Case Law Details

ACIT Vs Indeed Fincap Pvt. Ltd. (ITAT Delhi)

The Income Tax Appellate Tribunal (ITAT), Delhi, dismissed the Revenue’s appeal and upheld the order of the Commissioner of Income Tax (Appeals), which had quashed the assessment made under Section 153C of the Income-tax Act for Assessment Year 2014-15. The Revenue had challenged the deletion of additions of ₹29 lakh under Section 68 and ₹4.40 crore under Section 69A, as well as the finding that the assumption of jurisdiction under Section 153C was invalid.

The Revenue contended that a search conducted on the SMC Global Securities group led to the seizure of digital evidence, including emails and Excel sheets, allegedly showing unaccounted cash transactions involving the assessee. It argued that the Assessing Officer had validly recorded a consolidated satisfaction note covering multiple assessment years because the seized material related to several years, and that the additions were supported by incriminating digital evidence corroborated by bank transactions.

The assessee challenged the validity of the proceedings, contending that the jurisdiction under Section 153C was assumed on the basis of a consolidated satisfaction note for seven assessment years without any year-wise analysis of the seized material or year-specific satisfaction demonstrating how the material affected the determination of income for the relevant assessment year. It also argued that the proceedings were barred by limitation.

The Tribunal observed that recording a valid satisfaction note is a mandatory condition precedent for invoking jurisdiction under Section 153C. It held that such satisfaction must be specific, based on cogent material, identify the seized material pertaining to the assessee, and clearly establish its bearing on the determination of total income for the relevant assessment year. The Tribunal emphasized that the Assessing Officer is required to identify the incriminating material separately for each assessment year before assuming jurisdiction.

On examining the satisfaction note, the Tribunal found that it was a common satisfaction note covering multiple assessment years without identifying any specific incriminating material relating to each year. It contained no reference to documents demonstrating undisclosed income for the relevant assessment year, no quantification or prima facie analysis of alleged undisclosed income, and appeared to have been recorded mechanically. The Tribunal held that such a generalized and omnibus satisfaction reflected non-application of mind and failed to satisfy the statutory requirements of Section 153C.

The Tribunal relied on the Supreme Court’s decision in CIT v. Sinhgad Technical Education Society and the Delhi High Court’s decision in Saksham Commodities Ltd. v. ITO, which require the existence of incriminating material relatable to each assessment year for valid assumption of jurisdiction under Section 153C. It also referred to several coordinate bench decisions supporting the same principle.

The Tribunal further observed that the material relied upon by the Assessing Officer was a third-party ledger that was neither corroborated by independent evidence nor supported by any meaningful enquiry. It found no material establishing a nexus between the seized documents and any undisclosed income of the assessee. It also noted that the transactions in question were duly recorded in the assessee’s books of account. Since the assessment for the relevant year was an unabated assessment, the absence of a valid, year-specific satisfaction note rendered the assumption of jurisdiction under Section 153C invalid.

Accordingly, the Tribunal held that the notice issued under Section 153C and the consequential assessment order were unsustainable in law and quashed them. Having decided the matter on the jurisdictional issue, it did not examine the remaining legal grounds or the merits of the additions, leaving those issues open. The Revenue’s appeal was dismissed.

FULL TEXT OF THE ORDER OF ITAT DELHI

1. This appeal is filed by the Revenue against the order of the Ld. Commissioner of Income-tax (Appeals)-23, New Delhi [hereinafter referred to as `1d. CIT(A)]dated 26.08.2025 for the Assessment Year 2014-15 raising the following grounds of appeal :-

“1. The Ld. CIT(A) erred in deleting the addition to the amount of Rs.29,00,000/- made u/s 68 of the Act, despite the assessee failed to discharge the primary onus of proving the identity, creditworthiness, and genuineness of the credit entries.

2. The Ld. CIT(A) erred in deleting the addition to the tune of Rs.4,40,00,000/- made u/s 69A of the Act, disregarding the direct evidentiary nexus between seized material and the assessee’s unaccounted cash transactions.

3. The Ld. CIT(A) erred in quashing the assessment without appreciating the specific and cogent material seized during the course of search and duly referred in the satisfaction note.

4. The Ld. CIT(A) erred in holding the satisfaction note as invalid merely because it was consolidated for multiple years, ignoring the fact that the same set of seized documents pertained to several assessment years and hence a single note was both appropriate and legally permissible.

5. The Ld. CIT(A) failed to appreciate that the seized material, including e-mails and Excel Sheets specifically belonged to the assessee, clearly evidencing unrecorded financial transactions.

6. The Ld. CIT(A) erred in ignoring the detailed reasoning and findings recorded by the AO based on incriminating digital evidence duly corroborated with the assessee’s bank transactions.

7. The Ld. CIT(A) failed to appreciate that approval u/s 153D was duly obtained before passing the assessment order, and therefore all procedural requirements were fully complied with.”

2. At the time of hearing, ld. DR of the Revenue brought to our notice the detailed facts of the case and heavily relied on the findings of the Assessing Officer and submitted written submissions which is reproduced below :

“PART I: CASE HISTORY/FACTS OF THE CASE (CHRONOLOGY)

- Jul 20, 2018: A search and seizure operation u/s 132 was conducted on the SMC Global Securities Ltd. group.

- Evidence Recovery: During the search, incriminating digital evidence (emails and Excel sheets) was seized from the backup of Sh. Pradeep Aggarwal and others. The data, specifically an email dated Aug 24, 2015, detailed unaccounted cash transactions between the assessee (Indeed Fincap, formerly Charles India Pvt. Ltd.) and the Multiplex Signature Global groups.

- Oct 18, 2022: The AO recorded a satisfaction note u/s 153C, noting that the seized material pertained to the assessee for the block period of AY 2013-14 to 2019-20.

- Mar 27, 2023: The AO passed the Assessment Order u/s 153C r.w.s. 143(3), making additions of Rs.290,000 u/s 68 (unexplained cash credit) and Rs.4.4M u/s 69A (unexplained money). The total assessed income was Rs.60,69,989.

- Aug 26, 2025: The CIT(A)-23 allowed the assessee’s appeal and quashed the assessment order. The CIT(A) held the initiation of proceedings bad-in-law because the AO recorded a “consolidated satisfaction note” for multiple years instead of year-wise satisfaction.

- Nov 21, 2025: The Pr. CIT (Central)-01, New Delhi, authorized the Department to file the present appeal before the ITAT.

- Dec 03, 2025: The Revenue filed the appeal along with a condonation of delay application for 3 working days.

PART II: SUMMARY OF GROUNDS OF APPEAL (FORM 36)

| Ground No. | Issue/Challenge | Finding & Reference |

| 1 & 2 | Deletion of Addition Challenging the deletion of Rs.2,90,000 (u/s 68) and Rs.4.4 M (u/s 69A) | The Revenue contends the CIT(A) erred in deleting these additions despite the assessee failing to discharge the primary onus of proving identity, creditworthiness and genuineness of credit entries. |

| 3 & 4 | Quashing of Assessment : Challenging the CIT (A)’s decision to quash the assessment based on the “satisfaction note” validly. | The Revenue argues that a consolidated satisfaction note is appropriate and legally permissible when the same set of documents pertains to multiple years. |

| 5 & 6 | Appreciation of Evidence: Failure to appreciate incriminating digital evidence (emails/Excel | The CIT (A) ignored detailed reasoning and findings of the AO based on incriminating digital evidence duly corroborated by bank transactions. |

| 7 | Procedural Compliance : Validity of section 154D approval | The Revenue asserts that all procedural requirements including the mandatory approval u/s 153D, were fully complied with before passing the assessment order. |

PART III: ARGUMENTS OF THE REVENUE TO DEFEND THE ADDITIONS

1. On the Validity of the Consolidated Satisfaction Note (Against Ground 4)

- The CIT(A) erred in quashing the assessment based solely on the “‘consolidated” nature of the satisfaction note. The Revenue contends that where the incriminating material (in this case, a specific email dated Aug 24, 2015, with 5 Excel attachments) contains data spanning several years, a single consolidated note is both logical and legally sufficient.

- Legal Position: While the CIT(A) relied on Signature Global India Ltd., the Revenue distinguishes this by emphasizing that the AO in the present case clearly identified the specific email (Annexure A5) and its relevance to the assessee’s undisclosed cash transactions for the specified block period.

2. On the Evidentiary Value of Seized Digital Records (Against Ground 6)

- The AO’s findings were not based on “surmises” but on a direct evidentiary nexus. The seized email between Dhananjay Shukla (Assessee’s Director) and Ganesh Dutt Sharma (Multiplex employee) contained Excel sheets (e.g. “CH12 DEMO_ 240815”) that recorded exact cash receipts and payments.

- Corroboration: The AO demonstrated a “routing” pattern where cash received by Multiple Fincap Ltd. resulted in identical RTGS transfers to the assessee’s bank account the same day. This corroborates the digital evidence as a “parallel set of books” recording real but undisclosed financial transactions.

3 Failure of Onus by the Assessee (Against Ground 1)

- Under Section 68 and 69A, once the Department provides evidence of unexplained credits/money, the onus shifts to the assessee. In this case, the assessee merely provided a general denial, stating they had “no connection”‘ with the transactions. The assessee failed to produce their own cash book or bank statements to rebut the specific entries found in the seized Excel sheets.

4 Distinguishing Assessee-Favored Precedents

- The assessee relies on cases like Jasjit Singh and Sunil Kumar

- Sharma to argue for year-wise satisfaction. However, the Revenue argues that the “usage of incorrect terminology” or the format of a note should not invalidate a notice if the underlying satisfaction regarding the “belongingness” of documents is clear. In the present case, the AO was “satisfied” that the material pertained to the assessee and had a bearing on the determination of total income for the relevant years.

PRAYER:

In view of the incriminating material and the clear nexus established by the AO, the order of the CIA) should be set aside, and the assessment order u/s 153C should be restored.”

3. At the time of hearing, ld. AR of the assessee submitted that the legal issue involved i.e. the validity of assumption of jurisdiction u/s 153C of the Income-tax Act, 1961 (for short ‘the Act’) is rightly upheld by the ld. CIT (A) in favour of the assessee as the issue is no longer res integra by the decisions of Hon’ble Courts and coordinate Benches of the Tribunal. Further, ld. AR submitted detailed findings which are reproduced below for the sake of brevity :-

“Date of Search in the case of SMC Global Securities Ltd: – 20/07/2018 Date of Satisfaction note recorded in the case of the appellant: 16/08/2022

1. Invalid proceedings u/s 153C

As per the assessment order, Search & Seizure Operation u/s 132 was conducted on 10/07/2018 in SMC Global Securities Ltd. Satisfaction note u/s 153C is stated to be recorded in the case of the assessee on 16/08/2022.

The assessment proceeding-initiated u/s 153C in this case is bad in law and without jurisdiction. It is most respectfully submitted that the powers of the Assessing Officer under Section 153C cannot be invoked in a light, whimsical and arbitrary manner and without complying with the basic pre-requisites specified under Section 153C of the Act. The object underlying the provisions of Section 153C is not to give unbridled power to the Assessing Officer to proceed against any person without reaching satisfaction in an objective manner based on cogent material seized at the time of search. The satisfaction note is the foundation of assumption of jurisdiction u/s 153C. In the absence of valid satisfaction, jurisdiction u/s 153C can not be assumed. The validity of the satisfaction note is required to be evaluated on the basis of the contents of such satisfaction note alone and it is not permissible to virtually expand the scope of the contents of the satisfaction note at a later stage by improving or supplementing the same.

The proceedings initiated u/s 153C is bad in law and without jurisdiction for the following reasons (without prejudice to each other) :-

- The satisfaction note recorded is a consolidated satisfaction note for 7 years.

- There is no description/analysis of seized material based on which satisfaction has been recorded.

- There is no year wise analysis of seized material.

- There is no year wise satisfaction that seized material is having a bearing on the determination of income.

1.1 It is humbly submitted that for making assessment u/s 153C of the Act, the AO is required:-

i) To record separate satisfaction for each year falling in the block period of six years.

ii) To issue separate notice u/s 153C for each year falling in the block period of six years.

iii) To obtain separate approval u/s 153D for each year falling in the block period of six years .

1.2 In the present case, the AO has recorded a consolidated satisfaction note for A.Y. 2013-14 to A.Y. 2019-20. The Hon’ble Karnataka High Court vide its decision dated 22.01.2024 in the case of DCIT vs. Sunil Kumar Sharma & Others (2024) (2) TMI 116 — held as under: –

53. Further, satisfaction note is required to be recorded under Section 153C of the IT Act for each Assessment Year and in the impugned proceedings, a consolidated satisfaction note has been recorded for different Assessment Years, which also vitiates the entire assessment proceedings. In view of all these findings, it is said that the appeals do not have any substance for seeking intervention as sought for by the appellant / Revenue.(Refer page no. 28 of the case law compilation)

1.3 The above decision of Karnataka High Court has been affirmed by the apex court in CIT Vs. Sunil Kumar Sharma & Others (2024)(8) TMI 1086-Supreme Court vide order dated 20.08.2024. The head note of Apex Court decision is as under: –

Validity of proceedings u/s 153C – whether the assessee should be treated as a “Searched Person” or “Other Person”? – Whether `Loose Sheets’ and ‘Diary’ have any evidentiary value? HELD THAT:- We are not inclined to interfere with the impugned judgment and order passed by the High Court of Karnataka at Bengaluru in Writ Appeal [2024 (2) TMI 116 – KARNATAKA HIGH COURT] held notices issued u/s 153C of the Act, based on the loose sheets/diaries are contrary to law, which require to be set aside in these writ appeals, as the same are void and illegal.

As satisfaction note is required to be recorded u/s 153C for each Assessment Year and in the impugned proceedings, a consolidated satisfaction note has been recorded for different Assessment Years, which also vitiates the entire assessment proceedings. In view of all these findings, it is said that the appeals do not have any substance for seeking intervention as sought for by the appellant / Revenue. As per the Panchanama provided herein, it is deemed appropriate to conclude that the notice provided u/s 153C is bad in law.

Special Leave Petition is dismissed. .(Refer page no. 33 of the case law compilation)

1.4 In the case of Rajender Rameshlal Gugale vs. PCIT (Central), Pune, 2025 (1) TMI 240 — ITAT Pune it was held as under:-

8.7. Since in the instant case a consolidated satisfaction note has been prepared for assessment years 2012-2013 to 20182019, therefore, the consolidation satisfaction note being not in accordance with law, therefore, the entire assessment proceedings is liable to be quashed. We hold accordingly and quash the assessment. (Refer page no. 45 of the case law compilation)

1.5 Further to above, the satisfaction recorded by the AO u/s 153C of the Act is bad in law and contrary to apex court decision in the case of Commissioner of Income Tax-III, Pune Versus Sinhgad Technical Education Society 2017 (8) TMI 1298 – Supreme Court in which the Hon’ble apex court held that the AO is required to make a year wise analysis of the incriminating seized material. In this case of Sinhgad Technical Education Society(supra)it was held as under: –

18) The ITAT permitted this additional ground by giving a reason that it was a jurisdictional issue taken up on the basis of facts already on the record and, therefore, could be raised. In this behalf, it was noted by the ITAT that as per the provisions of Section 153C of the Act, incriminating material which was seized had to pertain to the Assessment Years in question and it is an undisputed fact that the documents which were seized did not establish any co-relation, document-wise, with these four Assessment Years. Since this requirement under Section 153C of the Act is essential for assessment under that provision, it becomes a jurisdictional fact. We find this reasoning to be logical and valid, having regard to the provisions of Section 153C of the Act. Para 9 of the order of the ITAT reveals that the ITAT had scanned through the Satisfaction Note and the material which was disclosed therein was culled out and it showed that the same belongs to Assessment Year 2004-05 or thereafter. After taking note of the material in para 9 of the order, the position that emerges therefrom is discussed in para 10. It was specifically recorded that the counsel for the Department could not point out to the contrary. It is for this reason the High Court has also given its imprimatur to the aforesaid approach of the Tribunal. That apart, learned senior counsel appearing for the respondent, argued that notice in respect of Assessment Years 2000-01 and 2001-02 was even time barred.

19) We, thus, find that the ITAT rightly permitted this additional ground to be raised and correctly dealt with the same ground on merits as well.

Order of the High Court affirming this view of the Tribunal is, therefore, without any blemish. Before us, it was argued by the respondent that notice in respect of the Assessment Years 200001 and 2001-02 was time barred. However, in view of our aforementioned findings, it is not necessary to enter into this controversy. .

In the present case before your honour, no such year wise analysis has been done.

1.6 The head note of decision in the case of ITO Vs. Saksham Commodities Ltd., 2024 (12) TMI 1068 — SC Order is as under: –

Proceedings u/s 153C – issuance of the notice was preceded by the drawl of a Satisfaction Note by the jurisdictional AO – Distinction between Section 153A and Section 153C Period of limitation – Nature of the incriminating material that may be obtained and the years forming part of the block which would merit being thrown open

As decided by HC [2024 (4) TMI 461 – DELHI HIGH COURT] abatement of the six AYs’ or the “relevant assessment year” would follow the formation of that opinion and satisfaction in that respect being reached.

We come to the firm conclusion that the “incriminating material” which is spoken of would have to be identified with respect to the AY to which it relates or may be likely to impact before the initiation of proceedings under Section 153C of the Act. A material, document or asset recovered in the course of a search or on the basis of a requisition made would justify abatement of only those pending assessments or reopening of such concluded assessments to which alone it relates or is likely to have a bearing on the estimation of income. The mere existence of a power to assess or reassess the six AYs’ immediately preceding the AY corresponding to the year of search or the “relevant assessment year” would not justify a sweeping or indiscriminate invocation of Section 153C.

The jurisdictional AO would have to firstly be satisfied that the material received is likely to have a bearing on or impact the total income of years or years which may form part of the block of six or ten AYs’ and thereafter proceed to place the assessee on notice under Section 153C. The power to undertake such an assessment would stand confined to those years to which the material may relate or is likely to influence. Absent any material that may either cast a doubt on the estimation of total income for a particular year or years, the AO would not be justified in invoking its powers conferred by Section 153C. It would only be consequent to such satisfaction being reached that a notice would be liable to be issued and thus resulting in the abatement of pending proceedings and reopening of concluded assessments.

HELD THAT:- As there is a delay of 124 and 127 days in filing the Special Leave Petitions respectively, which has not been satisfactorily explained. Even otherwise, we have gone through the Special Leave Petition and do not find any merit in the same.

Special Leave Petitions are, therefore, dismissed on the ground of delay as well as on merits.

1.7 The head note of decision in the case of ACIT CC-31 Vs. Satya Pal Arya, 2025 (3) TMI 155 — SC Order.

1.8 The head note of decision in the case of ACIT Vs. Chander Parkash Gupta, 2025 (3) TMI 1290 — SC Order

1.9 In the case of Saksham Commodities Ltd. Vs. ITO Ward 22(1), 2024 (4) TMI 461 — Delhi High Court

1.10 In the case of Blue Ocean Travels Pvt. Ltd. Vs. DCIT CC — 15, 2024 (12) TMI 384 — ITAT Delhi

1.11 In the case of Super Bazar Stores Pvt. Ltd. C/O- Radheyshyam Sharma & Co., Ca Versus ACIT, Central Circle-6 Jhandewalan Ext. New Delhi 2025 (4) TMI 1130 – ITAT Delhi

1.12 In the case of MSN Institute Of Medical Sciences Pvt. Ltd., M/S. Prathima Resorts & Restaurants Pvt. Ltd., M/S. Prathima Eggset Private Limited., M/S. Spark Vidyut Pvt. Ltd. Versus The PCIT-(Central), Hyderabad. 2025 (4) TMI 599 – ITAT Hyderabad

1.13 In the case of Sarvo Technologies Ltd. Versus The DCIT- Central Circle – 19, ITA No. 1719/DEL/2025- ITAT Delhi

1.14 In the case of Rakesh Trisal v. The DCIT- Central Circle – 27, 2026 (3) TMI 66 – ITAT Delhi

2. That notice issued u/s 153C by the A.O. is without jurisdiction and barred by limitation.

Date of Search in the case of SMC Global Securities Ltd: – 20/07/2018

Date of Satisfaction note recorded in the case of the appellant: 16/08/2022

The assessing officer has issued notice u/s 153C for 7 years from A.Y. 2013-14 to A.Y. 2019-20 based on date of search. It is now a settled law that for initiating the proceedings u/s 153C the date has to be reckoned from the date of recording of satisfaction note. The date of recording of satisfaction note in the present case is 16/08/2022 (F.Y. 2022-23 i.e., AY 2023-24) and the 6 years which could have been taken up for assessment u/s 153C are A.Y. 2017-18 to A.Y. 2022-23. The same can be tabulated as under: –

| Sl.No. | A.Y. | Section |

| 1 | 2023-24 | 143(3) |

| 2 | 2022-23 | 153C |

| 3 | 2021-22 | 153C |

| 4 | 2020-21 | 153C |

| 5 | 2019-20 | 153C |

| 6 | 2018-19 | 153C |

| 7 | 2017-18 | 153C |

Accordingly, the notice u/s 153C for A.Y. 2015-16 could not have been issued by the A.O., as the same is barred by limitation. The issue is no longer res integra, as it is covered by Apex court decision in the case of Commissioner of Income Tax 14 Versus Jasjit Singh 2023 (10) TMI 572 – Supreme Court

Accordingly, applying the ratio of aforesaid judgments to the appellant’s case the initiation of proceedings u/s 153C for A.Y. 2015-16 is without jurisdiction and barred by limitation. Therefore, the proceedings initiated, and assessment order passed u/s 153C for year under consideration is also liable to be quashed as null & void.”

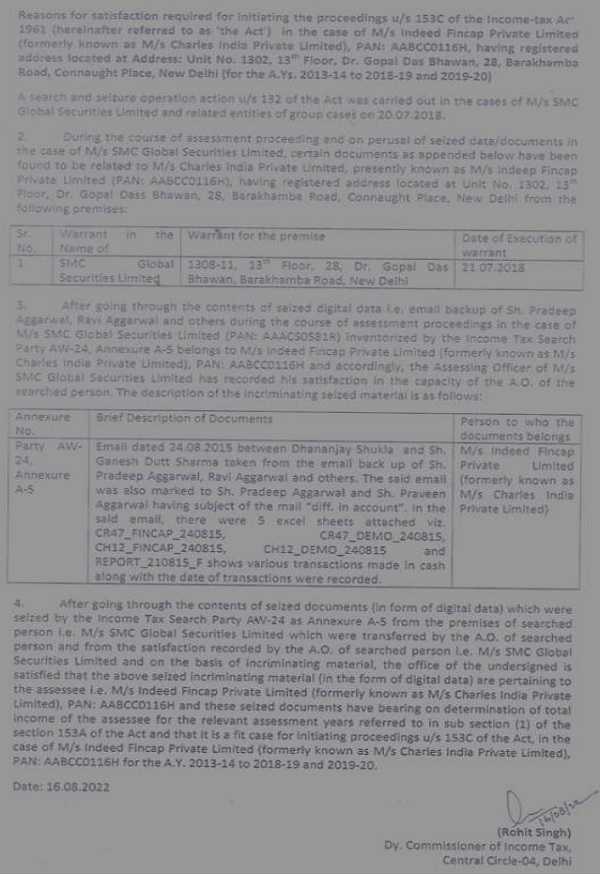

4. Considered the rival submissions and material available on record. We observed that the issue which arises for our consideration is whether the jurisdiction assumed u/s 153C of the Act is valid in law where the satisfaction note recorded by the Assessing Officer is common and does not identify any specific incriminating material qua the relevant assessment year. We observed that the Assessing officer has recorded following satisfaction note for issuance of notice u/s 153C:-

5. We further observed that it is a settled position of law that recording of satisfaction by the Assessing Officer is a condition precedent for invoking jurisdiction u/s 153C of the Act. Further, such satisfaction must be specific, based on cogent material and must clearly indicate that the seized material belongs to or pertains to the assessee and has a bearing on the determination of total income for the relevant assessment year. The satisfaction note thus forms the very foundation of jurisdiction and must reflect due application of mind. It is incumbent upon the Assessing officer to identify the material qua each year before proceeding to assume jurisdiction u/s 153C of the Act.

6. On perusal of the satisfaction note in the present case, we find that the Assessing Officer has recorded a common satisfaction note for multiple assessment years without making any distinction or identifying any specific incriminating material for each year within the Block Period. There is no reference to any document or evidence demonstrating undisclosed income for the year under consideration. The satisfaction note does not contain any quantification or even a prima facie analysis of alleged undisclosed income and appears to have been recorded in a mechanical manner. We are of the view that such a generalized and omnibus satisfaction clearly reflects non-application of mind and fails to meet the statutory requirement of section 153C of the Act.

7. The Hon’ble Supreme Court in CIT vs. Sinhgad Technical Education Society (397 ITR 344) has categorically held that existence of incriminating material qua each assessment year is sine qua non for valid assumption of jurisdiction u/s 153C of the Act. Further, Hon’ble Delhi High Court in the case of Saksham Commodities Ltd. v. ITO [2024] 464 ITR 1 (Delhi) has distinctly held that the satisfaction recorded must be specific and must clearly indicate the incriminating material relatable to each assessment year, failing which the assumption of jurisdiction would be invalid. The Hon’ble High Court emphasized that a generalized or omnibus satisfaction, without reference to specific material and without establishing nexus with the income of the relevant year, cannot sustain proceedings u/s 153C.

8. We further observed that the assessee has further made reference to various decisions of Coordinate Bench which are found to be relevant and applicable to the present case:-

i. Vidur Chharia v. DCIT (ITA No. 209/Del/25) (Delhi-Trib)

ii. Alankit Insurance TPA Ltd. v. DCIT (ITA No. 3801/Del/26) (Delhi-Trib)

iii. Sakshi Agarwal v. DCIT (ITA No. 4216 to 4223/Del/25) (Delhi Trib)

iv. Blue Ocean Travels Pvt. Ltd. v. DCIT (ITA No. 3281 to 3287/Del/24) (04/12/2024) (ITAT, Delhi)

v. 3D Tradex P. Ltd v. ADIT (ITA No. 2065 to 2070/Del/22) (12/02/2025) (ITAT, Delhi)

vi. Maheshwari Coal Benefication & Infrastructure (P.) Ltd. v. DCIT [2025] 171 com 842 (Nagpur – Trib.)

9. In the present case, the material relied upon by the Assessing Officer is stated to be a third-party ledger, which is neither corroborated by independent evidence nor supported by any meaningful enquiry. There is nothing on record to establish any nexus between such material and any undisclosed income of the assessee. In absence of corroboration and in the absence of opportunity of cross-examination, such material cannot be treated as incriminating in nature. Further, the transactions in question are duly recorded in the books of account of the assessee, thereby negating any inference of undisclosed income.

10. It is also not in dispute that the assessment for the year under consideration was unabated and as such in absence of recording of specific satisfaction note, the assumption of jurisdiction u/s 153C is vitiated at the threshold. In view of the foregoing discussion and respectfully following the ratio laid down by the Hon’ble Supreme Court in Sinhgad Technical Education Society (supra) and the Hon’ble Delhi High Court in Saksham Commodities Ltd. v. ITO (supra), we are of the considered opinion that the satisfaction recorded by the Assessing Officer is defective, being common, vague and mechanical, and does not satisfy the mandatory requirements of section 153C of the Act. Consequently, the assumption of jurisdiction u/s 153C is invalid and unsustainable in law and accordingly, the notice issued u/s 153C and the consequent assessment order is hereby quashed. The Ground No. 1(b) and 1(c) are allowed.

11. As the assessment order has been quashed on the legal ground of jurisdiction, the other legal grounds as well grounds on merits of the addition are not required to be adjudicated and kept open.

12. In the result, the appeal of the Revenue is dismissed.

Order pronounced in the open court on this 4th day of June, 2026.

Author Bio