Case Law Details

Jyoti Cariappa Saikia Vs ACIT (ITAT Delhi)

The assessee appealed before the ITAT Delhi against the order of the Commissioner of Income Tax (Appeals) [CIT(A)] for Assessment Year 2021-22, challenging proceedings initiated under section 153C of the Income-tax Act as well as the addition sustained under section 69A in respect of jewellery found during a search. The CIT(A) had granted partial relief by deleting part of the addition while sustaining an addition of ₹18,11,026 towards alleged unexplained jewellery.

The assessee raised legal grounds contending that the proceedings under section 153C were invalid because no incriminating material belonging to or relating to the assessee was found from any other searched person. It was argued that the jewellery had been found at the assessee’s own residence during the search and that, if at all, proceedings could only have been initiated under section 153A. The assessee also challenged the validity of the satisfaction note and the sustenance of the addition under section 69A, contending that the jewellery represented inheritance, streedhan, and jewellery accumulated over time.

The facts showed that a search under section 132 was conducted on the Triburg Group on 4 March 2021, during which the assessee’s residence was also searched. A notice under section 153C was issued after recording a satisfaction note, and the Assessing Officer completed the assessment by making an addition of ₹53,80,000 under section 69A on account of unexplained jewellery found during the search. The CIT(A) subsequently granted relief of ₹35,68,974 but sustained an addition of ₹18,11,026, leading to the present appeal.

Before the Tribunal, the assessee submitted that the sustained addition was arbitrary because documentary evidence explaining the source of the jewellery had been produced throughout the proceedings. The assessee relied upon the Will of her late mother, an affidavit from her brother, marriage photographs evidencing streedhan, and statements recorded during the search. It was argued that these explanations had been furnished from the very beginning and were consistently relied upon before the Investigation Wing, the Assessing Officer, and the CIT(A). According to the assessee, the Assessing Officer rejected the explanation merely by describing it as an “afterthought” without bringing any contrary material on record, while the CIT(A) failed to independently consider the Will and affidavit while sustaining the addition. The assessee further submitted that the jewellery explained through inheritance and purchase exceeded the total jewellery found during the search, leaving no unexplained jewellery liable to addition under section 69A.

The Revenue supported the orders of the lower authorities and argued that the claim of inheritance from the assessee’s mother was an afterthought. It submitted that the CIT(A) had already granted substantial relief after examining the available evidence and that the remaining addition should be upheld.

The Tribunal examined the material placed on record. It noted that the assessee was an employee of the searched company and had disclosed substantial income, including salary of ₹1.60 crore during the relevant year. During the search, jewellery weighing 1,758.93 grams valued at ₹1,25,89,817 was found, out of which jewellery worth ₹90,20,843 was seized. The assessee consistently explained that the jewellery comprised streedhan received at the time of marriage, jewellery purchased over time, and jewellery inherited from her mother.

The Tribunal further noted that the assessee produced purchase bills and corresponding bank statements evidencing jewellery purchases made between 2016 and 2021. It also examined the Will executed by the assessee’s late mother, the affidavit of the assessee’s brother, and the valuation report relating to inherited jewellery. Based on these documents, the assessee furnished reconciliations demonstrating that the inherited jewellery together with jewellery supported by purchase bills exceeded the jewellery found during the search.

FULL TEXT OF THE ORDER OF ITAT DELHI

This appeal by the assessee is directed against the order dated 03.02.2026 of the Commissioner of Income — tax (Appeals)-24, New Delhi [hereinafter referred to as the ‘W. CIT(A)] arising out of the Assessment Order dated 26.03.2025 passed under section 153C of the Income Tax Act, 1961 (hereinafter referred to as the ‘the Act’) by the Asst. CIT, Central Circle-5, New Delhi, (hereinafter referred to as the `AO’) pertaining to Assessment Years (A.Y.) 2021-22.

2. Grounds of appeal filed by the assessee are reproduced as under:

“1. That on the facts and in law, the order dated 03.02.2026 passed by the Ld. Commissioner of Income Tax (Appeals) [CIT(A)] under section 250 of the Income-tax Act, 1961 (“the Act’), partly affirming the assessment order dated 26.03.2025 passed under section 153C, is illegal, bad in law and void ab initio, as the mandatory statutory conditions for invoking section 153C were not satisfied .

2. That the Ld. CIT(A) erred in upholding proceedings under section 153C despite the admitted position that no incriminating material belonging to or relating to the assessee was found or seized from the premises of any other searched person, and that jewellery found and seized from the assessee’s own residential premises cannot, in law, constitute incriminating material of an “other person” for the purposes of section 153C.

3. Without prejudice and in alternative, the Ld. CIT(A) failed to appreciate that the assessee’s residential premises were covered under the search conducted under section 132 and jewellery was seized therefrom, rendering the assessee a “searched person”, and consequently, any assessment could only have been framed under section 153A and not under section 153C.

4. That the Ld. CIT(A) erred in law in upholding initiation of proceedings under section 153C despite the satisfaction notes dated 18.05.2023 being invalid and bad in law, as they: a) fail to record the mandatory satisfaction that the seized jewellery “belongs to” the assessee as required under section 153C(1); and b) are vague, mechanical, nonspeaking and do not identify or link any incriminating material to specific assessment years.

5. That the Ld. CIT(A) erred in law and on facts in confirming addition of V 8,11,026/-under section 69A on account of alleged unexplained jewellery, despite having categorically accepted that the jewellery represented accumulation over a long period, inheritance from mother, streedhan and customary receipts, and despite granting substantial relief on identical facts and evidence.

6. That the Ld. CIT(A) erred in restricting relief to jewellery worth X35,68,974/- merely on the ground that it was not seized, and in sustaining addition only in respect of seized jewellery, without drawing any qualitative, temporal or source-based distinction, rendering the partial confirmation arbitrary and unsustainable.

7. That having accepted that CBDT Instruction No. 1916 reflects the legislative intent to treat jewellery within prescribed limits as explained, the Ld. CIT(A) erred in not extending the benefit of the said Instruction to the entire jewellery found, including the seized portion, particularly when the appellant is a married lady married since 1977 and the total quantity of jewellery was reasonable and customary.

8. That the Ld. CIT(A) failed to adjudicate the specific ground that the Ld. Assessing Officer mechanically accepted jewellery of U2,09,817/- as explained merely on the basis= of purchase bills valued at historical cost, and once such inconsistent approach was demonstrated, the residual addition on account of jewellery was liable to be deleted in entirety.

9. That the Ld. CIT(A) erred in sustaining addition of V 8,11,026/- without recording any specific finding that such jewellery represented unexplained investment or undisclosed income of the relevant assessment year, and the confirmation is based purely on presumption and estimation, without any corroborative or incriminating material, contrary to section 69A.

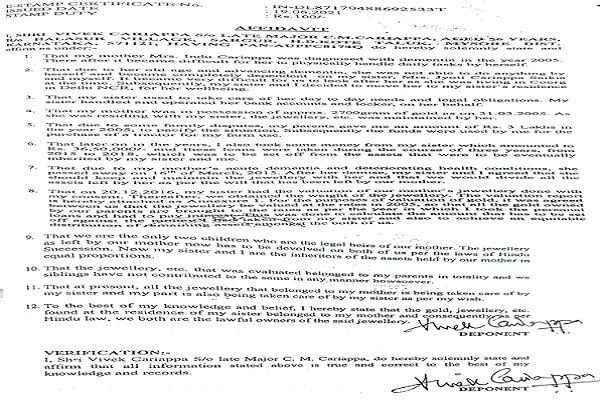

10. That the Ld. CIT(A) erred in law and on facts in not granting complete relief despite the appellant having furnished the Will of her late mother evidencing inheritance of jewellery, and in disregarding the uncontroverted affidavit of the appellant’s brother without any verification or cross-examination, contrary to settled legal principles.

11. That the Ld. CIT(A) erred in drawing adverse inference from enhancement of jewellery value in the revised return, without appreciating that even the original return under section 139(1) was filed after the date of search, rendering such inference factually incorrect and unsustainable.

12. That the appellant craves leave to add, amend, alter or withdraw any of the above grounds at or before the time of hearing.”

3. Brief facts of the case are that the assessee filed her original return for A.Y. 2021-22 on 30.12.2021 and revised return on 30.03.2022 declaring income of Rs. 2,75,05,840/-. A search action u/s 132 was conducted on Triburg Group on 04.03.2021 and the assessee’s residence was also searched during this action. Satisfaction note was recorded by the AO on 18.05.2023 and notice u/s 153C was also issued on 18.05.2023. Thereafter, the assessment was completed after making an addition of Rs. 53,80,000/- u/s 69A on account of unexplained jewellery found during the course of search.

3.1 Aggrieved, the assessee preferred an appeal before the Ld. CIT(A), who vide order dated 03.02.2026, granted part relief of Rs. 35,68,974/- and sustained the addition to the extent of Rs. 18,11,026/-. Further aggrieved, the assessee has filed appeal before the Tribunal.

4. Before us, the Ld. AR has submitted written submissions as well as made arguments with regard to the legality of the proceedings under section 153C which has been challenged vide ground nos. 1 to 4. With regard to Ground nos. 8 to 12, challenging the addition on merits, the Ld. AR has filed written arguments and placed supporting documents in support of the explanation regarding jewellery found, which is as under:

” C. The part-confirmation of Rs. 18,11,026/- is arbitrary and unsustainable on merits:

i. The Ld CIT(A) erred in sustaining the addition of Rs. 18,11,026 under section 69A by disregarding the material evidences placed on record explaining the source of the jewellery, namely, the Will of the mother, affidavit of the brother, and the factum of receipt of jewellery as streedhan, duly supported by marriage photographs.

ii. At the very first opportunity, i.e., during the course of search itself, the assessee had specifically explained that the jewellery found during search included jewellery received from her mother, purchased overtime and jewellery received at the time of marriage as streedhan. The said explanation is duly evident from Question No. 41 of the statement of the assessee recorded under section 132(4) on 04.03.2021. [Refer P No. 24 of Ply

iii. The aforesaid evidences were thereafter placed before the Investigation Wing, the AO, and the CIT(A). However, the Ld. AO brushed aside the said evidences merely by observing that the explanation was a “difficult theory to believe” [Para 8.3 of the assessment order] and an “afterthought” [Para 8.5 of the assessment order] , without bringing any contrary material on record.

iv. The Ld. CIT(A) further erred in mechanically sustaining the addition without independently examining or discussing these evidences in the appellate order. In fact, the CIT(A) has not dealt with the Will of the mother and affidavit while sustaining the addition. [Refer Para 5.3.6 of the CIT(A) order at P No. 37 of the order]

v. The Ld. CIT(A) failed to appreciate that once these evidences were made available at the time of search itself and consistently relied upon thereafter, the same could not have been rejected as an afterthought. Further, the said evidences have remained unrebutted throughout the proceedings and no adverse material has been brought on record to discredit the explanation of the assessee.

vi. The jewellery explained through the aforesaid evidences, in fact, exceeds not only the jewellery seized but also the total jewellery found during the course of search. Therefore, there remains no unexplained jewellery so as to warrant any addition under section 69A. A consolidated reconciliation of the jewellery is set out below for ready reference:

| Particulars | Cold Nt. | Stone (Carats) | Diamond (Carats) |

P. NO. of PB |

| Jewellery Found ,(A) | 1127.62 | 1553 | 126.1 | 21-22 |

| Jewellery Inherited (B) | 1896.006 | 1785 | 106 | 26-32 |

| Jewellery Supported by Bills (C) | 175.546 | 1041.12 | 23.5 | 53-69 |

| Balance/excess [A-(B+C)] | (943.932) | (1273.12) | (3.4) |

OR

| Sr. no. | Jewellery | Gross Weight (gms) | P. NO. of PB |

|

| A | 1. | Jewellery found | 1,758.930 | 21-22 |

| B | 2. | Jewellery Inherited | 2704.14 | 26-32 |

| C | 3. | Bills | 481.176 | 53-69 |

| Jewellery in excess [A-(B+C)] | -1426.386 |

i. The Ld. CIT(A) erred in not properly applying CBDT Instruction No. 1916 dated 11.05.1994 in its full purport, which mandates consideration of the financial and social status of the assessee while evaluating jewellery found during search.

ii. The Ld. CIT(A) further erred in accepting the valuation adopted by the AO based on historical purchase bills (pertaining to the period 2016 to 2020), without correlating or reconciling the same with the valuation determined at the time of search and seizure.

In view of the above, the addition sustained under section 69A is without any factual or legal basis and is liable to be deleted.”

4.1 Ld. DR, on the other hand, has strongly relied upon the orders of the lower authorities and argued that the assessee’s claim regarding jewellery received upon the death of her mother is an afterthought and, in any case, the Ld. CIT(A) has granted part relief to the assessee after examining the relevant details and evidences. He has, therefore, argued that the order of the Ld. CIT(A) should be upheld.

5. We have heard the rival submissions and perused the material available on record. Admittedly, the assessee was an employee of the search company Tribung Consultants Pvt. Ltd. and has been filing returns, declaring, inter alia, salary income from the company. During the year under consideration, the assessee had received salary of Rs. 1,60,00,000/- from the company, besides share of profit from a partnership firm, M/s Gratitude Consultant LLP of Rs. 22946 (exempt u/s 10), income from house property and capital gains. During the course of the search conducted at her residence, jewellery weighing 1758.93 grams valued at Rs. 1,25,89,817/- was found out of which jewellery worth Rs. 90,20,843/- was seized. The assessee explained the sources of jewellery as under:-

” (i) Jewellery received at the time of her marriage (Streedhan)

(ii) Jewellery purchased over time

(iii) By inheritance from mother

5.1 In this regard, bills/ invoices relating to purchase of jewellery during 2016-2021 to the extent of 481.176 grams have been filed as per the following details:

S. No. |

Invoice Date |

Goods |

Gross Weight (in grams) |

Net Weight (in grams) |

Stone Weight (in grams) |

Value of Gold |

Value of Stone |

GST |

Grand Total |

1 |

01.03.2021 |

Victorian Jewellery with Ruby and Pearls |

76.85 |

15 |

61.85 |

48,000 |

27,000 |

2,250 |

77,250 |

2 |

12.12.2020 |

Ring Blue with sapphire and Diamond |

6.47 |

5.086 |

1.39 |

– |

– |

6,990 |

2,39,990 |

3 |

08.03.2019 |

Pendent with emerald, pearl and diamond |

66.65 |

15 |

51.65 |

– |

– |

33,990 |

11,66,990 |

4 |

06.11.2019 |

Pendent |

11.09 |

– |

– |

52,450 |

– |

1,573 |

54,023 |

5 |

19.03.2018 |

Ring |

5.51 |

4.71 |

0.8 |

– |

– |

1,83,000 |

1,88,490 |

6 |

07.07.2018 |

One pair kada with emerald |

53.38 |

37.39 |

15.99 |

– |

– |

2,900 |

2,36,900 |

7 |

16.07.2018 |

One ring |

2.56 |

2.29 |

0.27 |

– |

– |

4,800 |

1,64,800 |

8 |

14.10.2017 |

Ruby String with Diamond emerald |

38.25 |

– |

– |

– |

– |

1,800 |

61,800 |

9 |

20.10.2016 |

One pendent with diamond |

54.38 |

47 |

7.38 |

– |

– |

5,050 |

5,10,050 |

10 |

25.02.2017 |

One pair earring diamonds |

37.97 |

15.07 |

22.9 |

– |

– |

6,691 |

6,75,816 |

11 |

26.12.2016 |

Polki Bangle |

40.90 |

– |

– |

– |

– |

– |

1,08,636 |

12 |

20.08.2016 |

Necklace with diamonds, pearl and silver |

45.77 |

9 |

36.77 |

– |

– |

2,980 |

3,00,930 |

13 |

24.12.2016 |

Ring with diamond and emerald |

7.76 |

6 |

1.76 |

– |

– |

12,800 |

12,92,800 |

14 |

24.12.2016 |

Pearl Necklace |

78.10 |

10 |

68.10 |

– |

– |

5,500 |

5,55,500 |

15 |

20.08.2016 |

Necklace with diamond, pearl and silver |

45.77 |

9 |

36.77 |

– |

– |

2,980 |

3,00,930 |

5.2 Copy of bank statement evidencing payments made in respect of above purchases has also been filed.

5.3 With regard to the jewellery inherited from her mother, the assessee has placed on record a copy of the will of her mother, late Smt. Indu Cariappa, dated 25.12.2014 and an affidavit of her brother, Vivek Cariappa dated 19.06.2021. It has been explained that as per the will of her mother, the jewellery weighing approx. 2700 grams was to be equally divided between the assessee and her brother. As the mother was staying with the assessee, the jewellery was kept with her and assessee, who got its valuation done on 20.12.2016. A copy of the Valuation Report of the approved valuer has also been filed along with the affidavit of her brother, wherein the following explanation regarding jewellery found in the assessee’s possession has been given:

5.4 In the light of these documents, Ld. AR has submitted the following reconciliation: –

| Particulars | Gold Nt. | Stone (Carats) | Diamond (Carats) | P. NO. of PB |

| Jewellery Found (A) | 1127.62 | 1553 | 126.1 | 21-22 |

| Jewellery Inherited (B) | 1896.006 | 1785 | 106 | 26-32 |

| Jewellery Supported by Bills (C) | 175.546 | 1041.12 | 23.5 | 53-69 |

| Balance/excess [A-(B+C)] | (943.932) | (1273.12) | (3.4) | – |

OR

| Sr. no. | Jewellery | Gross Weight (gms) | P. NO. of PB |

|

| A | 1. | Jewellery found | 1,758.930 | 21-22 |

| B | 2. | Jewellery Inherited | 2704.14 | 26-32 |

| C | 3. | Bills | 481.176 | 53-69 |

| Jewellery in excess [A-(13-1-C)] | -1426.386 |

5.5 After careful consideration of the above facts and circumstances, we are of the view that the assessee has duly explained the sources of acquisition of jewellery found in her possession at the time of search. Considering the details and documentary evidences coupled with the high income declared by the assessee in the year under consideration, as well as in the past years, we are inclined to accept the assessee explanation regarding purchase of jewellery over the years as well as regarding inheritance of jewellery from her mother. We, therefore, delete the addition sustained by the Ld. CIT(A) to the extent of Rs. 18,11,026/- on account of unexplained jewellery u/s 69A of the Act. Accordingly, this ground of the assessee is hereby allowed.

5.6. As the appeal has been allowed on merits, remaining legal grounds are rendered academic and hence these are not being adjudicated upon.

6. In the result, appeal of the assessee is allowed.

Order pronounced in the open court on 22.06.2026.

Author Bio