Case Law Details

Southern Steels Vs Assistant Commissioner (ST) (Madras High Court)

The Madras High Court disposed of a batch of writ petitions concerning proceedings initiated under Section 74 of the respective GST enactments. The petitions formed part of a larger batch of 250 writ petitions, with 53 matters heard on the common issue relating to the invocation of the extended period of limitation under Section 74.

The petitioner challenged two sets of assessment orders passed under Section 74 in respect of two GST registrations at Gobichettipalayam and Erode. Both sets of proceedings originated from an inspection conducted on 09.09.2021. One set of writ petitions challenged orders dated 05.07.2023 for the assessment years 2017-18 to 2021-22, which had been passed after the petitioner had earlier succeeded in challenging ASMT-13 orders before the High Court. The earlier order dated 01.03.2022 had set aside the ASMT-13 orders and remitted the matters to the assessing authority for reconsideration after granting the petitioner an opportunity of personal hearing and access to records.

The second set of writ petitions challenged assessment orders that were preceded by an intimation in DRC-01A, a show cause notice in DRC-01, and replies filed in DRC-06. The confirmed tax liabilities for the respective assessment years were recorded in the impugned DRC-07 orders.

The Court noted that the proceedings stemmed from the inspection conducted on 09.09.2021. During scrutiny under Section 61, an ASMT-10 intimation dated 09.12.2021 had been issued following the inspection, which allegedly revealed circular or reciprocal transactions and the passing of fictitious Input Tax Credit on non-supplies to other taxpayers. On that basis, the respondents justified the proceedings under Sections 74 and 122 of the GST enactments.

The Court held that these facts prima facie justified the invocation of the extended period of limitation under Section 74. It observed that sufficient material arising from the inspection and subsequent proceedings supported the invocation of Section 74, and therefore the challenge to the extended limitation could not be sustained.

However, the Court found a procedural irregularity in the first set of writ petitions. It observed that once an ASMT-10 notice is issued and a reply is filed in ASMT-11, the proceedings should conclude through ASMT-12 or proceed with DRC-01A followed by DRC-01. Since ASMT-13 is applicable only in cases of non-filers of returns under Section 62 read with the Rules, issuance of ASMT-13 after ASMT-10 and ASMT-11 was not in consonance with the statutory scheme. The Court further held that, before passing the DRC-07 orders dated 05.07.2023 pursuant to the earlier remand order, the authorities ought to have issued a DRC-01 notice under Section 74. Accordingly, those impugned orders were set aside and directed to be treated as DRC-01 notices under Section 74 for fresh adjudication after complying with the principles of natural justice. The period during which the proceedings remained pending was directed to be excluded while computing limitation.

With respect to the second set of writ petitions, the Court found no procedural irregularity. It observed that the petitioner had participated in the inspection and the subsequent proceedings involving DRC-01A, DRC-01 and the assessment orders, and that adequate material existed to justify invoking Section 74. Consequently, those writ petitions were dismissed. However, the Court granted liberty to the petitioner to file statutory appeals within 30 days from receipt of the order, subject to depositing 50% of the disputed tax liability.

T OF THE JUDGMENT/ORDER OF MADRAS HIGH COURT

By this Common Order, all these writ petitions have been disposed of.

2. These cases were heard along with a batch of 250 writ petitions and as one of the 53 writ petitions which were finally heard on the larger issue regarding the challenge to the proceedings under Section 74 of the respective GST Enactments.

3. By a separate order today in W.P.Nos.2142 of 2026 [Turbo Energy Private Limited], W.P.Nos.35967 of 2024 [Fastenex Private Limited], W.P.Nos.14487 of 2025 [Ispahani Estates] etc., a detailed order has been passed insofar as the invocation of extended period of limitation under Section 74 of the respective GST Enactments.

4. In these writ petitions, the petitioners have challenged two separate sets of orders passed under Section 74 of the respective GST enactments in respect of two separate GST Registration of the petitioner at Erode and Gobichettipalayam, which were preceded by an inspection on 09.2021. The details of the impugned orders in the two sets of writ petitions are extracted below:

Table-I

GOBICHETTIPALAYAM [GSTIN: 33ADGFS0181D1Z11]

Table-2

ERODE, PERUNDURAI ROAD [GSTIN: 33ACVFS3268F1ZQ]

| S. No. | W. P. Nos. | TP | Date of Inspection | DRC-01A | DRC-01 | DRC-06 | DRC-07 |

| 1. | 21113/2 024 | 2017-2018 | 09.09.2021 | 07.12.2021 | 08.02.2022 | 12.03.2022 | 29.09.2023 |

| 2. | 21115/2 024 | 2018-2019 | 09.09.2021 | 07.12.2021 | 09.02.2022 | 12.03.2022 | 26.09.2023 |

| 3. | 21122/2 024 | 2019-2020 | 09.09.2021 | 07.12.2021 | 11.02.2022 | 12.03.2022 | 26.09.2023 |

| 4. | 21126/2 024 | 2020-2021 | 09.09.2021 | 07.12.2021 | 11.02.2022 | 12.03.2022 | 27.09.2023 |

| 5. | 21110/2 024 | 2021-2022 | 09.09.2021 | 07.12.2021 | 11.02.2022 | 12.03.2022 | 29.09.2023 |

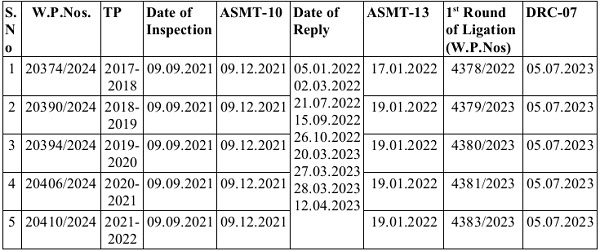

5. In W.P.Nos.20374, 20390, 20394, 20406 & 20410 of 2024, the petitioner has challenged the impugned orders dated 05.07.2023 passed for the Assessment Years 2017-2022, after having successfully challenged the ASMT-13 issued under Section 62 read with Rule 100(1) in the 1st round of litigation in W.P.Nos.4378, 4379, 4380, 4381 and 4383 of 2022.

6. This Court vide its Order dated 01.03.2022 had interfered with the ASMT-13. The relevant portion of the said order dated 01.03.2022 reads as under:

“16. In that view of the matter, this court is inclined to dispose of the writ petitions with the following directions:-

(i) That the impugned orders in each of these writ petitions are hereby set aside. The matters are remitted to the respondent for reconsideration. While reconsidering the same within a period of two weeks from the date of receipt of a copy of this order, a day may be fixed by the respondent and that shall be communicated to the petitioner. On the date, as the same shall be treated as a Personal Hearing date, the petitioner without fail, shall appear before the respondent with relevant documents, inputs, Books of Accounts, etc., with reply or defense anything and place all those documents and reply before the respondent in support of the cause of the petitioners.

(ii) This court feels that a chance may also be given to the petitioner in the morning session on the hearing date, to peruse the records and documents on the files of the respondent, so that an effective reply and defence can be made by the petitioner and after perusal of the records and in addition to that with further records and inputs, if any, available with the petitioner, an effective defense may be made by the petitioner in the afternoon session and considering the same, final orders can be passed by the respondent thereafter.”

7. Pursuant to the above Order dated 01.03.2022 in W.P.Nos.20374, WEB 20390, 20390, 20394, 20406 & 20410 of 2024 of this Court, Impugned Orders dated

05.07.2023 have been passed, which are subject matter of challenge in the writ petitions in Table-1. The petitioner has challenged the respective impugned orders passed in DRC-07 dated 05.07.2023, whereby the following amounts have been confirmed vide impugned orders challenged in the writ petitions in Table-1:

Table-3

| S. No. | W. P. Nos. | AY | DRC-07 | Tax Liability (In Rs.) |

| 1. | 20374/2024 | 2017-2018 | 05.07.2023 | 3329473 |

| 2. | 20390/2024 | 2018-2019 | 05.07.2023 | 8912397 |

| 3. | 20394/2024 | 2019-2020 | 05.07.2023 | 11565584 |

| 4. | 20406/2024 | 2020-2021 | 05.07.2023 | 15097489 |

| 5. | 20410/2024 | 2021-2022 | 05.07.2023 | 13375883 |

8. Impugned Orders in the writ petitions in Table-2 viz., W.P.Nos.21113, 21115, 21122, 21126 and 21110 of 2024 were preceded by an intimation in DRC-01A, a notice in DRC-01 and a reply of the petitioner in DRC-06. The amounts confirmed in the respective impugned orders are as under:

| S. No. | W. P. Nos. | AY | DRC-07 | Tax Liability (In Rs.) |

| 1. | 21113/2024 | 2017-2018 | 29.09.2023 | 3499390 |

| 2. | 21115/2024 | 2018-2019 | 26.09.2023 | 9012282 |

| 3. | 21122/2024 | 2019-2020 | 26.09.2023 | 8755050 |

| 4. | 21126/2024 | 2020-2021 | 27.09.2023 | 7163888 |

| 5. | 21110/2024 | 2021-2022 | 29.09.2023 | 2832004 |

9. Both the set of the impugned proceedings were preceded by an inspection on 09.09.2021. The contents of which would have been communicated to the petitioner in a notice in INS-01, and thereafter, in a report in INS-02. However, the pleading is silent on the same.

10. The impugned orders dated 05.07.2023 impugned in W.P.Nos.20374, 20390, 20394, 20406 & 20410 of 2024 indicates that the demand has been confirmed pursuant to the inspection held on 09.09.2021 and was followed by Notice in ASMT-10 and proceedings in ASMT-13 and DRC-07 passed between July 2023 and September 2023.

11. The scheme under the GST law has been spelt out in detail in the orders referred to in Paragraph No.2 of this order.

12. During scrutiny of Return under Section 61 of the respective GST enactments, a proposal/intimation in ASMT-10 dated 09.12.2021 was issued to the petitioner. This was in the background of inspection on 09.09.2021, wherein the petitioner was found to have been indulged in Circular / Reciprocal transactions, and for having passed on fictitious Input Tax Credit on non supplies to other Tax Payers. Thus, the proceedings have been justified by the respondent both under Section 74 and also Section 122 of the respective GST enactments.

13. The above facts prima facie justify the invocation of extended period of limitation under Section 74 of the respective GST enactments, as there is no doubt that there were adequate material available for justifying its invocation. This was in the light of inspection held on 09.09.2021, followed by an intimation in ASMT-10 and thereafter in ASMT-13, which were impugned in W.P.Nos.4378, 4379, 4380, 4381 and 4383 of 2022, and have culminated in order dated 05.07.2023, which are put to challenge in the present writ petitions in W.P.Nos.20374, 20390, 20394, 20406 & 20410 of 2024. Therefore, challenge to the invocation of extended period of limitation against the petitioner under Section 74 cannot be assailed.

14. Once ASMT-10 is issued and a reply is filed in ASMT-11, it has to either conclude in ASMT-12 or an Intimation in DRC-01A followed by a Notice in DRC-01. ASMT-13 is applicable only for non-filers of return under Section 62 read with Rule 10. Therefore, order under ASMT-13, after issuance of a Notice in ASMT-10 and a reply in ASMT-11 is puzzling and not in consonance with the scheme of the provision.

15. Before passing the impugned orders in DRC-07 dated 05.07.2023, pursuant to the earlier order of this Court dated 01.03.2022 in W.P.Nos.4378, 4379, 4380, 4381 and 4383 of 2022, a Notice in DRC-01 under Section 74 ought to have been issued. The impugned orders dated 05.07.2023 have been issued perhaps, in view of the order passed on 01.03.2022 earlier in W.P.Nos.4378, 4379, 4380, 4381 and 4383 of 2022. Therefore, the impugned orders dated 05.07.2023, are liable to be set aside for de novo adjudication, by treating them as notice in DRC-01 under Section 74.

16. Insofar as the impugned orders challenged in W.P.Nos.21113, 21115, 21122, 21126 and 21110 of 2024 are concerned, they cannot be interfered with, as no procedural irregularity has been committed by the respondent, while passing these orders. The petitioner was privy to the inspection conducted on 09.09.2021 and the subsequent proceedings viz., Intimation in DRC-01A followed by a Show Cause Notice in DRC-01 and thereafter the Impugned Assessment Order. There are adequate materials on record to inform the petitioner of the lapses to invoke Section 74 of the respective GST enatments. in view of the decision in the Common Order passed today in a batch by separate orders. There, it has been explained in detail that the threshold for invoking the extended period of limitation under Section 74 of the respective GST enactments is much lower compared to the threshold under earlier Indirect Tax Legislations.

17. In the result,

(i) The Writ Petitions in W.P.Nos.20374, 20390, 20394, 20406 & 20410 of 2024 are disposed of by setting aside the impugned orders dated 05.07.2023 passed by the respondent.

(ii) The above impugned orders dated 05.07.2023 shall be treated as DRC-01 notices under Section 74. The respondent shall thereafter pass orders, after complying with the principles of natural justice. The time during which proceedings are pending shall stand excluded for computation of limitation.

(iii) Since Writ Petition Nos.21110, 21113, 21115, 21122 & 21126 of 2024 are liable to be dismissed, and are dismissed. Liberty is given to the petitioner to file appeals against the impugned orders dated 05.07.2023, within a period of 30 days from the date of receipt of a copy of this order, subject to the petitioner depositing 50% of the disputed tax liability, within the aforesaid period. No costs. Connected miscellaneous petitions are closed.

Author Bio