Case Law Details

Pankaj Jhumarmal Bothra Vs ITO (ITAT Ahmedabad)

The Income Tax Appellate Tribunal (ITAT) allowed all four appeals filed by the assessee, holding that the Assessing Officer (AO) was not justified in treating credits appearing in the assessee’s personal HDFC savings bank account as undisclosed business turnover or in rejecting the books of account under Section 145(3) of the Income-tax Act.

The assessee, an individual carrying on business through two proprietary concerns, had declared a turnover of ₹9.61 crore and filed a return showing income of ₹9.50 lakh. During scrutiny assessment, the AO noticed credits of ₹2.64 crore in the assessee’s personal HDFC bank account, which was not reflected in the books of the proprietary concerns. Treating the entire credits as suppressed business turnover, the AO enhanced the turnover to ₹12.25 crore, rejected the books of account under Section 145(3), and estimated profit at 8% of the enhanced turnover, resulting in an assessed income of ₹98.06 lakh. The AO also imposed penalties under Sections 271A, 271B, and 272A(1)(d), which were upheld by the Commissioner (Appeals).

Before the Tribunal, the assessee contended that the HDFC account was a disclosed personal savings account and that the credits mainly consisted of internal transfers from proprietary concerns, family members, HUF, share broker receipts already offered to tax, rent income, dividend income, agricultural land sale, insurance receipts, reimbursements, and other non-business receipts. It was further argued that the declared turnover was fully supported by GST returns and TIS data and that no defects had been found in the books of account.

The Tribunal observed that the personal savings account had been disclosed in the return of income and that the assessee had furnished a detailed break-up of the credits. It held that the Revenue had failed to establish any direct nexus between the bank credits and business transactions. According to the Tribunal, mere credits in a personal savings account cannot automatically be treated as undisclosed business turnover without supporting material.

The Tribunal further noted that none of the impugned receipts represented business turnover. It also found that the declared turnover was supported by GST returns and TIS data and that the AO had not identified any specific defect in the books of account, quantitative records, purchases, sales, stock records, or supporting vouchers. It held that rejection of books merely on suspicion or on the basis of a low profit rate, without pointing out specific defects or incompleteness, was not sustainable.

Accordingly, the Tribunal held that invocation of Section 145(3) and estimation of profit at 8% on the enhanced turnover were unjustified and directed deletion of the addition.

Since the quantum addition was deleted, the Tribunal held that the basis for penalties under Sections 271A and 271B no longer survived and directed their deletion. It also deleted the penalty under Section 272A(1)(d), observing that although there was some delay in complying with statutory notices, the assessee had subsequently furnished the required details and had explained that the delay was caused by health issues and the time required to compile information. The Tribunal accepted this as a reasonable cause and allowed all the appeals.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

These four appeals filed by the assessee are directed against the separate orders, all dated 20.011.2025, passed by the Ld. Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (NFAC), Delhi (hereinafter referred to as ‘Ld. CIT (A)’ in short), under Section 250 of the Income-tax Act, 1961 (hereinafter referred to as ‘the Act’ in short), arising out of assessment order u/s 144 r.w.s. 144B of the Act dated 15.03.2024 and penalty orders u/s 271A, 271B dated 06.08.2024 and u/s 272A(1)(d) of the Act dated 31.07.2024, all for A.Y. 2022-23.

2. Since common facts and interconnected issues are involved in all the appeals, the same were heard together and are being disposed of by way of this consolidated order for the sake of convenience and brevity.

3. Briefly stated, the facts of the case are that the assessee, an individual engaged in business through proprietary concerns namely Pranav Enterprise and Dexxon Polycoating Enterprise, filed return of income declaring total income of Rs. 9,50,460/- and total turnover of Rs. 9,61,71,289/-. The case was selected for scrutiny under CASS and assessment was completed u/s 144 r.w.s. 144B of the Act on 15.03.2024. During the course of assessment proceedings, the Assessing Officer noticed credits aggregating to Rs. 2,64,06,767/- in HDFC Bank Account No. 18601530009580 held in the personal name of the assessee. Since the said bank account was not reflected in the books of accounts of the proprietary concerns, the Assessing Officer treated the entire credits as suppressed business turnover and enhanced the turnover from Rs. 9,61,71,289/- to Rs. 12,25,78,056/-. The Assessing Officer, thereafter, rejected the books of account u/s 145(3) of the Act and estimated profit @ 8% of the enhanced turnover, resulting in assessed income of Rs. 98,06,244/-.

4. Consequent thereto, the Assessing Officer also levied penalties u/s 271A and 271B of the Act for alleged failure to maintain and audit books of accounts and further levied penalty u/s 272A(1)(d) of the Act for non-compliance with statutory notices.

5. Aggrieved by the order of the Assessing Officer, the assessee carried the matter in appeal before the Ld. CIT(A), who upheld the action of the Assessing Officer both in quantum and penalty proceedings.

6. Aggrieved by the order of the Ld. CIT(A), the assessee has filed the present four appeals before the Tribunal.

ITA No. 422/Ahd/2026 (Quantum Appeal)

7. In quantum appeal, i.e. in ITA No. 422/Ahd/2026, the assessee has raised following grounds:-

“2. The Ld. CIT(A) has erred in upholding the action of the Ld. AO in considering Rs. 2,64,06,767/- as additional turnover from the personal bank account with HDFC Bank, failing to distinguish between personal and business transactions. The majority of these transactions were internal transfers from the Appellant’s proprietary concerns and family members, which do not constitute business income.

3. The Ld. CIT(A) erred in upholding the action of Ld. AO by rejecting the books of Assessee u/s 145(3) of the Act without there being any defects as to incorrectness or incompleteness of the accounts of the assessee and consequently making addition of Rs 98,06,244/- being 8% of Rs.12,25,78,056/- which comprises of the recorded turnover of Rs.9,61,71,289 and erroneously and arbitrarily increased turnover of Rs.2,64,06,767/- by the Ld. AO.”

8. Before us, the Ld. AR submitted that the HDFC bank account was a personal savings account duly disclosed in the return of income. The credits therein did not represent business turnover but consisted of internal transfers from proprietary concerns, family members, HUF, and other non-business receipts such as rent, agriculture income, dividend, interest, insurance receipts and reimbursement entries. The Ld. AR also submitted that the declared turnover of Rs. 9.61 crores is duly supported by GST returns and TIS data and no discrepancy has been found in regularly maintained books of accounts. The Ld. AR contended that the Assessing Officer has not pointed out any specific defect in books of accounts and, therefore, rejection u/s 145(3) is unjustified. Estimation of income at 8% on inflated turnover is arbitrary.

9. The Ld. DR, on the other hand, supported the orders of lower authorities and submitted that the assessee failed to include substantial receipts of Rs. 2.64 crores in its books of accounts. The Ld. DR submiited that the Assessing Officer rightly treated the same as business turnover since the assessee failed to substantiate the nature of credits with proper evidence. The Ld. DR submitted that rejection of books u/s 145(3) and estimation of profit is justified in absence of complete and reliable books.

10. We have considered rival submissions and perused material available on record.

10.1 The core issue for our consideration is whether the credits of Rs. 2,64,06,767/- appearing in the personal HDFC savings bank account of the assessee can be treated as undisclosed business turnover and whether rejection of books u/s 145(3) followed by estimation of profit @ 8% is justified.

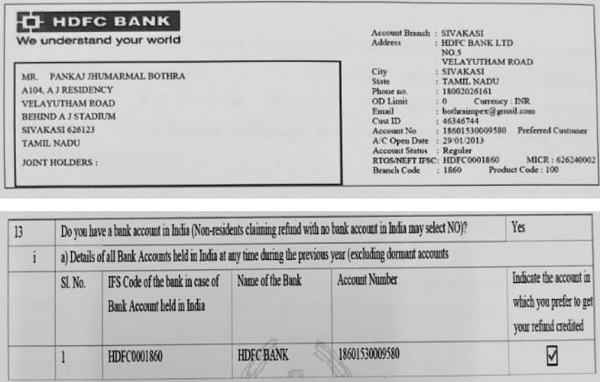

10.2 The details of the aforesaid bank account are set out hereinbelow. It is pertinent to note that the said account was duly disclosed in the return of income as well as in the statement furnished before the Assessing Officer:-

From the above, it is undisputed that the said account is a personal savings account and was disclosed in the return of income. The assessee has furnished a detailed bifurcation of credits showing that substantial amounts represent internal transfers between proprietary concerns, family members, HUF and other non-business receipts such as rent, agriculture income, dividend, interest and insurance receipts. The details as furnished before us by the assessee are as under:-

| Nature of Receipt in bank | Total amount credited in Bank Account (Rs.) |

| Internal Transfers from assessee’s proprietorship firm | 1,34,74,362 |

| Internal transfer from Family | 77,89,111 |

| Internal Transfer from HUF of Assessee | 20,23,747 |

| Receipt from Share Broker (Already offered in ITR) | 11,12,056 |

| Agriculture Land Sale (Not taxable) | 7,37,000 |

| Rent Income (already offered in ITR) | 4,92,892 |

| Internal Transfer from Friends | 4,00,000 |

| Receipt from term insurance | 2,29,914 |

| Misc. receipts / reimbursement for personal use | 1,30,970 |

| Cash Deposit | 12,500 |

| Dividend Income (Already offered in ITR) | 2,220 |

| Internal from bank (Already offered in ITR) | 1,488 |

| Receipt from National Pension Scheme (Not taxable) | 509 |

| Grand Total | 2,64,06,768 |

10.3 We find merit in the contention of the assessee that mere existence of credits in a personal savings account cannot automatically lead to the inference that the same constitute undisclosed business turnover unless the Revenue establishes a direct nexus between such credits and business transactions. Except for drawing a presumption on the basis of bank credits, no material has been brought on record by the Assessing Officer to demonstrate that the impugned receipts represented unaccounted sales or business receipts.

10.4 None of the amounts mentioned above of Rs.2,64,06,768/- can be considered as the amounts received in relation to the business activity or the turnover. We further note that the turnover declared by the assessee is duly supported by GST returns and TIS data and no discrepancy has been pointed out therein. The Assessing Officer has also failed to identify any specific defect in the books of accounts maintained by the assessee. No discrepancy in quantitative details, purchases, sales, stock records or supporting vouchers has been brought on record. Rejection of books merely on the basis of suspicion or low profit rate, without pointing out any specific defect or incompleteness, is not sustainable in law.

10.5 In view of the above, the Assessing Officer was not justified in invoking Section 145(3) of the Act and consequently estimating profit @ 8% on the alleged enhanced turnover of Rs. 12,25,78,056/-. Accordingly, the addition sustained by the Ld. CIT(A) is directed to be deleted.

Accordingly, the quantum appeal of the assessee is allowed.

ITA No. 423/Ahd/2026 (Penalty u/s 271A)

ITA No. 424/Ahd/2026 (Penalty u/s 271B)

ITA No. 425/Ahd/2026 (Penalty u/s 272A(1)(d))

11. We have heard rival submissions and perused the material available on record on this issue. Since, while adjudicating the quantum appeal in ITA No. 422/Ahd/2026 hereinabove, we have held that the Assessing Officer was not justified in rejecting the books of accounts u/s 145(3) of the Act and in treating the impugned bank credits as undisclosed business turnover, the very foundation for levy of penalties u/s 271A and 271B of the Act does not survive. Accordingly, the penalties levied u/s 271A and 271B are directed to be deleted.

11.1 As regards penalty levied u/s 272A(1)(d) of the Act, it is noticed that though there was some delay in compliance with the statutory notices, the assessee subsequently furnished the requisite details during the course of assessment proceedings. The assessee has also explained that the delay occurred due to health issues and time consumed in compilation of details. Considering the entirety of facts and circumstances of the case, we are satisfied that the assessee was prevented by reasonable cause; accordingly, the penalty levied u/s 272A(1)(d) is also directed to be deleted.

Accordingly, all penalty appeals filed by the assessee are allowed.

12. In the result, all the appeals filed by the assessee are allowed.

Order pronounced in the open Court on 23.06.2026

Author Bio