This is Part 1 of a 3 part series on Transitional Provisions.

Overview

The transitional provisions are contained under sections 139 to 142 provided under Central Goods and Services Tax Bill, 2017.

These sections deals with following:

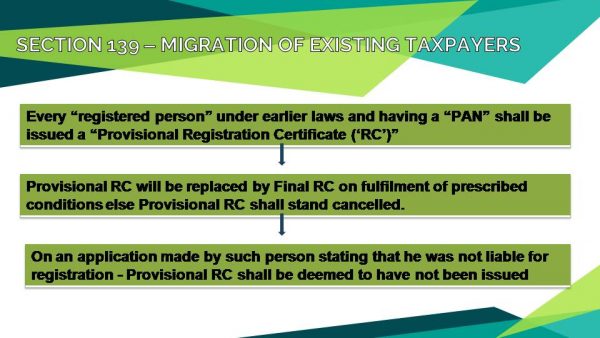

Section 139:- Migration of existing taxpayers.

Section 140:- Transitional arrangements for input tax credit.

Section 141:- Transitional provisions relating to job work-

Section 142:- Miscellaneous transitional provisions

PART A of the series deals with Section 139 only.

Section 140: – The objective of section 140 is to ensure smooth and seamless transition of all the ITC that were available to taxpayers in earlier law.

The provisions of the Section 140 are summarized as below:

140(1) – ITC CARRIED FORWARD IN RETURN

Registered person other than composition taxpayer allowed to take such credit in Electronic Credit Ledger.

However, no credit shall be allowed if –

1. Such credit is inadmissible as ITC in GST Act; or

2. Registered person fails to furnish all the returns of the last 6 months from the appointed day; or

3. Such credit is related to goods manufactured & cleared under exemption notifications

140 (2) – UNAVAILED CENVAT CREDIT ON CAPITAL GOODS

Registered person other than composition taxpayer is allowed to take credit of Unavailed cenvat credit of capital goods, not carried forward in Return, in Electronic Credit Ledger.

However, no credit shall be allowed unless such credit was admissible under Existing laws as well under GST Act.

Unavailed Cenvat Credit on Capital Goods =

Total CENVAT Credit on capital goods allowed

less CENVAT credit on capital goods already availed

![]()

140(3) – Credit Of Eligible Taxes On Inputs Held In Stock – Allowed In Certain Cases

A ‘Registered person’-

a) Who was not liable to be registered under the existing law, or

b) Who was engaged in the manufacture of exempted goods or

c) Providing exempted services, or

d) Who was providing works contract services and was availing benefit under Notification No. 26/ 2012, or

e) A first stage dealer, or

f) A second stage dealer, or

g) A registered importer

h) A depot of a manufacturer

Is Eligible To Take Credits Of Eligible Duties And Taxes On Inputs Contained In –

a) Stock

b) Semi-finished goods

c) Finished goods

Held in stock on appointed day

Eligible Duties and Taxes

a) BED

b) Other Addl Duties

c) CVD

d) SAD

e) Service Tax

Conditions to be fulfilled

1. Such Inputs or Goods are used or intended to be used for making taxable supplies;

2. Eligibility of credit on such inputs under this Act;

3. Possession of invoice/ documentary evidence of duty paid under existing law;

4. Such invoice/ documentary evidence was issued not earlier than 12 months immediately preceding the appointed day;

5. The supplier of services is not eligible for any abatement under the GST law.

PROVIDED that where a registered person, other than a manufacturer or a supplier of services, not in possession of such invoice or any other documents subject to prescribed conditions, be allowed to take credit at the rate and in the manner prescribed.

140(4): CREDIT OF INPUTS HELD IN STOCK IN CERTAIN SITUATIONS

A registered person who was engaged in manufacture of taxable/ exempted goods or providing taxable/ exempted services, but which are liable to tax under current Act shall be entitled to take credit-

a) Cenvat credit c/f in his return [as per sec 140(1)]; and

b) Cenvat credit of eligible duty in respect of inputs-relating to exempted goods or services [as per Sec 140(3)]

140(5): CREDIT OF TAXES IN RESPECT OF INPUT/ INPUT SERVICES DURING TRANSIT

A registered person-

a) shall be entitled to take credit of eligible duties and taxes

b) in respect of inputs/ input services received on or after the appointed day

c) the duty or tax is paid before the appointed day

d) provided the invoice is recorded within 30 days from the appointed day, and

e) a statement is also required be furnished in respect of such credit.

140(6): SWITCHING FROM COMPOSITION SCHEME TO GST

Credit of eligible duties and taxes on inputs held in stock to be allowed to a taxable person switching over from composition scheme

Registered taxable person who was earlier under composition scheme shall be eligible to take credits on:

a) Inputs

b) Semi-finished goods

c) Finished goods

Held in stock on appointed day

Conditions to be fulfilled

1. Inputs/Goods used for making taxable supplies under GST Act;

2. Registered Person is not paying tax under composition scheme of GST Act;

3. Registered Person is Eligible for ITC under GST Act;

4. Possession of invoices;

5. Invoices were issued not earlier than 12 months immediately preceding the appointed day

140(7): ITC ON SERVICES RECEIVED BEFORE THE APPOINTED DATE BY ISD ALLOWED FOR DISTRIBUTION EVEN IF INVOICES ARE RECEIVED LATER ON.

140(8): REGISTERED PERSON HAVING CENTRALISED REGISTRATION UNDER EXISTING LAWS IS ALLOWED TO TAKE CREDIT OF CENVAT CREDIT.

Conditions:-

1. Amount of Cenvat credit shall be amount carried forward in a return furnished for the period ending with day immediately preceding the appointed day.

2. If such return is furnished within 3 months of the appointed day, then credit shall be allowed only if such return is an original or revised return where the credit has been reduced from that claimed earlier.

3. Credit allowed only if admissible under GST Act.

4. Such credit may be transferred to other registered persons having same PAN.

140(9): IF CENVAT CREDIT AVAILED FOR THE INPUT SERVICES PROVIDED UNDER EARLIER LAWS HAS BEEN REVERSED DUE TO NON PAYMENT OF CONSIDERATION WITHIN A PERIOD OF 3 MONTHS, THE SAME CAN BE RECLAIMED PROVIDED THE REGISTERED PERSON HAS PAID THE CONSIDERATION WITHIN 3 MONTHS FROM THE APPOINTED DATE.

Author Bio