Case Law Details

Mrunmayee Priyadarshini Pattnaik Vs ITO (ITAT Delhi)

Non supply of approval U/s 151 despite specific request in RTI, invalidate reassessment proceeding

The Delhi ITAT allowed the assessee’s appeal and quashed the reassessment proceedings after holding that the non-supply of approval under Section 151 of the Income Tax Act rendered the reassessment invalid.

The assessee’s case was reopened through a notice under Section 148 dated 31.03.2022. The reopening was based on allegations that the assessee had purchased two properties at values lower than their stamp duty valuations, resulting in a difference of ₹48 lakh. The Assessing Officer concluded that income had escaped assessment and subsequently made an addition of ₹48 lakh under Section 56(2)(x) of the Act.

The assessee challenged the assessment before the CIT(A), who dismissed the appeal and upheld the addition. The assessee then appealed before the ITAT and also raised an additional legal ground contending that the reassessment proceedings were invalid because the Revenue failed to provide the approval or sanction obtained under Section 151 despite specific requests made through an RTI application.

The assessee argued that the issue was purely legal and did not require any fresh investigation of facts. The RTI response stated that, upon examination of the ITBA portal and records forwarded by the concerned Assessing Officer, no such approval document was available in the file records or the ITBA system.

The Tribunal admitted the additional ground, observing that it was a pure question of law and relying on the Supreme Court’s decision in National Thermal Power Company Ltd. v. CIT.

On merits, the Tribunal noted that despite repeated requests by the assessee and the RTI application, the Revenue failed to furnish a copy of the approval under Section 151. The Departmental Representative also acknowledged that the requested documents were not found in the records forwarded by the concerned Assessing Officer. Although the order passed under Section 148A(d) mentioned that prior approval of the Principal Commissioner had been obtained, the actual approval document was never supplied.

The Tribunal referred to its earlier decision in Arpit Goel v. ITO, where reassessment proceedings were quashed because the Revenue could neither demonstrate nor provide the approval required under Section 151. In that case, the Tribunal had held that reassessment proceedings undertaken without the mandatory approval of the competent authority were bad in law and void ab initio.

Applying the same reasoning, the Tribunal held that the failure to supply the approval under Section 151 amounted to non-compliance with the prescribed procedure. In view of the factual position and documentary evidence on record, the reassessment proceedings and the consequential assessment order could not be sustained.

Accordingly, the ITAT quashed the reassessment proceedings and the assessment order, allowed the additional ground raised by the assessee, and allowed the appeal.

FULL TEXT OF THE ORDER OF ITAT DELHI

The appeal of the assessee is directed against order of the ld. CIT(A)/NFAC, Delhi dated 10.09.2025 u/s 250 of the Income Tax Act, 1961 (hereinafter referred to as “the Act”), wherein the addition made u/s 56(2)(x) of the Act of Rs.48,00,000/-vide assessment order dated 25.03.2023 was confirmed and the appeal was dismissed.

2. Facts in brief as culled out from the authorities below are that the case of the assessee was selected for re-assessment by issuing notice u/s 148 of the Act dated 31.03.2022 on the ground that assessee has purchased two properties in the concerned year for consideration of Rs.48,50,000/- having stamp value of Rs.69,50,000/- along with basement for Rs.4,00,000/- having stamp valuation of Rs. 31,00,000/-. Order u/s 148A(d) was passed on 31.03.2022. The source of whole purchase of Rs.52,50,000/- remained unexplained (both transaction) and the assessee having purchased these properties for less than their stamp value having a difference of Rs.48,00,000/- and as such total income of Rs.1,00,50,000/-remained unexplained and has escaped assessment. During the re-assessment proceeding, opportunities were given to the assessee to explain the transaction and the consideration received therein. However, the Assessing Officer was not satisfied and made addition of Rs. 48,00,000/- u/s 56(2)(x) of the Act and also initiated penalty proceedings.

3. Aggrieved by the Assessment Order, the assessee filed appeal before the ld. CIT(A) who has dismissed the same observing that various notices u/s 250 of the Act were issued to the appellant who did not file any reply or documentary evidence in support of the grounds taken in the appeal. However, the ld. CIT(A) dismissed the appeal on merit and upheld the Assessment Order and the addition made therein.

4. Aggrieved by the impugned order, the assessee filed appeal before us and has raised following grounds of appeal:

“1. That, the notice u/s 148A(b) and order u/s 148A(d) the Income tax Act, 1961, is bad in law and on facts, as the enquiry before reassessment proceedings were initiated and completed without proper compliance to principles of natural justice. The appellant was deprived of adequate opportunity to present her case, and the assessment was done ex parte based on alleged non compliance which is factually incorrect.

2. That, the notice u/s 148 of the Income tax Act, 1961, is bad in law and on facts.

3. That, the Approval taken u/s 151 of the Income Tax Act, 1961 is illegal, invalid and bad in law.

4. That, the AO has not issued any notice under section 143(2). In such circumstances, the mere observation that the return is invalid in the assessment order, without any statutory notice under section 143(2), is a complete non application of mind and is contrary to settled law by Patna High Court in the case of CIT Vs. Nagendra Prasad, (2023) 156 com19 (Pat).

5. That, the learned Assessing Officer (AO) grossly erred in making an addition of Rs. 48,00,000 under section 56(2)(x) as Income from Other Sources on the ground of difference between the stamp duty value and the consideration paid for purchase of two properties, without appreciating that the transfer and possession actually took place in FY 2006-07 and FY 2013-14, which is prior to the insertion of section 56(2)(x) with effect from 1 April 2017. Hence, the provision does not apply to the impugned transactions.

6. That, the order passed under section 147 read with section 144 and 144B of the Income tax Act, 1961, is bad in law and on facts, as the reassessment proceedings were initiated and completed without proper compliance to principles of natural justice. The appellant was deprived of adequate opportunity to present her case, and the assessment was done ex parte based on alleged non compliance which is factually incorrect.

7. That, the appellant craves leave to add to, alter, amend, modify, substitute, DLEETE OR otherwise revise all OR any of the foregoing grounds of appeal, and to raise such further OR other grounds at OR before the time of hearing of this appeal, as may be considered necessary OR expedient.

8. Whether there is any delay in filing of appeal (if yes, please attach application seeking condonation of delay).”

5. During the hearing, the assessee moved an application dated 28.05.2026 for admitting additional grounds raised as under:

“On the facts and circumstances of the case and in law, the reassessment proceedings initiated under section 147/148 of the Income Tax Act, 1961 are bad in law and liable to be quashed as the Assessing Officer failed to provide the approval/sanction obtained under section 151 of the Act despite specific request of the assessee in RTI citing, thereby violating principles of natural justice and rendering the reassessment proceedings invalid.”

6. We have heard the ld. AR and the ld. DR on the additional ground. It is argued that the additional ground so raised is purely legal in nature and does not require any investigation into any facts outside the material already available on record. It is further submitted that assessee has specifically requested for supply of approval granted u/s 151 of the Act in RTI. In the reply to the RTI, it has been stated that “on perusal of the ITBA Portal as well as the file folder forwarded by ITO, Ward-54(1), Delhi, it is observed that no such documents is available in the file records and in the ITBA-Systems.” It is therefore submitted that additional ground be admitted and the re-assessment done in the absence of supply of approval u/s 151 of the Act being bad in law. The impugned order is liable to be quashed.

7. We have considered the rival submissions on admission of the additional ground. We have noticed that the ground raised as additional ground is purely legal ground and does not require any fresh facts to be brought on record. Hence, following the law laid down by the Hon’ble Supreme Court in the case of National Thermal Power Company Ltd. Vs. CIT reported in 229 ITR 383(SC), the additional grounds is admitted for adjudication.

8. In respect of additional ground, at the very outset, it has been submitted that the entire re-assessment done is bad in law and is liable to be quashed because despite repeated requests even during the re-assessment proceedings and also subsequently the Revenue has failed to provide the copy of sanction u/s 151 of the Act despite a specific request of the assessee in RTI. The ld. AR has relied various judgments including the judgment of Delhi Tribunal in the case of Arpit Goel Vs. ITO in ITA Nos. 349, 350 & 351/Del/2017 order dated 27.06.2025 wherein identical issue was decided in favour of the assessee.

9. The ld. DR on the other hand admitted that despite a report having been called from the Assessing Officer as placed on record on 03.06.2026, the concerned ITO in e-mail dated 06.05.2026 i.e. ITO, Ward-54(1), Delhi, conveyed that the “relevant documents as sought by RTI application is not found in the folder furnished by your office”. However, the RTI was disposed of observing as under:

“In response to mail dated 06.05.2026, the ITO, Ward-54(1) Delhi vide mail dated 07.05.2026 submitted that ‘all relevant records available with their office have already been forwarded to you. Furthermore, as the PAN data of the applicant is already accessible at your end. Therefore, you are requested to kindly process the RTI application and take further necessary action accordingly’.

Keeping in view the time limitation as per RTI section 7(1), this office vide mail dated 29.05.2026 disposed of the received RTI with the following remarks.

| S.No. | Query as per RTI | Remarks |

| 1. | Copy of request letter to sanction authority by ITO, Ward-54(1) and approval u/s 151 of the Income Tax Act, 1961 | On perusal of the ITBA Portal as well as the file folder forwarded by ITO, Ward-54(1) Delhi, it is observed that no such documents is available in the file records and in the ITBA- Systems. |

| 2. | Reason for non-issuance of notice u/s 143(2) of the Act, even return filed in response to notice u/s 148 | ‘Assessee filed an invalid return in response to notice u/s. 148 of the Act’. |

Further, it is worthy to mention here that the statutory order dated 31.03.2022 passed u/s 148A(d) of the Income Tax Act itself containing a remarks at the end para of the same that ‘_ This order is being passed with prior approval of the Principal Commissioner of Income Tax-12, Delhi. Notice u/s 148 of the Income Tax Act, 1961 is issued along with this order after obtaining prior approval of the PCIT-12 Delhi.”

10. It is thus clear from the above submissions on behalf of Revenue that the approval u/s 151 of CPC has not been supplied to the assessee in this case. We have noted that the identical issue has been decided by the Delhi Tribunal in ITA No. 349, 350 & 351/Del/2017 in the case of Arpit Goel (supra), the relevant portion from Paras 3 to 8 is extracted below as under:

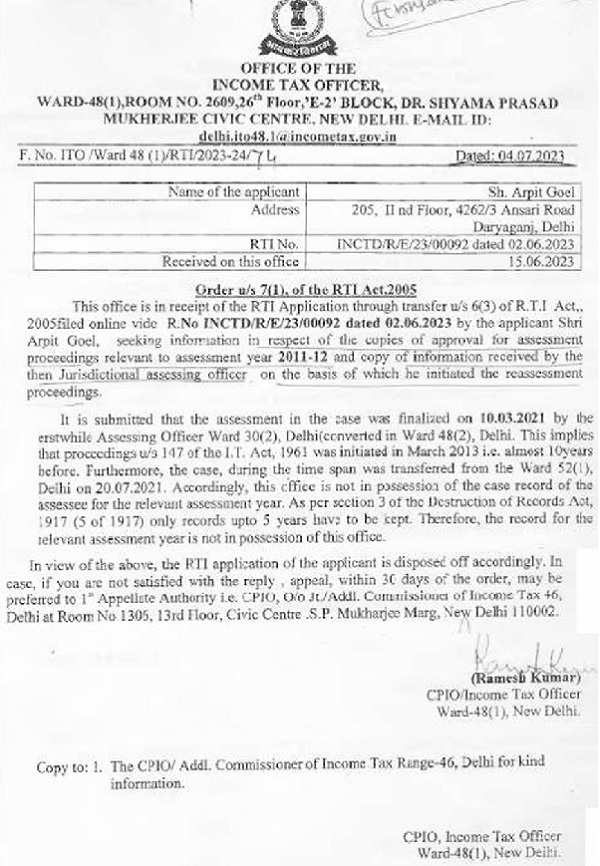

“3. The Ld. Counsel for the assessee further submitted that the AO reopened the assessment by issue of notice u/s 148 of the Act without the approval from the appropriate authority u/s 151 of the Act. Ld. Counsel for the assessee therefore submits that since the assessments were reopened without the approval of competent authority u/s 151 of the Act the consequential reassessments made by issue of notice u/s 148 in the absence of any approval of such reassessments are bad in law and void ab initio. 4. On the other hand, Ld. DR supported the orders of the authorities below. 5. Heard rival submissions, perused the orders of the authorities below. On perusal of the reasons recorded for initiation of proceedings u/s 147/148 issued by the AO for the assessment years 2009-10 to 2011-12 were all undated. Further the AO did not mention in the reasons whether he has taken any prior approval for initiating the reassessment proceedings and for issue of notice u/s 148 for these assessment years. We observe that the assessee also filed under RTI seeking to supply a copy of approval granted by the competent authority for reopening of these assessments. The 2 ITA Nos.349, 350 & 351/Del/2017 CPIO/ITO, Ward 48(1), New Delhi by order dated 04.07.2023 informed the assessee as under:-

6. From the perusal of the above order, we noticed that theRevenue could not provide any copy of approval as they werenot in a possession of the case records. We observed that since the AO never stated in the reasons recorded whether any approval has been taken by him from the competent authority before issue of notice u/s 148 of the Act for reopening of assessments for the assessment years 2009-10 to 2011-12 creating a doubt whether at all the AO has obtained any prior mandatory prior u/s 151 of the Act more so when the reasons for reopening of assessments were all undated. The Revenue also could not provide any copy of approval if any granted for reopening of the assessments. In the absence of any approval u/s 151 from the competent authority for reopening of assessments the assessments made without such approval becomes bad in law and void ab initio . Thus, we quash the reassessment orders for assessment years 2009-10 to 2011-12 as the reassessments were made without the prior approval of the competent authority u/s 151 of the Act.

7. Since we have quashed the reassessments for the assessment years 2009-10 to 2011-12 on a legal issue. We are not inclined to go into the merits of the addition/disallowance made by the AO in the assessment orders for all these years as it would be of only academic in nature at this stage and the same are left open.

8. In the result, appeals of the Assessee are partly allowed as indicated above.“

11. We have considered the rival submissions, in view of the factual position and the documentary evidence discussed above and respectfully following the judgment of the Delhi Tribunal in ITA No. 349, 350 & 351/Del/2017, we are of the considered opinion that the re-assessment in this case, without following the due procedure i.e. non-supply of approval u/s 151 of the Act has made the proceeding void ab initio and the re-assessment proceeding as well as the impugned order are not sustainable and the Assessment Order is accordingly quashed. The additional ground so raised is accordingly allowed in above terms.

12. In the result, the appeal of the assessee is allowed.

Order Pronounced in the Open Court on 15/06/2026.

Author Bio