Ayush Gupta

1. FORM GSTR-1 (within 10 days of the month following the month of supply):

- Details of Outward Supplies (Section 25 of the Draft Model GST Law).

- Every taxable person other than person registered under section 8, those paying tax under section 37 and Input service distributor.

- The recipient shall file his Inward details in FORM GSTR-2 (under section 26) or modified details in FORM GSTR-4 (under section 27), all such details shall be provided to the supplier for cross verification in FORM GSTR-1A, the supplier may accept or reject the modification made by the recipient and FORM GSTR-1 furnished by the supplier shall stand amended to the extent of modifications accepted by him.

- Any registered taxable person, who has furnished FORM GSTR-2 for any tax period and which have remained unmatched under section 29, can, upon discovery of any error or omission therein, rectify such error or omission in the tax period during which such error or omission is noticed and pay the tax and interest, if any, in case there is a short payment of tax on account of such error or omission, in FORM GSTR-2 to be furnished for such tax period.

- Provided that no rectification of error or omission in respect of the details furnished in FORM GSTR-1, shall be allowed:

– after filing of the return under section 27 for the month of September following the end of the financial year to which such details pertain, or

– filing of the relevant annual return,

whichever is earlier.

2. FORM GSTR-2 (within 15 days of the month following the month in which inward supply is received):

- Details of Inward Supplies (Section 26 of the Draft Model GST Law).

- Every taxable person other than Input Service distributor and person registered under section 8 (composition scheme). [as per Report of Empowered Committee of State Finance Ministers on GST Returns]

- Every taxable person as per Model GST Law.

- Details of all the credit is to be given whether on inward supplies, services from Input service distributor, where tax has been deducted under section 37 or where tax has been collected under section 43C.

- The details of all the suppliers, ISD, TDS, TCS shall be made available to the receiver of the service through the common portal in the following forms:

| S. No. | Particulars | Form in which it shall be made available to the taxable person providing details of inward supplies. |

| 1. | Details of Outward supplies furnished by provider in FORM GSTR-1 | PART A of FORM GSTR-2A |

| 2. | Details of Invoices furnished by Input Service Distributor in FORM GSTR-6 | PART B of FORM GSTR-2A |

| 3. | Details of Tax Deducted at source under section 37 furnished in FORM GSTR-7 | PART C of FORM GSTR-2A |

| 4. | Details of Tax Collected at source under section 43C furnished in FORM GSTR-8 | PART D of FORM GSTR-2A |

- The taxable person (recipient) can modify the details as per section 26(1) of the Model GST Law (only in case of outward supplies).

- Any registered taxable person, who has furnished FORM GSTR-2 for any tax period and which have remained unmatched under section 29, can, upon discovery of any error or omission therein, rectify such error or omission in the tax period during which such error or omission is noticed and pay the tax and interest, if any, in case there is a short payment of tax on account of such error or omission, in FORM GSTR-2 to be furnished for such tax period.

- Provided that no rectification of error or omission in respect of the details furnished in FORM GSTR-2, shall be allowed:

– after filing of the return under section 27 for the month of September following the end of the financial year to which such details pertain, or

– filing of the relevant annual return,

whichever is earlier.

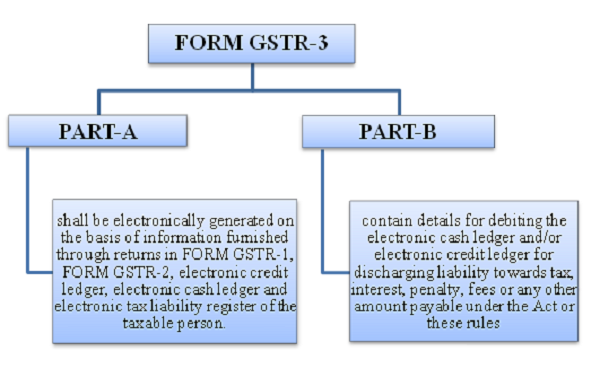

3. FORM GSTR-3 (within 20 days of the month following the month in which supply is made):

- Final details of both inward and outward supplies.

- Every taxable person other than person registered under section 8, those paying tax under section 37 and Input service distributor.

- The taxable person can claim refund of any balance outstanding in the electronic cash ledger as per section 35(6) of the act.

- Where the time limit for furnishing FORM GSTR-1 under sub-section (1) of section 25 and FORM GSTR-2 under sub-section (2) of section 26 has been extended, return in FORM GSTR-3 may be furnished in such manner as may be notified by the Commissioner/Board.

4. FORM GSTR-4 (within 18 days of the month following the Quarter in which supply is made):

- The details of inward supplies used by the recipient registered under section 8 i.e. composition scheme shall be given to the recipient itself in FORM GSTR 4A on the basis of details provided by the supplier in FORM GSTR- 1.

- A taxable person paying tax under the composition scheme, shall, after adding, correcting or deleting the details contained in FORM GSTR-4A, furnish a quarterly return in FORM GSTR-4.

- The taxable person shall, pay tax, interest, penalty, fees by debiting the electronic cash ledger.

5. FORM GSTR-5:

- A registered non-resident taxable person shall furnish a return in FORM GSTR-5 providing the details of outward supplies and inward supplies and shall pay the tax, interest, penalty, fees.

- Within twenty days:

–after the end of a tax period or

-within seven days after the last day of the validity period of registration,

whichever is earlier

- Tax period shall be taken as a month. [as per Report of Empowered Committee of State Finance Ministers on GST Returns]

6. FORM GSTR-6: (within 13 days of the month following the month in which supply is made):

- The details of inward supplies used by the input service distributor shall be given to the recipient itself in FORM GSTR 6A on the basis of details provided by the supplier in FORM GSTR- 1.

- A registered input service distributor shall, after adding, correcting or deleting the details contained in FORM GSTR-6A, furnish a return in FORM GSTR-6, containing the details of tax invoices on which credit has been received and those issued under section 17.

7. FORM GSTR-7: (within 10 days of the month following the month in which supply is made):

- Every registered taxable person required to deduct tax at source under section 37 shall furnish a return in FORM GSTR-7.

- The details given by the deductor (recipient) shall be given to the supplier itself in PART C of FORM GSTR 2A on the basis of details provided by the deductor under section 37 in FORM GSTR- 7.

- The certificate referred to in sub-section (3) of section 37 shall be made available electronically to the deductee on the Common Portal in FORM GSTR-7A on the basis of FORM GSTR- 7 filed by the deductor.

8. FORM GSTR-8: (within 10 days of the month following the month in which tax is collected):

- Every e-commerce operator required to collect tax at source under section 43C shall furnish a statement in FORM GSTR-8, containing details of supplies effected through such operator and the amount of tax collected.

- The details furnished by the operator, shall be made available electronically to each of the suppliers in Part D of FORM GSTR-2A.

9. FORM GSTR-9 (on or before the thirty first day of December following the end of financial year):

- Every registered taxable person (other than input service distributor, a deductor under section 37, a casual taxable person and a non-resident taxable person), shall furnish an annual return under section 30 electronically in FORM GSTR-9.

FORM GSTR-9A:

- A taxable person paying tax under section 8 shall file the annual return in FORM GSTR-9A.

FORM GSTR-9B:

- Every registered taxable person whose aggregate turnover during a financial year exceeds one crore rupees shall get his accounts audited under sub-section (4) of section 42 and he shall furnish a copy of audited annual accounts and a reconciliation statement [section 30(2)], duly certified, in FORM GSTR-9B.

10. FORM GSTR-10 (within three months of the date of cancellation or date of cancellation order, whichever is later)

- Every registered taxable person required to furnish a final return under section 31, shall furnish such return electronically in FORM GSTR-10.

11. FORM GSTR-11 (Tax period not yet known)

- Every person, who has been issued a Unique Identity Number and claims refund of the taxes paid on his inward supplies, shall furnish the details of such supplies of taxable goods and/or services in FORM GSTR-11.

- For persons, who have been issued a Unique Identity Number for purposes other than refund of the taxes paid, shall furnish the details of inward supplies of taxable goods and/or services as may be required by the proper officer in FORM GSTR-11.