Summary: The Income-tax Act, 2025 reorganises and renumbers the appellate provisions into Sections 356 to 374, while largely retaining the substantive framework of the Income-tax Act, 1961. The provisions cover appeals before the Joint Commissioner (Appeals), Commissioner (Appeals), Income Tax Appellate Tribunal (ITAT), High Court and Supreme Court, along with procedures, powers, limitation periods, and execution of appellate orders. The new Act consolidates Tribunal provisions, integrates faceless appeal procedures, simplifies drafting, and improves structural clarity without materially changing appellate rights or powers. It continues provisions relating to appeal forms, fees, condonation of delay, hearing procedures, enhancement powers, stay of demand, rectification, tax recovery despite appeals, amendment of assessments following appellate orders, exclusion of time taken to obtain certified copies, CBDT’s power to prescribe monetary limits for departmental appeals, and determination of the jurisdictional High Court. Overall, the appellate hierarchy, procedural safeguards and judicial remedies remain substantially unchanged, with the emphasis placed on clearer drafting and streamlined administration.

Page Contents

- Mapping of Appeal Provisions: Income Tax Act, 2025 vs Income-tax Act, 1961

- Section 356 – Appealable Orders before Joint Commissioner (Appeals)

- Section 357 – Appealable Orders before Commissioner (Appeals)

- Section 358 – Form of Appeal and Limitation

- Section 359 – Procedure in Appeal

- Section 360 – Powers of Joint Commissioner (Appeals) or Commissioner (Appeals)

- Section 361 – Appellate Tribunal

- Section 362 – Appeals to Appellate Tribunal

- Section 363 – Orders of Appellate Tribunal

- Section 364 – Procedure of Appellate Tribunal

- Section 365 – Appeal to High Court

- Section 366 – Case before High Court to be Heard by Minimum Two Judges

- Section 367 – Appeal to Supreme Court

- Section 368 – Hearing before Supreme Court

- Section 369 – Tax to be Paid Irrespective of Appeal

- Section 370 – Execution for Costs Awarded by Supreme Court

- Section 371 – Amendment of Assessment on Appeal

- Section 372 – Exclusion of Time Taken for Copy

- Section 373 – Filing of Appeal by Income-tax Authority

- Section 374 – Interpretation of “High Court”

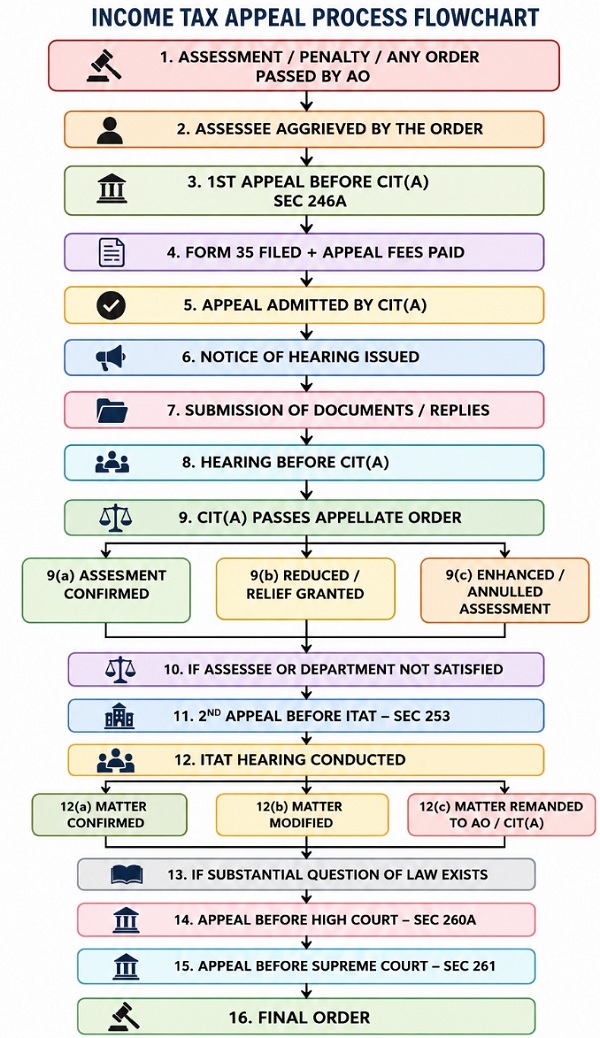

- Flowchart of Income Tax Appeal:

Mapping of Appeal Provisions: Income Tax Act, 2025 vs Income-tax Act, 1961

| Income Tax Act, 2025 | Particulars | Section in Income-tax Act, 1961 | Short Explanation | Major Changes |

| Section 356 | Appealable orders before Joint Commissioner (Appeals) | Section 246 | Specifies orders against which appeal can be filed before JC(A). | JC(A) framework retained with renumbering and procedural simplification |

| Section 357 | Appealable orders before Commissioner (Appeals) | Section 246A | Lists orders appealable before CIT(A) by assessee/deductor/collector. | Mostly same provisions; language simplified and reorganised |

| Section 358 | Form of appeal and limitation | Section 249 | Prescribes appeal form, fees, filing conditions and time limits. | Appeal fees and limitation substantially retained |

| Section 359 | Procedure in appeal | Section 250 | Explains hearing process, inquiry powers and disposal procedure of appeals. | Faceless appeal procedures integrated |

| Section 360 | Powers of JC(A)/CIT(A) | Section 251 | Defines appellate powers like confirm, reduce, enhance or annul assessment. | Powers remain similar; drafting simplified |

| Section 361 | Appellate Tribunal | Sections 252 & 252A | Provides constitution, members and administration of ITAT. | Tribunal provisions consolidated |

| Section 362 | Appeals to Appellate Tribunal | Section 253 | Specifies orders appealable before ITAT and filing procedure. | Similar provisions with structural simplification |

| Section 363 | Orders of Appellate Tribunal | Section 254 | Provides powers of ITAT including stay, rectification and final orders. | Stay provisions and rectification retained |

| Section 364 | Procedure of Appellate Tribunal | Section 255 | Explains bench structure and functioning of ITAT. | Mostly unchanged |

| Section 365 | Appeal to High Court | Section 260A | Allows appeal to High Court on substantial question of law. | No major substantive change |

| Section 366 | Case before High Court to be heard by minimum two judges | Section 260B | Requires High Court appeals to be heard by at least two judges. | No major change |

| Section 367 | Appeal to Supreme Court | Section 261 | Allows appeal to Supreme Court if certified fit by High Court. | Same concept retained |

| Section 368 | Hearing before Supreme Court | Section 262 | Provides procedure for Supreme Court appeals and implementation of orders. | Procedural continuity maintained |

| Section 369 | Tax payable notwithstanding appeal | Section 265 | Tax demand remains payable even if appeal is filed. | No major change |

| Section 370 | Execution for costs awarded by Supreme Court | Section 266 | Provides execution mechanism for Supreme Court cost orders. | Same provision continued |

| Section 371 | Amendment of assessment on appeal | Section 267 | Allows consequential amendment of member assessments after appellate orders. | Similar provision retained |

| Section 372 | Exclusion of time taken for copy | Section 268 | Excludes time taken for obtaining certified copy while calculating limitation. | Same concept retained |

| Section 373 | Filing of appeal by income-tax authority | Section 268A | CBDT may prescribe monetary limits for departmental appeals. | Monetary limit provisions retained |

| Section 374 | Interpretation of “High Court” | Section 269 | Defines jurisdictional High Court for different States and UTs. | No major change |

Section 356 – Appealable Orders before Joint Commissioner (Appeals)

Section 356 provides the statutory right to file an appeal before the Joint Commissioner (Appeals) [JC(A)] against certain orders passed by an Assessing Officer below the rank of Joint Commissioner. The section mainly covers appeals against intimations, assessment orders, reassessment orders, rectification orders and penalty orders where the assessee, deductor or collector is aggrieved by the decision of the Assessing Officer. The assessee may dispute the assessed income, tax determined, loss computed or even the status under which assessment has been made. However, appeals cannot be filed before JC(A) where the order has been passed by or with the prior approval of a higher income-tax authority above the rank of Deputy Commissioner. The section also empowers the Board or authorised authority to transfer appeals between JC(A) and CIT(A) to ensure administrative convenience. Further, the Central Government may notify a faceless appeal scheme for disposal of appeals electronically with minimum physical interaction, thereby improving transparency, accountability and efficiency in tax administration.

Section 357 – Appealable Orders before Commissioner (Appeals)

Section 357 specifies the various orders against which an assessee, deductor or collector may file an appeal before the Commissioner (Appeals). This section acts as the principal first appellate provision under the Income Tax Act. It covers appeals against assessment orders, reassessment orders, rectification orders, penalty orders, orders denying liability to tax, TDS/TCS related orders and orders treating a person as an agent of a non-resident. The section also includes appeals against orders enhancing assessment or reducing refund. The Commissioner (Appeals) therefore acts as the first independent appellate authority reviewing actions of the Assessing Officer. The provision ensures that taxpayers are granted an opportunity to challenge arbitrary or incorrect assessments and protects principles of natural justice within the tax administration system.

Section 358 – Form of Appeal and Limitation

Section 358 prescribes the procedural framework for filing appeals before CIT(A) or JC(A). It provides that every appeal must be filed in the prescribed form, verified in the prescribed manner and accompanied by the applicable statutory fee. The section further prescribes different appeal fees depending upon the assessed income involved in the dispute. It lays down a limitation period of thirty days from the date of service of notice of demand or communication of the order appealed against. The section also recognises the principle of condonation of delay by empowering the appellate authority to admit delayed appeals where sufficient cause for delay is established. Further, an appeal is generally not admitted unless the assessee has paid the tax due on returned income or the advance tax payable. The appellate authority may, in appropriate cases, exempt the assessee from such preconditions. Thus, the section balances procedural discipline with fairness to taxpayers.

Section 359 – Procedure in Appeal

Section 359 governs the procedure to be followed by the Commissioner (Appeals) or Joint Commissioner (Appeals) while disposing of appeals. The section requires the appellate authority to fix a date and place for hearing and issue notice both to the appellant and the Assessing Officer. It recognises the right of representation of both parties either personally or through authorised representatives. The appellate authority is empowered to adjourn hearings, conduct further inquiry or direct the Assessing Officer to carry out additional investigation and submit reports. It may also permit the appellant to raise additional grounds not originally included in the appeal where omission was neither wilful nor unreasonable. Importantly, the appellate authority is required to pass a speaking order in writing containing the points for determination, decision thereon and reasons for such decision. The section also provides that appeals should preferably be disposed of within one year from the end of the financial year in which they are filed. Overall, the provision ensures adherence to natural justice and fair adjudication.

Section 360 – Powers of Joint Commissioner (Appeals) or Commissioner (Appeals)

Section 360 defines the scope and extent of powers exercised by the appellate authority while disposing of appeals. In appeals against assessment orders, the Commissioner (Appeals) or Joint Commissioner (Appeals) may confirm, reduce, enhance or annul the assessment. In penalty matters, the authority may confirm, reduce, cancel or even enhance the penalty. The section grants wide powers enabling the appellate authority to comprehensively examine the correctness of the order appealed against. However, before enhancing an assessment or penalty or reducing a refund, the assessee must be granted a reasonable opportunity of being heard. The section also empowers the appellate authority to consider matters arising from the assessment proceedings even if such issues were not specifically raised by the appellant. Thus, the section establishes the appellate authority as a quasi-judicial body possessing extensive corrective powers over the actions of the Assessing Officer.

Section 361 – Appellate Tribunal

Section 361 provides for the constitution of the Income Tax Appellate Tribunal (ITAT), which functions as the second appellate authority under the Income Tax Act. The Tribunal consists of Judicial Members and Accountant Members appointed by the Central Government. The section also incorporates the provisions of the Tribunals Reforms Act, 2021 relating to qualifications, appointment, tenure and service conditions of members. The President of the Tribunal may be a sitting or retired High Court Judge or a Vice-President of the Tribunal. Vice-Presidents may also be appointed to assist in administration. ITAT occupies a significant position in the appellate hierarchy because it acts as the final fact-finding authority and independently adjudicates disputes between taxpayers and the tax department.

Section 362 – Appeals to Appellate Tribunal

Section 362 governs appeals before the Income Tax Appellate Tribunal. It specifies the orders against which appeals may be filed before ITAT by the assessee or the department. These include orders passed by CIT(A), JC(A), Principal Commissioner, Commissioner and certain orders passed pursuant to DRP directions. The section prescribes a limitation period of two months from communication of the order for filing appeals before ITAT. It also permits filing of cross-objections by the opposite party within thirty days of receipt of notice of appeal. The Tribunal is empowered to condone delay where sufficient cause is established. The section additionally prescribes appeal fees and fees for stay applications. This provision ensures a structured mechanism for independent appellate review of first appellate orders.

Section 363 – Orders of Appellate Tribunal

Section 363 confers powers upon ITAT to pass appropriate orders after hearing both parties to the appeal. The Tribunal may confirm, modify or reverse the orders appealed against. It may also rectify mistakes apparent from the record within six months from the end of the month in which the order was passed. The section further contains detailed provisions relating to stay of tax demand. ITAT may grant stay subject to payment of at least twenty percent of the disputed demand or furnishing equivalent security. The stay may be extended if delay in disposal is not attributable to the assessee, although the aggregate stay period cannot exceed three hundred and sixty-five days. Orders passed by ITAT attain finality subject only to appeal before the High Court on substantial questions of law.

Section 364 – Procedure of Appellate Tribunal

Section 364 prescribes the internal procedure and functioning of the Appellate Tribunal. The President of ITAT is empowered to constitute benches consisting generally of one Judicial Member and one Accountant Member. Single-member benches may hear smaller cases where assessed income does not exceed the prescribed monetary threshold. The President may also constitute Special Benches consisting of three or more members for important or complex matters. In cases where members differ in opinion, the matter is decided according to majority view. The Tribunal is also empowered to regulate its own procedure and possesses powers similar to those of a civil court for effective adjudication. Proceedings before ITAT are treated as judicial proceedings under law.

Section 365 – Appeal to High Court

Section 365 provides for appeal from ITAT to the High Court. Such appeal is maintainable only where the case involves a substantial question of law. Either the assessee or the department may file appeal within one hundred and twenty days from receipt of the Tribunal’s order. The memorandum of appeal must precisely state the substantial question of law involved. The High Court first determines whether such a question exists and formally frames the issue before hearing the appeal. Generally, the appeal is confined to questions so formulated, although the Court may consider additional substantial questions of law for recorded reasons. The High Court may also determine issues not properly decided by the Tribunal. Thus, the section limits High Court intervention primarily to legal interpretation rather than factual disputes.

Section 366 – Case before High Court to be Heard by Minimum Two Judges

Section 366 provides that appeals before the High Court under section 365 shall be heard by a bench consisting of not less than two judges. The decision is rendered according to the majority opinion. In cases where judges differ on any point of law, the point of disagreement is referred to one or more additional judges and the matter is ultimately decided according to majority opinion. This provision ensures collective judicial scrutiny and consistency in interpretation of tax laws.

Section 367 – Appeal to Supreme Court

Section 367 governs appeals from the High Court to the Supreme Court in income tax matters. Appeal lies only where the High Court certifies that the case is fit for appeal to the Supreme Court. Such cases generally involve substantial legal questions, interpretation of important statutory provisions or issues of national significance. The Supreme Court functions as the final judicial authority under the appellate structure of the Income Tax Act.

Section 368 – Hearing before Supreme Court

Section 368 lays down the procedure applicable to appeals before the Supreme Court. The provisions of the Code of Civil Procedure relating to Supreme Court appeals apply to such proceedings. The Supreme Court also possesses discretion regarding award of costs. Once judgment is delivered, the Assessing Officer is required to give effect to the decision in accordance with law. The section therefore ensures implementation of the final judicial verdict in tax disputes.

Section 369 – Tax to be Paid Irrespective of Appeal

Section 369 establishes the principle that tax demand remains payable despite filing of appeal before the High Court or Supreme Court. Filing an appeal does not automatically operate as a stay against recovery proceedings. Therefore, unless specific stay is granted by the appellate authority or court, the department may continue recovery proceedings for collection of tax demand.

Section 370 – Execution for Costs Awarded by Supreme Court

Section 370 provides the mechanism for execution of costs awarded by the Supreme Court in tax appeals. The High Court may, upon application, transmit the Supreme Court’s order relating to costs to a subordinate court for execution. The provision facilitates enforcement and recovery of litigation costs awarded by the highest court.

Section 371 – Amendment of Assessment on Appeal

Section 371 provides for consequential amendment of assessments in cases involving associations of persons or bodies of individuals. Where appellate orders result in changes in assessment of the entity, the appellate authority may authorise the Assessing Officer to amend or make fresh assessments in the hands of members. This ensures consistency and proper allocation of tax liability among members.

Section 372 – Exclusion of Time Taken for Copy

Section 372 provides that while calculating limitation periods for filing appeals or applications, the time required for obtaining a certified copy of the order shall be excluded where such copy was not provided along with the order. This provision protects litigants from hardship arising due to administrative delays in obtaining copies of orders.

Section 373 – Filing of Appeal by Income-tax Authority

Section 373 empowers the CBDT to issue instructions prescribing monetary limits for filing departmental appeals before appellate authorities and courts. The purpose of the provision is to reduce unnecessary litigation and focus departmental resources on substantial revenue matters. The section further clarifies that non-filing of appeal in one case does not amount to acceptance of the issue by the department in other cases.

Section 374 – Interpretation of “High Court”

Section 374 defines the expression “High Court” for purposes of Chapter XVIII by specifying the jurisdictional High Court applicable to different States and Union Territories. It identifies the appropriate High Court having authority over various regions including Delhi, Chandigarh, Puducherry, Lakshadweep and Jammu & Kashmir and Ladakh. This section determines the territorial jurisdiction for filing appeals under the Act.

Flowchart of Income Tax Appeal:

Author Bio