Month: August 2009

277 articlesIncome Tax

Income Tax

Expenditure Not allowable under new direct tax code 2009

Income Tax

Income Tax

New Direct tax code and welath tax provisions, exemption limit may increase to 50 crore

Income Tax

Income Tax

No Provision for Appeal to High Court in New direct tax code 2009

CA, CS, CMA

CA, CS, CMA

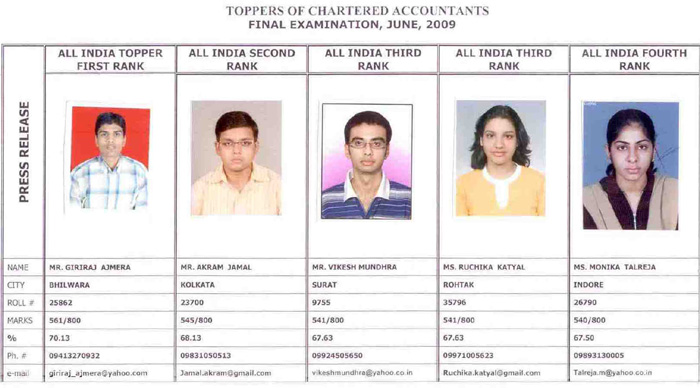

Merit List of CA final & Pass percentage of final & Final (New Course)

CA, CS, CMA

CA, CS, CMA

Due date extended for completion of IT training for students appearing in PCE & IPCE November 2009 Examination

Income Tax

Income Tax

Time limit for filing ITR-V extended to 60 days

Income Tax

Income Tax

Expenditure on convertible debentures is deductible

DGFT

DGFT

Notification No. 121(RE-2008)/2004-09, Dated: 13.08.2009

Custom Duty

Custom Duty

Amends Notification No. 36/2001-Customs Duty (N. T.), Dated: 03.08.2001

DGFT

DGFT