Introduction

The Goods and Services Tax (GST) system in India is based on the principle of destination-based taxation, under which tax revenue is allocated to the state where goods or services are ultimately consumed rather than the state where they are produced. Under destination-based taxation, the consuming state receives the tax revenue because consumption is considered the final taxable event. As a result, states with higher consumption levels and stronger purchasing power tend to generate higher GST collections. The mechanism of Integrated Goods and Services Tax (IGST) plays an important role in ensuring smooth transfer of tax revenue between the Centre and the consuming states in case of inter-state transactions.

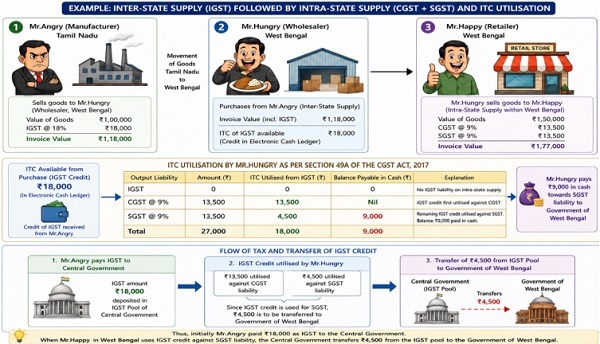

Example of inter state transaction showing revenue allocation to the state where final consumption occurs

In the GST Regime, there are 3 major heads namely IGST, CGST & SGST. IGST is charged when the location of the supplier and the place of supply is in different state. For example, Mr.Angry, a manufacturer located in Tamil Nadu sells goods worth ₹1,00,000 to Mr.Hungry, a wholesaler located in West Bengal. Here the place of supply is the place where the movement of goods terminates i.e. West Bengal and the location of the supplier is Tamil Nadu. Since the location of the supplier and the place of supply is in different state, IGST at the appropriate rate (Say 18%) is charged on the transaction. The manufacturer raises an invoice of ₹1,18,000, comprising ₹1,00,000 as the taxable value of goods and ₹18,000 as IGST. This IGST amount is required to be deposited with the Government. Since, Mr. Angry is a first stage dealer, thus, he do not have any input tax credit to adjust with the output tax liability. He has to pay the 18,000 from bank.

Thereafter, Mr.Hungry in West Bengal sells the same goods to Mr.Happy, a retailer within West Bengal for ₹1,50,000. Since the location of the supplier and the place of supply is in the same state, it is treated as an intra-state supply and attracts CGST and SGST. Accordingly, CGST at 9% amounting to ₹13,500 and SGST at 9% amounting to ₹13,500 are charged. The total invoice value becomes ₹1,77,000.

Mr.Hungry already has ITC of IGST amounting to ₹18,000 from the purchase made from Tamil Nadu which can be used to set-off the liability of CGST and SGST.

The set off rule has been given in Section 49A of the Central Goods and Services Tax Act, 2017 which is summarised below:

- IGST credit is first utilised against IGST liability.

- If no IGST liability exists, it is utilised against CGST and SGST in any order

ITC utilisation by Mr.Hungry –

| Output Liability | Amount (₹) | ITC Utilised from IGST (₹) | Balance Payable in Cash (₹) |

| CGST | 13,500 | 13,500 | 0 |

| SGST | 13,500 | 4,500 | 9000 |

Initially, Mr.Angry paid IGST of ₹18,000 to the Government. When Mr.Happy in West Bengal uses IGST credit against SGST liability, the Central Government transfers ₹4,500 from the IGST pool to the Government of West Bengal.

Factors Affecting GST Revenue Collection in a State

GST revenue collection in a state is influenced by several economic and demographic factors. The factors collectively impacting consumption patterns, business activities, and overall economic growth, thereby directly affecting GST revenue collection are listed below –

- Population Size– States with larger populations generally have higher consumption, leading to greater GST collection.

Example – Uttar Pradesh has a very large population, leading to high consumption of daily-use goods and services, which increases GST collection.

- Purchasing Power of People– Higher income and spending capacity increase taxable consumption and GST revenue.

Example – Maharashtra collects very high GST revenue because cities like Mumbai and Pune have high-income consumers with strong purchasing power.

- Urbanization – Urban areas usually witness greater commercial activity and consumer spending.

Example – Karnataka, especially Bengaluru, has high urbanization with strong purchasing power of the people staying there, resulting in substantial GST collection.

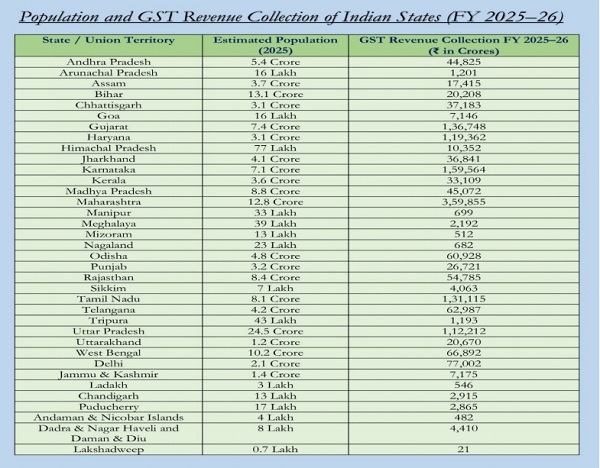

The following table presents the state-wise population and GST revenue collection of India for the Financial Year 2025–26.

West Bengal has an estimated population of 10.2 crore people, which is higher than Tamil Nadu’s 8.1 crore people. However, despite having a smaller population, Tamil Nadu collected ₹1,31,115 crore in GST revenue during FY 2025–26, while West Bengal collected only ₹66,892 crore. In fact, Tamil Nadu’s GST collection is almost twice that of West Bengal. This is because population is not only the sole factor affecting the amount of GST revenue collection in a state, equal attention is to be given to the other factors mentioned above. But the underlying factor remains the same that the consumer state is the ultimate beneficiary.

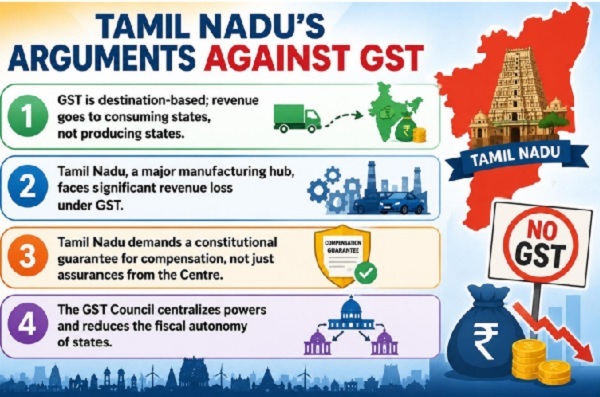

Why Tamil Nadu Opposed GST: A Manufacturing State’s Concerns

Despite broad political support for GST, the State of Tamil Nadu emerged as one of its strongest opponents during the constitutional amendment process. The opposition was not directed against tax reform itself, but against the structural and financial implications of GST on manufacturing states.

Tamil Nadu’s arguments against GST are listed below –

- Tamil Nadu argued that GST would adversely affect manufacturing states because GST is a destination-based tax system where revenue goes to the consuming state rather than the producing state.

- The state feared significant revenue loss since Tamil Nadu was one of India’s largest manufacturing and industrial hubs producing automobiles, textiles, engineering goods, leather products, and electronics.

- Tamil Nadu demanded a constitutional guarantee for compensation instead of relying merely on assurances from the Central Government regarding compensation for revenue losses.

- The state argued that the proposed GST Council would reduce the fiscal autonomy of states and centralize taxation powers in favour of the Union Government.

Conclusion

The GST system has shifted India’s fiscal focus: from “where goods are produced” to “where goods are consumed”. In today’s economic landscape, manufacturing alone no longer guarantees higher tax revenues; instead, population size, consumer spending, urbanization, and purchasing power have emerged as equally powerful drivers of fiscal strength. While industrial states continue to fuel India’s production engine, consumer-oriented states are increasingly becoming the major beneficiaries of GST due to their expanding markets and rising demand. The evolving GST framework therefore reflects a broader transformation in the Indian economy, where consumption-driven growth is becoming the new foundation of state revenue generation and economic competitiveness.

The message of destination-based taxation is therefore loud and unmistakable — in the GST era, economic strength is no longer determined solely by where goods are made, but by where India chooses to spend.