Case Law Details

ITO Vs Amrat Mali (ITAT Ahmedabad)

The Income Tax Appellate Tribunal (ITAT), Ahmedabad, dismissed the Revenue’s appeal and upheld the order of the Commissioner of Income-tax (Appeals) [CIT(A)] deleting an addition of ₹26,08,000 made under Section 68 of the Income-tax Act, 1961. The addition had been made during reassessment proceedings on the basis of information received from the Investigation Wing following a search conducted under Section 132 in the cases of certain individuals. According to the information, the assessee was alleged to have received accommodation entries amounting to ₹26,08,000 through two companies controlled by the searched persons. The Assessing Officer completed the reassessment under Sections 144 read with 147 and treated the amount as unexplained cash credit under Section 68, primarily relying on the information received from the Investigation Wing.

The CIT(A), after examining the material on record, deleted the addition. It was noted that the Assessing Officer had relied solely on information received from the Investigation Wing and the assessee’s alleged non-compliance without conducting any independent enquiry or verification. The CIT(A) observed that the assessee had filed a response, stated that the alleged companies were unlisted companies, and submitted details of capital gains, which did not show any transactions with those companies. The assessee had also declared business income under Section 44AD and stated that there were no debtors or creditors. The assessee specifically denied having any dealings with the alleged accommodation entry providers and requested the Assessing Officer to furnish details and break-up of the alleged transactions to enable an appropriate response. According to the CIT(A), the Assessing Officer did not provide such details or undertake any further enquiry.

The CIT(A) further held that the addition under Section 68 was based only on suspicion arising from the information received from the Investigation Wing. It observed that the Assessing Officer had neither conducted any independent investigation nor verified bank transactions to establish any link between the assessee and the alleged accommodation entry operators. The CIT(A) also noted that the basis of reopening referred to bogus long-term capital gains (LTCG), whereas the assessee had declared a capital loss and had no transactions with the two unlisted companies referred to in the assessment order. Relying on judicial precedents, the CIT(A) concluded that suspicion, however strong, cannot take the place of evidence and deleted the addition of ₹26,08,000.

Before the Tribunal, the Revenue contended that the Assessing Officer had acted on specific information obtained during the search and that the assessee had been identified as a beneficiary of accommodation entries. The assessee supported the CIT(A)’s order, arguing that no corroborative evidence or independent enquiry had been undertaken to establish that the impugned amount represented unexplained income.

After considering the submissions, the Tribunal found that the addition had been made solely on the basis of information received from the Investigation Wing and the alleged involvement of third parties, without any independent enquiry or corroborative evidence linking the assessee to the alleged accommodation entries. It observed that the Revenue had not produced any material before the Tribunal to controvert the factual findings recorded by the CIT(A) or establish a direct nexus between the assessee and the alleged accommodation entry providers. The Tribunal also noted that, contrary to the allegation of bogus LTCG of ₹19,14,000 and ₹6,94,000, the assessee had not claimed any exempt long-term capital gain in the return of income and had instead reported a short-term capital loss of ₹39,775. In the absence of evidence supporting the allegation, the Tribunal found no infirmity in the CIT(A)’s order deleting the addition under Section 68. Accordingly, the Revenue’s appeal was dismissed.

FULL TEXT OF THE ORDER OF ITAT AHMEDABAD

This appeal has been filed by the Revenue against the order passed by the Ld. Commissioner of Income-tax (Appeals), National Faceless Appeal Centre (NFAC), Delhi (hereinafter referred to as “CIT(A)” for short), dated 12.09.2025, under Section 250 of the Income-tax Act, 1961 [hereinafter referred to as “the Act” for short], for Assessment Year (AY) 2016-17.

2. The Revenue has raised the following grounds:-

“1. “Whether on facts and circumstances and in law, the Ld. CIT(A) has erred in deleting addition of Rs.26,08,000/- u/s. 68 being accommodation entry in the form of bogus LTCG in lieu of cash, without appreciating the facts of the case?”

2. “Whether on the facts and in the circumstances of the case and in law, the ld. CIT(A) has erred in ignoring the fact that the assessee has obtained accommodation entry of bogus LTCG amounting to Rs. 19,14,000/- and Rs.6,94,000/- through the transaction with M/s Pranatpal Tradelink Pvt. Ltd and Suramya Tradelink Pvt. Ltd. respectively during the F.Y. 2015-16 which were controlled and managed by Jignesh Shah & Sanjay Shah ofAhmedabad, who do not carry genuine business activities?”

3. The brief facts of the case are that the assessee had originally filed the return of income declaring total income of Rs.3,73,310/-. Subsequently, on the basis of information received from the Investigation Wing pursuant to a search conducted u/s 132 of the Act in the cases of Shri Jignesh Shah and Shri Sanjay Shah, Ahmedabad, the Assessing Officer formed a belief that income chargeable to tax had escaped assessment. According to the information received, the assessee was identified as a beneficiary of accommodation entries amounting to Rs.26,08,000/- allegedly routed through M/s Pranatpal Tradelink Pvt. Ltd. and M/s Suramya Tradelink Pvt. Ltd. During reassessment proceedings, the Assessing Officer called upon the assessee to explain the nature and source of the impugned transactions. According to the Assessing Officer, the assessee failed to furnish the requisite details and, therefore, the reassessment was completed ex parte under section 144 r.w.s. 147 of the Act. Relying primarily upon the information received from the Investigation Wing, the Assessing Officer treated the amount of Rs.26,08,000/- as unexplained cash credit u/s 68 of the Act and added the same to the income of the assessee.

4. Aggrieved by the order of the Assessing Officer, the assessee carried the matter in appeal before the Ld. CIT(A), who, after considering the material available on record, deleted the impugned addition.

5. Aggrieved by the order of the Ld. CIT(A), the Revenue is now in appeal before the Tribunal.

6. Before us, the Ld. DR relied upon the assessment order and submitted that the Assessing Officer had acted on specific information emanating from a search action wherein it was found that the concerns controlled by Shri Jignesh Shah and Shri Sanjay Shah were engaged in providing accommodation entries. It was contended that the assessee was identified as a beneficiary of such accommodation entries and, therefore, the Ld. (A) was not justified in deleting the addition.

7. The Ld. AR supported the order of the Ld. CIT(A) and submitted that the addition u/s 68 of the Act was made solely on the basis of information received from the Investigation Wing without any independent enquiry or corroborative material. The Ld. AR also submitted that no evidence was brought on record by the Assessing Officer to establish that the assessee had received any accommodation entry or that the impugned amount represented his undisclosed income. The Ld. AR thus submitted that the Ld. CIT(A), after appreciating the facts and material available on record, has rightly deleted the addition and, therefore, no interference is called for in the impugned order.

8. We have heard the rival contentions and perused the material available on record. We find that the addition has been made solely on the basis of information received from the Investigation Wing and the alleged involvement of certain third parties in providing accommodation entries. In this regard, it is pertinent to note the observations of the Ld. CIT(A), which is as under:-

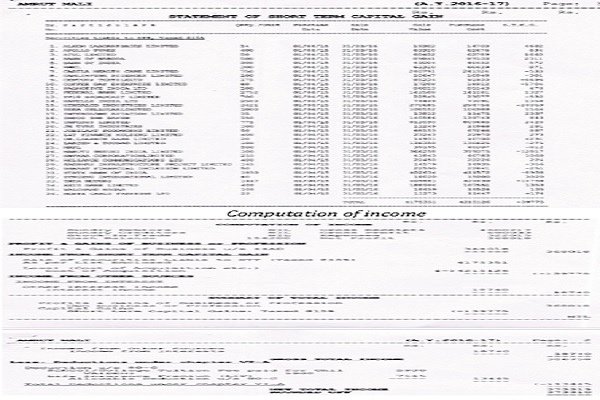

“I have considered the appellant’s submissions and the facts of the case. The appellant submitted response on 31.07.2025. The appellants contented that the Companies alleged in the order of AO are unlisted companies. Appellant had also submitted details of his capital gains from which it is seen that no transactions are there with these two companies. Appellant’s business income has been declared u/s 44AD at 8 percent of Rs.4600217/-. There are also no debtors or creditors. The details of share transactions of appellant are as under:

I find that the AO had only based his conclusions on the information received and the non-compliance of Appellant. Appellant had stated that the information was provided on 16.03.2022. In this regard, I find that the assessment order was passed on 22.03.2022.

I find that AO had not done any independent enquiry or bank verifications regarding the amount alleged to have been received by the assessee. The basis of the reopening was that the accommodation entry operators did synchronised transactions in exchange and provided bogus LTCG. However, in the case of appellant there is a loss declared under Capital Gains. No capital gains or losses were seen with the companies which were unlisted. The appellant during assessment had denied the transactions. Appellant stated

” Your goodself has alleged that as per information available on record, during F.Y2015-16 relevant to A.Y 2016-17, I have taken accommodation entries of Rs.26,08,000/- from the firms controlled by Jignesh Shah and Sanjay Shah. In regards to the above I humbly request your goodself to provide me with the breakup / details of Rs. 26,08,000/- as well as the name of the parties from whom the amounts have been taken. Since the requested information will enable myself to furnish appropriate required details, for the kind consideration of your goodself. Since I have not dealt with Jignesh Shah or Sanjay Shah, I am unable to identify the single amount and parties mentioned in the notice from my books of account.”

Therefore, in response to the last line of the submission, AO had the onus to provide further details of credit into appellant’s account.

Addition u/s 68 on the basis of information from investigation wing without corroborative evidence and linkage of the assessee with the alleged accommodation entry will fall in the domain of suspicion only. Suspicion alone without there being evidence specific to a transaction cannot become the basis for creating charge for levying tax as each transaction has to be independently inquired into. Suspicion howsoever strong cannot take the character of evidence. Reliance is placed on the decision in…

Dhakeswari Cotton Mills Ltd. v. CIT [1954] 26 ITR 775 (SC), Lalchand Bhagat Ambica Ram v. CIT [1959] 37 ITR 288 (SC), CIT v. East Coast Commercial Co. Ltd. [1967] 63 ITR 449 (SC), CIT v. Daulatram Rawatmull [1964] 53 ITR 574 (SC); and Umacharan Shaw & Bros. v. CIT [1959] 37 ITR 271 (SC);

In the above decisions, it was held that suspicion cannot be treated as evidence. The AO had not done independent enquiry to trace the trail offunds linking the accommodation entry operator to the assessee. In view of the circumstances of the case, the addition of Rs.2608000/- is deleted.”

8.1 From the aforesaid findings, it is evident that the Ld. CIT(A) has examined the material available on record and recorded a categorical finding that the Assessing Officer had proceeded solely on the basis of information received from the Investigation Wing without carrying out any independent enquiry or bringing any corroborative material on record to establish that the impugned amount represented unexplained income of the assessee. The Ld. CIT(A) has further noted that the assessee had specifically denied having any transaction with the concerns. We further note that the Revenue has not placed any material before us to controvert the factual findings recorded by the Ld. CIT(A). No evidence has been brought on record demonstrating any direct nexus between the assessee and the alleged accommodation entry providers. In the absence of any independent enquiry or corroborative evidence linking the assessee with the impugned transactions, the addition made u/s 68 of the Act cannot be sustained merely on the basis of information received from the Investigation Wing.

8.2 The Assessing Officer held that “As per departmental information, it is evident that the assessee had taken accommodation entry of bogus LTCG amounting to Rs. 19,14,000/- and 6,94,000/- through the transaction with M/s. Pranatpal Tradelink Pvt. Ltd. and Suramya Tradelink Pvt Ltd. respectively during the F.Y.2015-16. The information was gathered through a search operation conducted on 11.09.2018 in the case ofJignesh Shah & Sanjay Shah, Ahmedabad. It was found during investigation that both Jignesh Shah and Sanjay Shah were managing and controlling multiple companies and concerns which are not carrying out any genuine business activity. The above mentioned companies were also in the list. These concerns/companies are involved into activity of providing accommodation entries through Jignesh Shah and Sanjay Shah. While giving statement they are admitted the fact. Beneficiaries had been identified by analysis of data found during investigation and perusal of such data revealed that the assessee was one of such beneficiary who had taken accommodation entry.”

We find that the assessee has not claimed any LTCG as exempt in the return of income, rather it was a Short Term Capital Loss of Rs. 39,775/-. Since there were no evidences on record to prove that assessee had received bogus LTCG of Rs.19,14,000/- and Rs.6,94,000/- as alleged in the assessment order mentioned above, we do not find any infirmity in the order of the Ld. CIT(A) deleting the addition of Rs.26,08,000/-. Accordingly, the grounds raised by the Revenue are dismissed.

9. In the result, the appeal filed by the Revenue is dismissed.

Order pronounced in the open Court on 17.06.2026

Author Bio