the Hon’ble ITAT is erred in holding that sum of Rs.49,02,46,630/- as cost to cost reimbursement on account of secondment of employees should not be treated as FTS as per the provisions of section 9(1)(vii) as well as under Article 12 of the India- USA Double Taxation Avoidance Agreement(DTAA) ?

B. Whether on the facts and in the circumstances of the case and in law, the Hon’ble ITAT has erred in appreciating the application of “Make available” clause, in the case of Assessee, which is necessary for holding Rs.30,73,50,907/-as FTS as per Article12 of India- USA DTAA? |

| ITA 760/2025 arising from ITAT ITA No.1243/Del/ 2025 against Assessment Order dated 12.12.2024 | 2022-23 | (a) To formulate the Substantial Questions of Law mentioned in Para 3 of the Memo of Appeal;

(b) To formulate any other Substantial Questions of Law which may arise from the impugned order dated 31.07.2025; (c) To set aside the impugned order dated 31.07.2025 of the ITAT in ITA No. 1243/Del/2025. |

Vide order dated 18.12.2025

(A) Whether on the facts and in the circumstances of the case and in law, the ITAT is erred in holding that sum of Rs.13,94,26,424/- as cost to cost reimbursement on account of secondment of employees should not be treated as FTS as per the provisions of section 9(1)(vii) of the Income Tax Act, 1961 as well as under Article 12 of the India-USA Double Taxation Avoidance Agreement (DTAA)? (B) Whether in the facts of this case, the amount of Rs.97,78,94,279/- received by the assessee shall fall within the provisions of the Article 12(4) (b) or 12(5)(e) read Article 15 of the India-USA DTAA? |

12. Before delving into the merits of the controversy, it is pertinent to give a brief factual background surrounding these appeals. The respondent assessee which in this case is Ernst & Young U.S. L.L.P. (‘EY US’ hereinafter) is based in the United States of America and is a member of the Ernst & Young (EY) network. As per the appellant there are three EY entities which operate in India (EY India entities), they are as under:-

(i) EY GBS (India) Pvt Ltd.;

(ii) EY Global Delivery Services India LLP (EYGDS) and;

(iii) Ernst &Young LLP.

SUBMISSIONS ON BEHALF OF THE APPELLANT/REVENUE

13. It is the case of the appellant/Revenue and contended by Mr. Puneet Rai, learned Senior Standing Counsel that the assessee is a limited liability partnership firm, incorporated under the laws of the USA and is engaged in the business of providing professional services in the field of assurance, tax, transaction and business advisory services etc., to its clients across the globe including India.

14. It is the case of Mr. Rai that the primary issue in these appeals is whether the payments received by the assessee company on account of secondment of its employees would be taxable as FTS under Article 12 of the India-USA DTAA.

15. As per Mr. Rai, the AO had rightly made additions in respect of payments received by the assessee from the EY India entities since the services rendered by the assessee to the EY India entities was with regard to technical knowledge, experience, skill, know-how or the processes which come within the meaning of Article 12(4)(b) of the DTAA and therefore should be taxable as FTS under Article 12 of the DTAA. He stated that the ITAT had erroneously held that the seconded personnel are to be treated as employees of EY India entities; payment received by the assessee company is a cost to cost reimbursement on account of secondment of employees and thus cannot be treated as FTS under Article 12 of the India-USA DTAA.

16. Mr. Rai in respect of issue of receipts for service rendered in and from the USA (as per questions of law framed as B and C in all the appeals with an exception of the issues involved in ITA 423/2025) fall under the exemption of Article 12(5) (e) of the DTAA has argued that unlike the services which are termed to be “professional services” under Article 15 of the DTAA the services which are offered by the seconded employees are in the nature of technical services and as such they are not covered under the exemption carved out in Article 12(5) (e) of the DTAA. The exemption pertains to independent scientific, literary, artistic, educational or teaching activities as well as the independent services rendered by physicians, surgeons, dentists, lawyers, engineers, architects and accountants. According to Mr. Rai the exemption for professional services as defined under Article 15 of the DTAA is only applicable if such services were rendered in India and not from outside India. The assessee belongs to the latter category and thus, the protection under Article 12(5) (e) of the DTAA is not available to the assessee.

17. On the first issue, it is his case that the ITAT has erred in returning a finding that “make available” in terms of Article 12(4)(b) of the DTAA is not satisfied. He states that the AO and DRP on this issue have given concurrent findings and this Court ought to refer to these findings and uphold the same.

18. In other words, the submission of Mr. Rai, is that the AO had rightly made additions on account of payments received by the assessee from the EY India entities since the services rendered by the assessee to the EY India entities is covered by Article 12(4)(b) of the DTAA and therefore, should be deemed to be taxable as FTS.

19. According to him, the AO as well as the DRP have given concurrent findings of fact that the employment offered by the EY India entities is for a limited period of time of 2-3 years, and on completion of their tenure, the said employees were repatriated back to the assessee company. He has reinforced his argument that the employment with EY India entities comes with a lien marked on the employment with the parent company which is the assessee in the present case. The seconded employees are not free to move anywhere but they must go back to the parent company i.e., back to the assessee, on the expiry of the said tenure, which means that the seconded employees never ceased to be the employees of the assessee, i.e., EY US. According to him, this factum is further corroborated by the fact that the employees working in India still contribute to the social security benefits in the USA through the assessee. Therefore, the employer-employee relationship between the assessee and the employees continued to exist even though they were working in India. Accordingly, the seconded employees also cannot opt out from contributing to the social security benefits in USA. The employees who were working outside USA with the assessee company are the only ones eligible for the social security scheme and, thus, by making these contributions it is clear that the employees are still working for the US entity being the assessee. In this regard, he has referred to the extracts of the Internal Revenue Services, USA (IRS) website on social security contribution of the employees.

20. As per Mr. Rai, the seconded employees of EY US came to India to provide professional services in the field of assurance, tax, transaction and business advisory services etc., to ensure the application of EY Group policies / processes and other quality standards in the EY India entities. This would demonstrate that the processes and policies are retained by the EY India entities and they do not require the services of the seconded employees of the assessee in future. In this regard, Mr. Rai has relied upon a judgment of a coordinate Bench of this Court in the case of Centrica India Offshore (P) Limited v. CIT, 2014:DHC:2172-DB, wherein according to him, this Court has held that amounts reimbursed by Indian entities to an overseas company in terms of a secondment agreement amounted to FTS and are liable to tax in India. The submission that the payments made by the assessee to overseas entities therein was a cost to cost reimbursement was rejected. According to him, the Court has observed that the fact the overseas entity does not charge a markup over and above the cost for maintaining the secondee is irrelevant in itself, since the absence of markup subject to an independent transfer pricing exercise, cannot negate the nature of the transaction. He stated in that case, the salaries of the seconded employees were paid by the overseas companies and the same was paid back by the Indian entity to the overseas companies. It was in this background that according to Mr. Rai, this Court had held that the overseas entities were providing technical services to the Indian entity which would make the case fall within the scope of Article 12 of the India-Canada DTAA.

21. He would also contend that the decision in Centrica India Offshore (P) Limited (supra) has attained finality since the Special Leave Petition against the said decision has been dismissed by the Supreme Court.

22. According to Mr. Rai, since there is a concurrence of facts in Centrica India Offshore (P) Limited (supra) and the present case, the ITAT erred in holding that the amount received by the assessee is not taxable in India solely on the basis that the seconded employees have offered tax on the amount received by them. The tax paid by the seconded employee cannot decide the taxability of the assessee in India, if the services provided by them through their employees in India is covered under the scope of FTS within the meaning of Article 12 of the DTAA.

23. On the issue of professional receipts added as FTS, he has stated that the AO had rightly treated the amounts received by the assessee on account of services as fees for inclusive services as per Article 12(4)(b) of the DTAA because the said services do not qualify within the definition of independent personal services as per Article 15 of the DTAA, which has described “Professional Services”. According to him, only those services, which are related to activities mentioned in the said Article qualify as “Professional Services” and thereby exempted as per the DTAA. He stated that the ITAT ought not have held that the case of the assessee falls within the meaning of Article 15(2) of the DTAA and entitling them to the benefits under Article 12(5) (e) of the DTAA. Mr. Rai has stated that ITAT has erred in confining the definition of “Professional Services” to persons who are governed by professional organizations. According to him the ITAT has wrongly drawn a parallel on the scope of “Professional Services” with Section 194J and Section 44AA of the Act. The scope of tax relief based on certain terminology provided by the provisions of the Act cannot be used to interpret the provision of DTAA which in itself separate specific document arrived at after deliberations between two sovereign nations and hence, these analogies made by the ITAT are misplaced.

24. It is also his submission that the Article is only applicable if the services were rendered in India. In this case, the services have been rendered from outside India, making these transactions fall outside of Article 15 of the DTAA.

25. He has challenged the finding of the ITAT, by stating that “make available” in terms of Article 12(4) (b) of the DTAA is fully satisfied as the seconded employees have transferred skill, knowledge and experience to the EY India entities.

26. He contended that as these appeals cover identical questions of law for different assessment years, he shall adopt the arguments advanced in ITA 423/2025 and ITA 424/2025 in the other appeals numbered as ITA 715/2025, ITA 753/2025 & ITA 760/2025. He has sought the prayer(s) made in the appeals.

SUBMISSIONS ON BEHALF OF THE RESPONDENT/ASSESSEE

27. Mr. S. Ganesh, learned Senior Advocate appearing with Ms. Ananya Kapoor, Advocate on behalf of the respondent/assessee stated that since the issues involved in the present appeals are identical he wishes to adopt the arguments advanced in ITA 423/2025 and ITA 424/2025 across the other appeals being ITA 715/2025, ITA 753/2025 and ITA 760/2025.

28. He further stated that EY US had entered into a deputation agreement with the EY India entities under which certain personnel of EY US were seconded to the three EY India entities. In this regard he has referred to certain clauses of the Deputation Agreement which we reproduce as under:-

“AND WHEREAS EY US has personnel who possess the requisite qualification and experience and who are agreeable to be assigned to EYGDSINDIA and who were selected by EY GDS India to be acceptable to it.

AND WHEREAS EYUS has agreed to relieve such personnel (hereinafter EYGDS India Employee) so that he can work in employment with EYGDS INDIA on the terms and conditions as agreed between EYGDS INDIA and Employee;

AND WHEREAS the personnel shall be released from their work at EYUS and shall be integrated in EYGDS INDIA for the period of employment with EYGDS INDIA.

xxx xxx xxx

“Assign” shall mean employment by EYGDS INDIA of an International Assignee released by EYUS (and “Assigned” shall be construed accordingly).

“Assignment” shall mean release of personnel of EY US to and who is to be in employment by EYGDS India for period of employment under the terms and conditions agreed by EYGDS India and employee.

xxx xxx xxx

(iii) Clause 2:

(2) Engagement of International Assignees EYUS shall release the employee to EYGDS INDIA and EYGDS INDIA shall engage employ him in its own business and as its own employee……

(iv) Clause 3

“3. General terms and conditions of Assignment

1. During the Period of Assignment, the International Assignees shall function solely under the control, direction and supervision of EYGDS INDIA and in accordance with all rules, regulations, policies, guidelines and other practices, generally applicable to the employees of EYGDS INDIA. International Assignees shall work exclusively for EYGDS INDIA and shall be solely responsible to EYGDS INDIA for their work during the period of Assignment. EYGDS INDIA shall decide the nature of work of the International Assignee and EYGDS INDIA shall be solely responsible for the work of International Assignees during the period of Assignment.

3.2 EYUS shall not be responsible for the work of the International Assigner, or assure any risk for results produced from the work performed by the International Assignees during the period the International Assignees shall not be regarded as an employee or EYUS and shall not in any way be subject to any kind of instructions or control of EYUS during the Period of Assignment.

3.3 EYUS shall not have any obligation towards EYGDS INDIA with regard to the performance of International Assignees. The privity and lien of EYUS would cease during the period of employment with EYGDS INDIA on entering of Employment Contract by International Assignee with EYGDS INDIA.

3.4 EYGDS INDIA shall be solely responsible to pay salary and other costs of International-Assignees during the Period of Assignment as provided in Section 4 of the Agreement, EYGDS INDIA also undertakes to:

(i) bear all reasonable expenses relating to boarding & lodging, food & beverage, travel and other miscellaneous expenses associated with the performance of work by the International Assignees;

(ii) pay any terminal payments or any special allowances to International Assignees in accordance with the terms of Employment Contract.

3.5 The tools, equipment, infrastructure and information necessary for the International Assignees to carry out their duties of employment during the Period of Assignment would be provided by EYGDS INDIA. EYGDS INDIA shall also undertake necessary steps for the International Assignees to comply with regulatory formalities like procuring visas, work permits meet any other regulatory requirements.

3.6 During the Period of Assignment, EYGDS INDIA shall have a right to undertake performance appraisal of the International Assignees in accordance with policy of EYGDS INDIA.

3.7 EY LLP shall have a right to terminate the Assignment of an International Assignee.

3.8 During the Period of Assignment, EYUS shall not save a right to recall any International Assignee without the approval of EYGDS INDIA, EYUS will also not be under any obligation to replace any of the Assigned personnel in the event where employment of any personnel is terminated with EYGDS INDIA for any reason.

3.9 During the Period of Assignment, International Assignees shall not act tor and on behalf of EVUS nor make any representations or warranties on behalf of EVUS. Likewise, International Assignees shall not assume any obligations in the name of or on account of EYUS nor has authority to create any obligations in favor or on third parties with regard to EVUS.

3.10 During the Period of assignment, EYGDS INDIA shall have the exclusive right to undertake any legal or disciplinary action against any misconduct, fraud, willful negligence or any other illegal action of any International Assignee. EYGDS INDIA can terminate the employment prior to the agreed period and relieve him from EYGDS INDIA in the event of any misconduct or fraud or willful negligence of any other illegal action. EYGDS INDIA shall be solely obligated to address any conflicts with the International Assignees in relation to the Assignment under this Agreement, International Assignees shall not have any legal recourse to EYUS for any conflicts arising in relation to his/her Assignment.

3.11 In addition to above, Assignment under this Agreement shall be subject to other specific terms and conditions as laid down in the Employment Contract of each International Assignee. The terms of Employment Contract shall specifically include details with regard to term of employment with EYGDS INDIA like Period of Assignment, nature of work, details of salary and other costs and such other terms as are customary.

4. Remuneration to International Assignee

4.1 During the Period of secondment, EYGDS INDIA alone shall be solely responsible to bear and pay salary and other costs of international Assignees. However, for administrative convenience, EYUS may make payment (on behalf of EYGDS INDIA) towards salary and other costs to the International Assignees as agreed between international Assignees and EYGDS INDIA and as recorded in Employment-Contract of International Assignees EYUS shall intimate EYGDS INDIA and EYGDS INDIA shall reimburse EYUS for such payments made towards salary and other costs in relation to the period of secondment of the International Assignees on an actual basis subject to tax being withheld as per the applicable provisions of the India tax laws. For this purpose, EYUS would produce the necessary documentary evidence supporting the payment towards salary and other costs to the International Assignees, to EYGUS INDIA, to enable the latter to reimburse the cost so defrayed on behalf of EYGDS INDIA EYUS agrees not to charge any additional amount or mark up over and above the reimbursement of actual payments made by it on behalf of EYGDS INDIA.

4.2 All other costs and expenses in India relating to the International Assignees, including without limitation, reasonable expenses relating to boarding & lodging, food & beverage, travel and other miscellaneous expenses associated with the performance of work by the International Assignees shall be borne by EYGDS INDIA. In addition EYGDS INDIA may also make an additional payment by way of a special allowance to the International Assignees as agreed in the Employment contracts.

5. Taxation

EYGDS INDIA shall alone be responsible for complying with the complying of withholding tax under the Indian tax laws, salary and other costs paid to the International Assignees.”

29. According to Mr. Ganesh the above results in the following:-

a) The secondees cease to be employees of EY US during the period of deputation and become employees of the EY India entities.

b) The EY India entities discharge their obligations in respect of deduction of tax at source under Section 192 of the Act to pay taxes to the Indian Authorities, resulting in the issuance of the requisite TDS certificate to the employees.

c) The money which is paid by EY US to its employees in USA is on behalf of the EY India entities. The same is only for the sake of administrative convenience. Salary and other costs remain the liability of the EY India entities.

d) EY US raises an invoice to the EY India entities for reimbursement of the exact amount which is paid by EY US to the secondees without any addition or subtraction.

e) This reimbursed amount is now sought to be taxed by the Indian Authorities. This addition made to the taxable income of EY US has been rightly set aside by the ITAT.

30. Mr. Ganesh stated that the ITAT has elaborately dealt with the issue of cost to cost reimbursement within the provisions of Section 9(1)(vii) of the Act and Article 12 of the DTAA. In this regard, he has placed reliance on the judgment of a coordinate Bench of this Court in the case of P.C.I.T. v. Boeing Limited, 2022:DHC:4188-DB which according to him, has distinguished the judgment in Centrica India Offshore (P) Limited (supra) wherein the foreign company was rendering services to the Indian entity through its own employees who never became employees of the Indian entity, but remained employees of the foreign employer at all times. It is therefore, held in Centrica India Offshore (P) Limited (supra) that the payment made by the Indian entity is nothing but compensation or service charges paid to the foreign entity. This position, he contended is entirely different from that in the present case, given the unequivocal findings of fact by the ITAT to the effect that the payment made by the assessee to EY India entities is nothing but a cost to cost reimbursement. In this regard, he has relied upon the judgment the of ITAT in Pr. Commissioner of Income Tax-1 v. AT & T Communication Services India Pvt Limited, ITA No.354/Del/2017 dated 31.10.2018which according to him, has distinguished the decision in Centrica India Offshore (P) Limited (supra). He has also buttressed his submissions by relying on the findings of the Supreme Court and this Court in the cases of DIT (International Taxation) v. AP Moller Maersk AS, (2017) 392 ITR 186 (SC) and CIT v. Industrial Engineering Projects (P) Ltd, [1993] 202 ITR 1014 (Delhi).

31. It is his case that since the ITAT is an authority which may determine questions of fact, the same cannot be challenged at this stage before this Court. Reference in this regard has been made to Ravindranathan Nair v. CIT, (2001) 247 ITR 178.

32. The ITAT has clearly held that the seconded personnel are employees of the EY India entities. The ITAT has also held that the amounts paid by the EY India entities to EY US have been taxed as salary at the hands of the seconded employees and further the amounts paid by EY India entities to EY US is a cost to cost reimbursement of the amount paid by EY US for and on behalf of EY India entities. The amounts having already been taxed at the hands of their seconded employees employed in India, the same cannot be subject to double taxation again through the assessee company i.e., EY US. He stated that the Supreme Court has clearly laid down two conditions which have to be fulfilled in order to make a tenable challenge to a finding of fact given by the ITAT. Firstly, raising a specific question of law which records an express issue of perversity of a finding of fact; and secondly, establishing the perversity by showing that such a finding is not based on any evidence or material on record or rather the same is inconsistent with the material or evidence on record. In this present case, the appellant has not challenged the said findings in the manner which has been laid down by the Supreme Court in K. Ravindranathan Nair (supra) and that this Court is bound by the findings of the ITAT.

33. Mr. Ganesh stated that this appeal is identical in terms of the question of law which arises ITA No. 423/2025, for the AY 2019-2020. He submitted that the order of the ITAT should also be upheld in so far as this appeal is concerned.

34. According to Mr. Ganesh, the Revenue now seeks to place reliance for the very first time, at this juncture on a document titled “Social security tax consequences of working abroad”. According to him, the said document is only a general statement and a highly simplified version with regard to the employees who are sent abroad on deputation. The said document does not cover a situation where specific agreements are entered between two independent entities i.e., EY US and EY India entities, which contain specific and unequivocal clauses, as per which the secondees shall be the exclusive employees of EY India entities, which ultimately exercises the administrative and disciplinary control over them. According to him, EY India entities have been discharging all the above said functions and the same has not been questioned by the Indian Revenue authorities, hence the extracts from IRS website are not applicable in the present case whatsoever. Further, this document was not placed before the ITAT and the Tribunal could not comment or consider the same let alone giving any finding on that document. According to him, it is a well settled principle of law that in an appeal under Section 260A of the Act only those questions can be raised which are substantial questions of law and arise out of the order of the ITAT, which means that these questions ought to have been first raised before the ITAT and the ITAT ought to have also decided them. Since, none of these fundamental requirements are fulfilled in these cases, the extract from the IRS website cannot now be relied upon given the findings of the ITAT in respect of AY 2019-20.

35. The Revenue also cannot argue to the contrary to the indisputable position that EY India entities have been accepted as employers and the secondees as their employees and the TDS certificate issued by the EY India entities to the secondees have not been questioned or disputed by the Revenue.

36. He stated that another distinct aspect of this issue is that the Supreme Court in AP Moller Maersk AS (supra)had clearly laid down the law on cost to cost reimbursement. This principle is not in any way dependent on the object or the purpose of the payment or even the person to whom the payment is made and whether this payment was obligatory or mandatory. Even if the payment is partly or wholly towards social security dues, it does not in any way detract from the fact that it is a cost to cost reimbursement, which by itself is conclusive that the matter does not give rise to any taxable income.

37. In this regard, he has relied upon the order of the ITAT for the AY 2020-21 which followed the order for AY 2021-22 in which the ITAT has categorically found that the services rendered by the assessee do not fulfill the ‘make available’ requirement under Article 12(4)(b) of the DTAA.

38. The second question of law which has been raised in these appeals are in respect of the fees received by EY US from various Indian establishments for the professional services which have been rendered by EY US. It is his case that the contention of the Revenue that these amounts are taxable in India as the fees for Included Services which are FTS under Article 12 of the India-USA DTAA, is unmerited. The provisions under Article 12(5)(e) provide that payments made for professional services as defined in Article 15 are not covered by Article 12 of the DTAA. He stated that the ITAT has rightly upheld the contention of the assessee and given a finding that the services are not covered under Article 12(4)(b) of the DTAA which clearly provides that if the conditions of “make available” are not fulfilled this Article would not be applicable. In this regard he has cited the following judgments in support of his argument:-

i. C.I.T v. Bio-Rad Laboratories (Singapore) Pte Ltd, (2023) 459 ITR 5 (Del)

ii. C.I.T v. RELX Inc, 160 taxmann.com1090

iii. Aecom Techinal Services Inc. ITO, 174 com1173

39. Mr. Ganesh has relied upon the reasoning of the ITAT to state that the issue of professional services rendered by EY US to the Indian establishments has been examined in great detail and the ITAT has given a categorical and unequivocal finding in paragraph 27 of the impugned order to hold that the services rendered by EY US do not fulfill the requirements of Article 12(4)(b) of the DTAA. He has relied upon the judgment of the Supreme Court in K. Ravindranathan Nair (Supra) to state that this Court ought not look into a finding of fact which has been returned by the ITAT.

40. Mr. Ganesh has contested the arguments advanced by the appellant in reference to Article 12(4)(b) read with Article 12(5)(e) and Article 15 of the DTAA to state that EY US has rendered services to the Indian establishments which were “professional services” within the meaning of Article 15(2) of the DTAA and therefore such payments are in fact covered under Article (12)(5)(e) and not taxable in India. The only argument advanced on behalf of the appellant regarding this issue is that the people rendering these services where engineers, economists, technical experts, and computer and software experts who are not members of a statutory professional body such as the Bar Council of India or the Medical Council of India and therefore according to the appellant even though these persons were recognised experts in their respective fields, they could not be considered to be “professionals” within the meaning of Article 15 of the DTAA. He stated that this ground was already set out in the show cause notice by the AO and also in the DAO based on which adverse directions were given by the DRP. He stated that a plain reading of Article 15 along with Article 12(5)(e) would show that such an interpretation is wrongful in law. Article 15(2) of the DTAA reads as under:-

“(2). The term “professional services includes independent scientific, literary, artistic, educational or teaching activities as well as the independent activities of physicians, surgeons, lawyers, engineers, architects, dentists and accountants.

41. Section 194J of the Act, which has been referred to by Mr. Ganesh reads as under:-

“(a) “Professional services” means services rendered by a person in the course of carrying on legal, medical, engineering or architectural profession or the profession of accountancy or technical consultancy or interior decoration or advertising or such other profession as is notified by the Board for the purposes of section 44A or of this section.”

42. Mr. Ganesh further stated that Section 44AA of the Act also treats the same activities as professional services and authorises the Central Board of Direct Taxes to notify other professionals. The Board has issued notifications and has declared, artists, actors, directors, editors and computer experts as professionals, even though none of these persons belong to any professional body. He stated that this Court ought to follow the findings of the ITAT in the impugned order to hold that the contentions as advanced by the Revenue are erroneous and therefore must be rejected.

43. He stated that the ITAT has rightly accepted the contentions of the assessee and held that under Article 12(5) (e) read with Article 15(2) of the DTAA, the said professional fees received by the assessee cannot be taxed in India at all.

44. In light of the above arguments, he prayed that these appeals be dismissed.

ANALYSIS AND CONCLUSION

45. Having heard the learned counsel for the parties and perused the records, the issues involved in this batch of appeals can be summarised as follows:-

| ITA No. | AY | Issue involved | Amounts involved (INR) |

| 753/2025 | 2018-19 | Cost to cost reimbursements added as FTS | 24,05,12,955 |

| Professional receipts added as FTS | 3,72,22,932 | ||

| 423/2025 | 2019-20 | Cost to cost reimbursements added as FTS | 50,99,38,561 |

| 715/2025 | 2020-21 | Cost to cost reimbursements added as FTS | 68,02,25,664 |

| Professional receipts added as FTS | 29,89,50,386 | ||

| Assessee falls within the meaning of Article 12(5)(e) of the India – USA DTAA | — | ||

| 424/2025 | 2021-22 | Cost to cost reimbursements added as FTS | 49,02,46,630 |

| Professional receipts added as FTS | 30,73,50,907 | ||

| 760/2025 | 2022-23 | Cost to cost reimbursements added as FTS | 13,94,26,424 |

| Professional receipts added as FTS | 97,78,94,279 |

46. As these connected appeals are in respect of same assessee relating to different AYs with different amounts, but on identical facts, we deem it appropriate not to repeat the facts more particularly those that are overlapping. Moreover, since the questions of law are interconnected, we deem it appropriate to answer them with our analysis below.

47. The challenge in these five appeals by the Revenue is to the orders passed in the appeals filed by the assessee / respondent before the ITAT. We have already reproduced the substantial questions of law framed in these appeals. The records reveal that EY US is engaged in the field of assurance, tax, transaction and business advisory services etc., to its client across the globe, including India. The assessee received the payments on account of secondment of its employees and for services rendered to Indian establishments in and from USA. The employees were posted in EY India entities in terms of the deputation agreement executed between the assessee and the EY India entities. One of the questions is whether the payment received by the assessee company on account of secondment of its employees in the EY India entities would be taxable as FTS.

48. It may be stated here that the first appeal which was decided by the Tribunal was ITA No.2332/Del/2022 pertaining to AY 2019-20, which has been challenged in ITA No.423/2025. The assessment order dated 27.07.2022, which was subject matter of the appeal before the Tribunal was preceded by the DRP order dated 24.05.2022. In the assessment order dated 27.07.2022, the AO has inter alia, stated as under: –

“8. The arguments of the assessee have been considered but are found to be untenable due to the following reasons:

-

- The case of employment with EY Indian entities is, unlike an independent employment comes with a lien marked on the employment with the parent and the employee is not at a free will to move anywhere but only to go back to the parent on expiry of their tenure;

- The employees never ceased to be the employees of overseas entities, which is evident from the fact that EY US is making payment to the employees of Indian entities. Hence the salary paid to the employees of EY US LLP has borne out of the inherent obligation in the EY US LLP as the employer;

- EY US LLP on request / requisition from EY India entities (hereinafter refer as ‘EY India’) deputes its / group entities staff based on Indian company’s requirement. On completion of their tenure, the personnel are repatriated to the assessee. The personnel retain their lien when they come to India. They lend their experience as an employee of EY US LLP only in providing the consultancy services and not otherwise as the groups/processes standards are sought to be implemented;

- The deputed personnel have come to India, to imbibe the culture of the group and ensure the application of the EY group policies / processes and other quality standard sin EY India. This clearly demonstrates once the processes and policies are imbibed/retained, there is no need for the personnel again and EY India entities can apply the same by itself. Hence the services have also made available the technical knowledge/skill and experience;

- The cost to cost reimbursement of the expenses is not an argument as the fee for technical services/ Independent Personal Services do not mandatorily require to have a mark-up.

xxxx xxxx xxxx

It was also held in this ruling that consultancy services could also be technical in nature. These two expressions are not to be treated as watertight compartments. However, advisory services which merely involve discussion and advice of routine nature or exchange of information cannot appropriately be classified as consultancy service. An element of expertise or special knowledge on the part of consultant is implicit in the consultancy services.

1. This clearly establishes that the employees seconded to India make available technical knowledge, experience and skill to the Indian entities and hence is a fee for technical service. As per the discussion above the amount of Rs.50,99,38,561/ is proposed to be taxed as Fees for technical services as per Section 115A of the Act or treaty whichever is beneficial.

1. In view of the above discussion, the assessee’s total income is computed asunder: –

Amount (INR)

Return income declared in ITR – 32,73,620/-Secondment cost taxable as FTS

Under the provision of DTAA – 50,99,38,561

Total Income – 51,32,12,181/-

ITA 423, 424, 715, 753 & 760 of 2025 Page 28 of 80

11. Proposed to be Assessed at Rs.51,32,12,181/-. Necessary forms are being issued with this order. Credit for all pre-paid taxes are to be given after due verification. Charge interest u/s234A,234B,234Cand 234D of the Income Tax Act. Penalty proceedings u/s 270A of the IT Act are to be initiated separately for mis-reporting of income. Necessary forms are being issued with this order. Credit for all pre-paid taxes are to be given after due verification. Charge interest u/s234A,234B, 234C and234 D of the Income Tax Act.

12. Penalty proceedings u/s 270A of the IT Act are to be initiated separately for under-reporting of income.”

49. The question of law (A) that requires examination is concerned with the terms agreed by the assessee and EY India entities which have a bearing on the nature of services undertaken by the secondees. Some of the stipulations in the deputation agreement dated 04.10.2017 have already been quoted in the submissions advanced on behalf of the assessee.

50. We may at this stage refer to the findings of the AO in the assessment order dated 30.05.2023 for AY 2020-21 as available in ITA No.715/2025, concerning services rendered in and from the USA as under:-

“Addition for Receipts from Indian based clients taxable as FTS

xxxx xxxx xxxx

5.15 Engagement letter of such services was examined. It was found that services are clearly in technical as well as consultancy in nature. Scope of such services as mentioned in the agreement is reproduced below:

| 1. Statement of Work

This Statement of Work, dated May 1, 2019 to December 31,2019 (this “SOW”) is made by Ernst & Young LLP (“we” or “EY”) and Infosys Limited (“you” or “Infosys”), to contribute to Infosys implementation of Oracle Utilities Customer Care and Billing(“CC&B”) for Consolidated Edison (“ConEd” or “Client” or ‘ The Company”). EY will provide these services pursuant to the SUBCONTRACTING AGREEMENT , dated April, 30 2019 (the “Agreement”), between EY and Infosys. Infosys is the prime contractor for Client’s Oracle CIS project(“Project”). Client has evaluated alternative systems and selected an approach for meeting its business requirements. Client has selected the Software. EY will contribute with the implementation of the Software as set forth herein. Except as otherwise specifically set forth in this SOW, this SOW incorporates by reference, and is deemed to be a part of, the Agreement. The additional terms and conditions of this SOW shall apply only to the services covered by this SOW (“Services”) and not to services covered under any other SOW pursuant to the Agreement. |

–

| 2. Scope of Services

EY will have responsibility for the oversight and delivery of OCM and training services, in collaboration with the Company designated OCM and Training resources, defined in this scope of work. For non OCM and training services to be performed by EY, EY will be assigned specific tasks and will work under Infosys direction. EY will provide resources for the following terms; a. Project Management b. Organizational Change Management &Training c. Business Workstream focusing on Credit and Collections – Deposits, Cancel/Rebill, Exceptions and Design Workshop Preparation d. Technical Infrastructure e. Data Conversion EY will provide input and feedback on the Infosys -developed Project Plan for the performance of the Services. The Project Plan may be amended by the parties in writing. The Project Plan, once effective, will supersede all prior Project Plans for this SOW. |

5.16 Further, scope of such service also include provision for training to be rendered by EY to the customer. Relevant part of same is reproduced below:

2.Scope of Services

EY will have responsibility for the oversight and delivery of OCM and training services, in collaboration with the Company designated OCM and Training resources, defined in this scope of work.

For non OCM and training services to be performed by EY, EY will be assigned specific tasks and will work under Infosys direction. EY will provide resources for the following terms;

similar clause for training to be rendered by EY employees to end customer is also mentioned in clause 6 of said agreement where clearly role played by EY with regard to same service is elaborated. Relevant part of said agreement is reproduced below:

| EY Personnel | EY Role | Responsibilities |

| Scott Brown | Engagement Partner | -Provide Project with senior leadership and guidance where needed

-Resolve any escalated risks and issues with Infosys stakeholders -Actively participate in project Executive Steering Committee meetings -Escalate relevant program issues and risks to the Executive Steering Committee -Define and communicate overall program vision, plan, dependencies and critical path |

| Prince Schwenck | Data Architect | -Prepare the data conversion plan and strategy in accordance with the Infosys

Data conversion methodology and |

| Umer Malik | Conversion /ODI SMR | -Ensure that all data required by the Product will be available and accurate -Work on the Data Mapping specifications document, and approach

-Work on the data mapping template from source to template and from template to target system -Analyze the existing data structures |

| Bhumit Patel | Data Architect | -Assist with the technical approach for extracting, transforming, and populating data in the target database

-Assist with set up of conversion tools for improving data conversion efficiency i.e. Oracle Data Integrator (ODI) -Assist with the mock conversions to test the conversion process -Assist with go-live data conversion |

| Andrew Hobaugh | Credit and Collections

– Deposits Cancel/ Rebill Exceptions |

-Lead the Functional Workstream for the functional areas assigned by Infosys

-Report workstream progress to Infosys -Confirm that the Client’s operational -Support resolution of functional gaps when mapping business requirements to CC&B -Represent the project with business area -Confirm that the process design supports -Manage execution of unit integration and -Signoff the design, then approve and |

| Steve Verlander | Technical Architect | – Work with the Client to define application and technical requirements

– Assist with the review and integration of all application requirements, including functional, security, integration, performance, quality, and operations requirements – Review and integrate the technical architecture for the development, execution, and production environments – Assist with all decision regarding hardware, network products, system software, and security – Assist with hardware sizing and capacity planning |

| Shwetha Ramakrishnan | Engagement & Readiness Lead | – Responsible for oversight of stakeholder engagement activities – Conduct and coordinate change impact analysis / plans

– Develop Business Readiness Strategy – Develop Change Advisory Council Materials and Deployment – Collaborate with identified business process owners to develop Change Management Metrics Dashboard |

5.17 Thus, it is clear that scope of above said service includes training also. It is well established that rendering training basically provides enduring benefits to recipient and thereby it qualifies Make Available Test. Moreover, scope of above said service clearly is of nature of technical in nature as well as involves consultancy elements also.”

51. The AO came to the conclusion that the scope of the above services includes training and rendering training shall mean providing enduring benefits to the recipient to qualify ‘make available’ test, and as such the payments made are FTS as stipulated in Article 12of the DTAA. We reproduce Article 12 and 15 of the DTAA as under:-

“ARTICLE 12 – Royalties and fees for included services –

1. Royalties and fees for included services arising in a Contracting State and paid to a resident of the other Contracting State may be taxed in that other State.

2. However, such royalties and fees for included services may also be taxed in the Contracting State in which they arise and according to the laws of that State; but if the beneficial owner of the royalties or fees for included services is a resident of the other Contracting State, the tax so charged shall not exceed :

(a) in the case of royalties referred to in sub-paragraph (a) of paragraph 3 and fees for included services as defined in this Article [other than services described in subparagraph of this paragraph] :

(i) during the first five taxable years for which this Convention has effect,

(a) 15 per cent of the gross amount of the royalties or fees for included services as defined in this Article, where the payer of the royalties or fees is the Government of that Contracting State, a political sub-division or a public sector company ; and

(b) 20 per cent of the gross amount of the royalties or fees for included services in all other cases; and

(ii) during the subsequent years, 15 per cent of the gross amount of royalties or fees for included services ; and

(b) in the case of royalties referred to in sub-paragraph (b) of paragraph 3 and fees for included services as defined in this Article that are ancillary and subsidiary to the enjoyment of the property for which payment is received under paragraph 3(b) of this Article, 10 per cent of the gross amount of the royalties or fees for included services.

3. The term “royalties” as used in this Article means : (a) payments of any kind received as a consideration for the use of, or the right to use, any copyright or a literary, artistic, or scientific work, including cinematograph films or work on film, tape or other means of reproduction for use in connection with radio or television broadcasting, any patent, trade mark, design or model, plan, secret formula or process, or for information concerning industrial, commercial or scientific experience, including gains derived from the alienation of any such right or property which are contingent on the productivity, use, or disposition thereof ; and

(b) payments of any kind received as consideration for the use of, or the right to use, any industrial, commercial, or scientific equipment, other than payments derived by an enterprise described in paragraph 1 of Article 8 (Shipping and Air Transport) from activities described in paragraph 2(c) or 3 of Article 8.

4. For purposes of this Article, “fees for included services” means payments of any kind to any person in consideration for the rendering of any technical or consultancy services(including through the provision of services of technical or other personnel) if such services :

(a) are ancillary and subsidiary to the application or enjoyment of the right, property or information for which a payment described in paragraph 3 is received ; or

(b) make available technical knowledge, experience, skill, know-how, or processes, or consist of the development and transfer of a technical plan or technical design.

5. Notwithstanding paragraph 4, “fees for included services” does not include amounts paid :

(a) for services that are ancillary and subsidiary, as well as inextricably and essentially linked, to the sale of property other than a sale described in paragraph 3(a) ;

(b) for services that are ancillary and subsidiary to the rental of ships, aircraft, containers or other equipment used in connection with the operation of ships or aircraft in international traffic ;

(c) for teaching in or by educational institutions;

(d) for services for the personal use of the individual or individuals making the payments; or

(e) to an employee of the person making the payments or to any individual or firm of individuals (other than a company) for professional services as defined in Article 15(Independent Personal Services).

6. The provisions of paragraphs 1 and 2 shall not apply if the beneficial owner of the royalties or fees for included services, being a resident of a Contracting State, carries on business in the other Contracting State, in which the royalties or fees for included services arise, through a permanent establishment situated therein, or performs in that other State independent personal services from a fixed base situated therein, and the royalties or fees for included services are attributable to such permanent establishment or fixed base. In such case the provisions of Article 7 (Business Profits) or Article 15 (Independent Personal Services), as the case may be shall apply.

7. (a) Royalties and fees for included services shall be deemed to arise in a Contracting State when the payer is that State itself, a political sub-division, a local authority, or a resident of that State. Where, however, the person paying the royalties or fees for included services, whether he is a resident of a Contracting State or not, has in a Contracting State a permanent establishment or a fixed base in connection with which the liability to pay the royalties or fees for included services was incurred, and such royalties or fees for included services are borne by such permanent establishment or fixed base, then such royalties or fees for included services shall be deemed to arise in the Contracting State in which the permanent establishment or fixed base is situated.

(b) Where under sub-paragraph (a) royalties or fees for included services do not arise in one of the Contracting States, and the royalties relate to the use of, or the right to use, the right or property, or the fees for included services relate to services performed, in one of the Contracting States, the royalties or fees for included services shall be deemed to arise in that Contracting State.

8. Where, by reason of a special relationship between the payer and the beneficial owner or between both of them and some other person, the amount of the royalties or fees for included services paid exceeds the amount which would have been paid in the absence of such relationship, the provisions of this Article shall apply only to the last-mentioned amount. In such case, the excess part of the payments shall remain taxable according to the laws of each Contracting State, due regard being had to the other provisions of the Convention.

xxx xxx xxx

ARTICLE 15 – INDEPENDENT PERSONAL SERVICES

1. Income derived by a person who is an individual or firm of individuals (other than a company) who is a resident of a Contracting State from the performance in the other Contracting State of professional services or other independent activities of a similar character shall be taxable only in the first mentioned State except in the following circumstances when such income may also be taxed in the other Contracting State :

(a) if such person has a fixed base regularly available to him in the other Contracting State for the purpose of performing his activities; in that case, only so much of the income as is attributable to that fixed base may be taxed in that other State; or

(b) if the person’s stay in the other Contracting State is for a period or periods amounting to or exceeding in the aggregate 90 days in the relevant taxable year.

2. The term “professional services” includes independent scientific, literary, artistic, educational or teaching activities as well as the independent activities of physicians, surgeons, lawyers, engineers, architects, dentists and accountants.”

52. The arguments of Mr. Ganesh can be summed up to mean that the secondees are the employees of the EY India entities; the services offered are neither in the nature of technical nor consultancy; tax has been deducted by the EY India entities on the salary paid to the secondees; and as such the ‘make available’ test is not applicable.

53. The above submissions have been contested by Mr. Rai by drawing our attention to the assessment order as well as the directions of the DRP. As we have already reproduced part of the assessment order, in paragraphs 48 and 50; the relevant portions of the DRP directions dated 19.11.2024 pertaining to AY 2018-19 are reproduced as under:-

“E) In the light of the above judgments and tests laid out by the courts- the facts of the instant case are analyzed.

i) That in addition to the findings of the AO in para 4.2.3 of the DAO, the Panel adds to the facts delineated from the deputation agreement which will establish that the EY US is the de facto controller and employer of the seconded personnel to the EY India.

ii) That the EY US has a right to terminate the assignment of the international assignee (clause 3.7)

iii) During the period of secondment, EY GDS India would be responsible to bear and pay salary and other costs of international assignee but for administrative convenience EY US will make payment towards salary and other cost to international assignee, (clause 4.1)

iv) EY India will reimburse EY US for such payments made towards salary and other cost in relation to the period of secondment (clause 4.1)

v) Pension contribution/approvals, social security contribution and similar payments and related compliance shall be done by EY US. EY India shall reimburse such contributions or accruals to the EY US as part of other cost of international assignee, (clause 6)

vi) EY US is merely releasing its personnel for assignment with EY India and EY US is not acting as provider of manpower supply to EY India (clause 9.2)

vii) EY US agreed not to charge any fees from EY India for assignment of its personnel (clause 9.3)

viii) EY India shall neither solicit nor hire any international assignee for the period of 6 months after the period of assignment without obtaining the prior written consent of EY US (clause 14)

5.5 From the above agreement, read in entirety it transpires that the assessee company EY US is the actual employer of the secondees as not only the alleged salary payment and other costs are paid by it but also the secondees returned to the assessee company after completion of the period of secondment. Further, secondees are always on the roll of the assessee company and for that matter even if they are on a secondment tenure then also they are paid by the assessee company. So, there is no employee employer relationship between the EY India and the secondees. Further, as it is categorically mentioned in the deputation agreement that EY India is engaged in the business of providing consultancy service and needs personnel for facilitating its operations in India for limited period of time and that as the assessee company has those personnel who possess the requisite qualification and experience and who were also agreeable to be assigned to the EY India and that the assessee company EY US had agreed to relieve such personnel for the limited period, it clearly establishes that the assessee’s AE (EY India) wanted those personnels for their technical skills/professional skills to be utilized for their operations. This entails that the EY US has a service PE in India which is engaged in the activity of providing manpower services and the reimbursement is nothing but fee for technical services as rightly held by the AO in the DAO.

5.6 Further, the insertion of clause 9.2, 9.3 which defines the relationship between parties as the assessee company not acting as provider of manpower supply and not charging any fees for assignment of its personnel and has been introduced as an abundant precaution so that the tax incidence on account of provisioning of manpower service and fee for technical service is not invoked in the case. Here it is imperative to state that the language of the contract has been worded by the assessee company to suit its requirement.

5.7 So, this logically entails examining another aspect which is the ‘Doctrine of Substance and Form ‘ which has long guided the tax authorities for interpretation of agreements and forms an important element of jurisprudence. The intent of the terms of Deputation Agreement is crystal clear which is basically to second the employees of the assessee company to its AE in India with a careful usage in the terms of the contract that it should not be treated as manpower supply contract and would not cast any obligation on the AE to pay any technical fees on the same. Here the Panel examines the agreement under the substance over form doctrine. Tax authorities ought to examine the true nature of a transaction, even if it is worded to imply a non-taxable service or FTS payment. It is imperative that tax laws should not be allowed to be circumvented by superficially crafted agreements. The courts have also emphasized that while tax payer’s right to structure their affairs to minimize taxes, they cannot do so in a way that distorts the transaction’s reality. So, putting the pieces of the jigsaw puzzle together and reading the clauses of contract in totality in important. Substance over form is a fundamental concept in tax law, aimed at ensuring that tax liability is based on the actual economic substance of transactions rather than merely their legal or contractual form. Courts and tax authorities have used this principle to prevent tax avoidance schemes structured solely to exploit tax benefits, treating transactions according to their real purpose and substance rather than their labels. Assessee cannot escape the consequences of law merely by describing an agreement in a particular form though in essence and in substance, it may be a different transaction. It is imperative to disregard the labels used in contracts and instead focus on the true economic purpose of the transaction. Here it is abundantly clear that the structure of a transaction was not designed to achieve genuine business purposes but merely to avoid taxes through contractual language.

5.8 Hon’ble SC in the decision of M/s Northern Operating System Pvt Ltd ( NOSPL) [2022- TIOL-48-SC-ST-LB] also intends to drive home the same point. Further, It has been laid out by the Hon’ble Supreme Court in the case of CIT Vs. Panipat Woollen & General Mills Co. Ltd. (SC) 103 ITR 66 that a party cannot escape the consequences of law merely by describing an agreement in a particular form though in essence and in substance, it may be a different transaction. Also, in the case of India – Vodafone International Holdings B.V . v. Union of India (2012) the Hon’ble Supreme Court’s ruling in Vodafone dealt with the application of the substance over form doctrine to cross-border transactions. The Court although ruled in the favour of the assessee but nonetheless emphasized that tax should be levied based on the form in this case because the transaction was between two non-Indian entities. However, it clarified that transactions structured with the sole purpose of tax avoidance could still be subject to taxation if the economic substance indicated an intention to dodge tax. Directions of DRP: