Case Law Details

Bright Metal Refiners Vs Director General (Delhi High Court)

The Delhi High Court allowed a writ petition filed by an importer of precious metals seeking clearance of consignments of platinum alloy jewellery studded with rubies imported from Thailand. The petitioner had imported goods classified under Tariff Entry 71131925, which, at the time of shipment, were covered under the “Free” import policy. Airway Bills for the consignments were issued on 30 March 2026 and 31 March 2026, and the consignments arrived at different Indian airports, with the final consignment reaching India on 2 April 2026 at 01:39 a.m.

Subsequently, Notification No. 02/2026-27 dated 1 April 2026 was published in the e-Official Gazette on 2 April 2026 with a digital timestamp of 20:52:28 hours. By virtue of this notification, the import policy applicable to goods falling under Customs Tariff Heading 7113 was amended from “Free” to “Restricted”. The notification further stipulated that transitional arrangements under the Foreign Trade Policy, 2023 would not apply and that the revised policy would operate irrespective of prior contracts, letters of credit, advance payments, or shipment status.

The petitioner contended that the notification could acquire the force of law only upon its publication in the Official Gazette and that all consignments had either been dispatched or had arrived in India before the notification was published. Therefore, the petitioner argued that the revised import restrictions could not be applied retrospectively to its consignments. Reliance was placed on judicial precedents holding that delegated legislation becomes enforceable only upon publication in the Official Gazette.

The respondents raised several objections. They argued that the petitioner had not specifically challenged the validity of the notification, that an alternative remedy was available under the Foreign Trade Policy through the Policy Relaxation Committee, and that territorial jurisdiction issues arose because multiple consignments were involved. On merits, the respondents maintained that the goods had not been cleared prior to the notification coming into force and, therefore, the import process remained incomplete. They also referred to a subsequent Office Memorandum stating that consignments not cleared before 1 April 2026 would be governed by the revised policy.

The Court first addressed the objection regarding the absence of a specific challenge to the notification. It held that the petitioner was not seeking to invalidate the notification but was contending that the notification did not apply to the consignments in question. Therefore, it was unnecessary to adjudicate the validity of the notification itself.

The Court then considered the principal issue: whether the notification published electronically on 2 April 2026 at 20:52:28 hours could apply to goods already dispatched and imported before its publication. In doing so, the Court examined several judicial precedents. It referred to the Supreme Court’s decision in Viraj Impex Pvt. Ltd. v. Union of India, which emphasized that delegated legislation becomes enforceable only upon publication in the Official Gazette and that publication is an essential requirement for transforming executive decisions into binding law. The Court also relied on the Supreme Court’s ruling in Union of India v. G.S. Chatha Rice Mills, which recognized that in the era of electronic gazettes, the precise date and time of publication assume legal significance.

Further reliance was placed on the Supreme Court’s observations in Director General of Foreign Trade v. Kanak Exports, wherein it was held that subordinate legislation ordinarily operates prospectively unless the parent statute expressly authorizes retrospective operation. The Court also noted the Gujarat High Court’s decision dealing with the same notification, wherein it had been held that the notification could not retrospectively affect consignments that had already landed in India prior to its publication.

Applying these principles, the Delhi High Court found that the factual position in the present case was similar to that before the Gujarat High Court. The consignments had been dispatched before the notification came into force, and the final consignment had arrived at the Indian port of import on 2 April 2026 at 01:39 a.m., nearly twenty hours before the notification was published in the e-Official Gazette. The respondents did not dispute these facts.

The Court observed that prior to the notification, the imported goods fell under the “Free” category. Since the goods had been imported before the notification acquired legal force through publication, the restrictions introduced by the notification could not retrospectively apply to those consignments. Consequently, the goods were liable to be assessed and cleared under the legal regime prevailing before the notification came into effect.

Accordingly, the writ petition was allowed. The Court directed the authorities to process and release the petitioner’s goods immediately in accordance with its findings. Pending applications were also disposed of, and the Court directed that a copy of the judgment be uploaded on its website.

FULL TEXT OF THE JUDGMENT/ORDER OF DELHI HIGH COURT

1. The present petition has been filed by the petitioner under Article 226 of the Constitution of India, seeking directions to the respondents to allow clearance of goods covered under Airway Bills dated 30thMarch, 2026 and 31st March, 2026.

2. The relevant facts leading to the filing of the present petition are as follows:

i. The petitioner, M/s Bright Metal Refiners, has its registered office at Babar Road, New Delhi–110001 and is engaged in the business of importing and trading precious metals.

ii. The petitioner sought to import Platinum Alloy Jewellery studded with precious stones (Ruby), falling under Tariff Entry 71131925 of the First Schedule to the Customs Tariff Act, 1975.

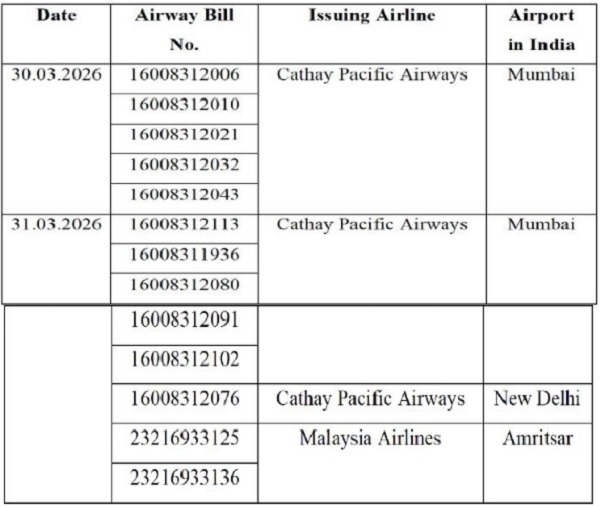

iii. On 30thMarch, 2026 and 31st March, 2026, Airway Bills were issued by Malaysia Airlines and Cathay Pacific Airlines for export of platinum alloy jewellery studded with precious stone(Ruby) from Bangkok, Thailand to different airports in India. The details of the Airway Bills are as follows:

iv. Subsequently, in exercise of powers conferred under Sections 3 and 5 of the Foreign Trade (Development & Regulation) Act, 1992, read with paragraphs 1.02 and 2.01 of the Foreign Trade Policy, 2023, Notification No. 02/2026-27 dated 01st April, 2026 was published in the e-Official Gazette on 2nd April, 2026, bearing a digital timestamp of 20:52:28 hrs, whereby the import policy of goods falling under CTH 7113 was changed from “Free” to “Restricted”.

v. The said Notification amended the import policy and stated that notwithstanding anything contained in Paragraph 1.05(b) of the Foreign Trade Policy, 2023 or any other provision, the benefit of transitional arrangements shall not be available in respect of the restrictions imposed under the said Notification. It further provided that the amended import policy shall come into force with immediate effect and shall apply irrespective of any prior contract, irrevocable letter of credit, advance payment, shipment status. Relevant paragraph of the said notification reads as under:

“2. Notwithstanding anything contained in Para 1.05(b) of the Foreign Trade Policy, 2023, (FTP) or any other provision, the benefit of transitional arrangements shall not apply to the restrictions imposed under this Notification.

3. The import policy as amended above shall come into force with immediate effect and shall apply irrespective of any prior contract, irrevocable letter of credit, advance payment, or shipment status.”

vi. The grievance of the petitioner is that the goods are not being cleared by Customs. The Customs authorities at the respective ports have orally communicated to the petitioner that the goods sought to be imported by the petitioner are not being cleared on account of aforesaid notification.

vii. Thereafter, the petitioner requested the DGFT to issue appropriate clarification and the Customs Department at the respective ports to allow clearance of its goods, on the ground that the same had been imported prior to the coming into force of Notification No. 02/2026-27 and therefore, the changed policy restriction would not apply to the subject imports, which remains unanswered by the respondents till date.

viii. The petitioner, however, received a response from the Office of the Commissioner of Customs (APSC), Mumbai, vide letter dated 16thApril, 2026, wherein reference was made to Notification No. 02/2026–27 and it was stated that the goods covered under the Bills of Entry could not be permitted for clearance without a valid import authorization/license. The petitioner was further advised to avail any other permissible remedy as it deems appropriate.

ix. The Office of the Commissioner of Customs (APSC), Mumbai, further informed the petitioner that, vide letter dated 15thApril, 2026, clarification had been sought from the Central Board of Indirect Taxes and Customs (CBIC), New Delhi, regarding the applicability of the expressions “irrespective of shipment status” and “transitional arrangements”, as is mentioned in Notification No. 02/2026– 27, in respect of the goods in question. However, till date, no clarification has been issued by CBIC in this regard.

x. In these circumstances, the petitioner has approached this Court seeking directions for clearance of the subject goods.

3. Amongst others, the contention of Prakash Shah, learned Senior Counsel for the petitioner is that a notification comes into force only from the date and time of its publication in the official Gazette. As such, the said notification acquired the force of law only on 2ndApril, 2026 at 20:52:58 hrs. To strengthen his plea, he has relied on the judgment of the Apex Court in Viraj Impex Pvt. Ltd. vs. Union of India, (2026) 38 Centax 243 (SC).

4. It is further his contention that the present case is squarely covered by the judgment passed by the Gujarat High Court in Enero Jewels Pvt. Ltd. v. Union of India, R/SCA No. 5512/2026, decided on 20thApril, 2026, wherein it was held that the aforesaid Notification would come into force only when it is digitally signed in the Official Gazette. The Court further held that where the goods had landed prior to the publication of the Notification, the effect of such Notification could not operate retrospectively to such goods, particularly when the Notification came to be published nearly 22 hours after the arrival of the goods therein.

5. It is his submission that the last consignment of the petitioner reached the Indian ports on 02ndApril, 2026 at 01:39 AM, which was about 20 hours prior to the date and time when Notification No. 02/2026–27 was published in the Official Gazette.

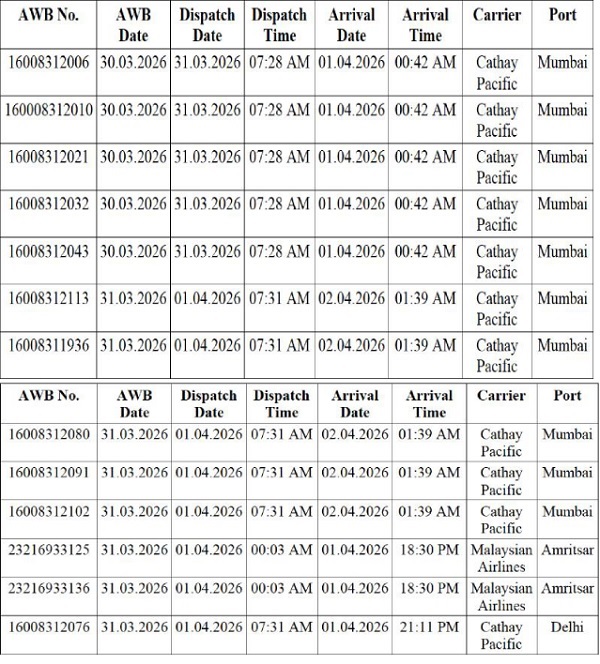

6. The learned Senior Counsel for the petitioner has provided a tabular chart detailing all his consignments, along with their respective airway bill numbers and time of arrival. The said chart is reproduced hereinbelow:

7. Further, the learned Senior Counsel would urge that paragraphs 2 and 3 of the Notification apply only to goods shipped/dispatched after the imposition of the restriction, as the transitory provisions of paragraph 05(b) applies to goods already shipped/dispatched post such restriction. Consequently, the said provisions do not apply to the goods which already arrived in India before imposition of the restriction, as such, goods fall outside the scope of the said Notification.

8. As against above, learned counsel for the respondents would urge that no prayer was made qua the said Notification in the prayer clause. The prayer and the relief sought in the present petition cannot be granted to the petitioner unless and until the legality of the notification is decided.

9. It is submitted that there lies an alternative remedy available to the petitioner under the Foreign Trade Policy, 2023. In terms of paragraph 59 of the said Policy, the petitioner is at liberty to approach the Policy Relaxation Committee for grant of exemption, relaxation, or any other appropriate relief in cases involving genuine hardship or adverse impact on trade. In view of the availability of such alternative remedy, this Court ought not to entertain the present petition.

10. Further, an objection as to the territorial jurisdiction of this Court has also been raised by the respondents, stating that the petition has joined multiple causes of action, most of which do not arise in the territorial jurisdiction of this Court.

11. It is their contention that the Notification explicitly excludes the applicability of paragraph 1.05(b) relating to transitional protection, and therefore, the legislative intent is clear and overriding.

12. According to them, though the shipment was dispatched on 30th and 31stMarch, 2026, and the Bills of Entry were filed on 03rd April, 2026 and 07th April, 2026, the fact remains that the Notification came into effect on 02nd April, 2026 at 20:52:28 IST, and the goods had not been cleared prior to that date. Thus, the import remained incomplete until clearance and, therefore, the subject goods are subject to the restriction.

13. It is claimed that, pursuant to the representation made by Customs (Amritsar) to the DGFT, the DGFT issued an Office Memorandum dated 13thMay, 2026, stating that any import consignment not cleared before 1st April, 2026 would be governed by the revised restricted policy, irrespective of the date of arrival of the goods or the date of filing of the Bills of Entry.

14. In rebuttal to the aforesaid contentions of the respondents, the learned Senior Counsel for petitioner has submitted that the date of clearance of the goods is wholly irrelevant and the relevant date for reckoning import is defined, under Paragraph 2.17 of the Foreign Trade Policy, 2023 read with Paragraph 11.11 of the Handbook of Procedures, 2023, as the date of shipment/dispatch of the goods from the supplying country, and not the date of arrival of the goods at an Indian port or their subsequent clearance.

15. In regard to the contention that there exists an alternative remedy, the petitioner submits that the same is misconceived and the said paragraph does not provide for any effective remedy in law. So also, the fact that when the impugned Notification itself has no application to the petitioner’s consignments (the date of import being prior to its coming into force), the question of seeking any authorisation or approaching the Policy Relaxation Committee does not arise.

16. According to the petitioner, it is well settled that rules or regulations, being in the nature of subordinate legislation, if found to be ultra vires, are liable to be disregarded by the Courts when the question of their enforcement arises. The mere absence of a specific relief seeking to strike down or declare such provisions ultra vires cannot preclude the Court from refusing to enforce them. Reliance in this regard has been placed on the judgment of M/S Shree Bhagwati Steel Rolling Mills vs Commnr. Of Central Excise &Anr (2016) 3 SCC 643.

17. We have heard the learned counsel for the parties.

18. Before we begin to proceed and decide the present petition on merits, we may deal with the objection raised by the respondents that there is no specific relief prayed qua the validity of the said notification and the relief sought for cannot be granted unless and until the legality of the notification is decided.

19. As against this objection, reliance was placed by the petitioner on the judgment of the Apex Court in Shree Bhagwati Steel Rolling Mills v. Commissioner of Central Excise, 2015 (326) E.L.T. 209 (S.C.) to urge that the Courts can ignore the subordinate legislation which are ultra vires when the question of their enforcement arises. Relevant paragraph of the said judgment reads as under:

“29. It would be seen that Shri Aggarwal is on firm ground because this Court has specifically stated that rules or regulations which are in the nature of subordinate legislation which are ultra vires are bound to be ignored by the Courts when the question of their enforcement arises and the mere fact that there is no specific relief sought for to strike down or declare them ultra vires would not stand in the Court’s way of not enforcing them. We also feel that since this is a question of the very jurisdiction to levy interest and is otherwise 15/05/2026, 11:40 10/15 140 covered by a Constitution Bench decision of this Court, it would be a travesty of justice if we would not to allow Shri Aggarwal to make this submission.”

20. Even otherwise, we are of the view that the nature of the relief sought in the present petition does not require us to adjudicate the validity of the notification, as the case of the petitioner is that the subject goods had already landed prior to the publication of the notification and the notification in question has no application to the facts of the present case. Therefore, if the petitioner succeeds in the said contention, there would be no relevance of examining the validity of the notification. In such an eventuality, we overrule the said objection.

21. Now, moving to the principal question that falls for consideration before this Court that whether the notification published in the e-official Gazette on 2nd April, 2026 with a time stamp of 20:52:28 hrs can be made applicable to the goods that were already booked vide Airway Bills before the notification came to be published.

22. To answer the aforesaid question, it would be pertinent to consider the judicial precedents that have a bearing on the issue.

23. We may begin by noting the decision in Viraj Impex Pvt. Ltd. (supra), wherein the Apex Court held that the legal position has been crystallised that a notification or any other form of subordinate legislation becomes enforceable only when the same is published in the manner reasonably calculated to bring it to the notice of all the persons who may be effected by it. It was observed that the requirement of publication in the gazette is not an empty formality. The relevant portion of the said judgment reads thus:-

“16. We have given our thoughtful consideration to the rival submissions and have taken note of the relevant statutory provisions. Law, to bind, must first exist. And to exist, it must be made known in the manner ordained by the legislature. Delegated legislation, unlike plenary legislation enacted by the Parliament, is framed in the executive chambers without open legislative debate. The requirement of publication in the Gazette, therefore, serves a dual constitutional purpose i.e. (a) it ensures accessibility and notice to those governed by the law, and (b) it ensures accountability and solemnity in the exercise of delegated legislative power. The requirement of publication in the Gazette, is therefore not an empty formality. It is an act by which an executive decision is transformed into law. It is precisely for this reason that courts have consistently insisted that strict compliance with the publication requirements is a condition precedent for the enforceability of delegated legislation.

17. The legal position in this regard stands crystalised by a long line of decisions of this Court. The true test of the effective commencement of a statutory order or subordinate legislation is whether it has been published in a manner reasonably calculated to bring it to the notice of all persons who may be affected by it, namely, through a mode Which Is ordinarily and generally accepted for that purpose, Johnson v. Sargant and Sons, (1918) 1 KB 101 : 87 LJ KB 122. The aforesaid principle was referred to with approval by this Court HARLA v. State of Rajasthan, 1951 Supreme Court Cases 936 and it was held that natural justice requires that before a law can become operative, it must be promulgated or published. It must be broadcast in some recognisable way so that all men may know what it is, or, at the very least, there must be some special rule or regulation or customary channel by or through which such knowledge can be acquired with exercise of due and reasonable diligence.

19. In the backdrop of aforesaid well-settled legal position, we may advert to the facts of the case in hand. The parent statute, namely the Act expressly mandates that any order regulating imports or exports shall be made by an order published in the Official Gazette. The legislature in its wisdom, has not left the mode of promulgation to executive discretion. Delegated legislation is an instrument to give effect to the policy and purpose of the parent statute. It, therefore, has to be construed in the manner that advances the object of the Act, namely to regulate foreign trade through transparent, predictable and legally certain measures. Tested on the aforesaid legal principles, coupled with requirement of publication in the Official Gazette, contained in parent statute, it is manifest that the Notification could not have acquired the force of law prior to its publication in the Official Gazette on 11.02.2016. Indeed, the Notification itself acknowledges its incompleteness by declaring that it is ‘to be published in the Gazette of India’. The acknowledgement is a confession that, until such publication, the Notification had not crossed the threshold from intention to obligation. Once the legislature has prescribed the specified mode of promulgation, the executive cannot introduce an alternative mode and attribute legal consequences to it. A Notification cannot operate in a fragmented manner. In law, it is born only upon publication in the Official Gazette, and it is from that date alone that rights may be curtailed or obligations imposed. To hold otherwise, would permit unpublished delegated legislation to burden citizens, a proposition expressly rejected by this Court in long line of decisions referred to supra.”

(Emphasis supplied)

24. As regards the point of time at which a notification takes effect after its publication, this issue was examined by the Apex Court in Union of India v. G.S. Chatha Rice Mills 2020 (374) E.L.T. 289 (S.C.), wherein the Court emphasized that the exact date and time of publication assume significance, especially having regard to the manner in which the gazettes are being published, has shifted from analog to digital. The same reads as under:

“58. With the change in the manner of publishing gazette notifications from analog to digital, the precise time when the gazette is published in the electronic mode assumes significance. Notification No. 5/2019, which is akin to the exercise of delegated legislative power, under the emergency power to notify and revise tariff duty under Section 8A of the Customs Tariff Act, 1975, cannot operate retrospectively, unless authorized by statute. In the era of the electronic publication of gazette notifications and electronic filing of bills of entry, the revised rate of import duty under the Notification No. 5/2019 applies to bills of entry presented for home consumption after the notification was uploaded in the e-Gazette at 20:46:58 hours on 16 February, 2019.”

25. The effect of giving a notification retrospective effect was also examined by the Apex Court in the case of Director General of Foreign Trade vs Kanak Exports 2015 (326) ELT 26, wherein it was held as under:

“108. We may, in the first instance, make this legal position clear that a delegated or subordinate legislation can only be prospective and not retrospective, unless rule making authority has been vested with power under a statute to make rules with retrospective effect. In the present case, Section 5 of the Act does not give any such power specifically to the Central Government to make rules retrospective. No doubt, this Section confer powers upon the Central Government to ‘amend ’the policy which has been framed under the aforesaid provisions. However, that by itself would not mean that such a provision empowers the Government to do so retrospective. This legal position is rightly discussed by the Bombay High Court in the impugned judgment in the following words :

“We are unable to accept the submissions of learned Additional Solicitor General. The word “amend” does not give power to make amendment retrospectively if it is used in relation to the power to make a piece of delegated legislation. The connotation of the word “amend” when it is used for the exercise of power by a legislature cannot be pressed to construe the word “amend” in relation to the power to make delegated legislation. In this regard the following observations of the Supreme Court in Accountant General and Another v. Doraiswamy – (1981) 4 SCC 93 are pertinent :

“The next question is whether clause (5) of Article 148 permits the enactment of rules having retrospective operation. It is settled law that unless a statute conferring the power to make rules provides for the making of rules with retrospective operation, the rules made pursuant to that power can have prospective operation only. An exception, however, is the proviso to Article 309. In B.S. Vadera v. Union of India – AIR 1969 SC 118, this Court held that the rules framed under the proviso to Article 309 of the Constitution could have retrospective operation. The conclusion followed from the circumstance that the power conferred under the proviso to Article 309 was intended to fill a hiatus, that is to say, until Parliament or a State Legislature enacted a law on the subject-matter of Article 309. The rules framed under the proviso to Article 309 were transient in character and were to do duty only until legislation was enacted. As interim substitutes for such legislation it was clearly intended that the rules should have the same range of operation as an Act of Parliament or of the State Legislature. The intent was reinforced by the declaration in the proviso to Article 309 that “any rules so made shall have effect subject to the provisions of any such Act”. Those features are absent in clause (5) of Article 148. There is nothing in the language of that clause to indicate that the rules framed therein were intended to serve until parliamentary legislation was enacted. All that the clause says is that the rules framed would be subject to the provisions of the Constitution and of any law made by Parliament. We are satisfied that clause (5) of Article 148 confers power on the President to frame rules operating prospectively only. Clearly then, the Rules of 1974 cannot have retrospective operation, and therefore, sub-rule (2) of Rule 1, which declares that they will be deemed to have come into force on July 27, 1956 must be held ultra vires.”

The reliance placed on the power to regulate under Section 3 of the Act is equally misconceived. Section 5 gives express power to formulate the policy and to amend it. This is specific power. The power to regulate therefore, cannot be read as a power to amend when a specific power to amend is given. If the power to regulate does not include the power to amend retrospectively such a power cannot be read into Section 3 of the Act.

Section 21 of the General Clauses Act on which reliance is placed by learned Additional Solicitor General is also of no assistance to sustain the retrospective operation of the notification. Section 21 of the General Clauses Act embodies a rule of construction, nature and extent of application of which must inevitably be governed by the relevant provisions of the statute which confers power to issue the notification. The said power must be exercised within the limits prescribed by the provisions conferring the said power. (See Gopichand v. Delhi Administration, AIR 1959 SC 609, Lachmi Narayan and Ors. v. Union of India and Ors., (1976) 2 SCC 953 and State of Kerala and Ors. v. K.G. Madhavan Pillai and Ors. – (1988) 4 SCC 669. The ratio in H.C. Suman’s case also cannot be applied because in that case it was found that Section 88 of the Delhi Cooperative Societies Act, 1972 contained the power to exempt and if the provisions of Section 12 of the said Act were to be exempted the provisions which provided that bye-laws are effective from the date of registration. The notification issued under Section 88 would exempt it and Section 88 would contain the power to exempt retrospectively. Similarly, Section 14 of the General Clauses Act has no application as it merely provides that where any power is conferred on the Government, then that power can be exercised from time to time as occasion requires.

Under that Scheme the status holder is eligible for benefits upon achieving the incremental growth of 25% of the FOB value of exports in the current year over the previous year. It therefore follows that no sooner the status holder achieves 25% incremental growth, the status holder would be entitled to the benefits under the Scheme. Immediately upon attaining the prescribed incremental growth, the status holder becomes eligible to certificate for duty free import and thereby a right vests in the exporter to receive the same.”

26. The effect of the decisions in Viraj Impex (supra) and G.S Chatha Rice Mills (supra) was examined by a Division Bench of Gujarat High Court in Enero jewels Pvt Ltd (supra). The effect of the very same notification as in the present petition was before it. The Division Bench held as follows:

“15. Hence, in our considered opinion, since the intention of the Notification was to come into force with immediate effect which in fact would be when the same has been digitally signed at 22:46:52 Hrs on 02.04.2026. Thus, the Notification came into effect after the goods already landed at the Ahmedabad Airport at 00:15 Hrs on 02.04.2026. Hence, the effect of the Notification cannot travel retrospectively to such goods, more particularly, when it is published / promulgated nearly 22 Hrs after the arrival of the goods. Therefore, the respondent nos. 4 and 5 fall in error in applying the Notification issued on 02.04.2026 to the goods of the petitioner.

16. Accordingly, the writ petition partly succeeds. The respondent nos. 4 & 5 are directed to immediately assess, clear and grant out-of-charge to the petitioner’s consignment covered under IGM No. 3020909 dated 02.04.2026, without insisting upon any import authorization / license under the impugned Notification No.2/2026-27 dated 01.04.2026 subject to fulfillment of other official procedure. Rule is made absolute to the aforesaid extent.”

27. In view of the aforementioned judgments of the Apex Court, we find ourselves in agreement with the view taken by the Gujarat High Court. The factual position in the present case does not differ from what was before the Gujarat High Court. In the present case the imported goods were dispatched from the country of export on 31st March, 2026 and 01st April, 2026 respectively, and arrived at the Indian ports of import on 01st April, 2026 and 02nd April, 2026, the tabular chart of which has been reproduced herein above. The last consignment imported by the Petitioner arrived at the Indian port of import on 02nd April, 2026 at 01:39 AM, which is prior to the time when the Notification was published. The said fact has not been disputed by the respondents. Also, admittedly before the said notification the goods sought to be imported were under the “free” category.

28. Thus, in such an eventuality, the goods in question were imported prior to the notification coming into force and are liable to be cleared in accordance with the conditions and legal position that prevailed before the issuance of the said notification.

29. In view of the aforesaid, the present petition is allowed in terms of prayer clause ‘a’.

30. We direct that the goods of the petitioner be processed for release immediately in terms of above observations.

31. Pending application, if any, also stands disposed of.

32. A copy of judgment be uploaded on the website of this Court.

Author Bio