Case Law Details

Sudipta Traders Pvt. Ltd. Vs ITO (ITAT Kolkata)

The assessee filed an appeal before the Income Tax Appellate Tribunal (ITAT), Kolkata against the order of the Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (NFAC), Delhi for Assessment Year (AY) 2012-13. The principal grievance was that the CIT(A) had wrongly dismissed the assessee’s appeal as time-barred despite it having been filed within the prescribed limitation period.

The assessee had filed its return of income for AY 2012-13 on 29.09.2012 declaring a total loss of ₹70,857. During assessment proceedings, the Assessing Officer (AO) examined the share capital and share premium raised during the year. The AO observed that the assessee had failed to justify the high share premium and establish the creditworthiness of the investors despite being provided reasonable opportunity. Consequently, the AO treated the share premium of ₹2,69,50,857 and share capital of ₹11,20,000 as unexplained cash credits under Section 68 of the Income-tax Act, 1961. A total addition of ₹2,80,70,857 was made, and the assessee’s total income was assessed at ₹2,80,00,000.

The assessee challenged the assessment order before the CIT(A), explaining that although the assessment order was dated 21.03.2015, it was received by speed post only on 30.05.2015. According to the assessee, the appeal filed on 08.06.2015 was therefore within the prescribed limitation period. However, the CIT(A) held that the assessee had not furnished supporting documentary evidence to substantiate the claim regarding the date of receipt of the assessment order. Accordingly, the delay was not condoned, the appeal was dismissed as time-barred, and the additions made by the AO were confirmed.

Before the Tribunal, the assessee challenged the dismissal of its appeal on the ground of limitation. After considering the rival submissions and examining the record, the Tribunal found that the CIT(A) had dismissed the appeal on the ground of delay even though there was, in fact, no delay. The Tribunal noted that the assessment order dated 21.03.2015 had been served on the assessee on 30.05.2015 and that the appeal was filed on 08.06.2015. The assessee had also produced the scanned copy of the speed post envelope as evidence of the actual date of receipt of the assessment order.

Although the Departmental Representative relied upon the order of the CIT(A), no material was produced to dispute the date of receipt of the assessment order as evidenced by the speed post envelope.

After examining the facts and applicable law, the Tribunal held that the appeal had been erroneously dismissed as time-barred when there was no delay. It observed that the CIT(A) ought to have adjudicated the appeal on its merits instead of rejecting it on limitation.

Accordingly, the Tribunal set aside the order of the CIT(A) and restored the matter to the CIT(A) for fresh disposal of the grounds of appeal on merits by passing a speaking order. The Tribunal directed that the assessee should be given a reasonable opportunity of being heard and permitted to make further submissions in support of its case. It also directed that the assessee should not seek unnecessary adjournments, that Rule 46A of the Income-tax Rules, 1962 should be followed, and that an opportunity of hearing should be provided to the Assessing Officer wherever required.

FULL TEXT OF THE ORDER OF ITAT KOLKATA

This appeal filed by the assessee is against the order of the Commissioner of Income Tax (Appeals)-NFAC, Delhi [hereinafter referred to as Ld. ‘CIT(A)’] passed u/s 250 of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’) for AY 2012-13 dated 29.12.2025.

2. The assessee is in appeal before the Tribunal raising the following grounds of appeal:

“1. For that the Orders passed by the lower authorities are arbitrary, erroneous, without proper reasons, invalid and bad-in-law, to the extent to which they are prejudicial to the interests of the appellant.

2. For that the Ld. CIT(A), NFAC ought to have properly considered the reply of the appellant to his query and explanation in the matter of filing of the appeal alleged to be out of time and ought not to have proceeded to treat it not within the time allowed under Income Tax Act, 1961.

3. For that the Ld. CIT(A), NFAC incorrectly misconstrued the factual aspect of the case of the appellant in the matter of timely submission of appeal as explained on 15.12.2025 and ought not to have dismissed the appeal for disposal on the ground of the same being time barred.

4. For that the appellant duly explained having received Order of Assessment dated 21.03.2015 on 30.05.2015 by post and the appeal having been filed on 08.06.2015 was well within time.

5. For that the appellant craves leave to amend, alter, modify, substitute, add to, abridge and/or rescind any or all of the above Grounds.”

3. Brief facts of the case are that the assessee had filed the return of income for AY 2012-13 on 29.09.2012 declaring total loss of Z70,857/. During the assessment proceedings, the Assessing Officer (hereinafter referred to as Ld. ‘AO’) examined the share capital and share premium raised by the assessee during the year and observed that the assessee had failed to justify the high value of the share premium and to corroborate the creditworthiness of the investors despite reasonable opportunity. The Ld. AO treated the share premium of Z2,69,50,857/-and share capital of Z11,20,000/- as unexplained cash credits u/s 68 of the Act, added a sum of 22,80,70,857/- to the total income of the assessee and assessed the total income at 22,80,00,000/-. Aggrieved with the assessment order, the assessee filed an appeal before the Ld. CIT(A) with a delay, claiming that the assessment order dated 21.03.2015 was received via speed post on 30.05.2015 and the appeal was filed on 18.06.2015 and was filed in time. The Ld. CIT(A) noted that the assessee failed to furnish supporting documentary evidence for this claim and therefore, he did not condone the delay, dismissed the appeal of the assessee and thereby confirmed the additions made by the Ld. AO.

4. Aggrieved with the order of the Ld. CIT(A), the assessee has filed the appeal before the Tribunal.

5. Rival contentions were heard and the submissions made have been examined.

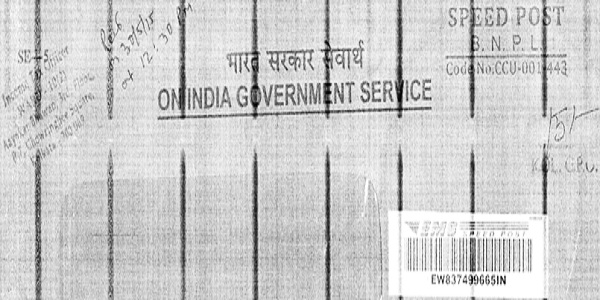

6. The Bench noted that the Ld. CIT(A) had dismissed the appeal of the assessee on account of delay while apparently there was no delay. The appellate order was passed on 21.03.2015 which was served on 30.05.2015 upon the assessee and the appeal was filed before the Ld. CIT(A) on 08.06.2015. The scan of the speed post envelope filed as evidence before us by the assessee as a proof of the date of receipt of the order is reproduced hereunder:

7. The Ld. DR relied upon the order of the Ld. CIT(A) and requested that the same may be upheld, but could not rebut the date of receipt of the order. We have considered the submissions made, gone through the facts of the case and perused the record and the order of the Ld. CIT(A). After examining the facts of the case and the law, the bench was of the view that the appeal was erroneously dismissed on account of delay while there was no delay and therefore, the same ought to have been decided on merits. We, therefore, deem it appropriate to set aside the order of the Ld. CIT(A) and restore the appeal to him for disposal of the grounds of appeal taken by the assessee on merits by passing a speaking order. Needless to say, the assessee shall be given a reasonable opportunity of being heard to make any further submission it wants to make in support of its grounds of appeal and shall not seek unnecessary adjournments and rule 46A of the I.T. Rules, 1962 shall also be followed and an opportunity of being heard may be provided to the Ld. AO, if required. Accordingly, the grounds taken by the assessee in the appeal are partly allowed for statistical purposes.

8. In the result, the appeal filed by the assessee is partly allowed for statistical purposes.

Order pronounced in the open Court on 22nd June, 2026.

Author Bio