Case Law Details

Balajee Loha Private Limited Vs ACIT (ITAT Raipur)

The Income Tax Appellate Tribunal (ITAT), Raipur, dismissed the assessee’s appeal for Assessment Year 2018-19 and upheld the order of the Commissioner of Income Tax (Appeals) [CIT(A)] sustaining a disallowance of 12.5% of purchases treated as bogus.

The assessee, engaged in the business of manufacturing and trading steel products, filed its return of income declaring income of Rs.7,13,26,490. The return was initially processed under Section 143(1), wherein employees’ contribution to PF and ESIC paid beyond the prescribed due dates was disallowed. Subsequently, the assessment was reopened under Section 148 on the basis of information that the assessee had allegedly made bogus purchases of Rs.44,92,645 from M/s Mideast Integrated Steels Limited. During the reassessment proceedings, the Assessing Officer (AO) called upon the assessee to establish the genuineness of these purchases.

The assessee furnished a reply, but the AO found it unsatisfactory. The AO noted that the supplier had not complied with the notice issued under Section 133(6), the assessee had not furnished input-output analysis demonstrating consumption of raw material, GSTR-2A, delivery acknowledgements, transport details, signed purchase bills or evidence of physical movement of goods. The AO also relied upon information received from the Investigation Wing stating that the supplier was engaged in paper transactions without actual movement of goods. Referring to the Supreme Court’s observations in State of Karnataka v. Ecom Gill Coffee Trading Pvt. Ltd., the AO held that invoices and cheque payments alone were insufficient to establish genuine movement of goods and disallowed 25% of the purchases under Section 37(1), treating it as the estimated profit from fictitious purchases.

Before the CIT(A), the assessee produced additional evidence comprising copies of purchase invoices, delivery challans/gate passes, GSTR-2A reflecting corresponding input tax credit, and ledger accounts along with payment details through banking channels. The CIT(A) admitted these documents and observed that judicial precedents have consistently held that where purchases are supported by books of account, invoices and banking transactions, the entire purchases cannot be treated as bogus merely because the supplier is alleged to be a hawala dealer. The CIT(A) further observed that the corresponding sales had not been found to be non-genuine and that the AO’s estimation of 25% was excessive. Relying upon judicial precedents, the CIT(A) restricted the disallowance to 12.5% of the disputed purchases, amounting to Rs.5,61,581, and deleted the balance addition.

Before the Tribunal, the Revenue argued that the assessee had still failed to produce evidence such as transport details to establish the actual physical movement of goods. It was submitted that the assessee had not demonstrated actual transportation or delivery of the goods and that the relief granted by the CIT(A) was not justified. The Revenue also requested that any finding in the assessee’s appeal should not affect its separate cross-appeal.

After examining the record, the Tribunal noted that the additional evidence produced before the CIT(A) consisted only of purchase invoices, delivery challans or gate passes, GSTR-2A and ledger accounts with banking details. It held that none of these documents established the actual physical movement of goods from the supplier’s premises to the assessee’s factory. The Tribunal also observed that the assessee had not produced any input-output analysis before the AO to establish actual consumption of the goods in the manufacturing process. Since the essential evidence relating to transportation and consumption of the goods had not been produced before the authorities below, the Tribunal found no infirmity in the CIT(A)’s decision sustaining the disallowance at 12.5% of the purchases. The Tribunal clarified that its findings would not have any bearing on the Revenue’s separate cross-appeal. Accordingly, the assessee’s appeal was dismissed.

FULL TEXT OF THE ORDER OF ITAT RAIPUR

This appeal for Assessment Year (‘AY’) 2018-19 filed by the assessee is directed against the order dated 07.11.2025 of Commissioner of Income Tax (Appeals), [CIT(A)], National Faceless Appeal Centre (NFAC), Delhi, passed under section 250 of the Income Tax Act, 1961 (Act).

2. In nutshell, the assessee, vide three grounds of appeal, has challenged the disallowance of bogus purchases of Rs.5,61,580/- upheld by the Ld. CIT(A).

3. Facts, in brief, relevant for adjudication of this appeal are that the assessee is engaged in the business of manufacturing and trading of steel products. It filed its Income Tax Return (‘ITR’) of the relevant year on 26.03.2019 declaring income of Rs.7,13,26,490/-. The ITR was processed under section 143(1) of the Act at income of Rs.7,19,40,170/- wherein the employee’s contribution towards PF and ESIC paid after due date specified in the said Act was disallowed by the Assessing Officer (‘AO’) – CPC. Later, this case was reopened under section 148 of the Act on the reasoning that the assessee has taken bogus purchases of Rs.44,92,645/- from M/s Midest Integrated Steels Limited. During the course of reopened assessment proceedings, the Ld. AO show-caused the assessee to explain the genuineness of purchases of Rs.44,92,645/- from Midest Integrated Steels Limited done during the relevant year. In response to said show cause notice, the assessee filed its submission dated 10.03.2023, which is duly scanned at page Nos. 6 and 7 of the assessment order. Dissatisfied with the submissions of the assessee, the Ld. AO observing as under disallowed 25% of purchases of Rs.44,92,645/- made from Midest Integrated Steels Limited:

“4.4 Point-wise rebuttal of reply of the assessee including analysis of any case law relied upon.

- The Information called u/s 133(6) from the M/s. Mideast Integrated Steel Ltd. by this office has not being complied till date.

- The assessee has submitted documents which cannot be relied upon as there is no Input/output analysis submitted so evidence that the raw material has been consumed in finished goods.

- The documents submitted are self serving in nature between the parties who have entered into collusive transaction hence the paper work are mostly kept prepared.

- There is information available with the department which has been shared with assessee and as per the same there is finding given that M/s. Mideast Integrated Steel Ltd. has indulged in purchase and sale only on paper without actual movement of goods.

- The assessee has not submitted GSTR-2A which is auto populated to evidence that the transactions are reported in GST.

- The assesse has not given proof of delivery slips/gate pass to evidence the actual movement of goods.

- Assessee has not submitted copy of purchase bill duly signed and stamped by the said party.

- The assessee has not submitted any transport details or any other details pertaining to movement and delivery of goods.

There is information received from ITO(INV) (OSD2) (Unit2), Delhi which has been shared with assessee and as per the same there is finding given that above entities have indulged in purchase and sale only on paper without actual movement of goods. The information is reproduced as below:-

……………………………..

…………………………..

- Recently, Hon’ble Supreme Court in TS-99-SC-2023-VAT has held that for claiming and the aforesaid can be proved only by furnishing the name and address of the selling dealer, details of the vehicle which has delivered the goods, payment of freight charges, acknowledgement of taking delivery of goods, tax Invoices and payment particulars etc. SC clarifies that “mere production of the lonvoices and/or payment by cheque is not sufficient and cannot be said to be proving the burden as per section 70..” since tax invoice as per rule 27 and rule 29 cannot be proving the actual physical movement of the goods. However, SC adds that while the tax invoice and cheque can be said to be proving one of the documents, it is not sufficient to prove genuineness transaction and on this lines, SC categorically mentions that aforesaid information regarding actual physical movement of the goods would be in addition to tax invoices. particulars of payment etc.: SC In this case the acknowledgement of taking delivery of goods has not been furnished by the assessee.

- In view of the above facts and circumstances of the case, the fictitious purchase transactions, the profit earned from the value of bogus purchases is fairly estimated at 25% of the bogus purchases and accordingly 25% of the entire fictitious purchases are disallowed u/s 37(1) as the same is not incurred for the purposes of the business.”

4. Aggrieved with the assessment order, the assessee filed appeal before the Ld. CIT(A). The Ld. CIT(A) admitting additional evidences, such as, (i) Copy of purchase invoices from M/s Mideast Integrated Steels Ltd., (ii) Delivery challans / gate passes, (iii) GSTR-2A reflecting corresponding input tax credit and (iv) Ledger and payment details through banking channel, restricted the disallowance @ 12.5% of purchases of Rs.44,92,645/- instead of @ 25% done by the Ld. AO. The relevant part of the impugned order reads as under:

“7.3 Legal Position: Courts have consistently held that when purchases are supported by books, invoices, and payment through banking channels, merely because the supplier is found to be a “hawala” dealer. the entire purchases cannot be treated as bogus. At best, profit element can be estimated to cover possible inflation or non-genuine component.

- CIT vs. Nikunj Eximp Enterprises Pvt. Ltd. (2013) 35 taxmann.com 384 (Bom)

- PCIT vs. Paramshakti Distributors Pvt. Ltd. (ITAT Kolkata)

- CIT vs. Simit P. Sheth (2013) 356 ITR 451 (Guj.)

- However, the profit rate of 25% adopted by AO is arbitrary and excessive. In similar cases, Hon’ble Gujarat High Court in Simit P. Sheth (supra) and Bholanath Polyfab Pvt. Ltd. (355 ITR 290) restricted disallowance to 12.5% of such purchases to meet ends of justice.

Considering the nature of business (steel trading with moderate margins), the supporting evidence produced, and absence of any finding that the corresponding sales are bogus, the disallowance of 25% is found to be unreasonably high. A fair estimation of profit embedded in such purchases is 12.5%. Accordingly, the disallowance is restricted to 12.5% of Rs. 44,92,645/- Rs. 5,61,581/-. Balance addition of Rs. 5,61,579/-is deleted.”

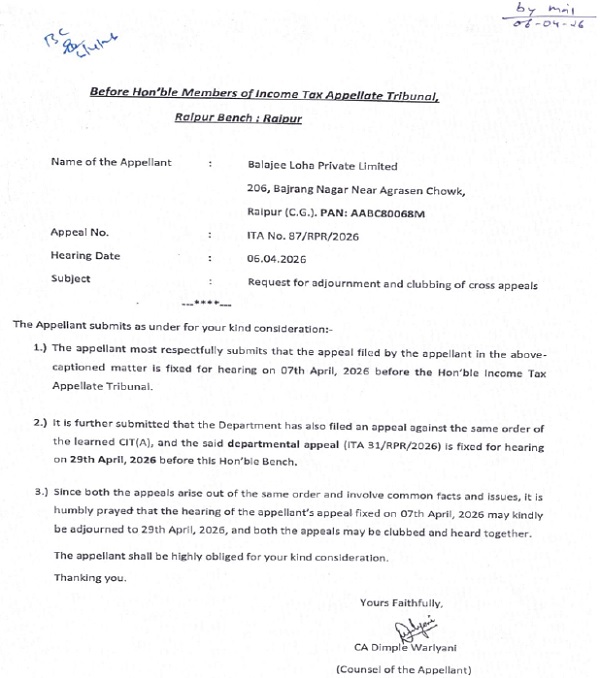

5. Before us, a petition for consolidation of Revenue’s appeal and assessee’s appeal was filed by the Ld. Authorized Representative of the assessee, which is reproduced hereunder:

6. None attended on behalf of the assessee. So we heard Dr. Priyanka Patel, Ld. Sr. DR, who argued the case vehemently. She submitted that the assessee had failed to produce the truck details etc. through which the goods were actually transported at the factory premises of the assessee. She drew our attention to the case law mentioned at page No. 11 of the assessment order in the case of State of Karnataka Vs. Ecom Gill Coffee Trading Pvt. Ltd.; SLP (Civil) 2572/2022 [TS-99-SC-2023-VAT], wherein the Hon’ble Supreme Court clarified that mere production of vouchers or payment by cheque were not sufficient and could not be said to be proving burden as per section 70 of the KVAT Act. She categorically submitted that the assessee had failed to demonstrate the actual physical movement of goods through any corroboratory evidence even during the appellate proceedings before the Ld. CIT(A). However, the Ld. CIT(A) deleted 50% of the disallowance made by the Ld. AO. She contended that the Ld. CIT(A), in principle, admitted the bogus purchases; therefore, he following the decisions of Hon’ble Gujrat High Court in the cases of Smith P Seth 356 ITR 451 and Bholanath Polyfab Pvt. Ltd. 355 ITR 290, sustained the disallowance @ 12.50% of bogus purchases. She submitted that the relief allowed by the Ld. CIT(A), keeping in view the finding of Hon’ble Supreme Court in the case of N. K. Protein reported in 250 Taxman 22 (SC), was not justified. She therefore, prayed for dismissal of this appeal. However, she showed her concern that any finding in this case should not have any direct/indirect bearing in the cross-appeal filed by Revenue which would be heard later.

7. We have heard Ld. Sr. DR and have perused the materials available on the record. We have taken note of the fact that the assessee has produced only following four evidence/documents as additional evidences during the appellate proceedings before the Ld. CIT(A):

(i) Copy of purchase invoices from M/s Mideast Integrated Steels Ltd.,

(ii) Delivery challans / gate passes,

(iii) GSTR-2A reflecting corresponding input tax credit and

(iv) Ledger and payment details through banking channel.

None of these evidence establishes the actual physical movement of goods from the premises of Modest Integrated Steels Limited to the assessee’s premises. Further, we have also taken note of the fact that the assessee has not filed any document before the Ld. AO, which may demonstrate input or output analyses establishing the actual consumption of the said goods in the production. Since, the core document regarding the transportation of goods and consumption of goods in the production were not filed before the Authorities below; therefore, we do not find any infirmity in the order of the Ld. CIT(A) as far as upholding the disallowance @ 12.5% of bogus purchases are concerned. Accordingly, this appeal is dismissed. Before parting out, we make it clear that the above finding will not have any bearing on the Revenue’s cross-appeal.

8. In the result, this appeal of assessee is dismissed

Order pronounced in the open court on 18/06/2026.

Author Bio