Articles by this Author

Income Tax

Income Tax

TDS / TCS Rates effective from 01st April 2025

Goods and Services Tax

Goods and Services Tax

GSTR 9C reconciliation now available and due date is 31.12.2021

Income Tax

Income Tax

Income tax TDS & TCS rates effective from 01st April 2021

Goods and Services Tax

Goods and Services Tax

Recent GST changes Impacting your business wef from 01.01.2021

Goods and Services Tax

Goods and Services Tax

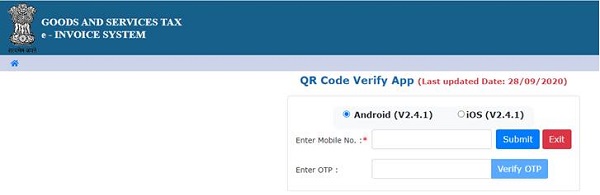

How to easily verify the E- invoice QR in your mobile

Income Tax

Income Tax

Income Tax TCS on sale of goods from 01st Oct 2020 with FAQ

Income Tax

Income Tax

Income tax TCS provisions applicable from 01st Oct 2020

Goods and Services Tax

Goods and Services Tax