Case Law Details

MPS Structure Private Limited Vs DCIT (ITAT Delhi)

The Income Tax Appellate Tribunal (ITAT), Delhi, allowed the assessee’s appeal by holding that the proceedings initiated under Section 153C of the Income Tax Act were invalid because the jurisdiction was assumed on the basis of a defective and composite satisfaction note that did not contain assessment year-wise bifurcation or correlate the seized material to the relevant assessment year.

The case arose from a search conducted on 22 October 2016 in the Ashish Bhegwani Group. During the search, the Revenue alleged that the assessee had received accommodation entries in the form of unsecured loans from entities controlled by the searched person. Based on a satisfaction note recorded by the Assessing Officer (AO) of the searched person and a subsequent satisfaction note recorded by the AO of the assessee, proceedings under Section 153C were initiated for Assessment Years 2011-12 to 2017-18. The AO treated an unsecured loan of ₹4.98 crore as an unexplained cash credit under Section 68 and also added ₹14.94 lakh as commission allegedly paid for obtaining the accommodation entry, resulting in a total assessed income of ₹5.16 crore. The Commissioner (Appeals) upheld these additions, following which the assessee approached the Tribunal.

Before the Tribunal, the assessee challenged the very assumption of jurisdiction under Section 153C, arguing that the satisfaction note was common for multiple assessment years and failed to identify the incriminating material relating to each individual assessment year. According to the assessee, the note merely referred to an Excel sheet without providing year-wise details or correlating the alleged undisclosed transactions with the year under appeal, rendering the satisfaction defective. The Revenue argued that, after insertion of Section 292BC, defects relating to approvals should not invalidate proceedings.

The Tribunal rejected the Revenue’s contention, observing that a satisfaction note is distinct from an administrative approval and that Section 292BC applies only to approvals, not to the statutory requirement of recording satisfaction before initiating proceedings under Section 153C. It found that the satisfaction note contained no reference to any specific incriminating material pertaining to the assessment year under appeal, nor did it provide any year-wise bifurcation of the alleged undisclosed transactions. The Tribunal held that such a composite satisfaction note was legally defective.

In reaching its conclusion, the Tribunal relied upon several judicial precedents, including the Karnataka High Court decision in Sunil Kumar Sharma, whose view was affirmed by the Supreme Court through dismissal of the Revenue’s Special Leave Petition. It also referred to earlier Delhi Tribunal decisions, including Honda R & D (India) Private Limited, Super Bazar Stores Pvt. Ltd., and SRS Panchratan Diamonds Pvt. Ltd., as well as the Delhi High Court’s decision in Saksham Commodities Ltd. These decisions consistently held that a valid satisfaction note under Section 153C must identify incriminating material with reference to each assessment year and cannot merely rely on a consolidated or generic satisfaction covering multiple years.

The Tribunal observed that the Assessing Officer had not referred to any material specifically relating to the year under appeal and had made only general observations. It held that a combined satisfaction note, without separate year-wise figures and without correlating the seized material to the relevant assessment year, failed to satisfy the statutory requirement for assuming jurisdiction under Section 153C. Consequently, the assessment order passed under Section 153C was held to be bad in law and was quashed. Since the Tribunal allowed the appeal on the jurisdictional issue, it treated the remaining grounds relating to the additions under Sections 68 and 69C as academic and did not adjudicate them. Accordingly, the assessee’s appeal was allowed.

FULL TEXT OF THE ORDER OF ITAT DELHI

This appeal is filed by the assessee against order of Learned Commissioner of Income Tax (Appeals)-24, New Delhi dated 20.05.2025 u/s 250 of the Income Tax Act, 1961 (“the Act” in short) arising out of the assessment order passed u/s 153C of the Act dated 29.12.2022 for Assessment Year 2016-17.

2. Briefly stated the facts are that a search and seizure action u/s 132 of the Income Tax Act, 1961 was carried out in the case of Ashish Bhegwani Group of cases on 22.10.2016. During the course of search, it was found that he was providing accommodation entries through various concerns after charging commission to various beneficiaries and one of such beneficiary was the assessee company who had taken accommodation entry from entities controlled by Sh. Ashish Bhegwani and Ors. Accordingly, the AO of the person searched i.e. Ashish Bhegwani has recorded the satisfaction note on 25.12.2021 and handed over the seized material along with the satisfaction note to the AO of the assessee. The AO of the person other than person searched i.e. the AO of the assessee has recorded the satisfaction on 31.12.2021 and initiate the proceedings u/s 153C of the Act for AY 2011-12 to AY 2017-18 and notice u/s 153C for all the years were issued. The assesse has filed the return of income u/s 139(1) on 15.02.2017 declaring total income at Rs.3,81,730/- and in response to notice u/s 153C of the Act, same income was declared in the return filed on 19.11.2022. The AO based on the information found as result of search that assessee has taken accommodation entry in the shape of loan from the companies managed and operated by Sh. Ashish Bhegwani, observed that loan of Rs. 4.98 crores was received from M/s Sesun Marketing Pvt. Ltd. who is one of the lender and accordingly, the assessee was asked to establish the genuineness of the loans so taken. After considering the submissions and the material found as a result of search, the AO concluded that M/s Sesun Marketing Pvt. Ltd. is company managed and controlled by Sh. Ashish Bhegwani has provided accommodation entry of unsecured loan and, therefore, the loan given to the assessee is bogus loan and made the addition of Rs .4.98 crores u/s 68 of the Act. The AO further made the addition of Rs.4,94,000/- being commission @ 3% for obtaining the accommodation entry of such loan and accordingly, the total income of the assessee was assessed at Rs.5,16,75,730/.

3.Against the said order, the appeal filed by the assessee before the Ld. CIT(A) wherein the assessee has challenged the addition so made, however, Ld. CIT(A) in terms of the impugned order dated 20.05.2025 has dismissed the appeal of the assessee.

4. Aggrieved by the said order, the assessee is in appeal before the Tribunal by taking following grounds of appeal:

“1. That having regard to the facts and circumstances of the case, Ld. CTT(A) has erred in law and on facts in confirming the action of Ld. AO in passing the impugned assessment order u/s 153C and that too without assuming jurisdiction as per law and without recording mandatory ‘satisfaction in accordance with law and without complying/following with the other mandatory conditions/procedure as laid down u/s 153C in accordance with law.

2. That having regard to the facts and circumstances of the case, the assumption of jurisdiction u/s 153C, is illegal, bad in law and against the facts and circumstances of the case and the same is not sustainable on various legal and factual grounds.

3. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law and on facts in confirming the action of Ld. AO in making addition of Rs.4,98,00,000/- on account of unsecured loan by treating it as alleged unexplained credits u/s 68 and that too by recording incorrect facts and findings and without following the principles of natural justice and without confronting the adverse material on record and without providing the opportunity of cross examination.

4. That in any case and in any view of the matter, action of Ld. CIT(A) in confirming the action of Ld. AO in making addition of Rs.4,98,00,000/- on account of unsecured loan u/s 68, is bad in law and against the facts and circumstances of the case.

5. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law and on facts in confirming the action of Ld. AO in making addition of Rs. 14,94,000/- on account of alleged commission paid by treating it as alleged unexplained expenditure u/s 69C of Income Tax Act, 1961.

6. That in any case and without prejudice to the above grounds, additions made in the impugned assessment order is beyond jurisdiction and illegal, also for the reason that such order could not have been made since no incriminating material has been found as a result of search.

7. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law and on facts in quashing the impugned assessment order passed by Ld. AO without there being requisite approval in terms of section 153D and in any case approval, if any, is mechanical without application of mind and is no approval in the eyes of law.

8. That the appellant craves the leave to add, modify, amend or delete any of the grounds of appeal at the time of hearing and all the above grounds are without prejudice to each other.”

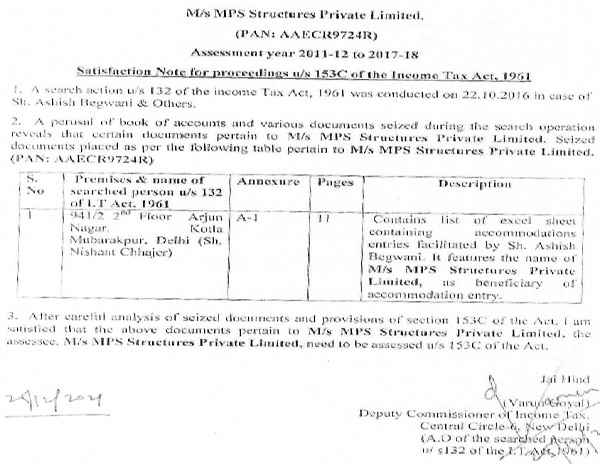

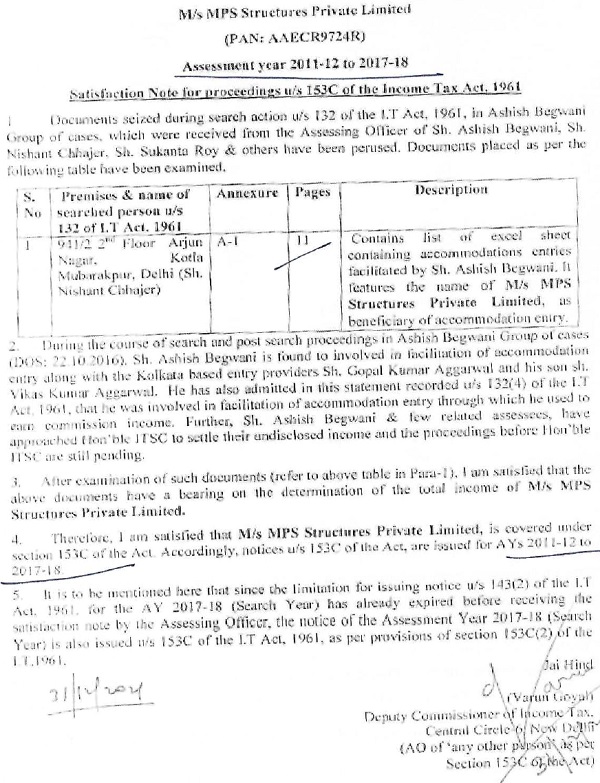

5. Grounds of appeal No. 1 & 2 are with respect to the initiation of proceedings u/s 153C of the Act on the basis of defective satisfaction recorded. The Ld. AR for the assessee drew our attention to page 3 & 4 of the assessment order which is the copy the satisfaction note recorded by the AO of person searched and of the AO of person other than the person searched .i.e. AO of the assessee are reproduced. The Ld. AR submits that the jurisdiction was assumed through the common satisfaction note recorded for various assessment year starting from AY 2011-12 to AY 201718, where no further efforts were made to co-relate the seized material referring as Annexure A1 having total pages 11, to each individual assessment year nor any assessment year wise break-up of the amount alleged as undisclosed transactions were stated. As per the Ld. AR ,the common and composite satisfaction note was recorded without corelating the seized material with the year under appeal. He therefore, submits that such satisfaction note is defective and based on the said satisfaction note, proceedings initiated u/s 153C of the Act deserves to be hold bad in law. Reliance is placed on the judgment of the Hon’ble Karnataka Court of in the case of DCIT vs. Sunil Kumar Sharma, reported in 469 ITR 271 (Kar.). It is further stated that such order stood confirmed by Hon’ble Supreme Court by dismissing the SLP of the Revenue as reported in 469 ITR 197 (SC). The Ld. AR submits that based on the following aforesaid judgment, the Co-ordinate Delhi Benches of the Tribunal in numerous cases has held the assumption of jurisdiction u/s 153C as invalid, defective and quashed the order passed u/s 153C of the Act. He thus prayed accordingly.

6. On the other hand, the Ld. Sr. DR submits that approval granted for initiation of proceedings u/s 153C as now been the settled in terms of the amendment in the statute by inserting section 292BC in the Act wherein it is provided that the approval granted under any section of the Act after 01.04.2021 would be deemed to be administrative approval and does not vitiate the proceedings initiated based on such approval. It is therefore, requested that even if the argument of the assessee is accepted of common satisfaction note, the consequent order passed should not be quashed merely on the basis of such defective approval. She prayed accordingly.

7. Heard the parties and perused the materials available on record. In the instant case, while initiating the proceedings u/s 153C of the Act, the satisfaction note was recorded by the AO of the person searched and by the AO of other person i.e. the AO of the assessee which are reproduced as under:

–

–

8. From the perusal of the above, satisfaction note it is observed that in the satisfaction note no reference is made of any particular entry found recorded in the seized material related to the assessee for the year under appeal which was not disclosed and in the said satisfaction note merely a reference is made of the excel sheet containing the accommodation entries provided by Sh. Ashish Bhegwani. However, no such excel sheet was supplied along with satisfaction note. It is observed that year wise bifurcation of the seized material so as to reached to the satisfaction that certain undisclosed transactions were carried by the assessee for which proceedings u/s 153C could be initiated has not been given in the satisfaction note which leads the such satisfaction note as defective.

9. Regarding the argument of the Revenue that after insertion of section of 292BC in the statute, such approvals cannot be held as defective, on or after 01.04.2021 and should be treated as administrative approval, in our considered opinion, the satisfaction note recorded before initiation of proceedings u/s 153C of the Act does not fall under the category of “approval” as provided in section 292BC of the Act. There is difference between “satisfaction” by the Ao for initiating any proceedings and obtaining approval from the higher authorities and both cannot be equated and, therefore, the provisions of section 292BC of the Act cannot be applied in the instant case.

10. Now coming to the issue of common and composite satisfaction for various assessment years, as observed above, the AO has referred certain excel sheet containing the entries of accommodation entry facilitated by Sh. Ashish Bhegwani, however, these loan alleged as accommodation entry were taken through banking channel and all the necessary details were filed by the assessee, therefore, the same cannot be treated as unexplained for which the proceedings u/s 153C could cbe initiated. Under identical circumstances in the case of Honda R & D (India) Private Limited vs. DCIT in ITA No.2459/Del/2025 vide order dated 06.02.2026, the Coordinate Bench of the ITAT Delhi by placing reliance on the judgment of the Hon’ble Supreme Court in the case of Sunil Kumar Sharma (supra) and further on the judgment of Hon’ble Delhi High Court in the case of Shaksham Commodities reported in [2024] 161 taxman.com has held the satisfaction note as defective and quashed the consequent order passed u/s 153C of the Act. The relevant observations as contained in para 7 & 8 of the order are reproduced as under:

“16. Now let us come to the satisfaction note recorded by the Learned AO of the assessee herein. The Learned AO of the assessee herein recorded satisfaction note on 15-12-2022 assuming jurisdiction under section 153C of the Act which is enclosed in Pages 5 to 15 of the Paper Book. It is pertinent to note that the Learned AO of the assessee had recorded single and consolidated satisfaction note for Assessment Years 2015-16 to 2021-22. For the sake of convenience, the last paragraph of the satisfaction note dated 15-12-2022 recorded by the Learned AO of the assessee herein is reproduced below:-

“The above satisfaction notes recorded as the AO of the person searched has been placed on record. As AO of the person other than the searched person, I have also examined the above referred seized material and the contents of the same. After examining the entries in these documents, I am satisfied that these documents pertain to M/s Gulshan Homes and Infrastructure Pvt. Ltd. and entries appearing therein have a bearing on the determination of the income of M/s Gulshan Homes and Infrastructure Pvt. Ltd. In view of the same, I am satisfied that it is a fit case for initiating proceeding under Section 153C r.w.s. Section 153A of the IT Act, 1961 for the assessment years 2015-16 to 2021-22.”

17. From the above, it could be seen that the Learned AO of the assessee herein had recorded consolidated satisfaction note for the Assessment Years 2015-16 to 2021-22. Whether recording of consolidated satisfaction note for various assessment years would prove fatal to the assumption of jurisdiction of the Learned AO and consequential framing of assessments under section 153C of the Act was subject matter of consideration by the Hon’ble Karnataka High Court in the case of DCIT vs Sunil Kumar Sharma reported in 159 taxmann.com 179 (Karnataka) dated 22-1-2024, wherein it was held as under:-

“53. Further, satisfaction note is required to be recorded under section 153C of the IT Act for each Assessment Year and in the impugned proceedings, a consolidated satisfaction note has been recorded for different Assessment Years, which also vitiates the entire assessment proceedings. In view of all these findings, it is said that the appeals do not have any substance for seeking as sought for by the intervention appellant/Revenue.

17.1. We find that the Special Leave Petition filed by the revenue before the Hon’ble Supreme Court against the aforesaid judgement was dismissed which is reported in 165 taxmann.com 846 (SC). The relevant portion of the Head Notes and the order of Hon’ble Apex Court is reproduced hereunder:-

“Section 153C, read with sections 132, 153 and 153A, of the Income-tax Act, 1961 Search and seizure Assessment of any other persons (General principles) Assessment years 2012-13 to 2018-19 High Court held that satisfaction note is required to be recorded under section 153C for each assessment year and where a consolidated satisfaction note had been recorded for different assessment years, it would vitiated entire assessment proceedings- Whether SLP filed against impugned order of High Court was to be dismissed-Held, yes [Para 3] [In favour of assessee].

ORDER

1. Delay condoned.

2. Heard the learned Senior Counsel appearing for the appellants.

3. We are not inclined to interfere with the impugned judgment and order passed by the High Court of Karnataka at Bengaluru in Writ Appeal No. 831/2022 (T-IT) dated 22-01-2024/Deputy Commissioner of Income-tax v. Sunil Kumar Sharma [2024] 159 com 179 (Karnataka).

4. The Special Leave Petition is dismissed.

5. Pending application(s), if any, shall stand disposed of.

18. The Learned AR before us vehemently argued that the satisfaction note prepared by the AO of the assessee is still more audacious. The imaged messages are reproduced therein and legible copy is reproduced in para 4.2 to para 4.7 of the assessment order and the name of the assessee nowhere figures in these messages. As shown in para 4.2, the impugned images were found from the mobile phone of Shri Parveen Jain received from his son, Shri Vaibhav Jain and it shows nine names, Sita Gupta to Sanjeev Gupta-but name of the assessee is not there at all. Identical is the situation in para 4.4 of the assessment order. The Learned AR stated that it is beyond any sane comprehension that when name of the assessee is not even mentioned in the alleged seized documents, how could, the AO of the searched person, be satisfied that the alleged seized material belonged to the assessee or the alleged information pertained to the assessee. reasons to rope in the assessee are contained in para 4.5 to para 4.10 of the assessment order. The sheets bearing the names of nine parties therein and definitely not of the assessee, was analysed by the revenue to come to the conclusion that the items denoted with ‘C’ were cash entries and with ‘B’ were bank entries. The revenue proceeded to examine the bank entries and certain individuals were found and traced on Insights and other The Income-tax Database who were supposedly paying the impugned amount. Now, on examination of the matter related to Ms Sita Gupta, first out of the nine entries, the AO claimed to have detected that she had received interest from Gulshan Homes and Infrastructure Pvt Ltd -the assessee herein. The Investigation Unit thereafter and not the AO of the assessee, collected details etc. from the assessee company and as is mentioned in the para 4.15 of the assessment order, the total amount of the alleged cash receipt/ interest was interpolated which did not at all figure in the impugned seized WhatsApp chat. Noteworthy, the name of the assessee was not at all appearing in any seized material. The ld. Counsel further elaborated that the revenue has relied on a WhatsApp chat between Mr Praveen Jain and Mr Sanjeev Gupta as is mentioned in para 4.1 of the assessment order, where Mr Praveen Jain was requesting Mr Sanjeev Gupta to arrange 1/- for some Gulshan ji and not at all for the assessee company. This even does not say what is 1/ or whether it was arranged or not. It also does not at all mention whether it was cheque amount or cash amount. It is also not known whether the same was to be given only to which Gulshan ji (as the name of the assessee is conspicuously absent therein and no presumption at all could be derived that it belonging to the assessee) as loan in cash or for some property to be purchased by Mr Sanjeev Gupta from the assessee or from some other entity belonging to the group of Shri Gulshan Nagpal, if at all, it was he. However, on confrontation by the revenue officer, Mr Sanjeev Gupta categorically stated that he did not know whether it was bank or cash.

19. The Learned AR then submitted that after receipt of the material from the AO of the searched person, the Learned AO of the assessee was required to be satisfied that the material sent by the AO of the searched person (cloned data of Shri Parveen Jain’s mobile vide seized document reference Annexure A-5) or any information therein ever belonged/ pertained to the assessee herein. As against this patent position of law, the AO of the assessee has used data from the Appraisal report (para 2 of assessment order) as below in his satisfaction note:

i. Para 4- Upon this co-relation, various individuals were found and traced on Insight portal and other Income Tax database.

ii. Para 5- Sita Gupta was found to have received interest from Gulshan Homes along with TDS

iii. Para 8. From the TDS analysis above, it is clear that the amount of interest paid to Shikha is in 7 transactions….

iv. Para 9-further, additional evidences in the form of WhatsApp conversation between Sanjiv Gupta and Parveen Jain…

υ. Para 10- Therefore, summons were issued to Gulshan Homes on 18/08/2021 (a date definitely prior to the satisfaction note of the AO of the searched person) to provide ledger account and interest payment details to parties against whom any bank account was reflected……………… The response received from Gulshan Home establishes the bank transactions…. account

vi. Para 11- Upon examining of various ledger accounts submitted on behalf of Gulshan Homes, the initial point of providing loan.

vii. Para 12 is sufficient proof that this satisfaction note is copy of Appraisal report. It is mentioned that ‘additionally AO may consider calculating the cash interest amount paid as addition in the hands of Gulshan…’ and ‘the monthly interest and date of payment of principle amount is mentioned above for the perusal of AO’.

viii-Para13- it is clear that the sheet found is summary of undisclosed investments facilitated of various clients by Parveen in Gulshan Homes and he himself has invested through wife Seema Jain and person known as Mama..

ix. Para 14 Further, Sh. Gulshan Nagpal was called on 16/09/2021 (a date definitely prior to the satisfaction note of AO of the searched person) for personal examination u/s 131(1A)…

(emphasis supplied by us)

20. The Learned AR submitted that that the Learned AO of the assessee was only required to be satisfied vis-a vis the seized material handed over by the AO of the searched person without any reference to any other information or document even if in his possession received from any source. The satisfaction note based upon the appraisal report, data on Insight Portal regarding TDS of third parties, statements of Shri Gulshan Nagpal etc and therefore, is legally untenable and void ab initio. Moreover, this is not a satisfaction note to initiate any proceedings under section 1530 of the Act but conclusions regarding undisclosed income drawn in a firm language. The Hon’ble Supreme Court in Oryx Fisheries Put Ltd in Civil Appeal No. of 2010 (Arising out of Special Leave Petition (C) No.27615/08) on 29-10-2010 has held that:-

“28. It is no doubt true that at the stage of show cause, the person proceeded against must be told the charges against him so that he can take his defence and prove his innocence. It is obvious that at that stage the authority issuing the charge sheet, cannot, instead of telling him the charges, confront him with definite conclusions of his alleged quilt. If that is done, as has been done in this instant case, the entire proceeding initiated by the show cause notice gets vitiated by unfairness and bias and the subsequent proceeding become an idle ceremony.

29. the stage of show cause notice itself. Such a close mind is inconsistent with the scheme of Rule 43 which is set out below. The aforesaid rule has been framed in exercise of the power conferred under Section 33 of The Marine Products Export Development Authority Act, 1972 and as such that Rule is statutory in nature.

31.It is of course true that the show cause notice cannot be read hyper-technically and it is well settled that it is to be read reasonably. But one thing is clear that while reading a show-cause notice the person who is subject to it must get an impression that he will get an effective opportunity to rebut the allegations contained in the show cause notice and prove his innocence. If on a reasonable reading of a show-cause notice a person of ordinary prudence gets the feeling that his reply to the show cause notice will be an empty ceremony and he will merely knock his head against the impenetrable wall of prejudged opinion, such a show cause notice does not commence a fair procedure especially when it is issued in a quasi- judicial proceeding under a statutory regulation which promises to give the person proceeded against a reasonable opportunity of defence.” The Id. Counsel stated further that in fact, in the present case, the assessment order is substantially repetition of the satisfaction note. Gravamen of the above is that the AO was unable to arrive at the requisite satisfaction, solely based upon the seized material received but relied upon the external material which makes the entire proceedings bad in law ab initio.”

21. In view of the aforesaid observations and respectfully following the various judicial precedents relied upon hereinabove, we hold that the Learned AO had invalidly assumed jurisdiction under section 153C of the Act for more than one reason as detailed supra and hence the entire search assessment is hereby declared as void ab initio. Accordingly, the Ground Nos. 1,2,3,4,5,8 & 9 raised by the assessee are allowed.”

11. Further the Co-ordinate Bench of Tribunal in the case of Super Bazar Stores Pvt. Ltd. in ITA No.9757/Del/2020 considered the judgement of Hon’ble High Court in the case of Saksham Commodities Ltd. (supra) has held the common satisfaction as invalid, the relevant observations are as under:-

11. “Now coming to the issue of validity of the satisfaction note and initiation of the proceedings in the hands of assessee company based on such satisfaction note u/s 153C of the Act. Before us, the contention of the AR is that satisfaction note was recorded without referring to any incriminating material and collectively in assessment order for Assessment Year 2012-13 to 2018-19 without identifying any incriminating material having entries for each individual assessment year. From the perusal of the satisfaction note so recorded as reproduced hereinabove, we find that the satisfaction note had the reference of gross amounts of credit entries in the bank accounts maintained by the assessee company which are disclosed bank account and cannot be held as incriminating material. Therefore, the entries contained therein cannot be held as unexplained. Moreover, we are in agreement with the contention of the AR that in the satisfaction note no year wise transactions were reported which could be held as incriminating for which the proceedings u/s 153C were initiated. Identical issue was came before the Coordinate Bench for consideration in the case of Super Bazar Stores Pvt. Ltd. in ITA 9757/Del/2019 wherein the Co-ordinate Bench after considering the facts has held that the satisfaction note so recorded is vague and non-descriptive and quashed the consequent orders passed u/s 153C of the Act. The relevant observations of the Co-ordinate Bench wherein the Co-ordinate Bench has followed the judgment of the jurisdictional High Court in the case of Saksham Commodity Ltd. vs. ITO reported 161 txmann.com 483 and made the following observations:

“11. The assessee contends that ‘satisfaction note’ which is the first step for assumption of jurisdiction under s. 153C of the Act and provides foundation for conferment of jurisdiction is plagued with multiple legal infirmities. Viz:

i. the ‘satisfaction note’ has been recorded by the AO of assessee collectively for the period AYs 2010-11 to AY 2015-16 without identifying the incriminating material in respect of any particular Assessment Year. Besides, the assessee company itself has come into existence by Certificate of incorporation dated 03.01.2013 and therefore, the company was not in existence in AY 2010-11 to AY 2012-13 covered in the ‘satisfaction note,

ii. the AO has thrown upon whole basket of six months without giving reference to any concrete incriminating material of a particular Assessment Year and without taking note of commencement of activities of assessee;

iii. the act of the AO making sweeping averment in the ‘satisfaction note that documents in the form of hard disks have bearing on determination of total income of Super Bazar Stores Pvt. Ltd. for AYs 2010-11 to 2015-16, is without legal foundation and without application of mind, as the AO has even failed to name the alleged documents and further failed to mention as to how it is related/pertained to a given AY covered in the ‘satisfaction note’;

iv. the AO on receipt of material/documents from the AO of the searched person must necessarily apply his mind on the material received and ascertain precisely the specific year to which incriminating material relates. It is only when this determination/ascertainment is complete that the flood gates of an assessment would open qua those particular years. The issuance of notice cannot be an automated function unconnected to this exercise of analysis and ascertainment by the AO in the light of judgement rendered in the case of Agni Vishnu Feature Put.Ltd. vs DCIT (2023) 157 com 242 (Madras). In the instant case, non-application of mind on material supplied to AO is obvious as the company itself was not in existence for sizable period covered in proceedings under s. 153C of the Act;

v. the ‘satisfaction note’ is clearly very generic and devoid of any basic detail of the transaction in question.

12. We find ostensible potency in the plea of assessee towards allegation of legal infirmities in the ‘satisfaction note’. The Hon’ble Delhi High Court in the case of Sakham Commodities Ltd. Vs ITO 161 taxmann.com 485 (Delhi) deftly expounded the imperatives of a ‘satisfaction note’, and observed that unearthing of incriminating material in respect of particular AY will not automatically confer jurisdiction to invoke section 153C of the Act in respect of all the AYs mentioned therein. The Hon’ble Delhi High Court further observed that discovery of material for a particular AY is not intended to trigger a chain reaction or have a water fall effect on all the AYs which can form part of the ‘relevant AYs’ under section 1530 Of the Act. The Hon’ble Delhi High Court underscored well settled distinction which the law recognizes between the existence of power and the exercise thereof and thus, held that unless the AO is satisfied that the material gathered can potentially impact the determination of total income, it will be abrupt exercise of powers in mechanically re-opening or assessing all over again of the AYs covered in the block that could possibly form part of block of relevant AYs. For holding so, the Hon’ble Delhi High Court relied upon the judgement delivered by the Hon’ble Supreme Court in the case of Sinhgad Technical Education Society wherein the Hon’ble Supreme Court held that the assessment under section 153C could be made only for the year to which material relates to and exercise of power under section 153C of the Act in respect of other AYs would not sustain. The Hon’ble Delhi High Court also noted that the AO is bound to ascertain and identify the AY to which the material recovered relates and relevant AYs which can then be subject to action under section 153C of the Act will have to be necessarily those in respect of which the assessment is likely to be influenced or impacted by the material discovered. The Hon’ble Delhi High Court went one step further to hold that where material discovered in the course of search has the potential of constituting incriminating material for more than one AYs, even in such a situation, it will be incumbent upon the AO to duly record reasons that material is likely to be incriminating for more than one AY and thus, warranting the action under section 153C of the Act for years in addition to those to which material may be directly relatable. Thus, a nuanced application of mind and recording of reasons for drawing satisfaction as contemplated under section 153C of the Act qua different AYs is paramount. The Hon’ble Delhi High Court noticeably held that issuance of a notice under section 153C of the Act is clearly not intended to be an inevitable consequence to the receipt of material by the Jurisdictional AO and that the initiation of action under section 153C of the Act will have to be founded on a formation of opinion by the Jurisdictional AO that the material handed over and received pursuant to a search is likely to influence the determination of total income and would be relevant for the purposes of assessment/re-assessment in terms of section 153C of the Act.

13. The observation of the Hon’ble Delhi High Court noted above, clearly provides vehement support to the plea taken by the assessee on aspects of jurisdiction flowing from ‘satisfaction note’. The ‘satisfaction note’ under scrutiny defies most of the parameters expected of him while drawing satisfaction. While exercising the power under section 153C of the Act, neither has the AO related the material found in the course of search with a particular AY while making a consolidated ‘satisfaction note’ for several years nor provided any requisite details of transaction to enable an independent person to ascertain and form any independent opinion on facts stated in Note that invocation of section 153C of the Act is indeed warranted in the facts of the case. The AO has not even bothered to relate the so-called documents etc. with the AYs covered. The assessee company was non-existent in AY 2010-11; AY 2011-12; AY 2012-13, which were also covered under s. 153C in a non-chalant manner. Mere drawing of a perfunctory satisfaction without meeting basic ingredients of providing some tangible & descript information and application of mind thereon has no standing in law and would not confer drastic jurisdiction of assessment u/s 153C of the Act on a person other than searched person. The jurisdiction assumed based on such lackadaisical ‘satisfaction note’ beset with vital infirmities cannot be countenanced in law. The objections raised on behalf of the assessee towards lack of jurisdiction based on a cryptic and non-descript satisfaction thus deserves to be sustained. While recording a consolidated ‘satisfaction note’ is not a bar in law per se as rightly contended on behalf of the revenue, but however, in the same vain, the documents/assets searched need to be specified against each year covered in the satisfaction note to depict application of mind and initiation of action under section 153C of the Act qua such assessment years. The AO has apparently failed to do so in the present case. As a corollary, the notice issued under section 153C of the Act and consequent assessment order passed under section 153C of the Act is vitiated in law and requires to be quashed.

14. In this view of the matter, the jurisdiction assumed under s. 153C based on vague and non-descript ‘satisfaction note’ is vitiated at the threshold. The consequence assessment order passed under s 153C thus has no force of law. The first appellate order passed on non-est assessment order is thus set aside and the AO is directed to restore the position claimed by the assessee and delete the additions made.

15. In the result, the appeal of the assessee is allowed.”

12. Further the Hon’ble Supreme Court in case of Sunil Kumar Sharma (supra) while dismissing the SLP filed by the Revenue expressed the same view. It is also observed that in the case of SRS Panchratan Diamonds Pvt. Ltd. vs DCIT in ITA No.218 & 219/Del/2023, the Co-ordinate Bench has considered all the relevant legal procurements and reached to the conclusion that the common satisfaction without providing yearwise break-up of the income which has direct bearing on the determination of total income of the assessee is a precondition for initiating the proceedings u/s 153C of the Act. Thus, by respectfully following the aforesaid judgment of Hon’ble Supreme Court and Hon’ble jurisdictional High Court, we are of the view that combined satisfaction note recorded by the AO of the assessee without providing any bifurcation of figures of various assessment years separately based on the incriminating material, is invalid satisfaction more particularly, when no material whatsoever is referred pertaining to the year under appeal and general observations have been made. Therefore, based on such invalid and incomplete statistician, consequent order u/s 153C of the Act is bad in law and therefore, the same is hereby quashed. Hence, Grounds of appeal Nos.1 & 2 raised by the assessee are allowed.

13. Since, we have allowed grounds of appeal No.1 & 2, thus remaining grounds of appeal are thus become academic and not adjudicated.

14. In the result, the appeal filed by the assessee is allowed.

Order pronounced in the open Court on 07.04.2026.

Author Bio