Case Law Details

In re Nikoarc Industries Private Limited (CAAR Mumbai)

The Customs Authority for Advance Ruling (CAAR), Mumbai examined whether Anti-Dumping Duty (ADD) under Notification No. 15/2023-Customs (ADD) dated 22 December 2023 was applicable to Laser Engraving Machines imported by the applicant and classified under Tariff Sub-heading 84561100. The applicant contended that the imported products were compact DIY laser engraving machines intended for artistic, decorative, personalization, jewellery, signage, educational, hobby and small commercial applications, and not industrial laser machines used for cutting, marking or welding operations covered by the notification. The applicant also relied on the DGTR Final Findings, which recorded that laser engraving machines were not included within the scope of the Product Under Consideration (PUC).

The Authority first observed that there is no separate tariff entry specifically covering standalone laser engraving machines and that the classification and applicability of anti-dumping duty must be determined according to the nature and function of the imported goods. It found that the imported laser engraving machines work by laser beam technology and remove or alter material by laser process. Accordingly, they are classifiable under Customs Tariff Heading 84561100, which covers machine-tools operated by laser for working any material by removal of material.

The Authority, however, distinguished tariff classification from the levy of anti-dumping duty. It held that classification under Customs Tariff Heading 84561100 does not automatically attract Anti-Dumping Duty because the levy depends on whether the imported goods fall within the Product Under Consideration defined in the DGTR Final Findings and Notification No. 15/2023-Customs (ADD). The DGTR had clarified that tariff classification is only indicative and not determinative of the scope of the Product Under Consideration.

On examining the DGTR findings and the notification, the Authority found that the Product Under Consideration was confined to industrial laser machines used for cutting, marking and welding operations in industrial manufacturing environments. These products were described as industrial capital goods, customer-made systems and machines developed for specific industrial end-use requirements, generally characterised by high laser power, large working areas, industrial automation, factory installation and heavy-duty production applications. The Product Control Number methodology adopted by DGTR was also based on industrial parameters such as bed size, laser power, cutting heads and heavy-duty industrial configurations.

In contrast, the imported products were found to be compact, standardised, portable and low-powered laser engraving machines intended for artistic, decorative, personalization, jewellery, signage, educational, hobby and small commercial applications. They were marketed on the basis of engraving area, portability, software compatibility, laser source type and user convenience rather than industrial production specifications. The Authority held that their technical characteristics, commercial identity, intended use, customer base and market segment were materially different from those of industrial laser machines.

The Authority further referred to the DGTR Final Findings, which specifically recorded that laser engraving machines, laser bending machines, laser drilling machines and laser cleaning machines were not included within the scope of the Product Under Consideration. It also noted that the DGTR investigation concerned industrial capital goods and customer-made production systems rather than standardised compact engraving units.

Accordingly, the Authority concluded that although the imported Laser Engraving Machines are classifiable under Customs Tariff Heading 84561100, they are commercially, technically, functionally and technologically distinct from the industrial laser cutting, marking and welding systems covered by Notification No. 15/2023-Customs (ADD). Since Anti-Dumping Duty under the notification applies only to products falling within the Product Under Consideration, the imported Laser Engraving Machines do not attract Anti-Dumping Duty. The Authority ruled that ADD under Notification No. 15/2023-Customs (ADD) dated 22 December 2023 is not leviable on the import of the subject Laser Engraving Machines, subject to Customs authorities being satisfied through physical verification and the description of the goods in the Bill of Entry at the time of import.

FULL TEXT OF THE ORDER OF CUSTOMS AUTHORITY OF ADVANCE RULING, MUMBAI

M/s. NIKOARC Industries Private Limited (IEC No.: AA KCN2119A) (hereinafter referred to as ‘the Applicant’) filed an application (CAAR-1) for advance ruling in the Office of Secretary, Customs Authority for Advance Ruling (CAAR) Mumbai. The said application was received in the secretariat of the CAAR, Mumbai on 13.01.2026 along with its enclosures in terms of Section 281-I (1) of the Customs Act, 1962 (hereinafter referred to as the ‘Act also’). The Applicant is seeking advance ruling as to whether the Notification No. 15/2023-Customs (ADD) dated 22nd December 2023 is applicable for leviability of Anti-Dumping duty for the product of “Laser Engraving Machin”.

2. Applicant’s Submissions:

2.1 The Applicant submitted that they are into business of importing and trading of Laser Engraving Machines. having address at Ground Floor, No 133, UMA TOWERS, Near Pepsi Company, Mysore Road, Near Pepsi Company, Kumbalagodu Village, Kengeri Hobli, Bengaluru, Urban, Karnataka, 560074. They are also into trading of Laser Spare Parts and accessories and laser Source is one of the spare parts.

Applicant is importing laser cutting & marking machine parts and laser welding machine parts i.e Laser source as per below table:

| Sr. No. | Description | Tariff Sub-Heading CTSH/HSN Code |

| 1 | Laser Engraving Machines | 84561100 |

The applicant needs Advance Ruling as to whether the Notification No. 15/2023-Customs (ADD) Dated 22″ December 2023 is applicable for liveability of Anti-Dumping duty on the aforementioned Laser Engraving Machine.

2.2 The applicant stated that Laser Engraving Machine shall not be covered under the aforementioned notification. They submit their clarification in this regard as follows:

1. The said notification is not applicable to Laser Engraving Machine, their justification that Notification No. 15/2023-Customs (ADD), dated December 22, 2023, imposes anti-dumping duties on specific industrial laser machines, particularly those used for cutting, marking, or welding operations.

2. The applicant has also given reasons Why this Notification may not apply to Laser Engraving Machines as under:

A). Scope of the Notification:

i) The notification No. 15/2023-Customs (ADD), dated December 22, 2023 restricts “Industrial Laser Machines, used for cutting, marking, or welding operations.

ii) Laser engraving machines, are not included in recommendation, Refer : Notification Final Finding New Delhi, the 27th September, 2023.Case No. ADD (OI) — 07/2022, issued by Department of Commerce) (DIRECTORATE GENERAL OF TRADE REMEDIES) as ADD Notification No. 15/2013 Dt 22 Dec 2023 is based or the final findings and recommendations dated 27th Sept 2023 of the DGTR

C.1 Submission made by the interested parties

Para Cl(k). “The PUC is the industrial laser machine and other laser machine. However, the domestic industry has not itself included other types of laser machine within the scope of the PLIC such as laser engraving machines, laser bending machines, laser drilling machines and laser cleaning machines.”

iii. B. PRODUCT UNDER CONSIDERATION

Para B .4 (4) ………….All laser industrial machines used for purposes other than cutting, marking, or welding are excluded from the scope of the PUC.

iv. C. 3. Examination by the Authority

Para-C. 3 (7)… All laser industrial machines used, for purposes other than, cutting, marking, or welding are excluded from the scope of the PUC’.

B) Legal Position

The phrase used ” exclude ” “used for purposes other than cutting, marking, or welding” constitutes a clear and deliberate limitation on the scope of the investigation and consequently the imposition of anti-dumping duties. By specifying only those machines used for cutting, marking, or welding, the l)GTR has excluded by necessary implication all other types of laser machines from the purview of the PUC.

Interpretation of Taxing Statutes — Supreme Court Ruling

In the Supreme Court judgment titled: Chief Commissioner of Central Goods and Services Tax v. Safari Retreats Pvt. Ltd. 2024 (90) G.S.T.L. 3 (S.C.) Decided on: 3 October 2024 Bench: Hon’ble Justices Abhay S. Oka and Sanjay Karol

Key Legal Principle on Interpretation of Taxing Statutes:

As per Paragraph 25 of the judgment, the Hon’ble Supreme Court laid down clear rules regarding how taxing statutes must be interpreted. Rules of Interpretation Summarized:

-

-

-

- Rules regarding the interpretation of taxing statutes

-

-

25. Regarding the interpretation of taxation statutes, the parties have relied on several decisions. The law laid clown on this aspect is fairly well-settled. The principles governing the interpretation of The taxation statutes can he summarised as follows :

(a) A taxing statute must be read as it is with no additions and no Subtraction on the grounds of legislative intendment or otherwise

(b) If the language of a taxing provision is plain, the consequence of giving effect to it may lead to some absurd result is not a factor to be considered when interpreting the provisions. It is .for the legislature to step in and remove the absurdity;

(c) While dealing with a taxing provision, the principle of strict interpretation should he applied;

(d) If two interpretations of a statutory provision are possible, the Court ordinarily would interpret the provision in favour of a taxpayer and against the revenue;

(e) In interpreting a taxing statute, equitable considerations are entirely out Of place;

(f) A taxing provision cannot be interpreted on any presumption or assumption;

(g) A taxing statute has to be interpreted in the light of what is clearly expressed. The Court cannot imply anything which is not expressed. Moreover, the Court cannot import provisions in the statute to supply any deficiency;

(h) There is nothing unjust in the taxpayer escaping if the letter of the law .fitils to catch him on account of the legislature’s failure to express itself clearly;

(i) If literal interpretation is manifestly unjust, which produces a result not intended by the legislature, only in such a case can the Court modify the language;

(j) Equity and taxation are strangers. But if construction results in equity rather than injustice, such construction should be preferred;

(k) It is not a function of the Court in the fiscal arena to compel the Parliament to go .further and do more;

(I) When a word used in a taxing statute is to be construed and has not been specifically defined, it should not be interpreted in accordance with its definition in another statute that does not deal with a cognate subject. It should be understood in its commercial sense. Unless defined in the statute itself the words and expressions in a taxing statute have to be construed in the sense in which the persons dealing with them understand, that is, as per the trade understanding, commercial and technical practice and usage.

— Para 25(c), Supreme Court, Safari Retreats Case (2024)

C) Nature of Machines:

Industrial Laser Machines in fully assembled, SKD or CKD form, used for cutting, marking or welding operations.”

This definition specifically limits the scope to industrial-grade machinery used in manufacturing and fabrication environments.

DIY (Do-It-Yourself) Laser Machines:

-

-

- These arc compact, low-powered, desktop machines intended lbr personal, craft, hobby, or educational purposes.

- Typical applications include engraving on wood, plastic, acrylic, etc., not industrial-grade metals.

- These machines are not used for cutting, welding, or marking in industrial processes, and therefore do not meet the functional criteria of the PUC.

-

Commercial Classification:

-

-

- DIY laser machines are sold, marketed, and operated in a completely different market segment than industrial laser systems.

- They are designed for light commercial use, and their performance, design, and safety specifications arc significantly below industrial standards.

-

Conclusion:

Anti-dumping explicitly excludes laser engraving machines (and other such machines not used for cutting, marking, or welding). Therefore, the anti-dumping duties imposed by this. notification are not applicable to laser engraving machines.

2.3 Vide addition submission on personal hearing dated 19.05.2026, the applicant further stated that the imported products are laser engraving machines falling under IISN Code 84561100 intended for design, decorative, artistic and 31) engraving applications, and not Industrial Laser Machines, in fully assembled, SKI) or CKD form, used for cutting, marking, or welding operations, contemplated under the anti-dumping notification under 15/2023 Dt. 22 Dec 2023. The imported products are commercially marketed and traded based on:

- engraving area/work area,

- material compatibility,

- laser source type,

- wattage,

- desktop/tabletop format,

- hobby/commercial/jewellery/signage applications,

- portability,.

- speed/resolution,

- rotary attachment capability,

- and software compatibility.

2.4 The applicant further informed that the imported products are DIY / compact engraving systems and are not customer-made industrial production laser systems contemplated under the anti-dumping notification. It is respectfully submitted that the DGTR findings repeatedly describe the covered products as:

- “customer made products”,

- industrial laser systems developed for specific industrial end-use requirements,

- . capital goods manufactured in different industrial configurations depending upon industrial applications and customer requirements.

In contrast, the imported engraving machines are standardized compact engraving units and are not industrial production systems customized for heavy industrial manufacturing applications. Further, the imported products are DIY (“Do It Yourself’) laser engraving machines, i.e., compact user-operated engraving systems intended for hobby, artistic, decorative, personalization, signage, jewellery, craft and small commercial applications, and not heavy industrial manufacturing equipment.

2.5 The applicant also stated that the imported products are compact DIY laser engraving machines which can be easily carried by hand, handled and operated manually, unlike heavy industrial laser cutting, marking or welding systems contemplated under the anti-dumping notification. Such DIY engraving machines are standardized compact products and arc commercially distinct from industrial laser cutting, marking and welding systems contemplated under Notification No. 15/2023-Customs (ADD) dated 22.12.2023 and the corresponding Directorate General of Trade Remedies (DGTR) Final Findings.

Further, the imported DIY laser engraving machines are complete compact units and are not commercially traded in Semi Knocked Down (SKD) or Completely Knocked Down (CKD) condition in the industrial laser machinery market contemplated under the notification.

2.6 Further, the Directorate General of Trade Remedies (DGTR) findings relating to SK.D/CKD configurations pertain to large industrial laser cutting, marking and welding systems requiring industrial assembly and integration operations. In contrast, the imported engraving machines are standardized compact engraving units supplied as complete ready-to-use products for hobby, decorative, artistic and small commercial applications, and therefore are commercially and functionally distinct from the industrial laser systems contemplated under the Product Under Consideration (PIJC).

Further, the Product Control Number (PCN) structure itself demonstrates that the investigation was confined to industrial laser cutting, marking and welding systems. The entire PCN methodology is built around:

- industrial bed sizes,

- industrial cutting heads,

- industrial laser power ranges,

- 21)/31) industrial systems,

- heavy-duly industrial configurations.

The PCN structure itself is based on heavy industrial bed-size categories such as:

- 3000mm x 1.500mm,

- 6000mm x 2500mm,

- 12000mm x 2500mm etc.,

which are applicable only to industrial production laser systems.

In contrast, laser engraving machines are compact standard engraving units primarily intended for engraving applications and are not commercially traded, identified or categorized on the basis of such industrial bed-size configurations. It is further respectfully submitted that the I)GTR itself recognized that all laser machines were not included within the scope of the Product Under Consideration (PUC).

2.7 Furthermore, reference is invited to Final Findings, Case No. ADD (01)-07/2022 dated 27.09.2023 issued by the Directorate General of Trade Remedies.

Reference may kindly be made to Para C1 5(k), wherein the Authority specifically recorded as under:

“……The FIX is the industrial laser• machine and other• laser machine. However, the domestic industry has not itself included other types of laser machine within the. scope of the PUC such as laser engraving machines, laser bending machines, laser drilling machines and laser cleaning machines…….”

Further, reference may kindly be made to Para 143(b), wherein the Authority observed as under:

“….The product under consideration comes in a wide range of different sizes, laser power, bed size etc. Different categories/types are developed to meet specific end-user requirements. Since it is a capital good and customer made product, the design of the industrial laser machines is as per the end use requirements………”

The aforesaid observations clearly establish that the Authority was dealing with industrial customer-made laser production systems developed for industrial manufacturing requirements. However, the imported products in the present case are laser engraving machines, which are functionally, commercially and technologically distinct products and are not customer-made industrial production systems falling within the categories of industrial laser cutting, marking or welding machines contemplated under the PUC. Further, engraving machines are not commercially categorized or sold on the basis of industrial bed sizes. heavy-duty industrial configurations or customized production specifications as contemplated in the PCN methodology. Reference may also kindly be made to Para 26 of the Final Findings, wherein the Authority prescribed the PCN methodology fen• industrial laser machines. The prescribed, parameters themselves demonstrate that the investigation was confined to industrial production laser systems and not compact DIY / engraving machines.

2.8 The applicant also stated that the imported laser engraving machines do not fall within the scope of the Product Under Consideration (PUC). Thus, the present case is not a question of whether a particular variant/model/configuration is covered within the Pt C. Rather, the imported engraving machines themselves fall outside the notified product category altogether. Accordingly, the issue involved is one of complete exclusion from the scope of tile Product Under Consideration (PUC) itself. It is further respectfully submitted that laser engraving machines are specifically excluded from the scope of Notification No. 15/2023-Customs (ADD) dated 22.12.2023.

3. Port of Import and reply from jurisdictional Commissioner, Nhava Sheva-V, JNCH, Uran.

The applicant in their CAAR-1 indicated that they intend to import the subject goods from the jurisdiction of Office of the Commissioner of Customs. (Chennai-IV), –Import Commissionerate, Customs nouse, 60, Rajaji Salai, Chennai. The applications were forwarded to the Office of the Commissioner of Customs (Chennai-IV), Import Commissionerate, Chennai for their comments on 10.02.2026, 24.02.2026, 13.03.2026 and 02.04.2026, however, no replies have been received in this regard.

4. Details of Personal Hearing: :-

The personal hearing in the matter was conducted on 19.05.2026 in the office of CAAR, Mumbai. During the personal hearing the authorised representative submitted that his-product is excluded from the scope of Notification No. 15/2023-Cus. (ADD) dated 22.12.2023. However, he also sought 15 days more time to submit additional material. Nobody appeared the hearing from the department side.

5. Discussion and Findings: –

5.1 I have care filly considered all materials placed on record, including the applicant’s technical documentation. legal submissions and the detailed representations made during the personal hearing by M/s Nikoarc Industries Private Limited. This ruling is rendered in accordance with the evidence submitted and the applicable legal framework. The primary issue for determination is whether the imported Laser Engraving Machine are liable to anti-dumping duty under Notification No. 15/2023 Customs (ADD) dated 22nd December 2023.

5.2 Before deciding the matter, it is essential to examine the legal framework under the Customs Tariff Act, 1975, along with the relevant Chapter and Section Notes and the Harmonized System of Nomenclature (HSN) Explanatory Notes, which reveal that there is neither a general nor specific tariff heading in the First Schedule to the Customs Tariff Act, 1975. that precisely covers a standalone ” Laser Engraving Machine.” As such, the classification and the applicability of anti-dumping duty must be assessed in accordance with the nature and function o the imported goods.

5.3 Upon examination of the applicant’s submission, it emerges that the applicant is engaged in the business of importing and trading of Laser Engraving Machines, laser spare parts, accessories and laser sources. The applicant imports compact laser engraving machines marketed and commercially traded as DIY laser engraving machines, desktop laser engravers, tabletop engraving systems, portable laser engravers, hobby engraving systems, jewellery/signage engraving machines and artistic engraving devices. The applicant has classified laser engraving machine under Tariff Sub-heading 84561100. An advance ruling has been sought under Section 2811 of the Customs Act. 1962, to determine whether Notification No 15/2023–Customs (ADD), which applies to “Industrial Laser Machines in fully assembled, SKI) or CKI) form,” is applicable to such laser engraving machines. The applicant is seeking Ruling from the Authority as under:

Whether the Notification No. 15/2023-Customs (ADD) dated 22.12.2023 is applicable Jr leviability of Anti-Dumping Duty far the Laser Engraving Machines.

5.4 The imported products are compact laser engraving systems intended primarily for artistic engraving, decorative applications, personalization, signage, jewellery engraving, hobby applications, creator/maker applications, educational use and small commercial engraving operations. The imported products are commercially marketed and traded basic upon engraving area/work area, material compatibility, laser source type, wattage. desktop/tabletop format, portability, software compatibility, engraving resolution, rotary attachment capability, hobby/commercial applications, and user convenience. Hence, these products arc compact standardized engraving systems.

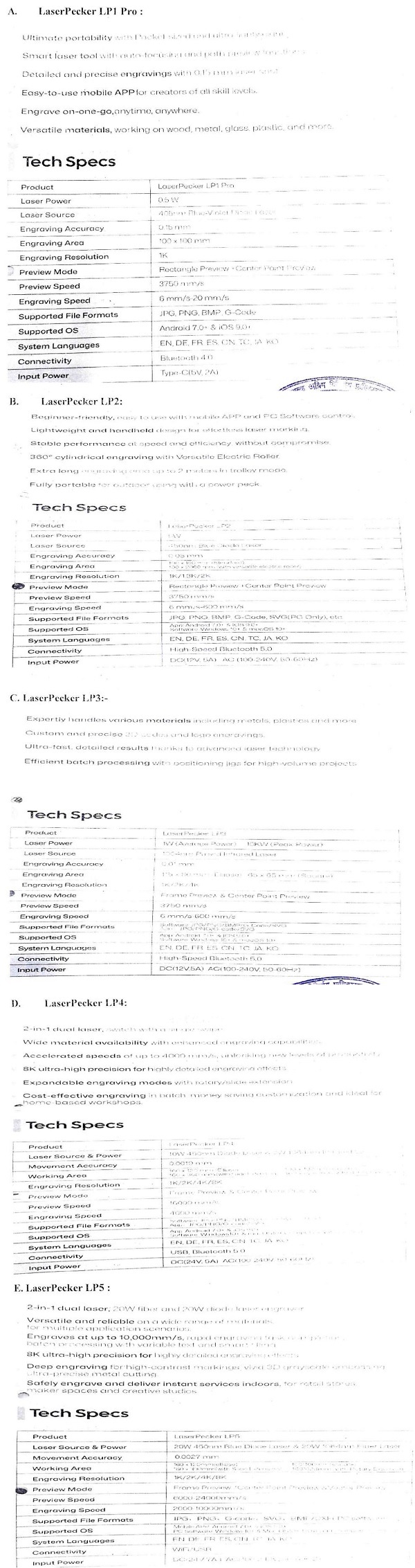

5.5 Further, accordingly Catalogue of products submitted by applicant, technical analysis of Models as under:-

These products i.e. IT I pre, LP2, L.P3 / 1_24 / LPS models are technically identifiable as portable laser engraving Machines, compast DIY laser engravers, handheld / desktop engraving devices, low-power laser marking/engraving systems, hobby/craft/personalization machines and not heavy industrial laser production machinery.

5.6 I also find that the ,applicant has proposed that the subject goods can be classified under Tariff entry. 84561 100. Relevant portion of CTH 8456 is reproduced below for case of reference:

| Tariff Item | Description | Unit | Rate |

| 8456 | MACHINE-TOOLS FOR WORKING ANY MATERIAL BY REMOVAL OF MATERIAL, BY LASER OR OTHER LIGHT OR PHOTON BEAM, ULTRA-SONIC, ELECTRO-DISCHARGE, ELECTRO-CHEMICAL, ELECTRON BEAM, IONIC-BEAM OR PLASMA ARC PROCESSES; WATER-JET CUTTING MACHINES | ||

| – Operated by laser or other light or photon beam processes: | |||

| 8456 11 00 | — Operated by laser | u | 7.5% |

| 8456 12 00 | — Operated by other light or photon beam processes | u | 7.5% |

| 8456 20 00 | – Operated by ultrasonic processes | u | 7.5% |

| 8456 30 00 | – Operated by electro-discharge processes | u | 7.5% |

| 8456 40 00 | – Operated by plasma arc processes | u | 7.5% |

| 8456 50 00 | – Water-jet cutting machines | u | 7.5% |

| 8456 90 | – Other: | ||

| 8456 90 10 | — For dry-etching patterns on semi-conductor materials | u | Free |

| 8456 90 20 | — Electro-chemical machines | u | 7.5% |

| 8456 90 90 | — Other | u | 7.5% |

I find that in Chapter 84, heading, 8456 covers the Machine-tools for working any material by removal of material, by laser or other light or photon beam, ultrasonic, electro beam. ionic beam or plasma arc processes; water jet cutting machines. I find that Laser Engraving Machine work material by laser process, engraving is performed through laser beam action and the machine remove/alter material surface by laser technology. The subject products is a complete laser working machine and therefore, will be covered under CTSH 845611.

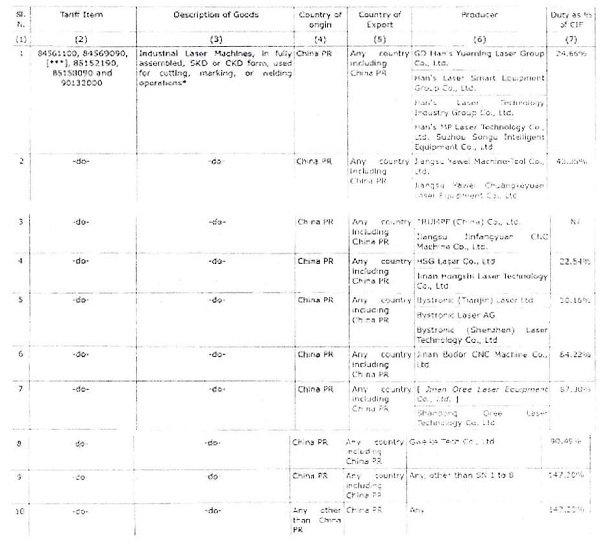

5.7 I observed that under Notification No. 15/202-Customs (ADD) dated 22.12.2023, Central Government imposes Anti-Dumping Duty on the subject goods, the description of which is specified in column (3) of the following Table, falling under tariff item of the First Schedule to the Customs Tariff Act as specified in the corresponding entry in column (2), originating in the country as specified in the corresponding entry in column (4), exported from the countries as specified in the corresponding entry in column (5), produced by the producers as specified in the corresponding entry in column (6), and imported into India, an antidumping duty calculated at the rate as specified in the corresponding entry in column (7) of the said Table. namely :-

It is amply clear from the above that ADD is imposable only on Industrial Laser Machines, in fully assembled. SKD or CKD form, used for cutting, marking or welding operations. Now the issue before me is whether the Industrial laser machines and the Laser Engraving Machines are the same or otherwise.

5.8 I find that Customs Tariff Heading 84561100 is a broad tariff entry covering all machine-tools operated by laser for working any material by removal of material. The heading does not distinguish between industrial laser machines and compact DIY laser engraving machines, and therefore both categories may be classifiable under the same tariff heading. However, classification under the Customs Tariff and applicability of Anti-Dumping Duty are two distinct legal issues. While tariff classification is based on the technical characteristics and operating principle of the goods, the levy of Anti-Dumping Duty depends. upon whether the imported goods fall within the scope of the Product Under Consideration (PUC) defined in the DGTR Final Findings and Notification No. 15/2023-Customs (ADD). The DGTR has also clarified that the customs tariff classification is only indicative and is not determinative of the scope of the PUC. Accordingly, the mere classification of the imported Laser Engraving Machines under CTH 84561100 does not automatically render them liable to Anti-Dumping Duty unless they satisfy the technical, functional and commercial characteristics of the industrial laser machines covered by the notification.

5.9 It is observed that the DGTR Final Findings in Case No. ADD (O1)-07/2022 and the consequent Notification. No. 15/2023-Customs (ADD) dated 22.12.2023 relate to Industrial Laser Machines used for cutting, marking and welding operations in industrial manufacturing environments. The findings describe such machines as industrial capital goods, customer-made systems and products developed according to specific industrial end-use requirements. These machines arc generally characterized by high laser power, large working areas, industrial automation, factory installation and heavy-duty production applications. In contrast, the imported Laser Engraving Machines are compact, standardized, portable and low-powered. devices intended for artistic, decorative, personalization, jewellery, signage, educational, hobby and small commercial applications. They are marketed ‘and traded on the basis of engraving area, portability, software compatibility, laser source type and user convenience rather than industrial production specifications. Their technical characteristics; commercial identity, intended use, customer base and market segment are materially different from those o C industrial laser machines.

5.10 I also find that Notification No. 15/2023-Customs (ADD) dated 22.12.2023 clearly establish that the Product Under Consideration (PUC) was confined to Industrial Laser Machines used for cutting, marking and welding operations, which were described by the Authority as capital goods, customer-made products and industrial systems designed for–specific manufacturing, requirements. The Product Control Number (PCN) methodology adopted by DGTR was based upon industrial parameters such as bed size, laser power, cutting heads and heavy-duty industrial configurations, demonstrating that the investigation was directed towards factory-installed industrial production machinery.

Further, in Para C.1(5)k of the Directorate General of Trade Remedies (DGTR.) in Case No. ADD (01)-07/2022 as under:

“The PUC is the industrial laser machine and other laser machine. However, the domestic industry has not itself included other types of laser machine within the scope of the PUC such as laser engraving machines, laser bending machines, laser drilling machines .and laser cleaning machines.”

I expressly recorded that laser engraving machines, laser bending machines, laser drilling machines and laser cleaning machines were not included within the scope of the PIJC. The imported goods in the present case are compact DIY/Desktop Laser Engraving Machines, commercially marketed for artistic, decorative, personalization, jewellery, signage, hobby and small commercial applications. They are portable, standardized, low-power engraving devices and not customer-made industrial production systems. Therefore, although classifiable under CTI 84561100, the imported laser engraving machines are commercially, functionally and technologically distinct from the industrial laser machines investigated by DGTR and consequently fall outside the intended scope of the Product Under Consideration covered under Notification No. 15/2023-Customs (ADD) dated 22.12.2023.

Furthermore, reference is invited to Para 143 (b) of the Final Findings wherein the Authority observed that:-

b. “The product under consideration comes -in a wide range of different sizes, laser power, bed size etc. Different categories/types’ are developed to meet specific end-user requirements. Since it is a capital good and customer made product, the design of the industrial laser machines is as per the end use requirements. It may be possible that the domestic industry would have produced machine similar to the imported product with some minor differences in product characteristics. In a situation where a product is produced and sold in a large number of types/forms/varieties, the Authority does not consider that the domestic industry should have produced and supplied each of them. Therefore, the Authority has considered lithe domestic industry has the technical capacity to provide such products.–

The above observations clearly establish that the investigation concerned industrial capital goods, customer-made production systems, industrial manufacturing configurations, and industrial fabrication machinery. In contrast, the subject products are standardized compact engraving units,. mass-produced consumer/commercial products, portable. engraving stems. ready-to-use .desktop devices, and not. customer-designed industrial. production machinery. Thus, the subject products belong to. an entirely separate commercial and functions category,

6. Hence, it. is seen that the subject products are compact DIV laser engraving machines intended for artistic, decorative, personalization and small commercial applications. The subject products are commercially distinct, technically distinct, functionally distinct and technologically distinct from the industrial laser cutting, marking and welding systems contemplated under Notification No. 15/2023-Customs (ADD). It is also observed that Anti Dumping Duty under aforesaid Notification applies only if the product also falls within the PUC. The subject products are compact DIY engravers, hobby/commercial desktop systems_ portable consumer devices, not industrial laser production machinery.

7. Therefore, in view of the above discussion, I am of the considered opinion that ADD as per Notification No. 15/2023-Customs (ADD) dated 22.12.2023 will not be imposable on the import of the subject products i.e. Laser Engraving Machines, subject to Customs Authority satisfaction with regard to physical verification and goods as per description in Bill of Entry at the time of import.

8. I rule accordingly.

Author Bio