Case Law Details

In re KGK Diamonds (I) Pvt. Ltd (CAAR Mumbai)

The Customs Authority for Advance Rulings (CAAR), Mumbai, considered an application filed by KGK Diamonds (I) Pvt. Ltd. seeking an advance ruling on the classification of natural rough diamonds bearing Galaxy/DiaExpert markings and their eligibility for exemption under Serial No. 345 of Notification No. 50/2017-Customs dated 30.06.2017. The applicant proposed to import natural rough diamonds scanned and mapped using the Sarine Galaxy® system and sought confirmation that such diamonds remained classifiable as natural rough diamonds under Customs Tariff Heading (CTH) 7102.31 and continued to qualify for Nil customs duty under the exemption notification.

The applicant explained that rough diamonds are a key raw material for manufacturing cut and polished diamonds and are imported from international markets. Under Chapter 71 of the Customs Tariff, gem-quality non-industrial rough diamonds are classifiable under CTH 7102.3100 and attract Nil duty under Serial No. 345 of Notification No. 50/2017-Customs. The notification was later amended by introducing Serial No. 345A for simply sawn diamonds following disputes regarding their classification.

According to the applicant, the proposed imports would consist of natural rough diamonds mapped using the Sarine Galaxy® system. The mapping process creates a three-dimensional model of the diamond’s internal structure to assist in planning the optimal cutting and polishing process. The applicant emphasized that the technology is non-invasive and does not involve sawing, cleaving, bruting, or any physical alteration of the diamond. It submitted that the diamonds remained unworked and therefore continued to be classifiable under CTH 7102.3100 with eligibility for exemption under Serial No. 345.

The applicant further stated that the DiaExpert markings placed on the surface of the diamonds are temporary planning marks consisting of lines, dots and numbers used solely to guide the cutting and polishing process. These markings are not permanent engravings and are removed during manufacturing. Relying on the HSN Explanatory Notes, the applicant argued that the goods fell within the category of diamonds in their natural state and not within the categories of simply sawn or semi-processed diamonds. It therefore maintained that the goods were covered by Serial No. 345 and not by Serial No. 350 relating to semi-processed, half-cut or broken diamonds.

The jurisdictional Commissionerate opposed the applicant’s interpretation. It submitted that scanning, planning and laser marking constitute processing and that the diamonds are no longer in their natural state once such activities have been carried out. According to the Commissionerate, planning and marking are integral stages in the manufacturing process and represent functional manufacturing inputs. The goods, at the time of import, are physically marked and therefore cannot be regarded as untouched rough diamonds.

The Commissionerate further argued that exemption notifications must be interpreted strictly and the burden of establishing eligibility rests on the applicant. It contended that diamonds bearing Galaxy/DiaExpert markings have undergone processing and should therefore be treated as semi-processed diamonds assessable under Serial No. 350 rather than as rough diamonds eligible for Nil duty under Serial No. 345. It also stated that such marked diamonds acquire a different commercial identity because they are prepared for cutting before importation.

During the proceedings, the applicant initially appeared through its authorised representative and reiterated that the goods were classifiable under CTH 710231 and entitled to the exemption. Although several further personal hearings were scheduled, no representative appeared on behalf of the applicant thereafter. The Authority therefore proceeded to decide the application on the basis of the material available on record and the applicable legal provisions under the Customs Act and the CAAR Regulations, 2021.

The Authority examined the relevant provisions of the Customs Tariff Act, the General Rules for Interpretation, and the HSN Explanatory Notes governing Heading 7102. It noted that the heading covers diamonds whether or not worked, but not mounted or set. The HSN Explanatory Notes distinguish between diamonds in their natural state, simply sawn or cleaved diamonds, chemically polished diamonds, polished diamonds and engraved diamonds.

After considering the applicant’s submissions and the technical literature relating to the Sarine Galaxy® and DiaExpert systems, the Authority observed that the imported diamonds would undergo scanning, planning and laser mapping using lines, dots and numbers. It considered whether the imported diamonds could still be regarded as being in their natural state and whether the markings amounted to engraving.

The Authority held that the HSN Explanatory Notes describing diamonds in their natural state cover only diamonds occurring naturally and sorted into lots or parcels. In the present case, the diamonds undergo scanning, planning and laser marking before importation. It agreed with the Commissionerate that planning is an important step in obtaining a finished diamond and that diamonds subjected to such planning and marking are no longer in their natural state.

The Authority also referred to dictionary meaning and HSN guidance relating to laser engraving. It observed that machines using laser beams are capable of engraving figures, letters and lines on resistant materials. Since the imported diamonds bear mapped lines, dots and numbers on their surface, the Authority concluded that such markings amount to engraving. As the diamonds were neither simply sawn, bruted nor cleaved, they were held to merit classification as engraved diamonds under CTH 71023990.

While considering the exemption under Notification No. 50/2017-Customs, the Authority noted that Serial No. 345 grants Nil duty to rough diamonds, whereas Serial No. 350 covers semi-processed, half-cut or broken diamonds. It held that scanning and laser planning altered the natural state of the diamonds and imparted a distinct commercial utility by enabling experts to optimise cutting, yield and brilliance. The Authority observed that naturally extracted diamonds and duly mapped diamonds possess different commercial identities and that the processing already undertaken adds value to the imported goods. Consequently, the Authority concluded that the subject goods fall within the category of semi-processed diamonds and are not entitled to the exemption available under Serial No. 345.

Accordingly, the Customs Authority for Advance Rulings ruled that diamond stones bearing Galaxy markings are classifiable under CTH 71023990 as “other” diamonds. It further held that such goods fall within the category of semi-processed diamonds and are therefore not eligible for exemption under Serial No. 345 of Notification No. 50/2017-Customs dated 30.06.2017.

FULL TEXT OF THE ORDER OF CUSTOMS AUTHORITY OF ADVANCE RULING, MUMBAI

KGK Diamonds (I) Pvt Ltd. (having IEC No. 0388087684) having its registered office at DE-4011-16, Tower-D, Bharat Diamond Bourse, BKC, Bandra (East), Mumbai-400 051 and hereinafter referred to as ‘the applicant’, in short) filed application (CAAR-1) for advance ruling before the Customs Authority for Advance Rulings, Mumbai (CAAR in short). The said application was received in the secretariat of the CAAR, Mumbai on 08.01.2026 along with enclosures in terms of Section 2814 (1) of the Customs Act, 1962 (hereinafter referred to as the ‘Act’ also). The applicant is seeking advance ruling on the issue of classification of the rough diamond stones with Galaxy mark on them & eligibility for exemption under serial Number 345 of Notification 50/2017-Cus dated 30.06.2017.

2. The Company is equipped with cutting edge technology for processing of rough Diamond in to Cut and Polished Diamond at its factory premises located at 4th Floor, Southern Portion, Plot No. 2 & 3, The Purushottam Ginning Mills Compound Khand, Surat-395 008 and is one of the leading manufacturers and exporters of Cut and Polished Diamond.

2.2 Rough Diamond, a key raw material for its manufacturing activities, is essentially sourced by the company from international markets. Thus, the Applicant is regularly importing ‘Natural Rough Diamonds’ from the Global market. The consignments of ‘Natural Rough Diamond’ arc either cleared at Precious Cargo Customs Clearance Center, Bharat Diamond Bourse, I3andra-Kurla Complex, Bandra (East), Mumbai or at Surat Diamond Bourse & Surat IIira Bourse located at Surat (Gujarat).

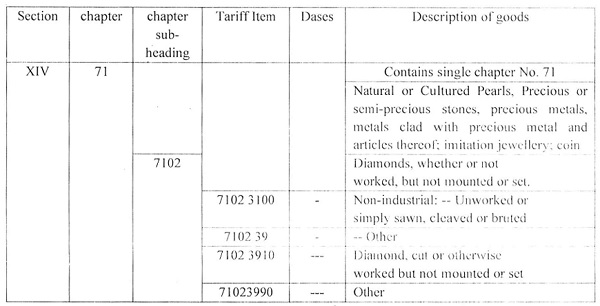

2.3 ‘Natural Rough Diamonds’ is covered under Chapter 71 of the Section-XIV of the Harmonized System of Nomenclature (IISN) developed by World Customs Organization (WC0). Heading, sub-heading and tariff entry for the ‘Natural Rough Diamond is tabulated hereunder:

Table-I

| Heading | Sub- heading | Sub-heading dashes. | Description |

| 71.02 | – | Diamonds whether or not worked, but not mounted or set | |

| 7102.10 | – | Unsorted | |

| – | Industrial | ||

| 7102.21 | – – | Unworked or simply sawn, cleaved or bruted | |

| – | Non Industrial | ||

| 7102.31 | Unworked or simply sawn, cleaved or bruted | ||

| 7102.39 | – – | Others |

2.4 Thus, the Gem quality (Non industrial) ‘Rough Diamonds’ are classifiable at CTH 7102 3100 and attract Nil rate of duty in terms of Sr. No. 345 of the Notification No. 50/2017-Cus dated 30.06.2017. The said Notification was further amended vide Notification No. 02/2022-eus dated 01.02.2022. Relevant entries arc tabulated hereunder:

Table-II

| Sr. No. | Chapter or Heading or sub- heading or Tariff item | Description of goods | Sid rate | Integrated goods and service tax | Condition No. |

| 1 | 2 | 3 | 4 | 5 | 6 |

| 345 | 71 | Rough diamonds (Industrial or non- industrial) | Nil | – | – |

| 345 A | 7102.21 & 7102.3100 | Simply Sawn Diamonds– | Nil | – | 110 |

| 350 | 71 | Diamonds including lab grown diamonds-semi- processed, half-cut or broken | 5 % | – | – |

2.5 Introduction of Sr. No. 345A was necessitated owing to the dispute pertaining to the classification of ‘sawn rough diamond’ & consequent demand of duty by the field formation. Prior to the introduction of Sr. No. 345A, the duty was demanded on the pretext that the ‘Sawn Rough Diamond’ is semi-processed and hence appropriately falls at Sr. No.350 of the Notification. Aggrieved by the decision, the trade filed appeals before the commissioner (Appeal) / Tribunal giving rise to litigation. However, finally the matter was put to rest by CBIC vide CBIC Notification No. 70/2024-Cus dated 23.10.2024 with retrospective effect.

Against this background, the Applicant wishes to import ‘Natural Rough Diamond’ duly mapped using Sarine Galaxy® technology. The process of mapping a rough diamond using the Sarine Galaxy® system is generally referred to as inclusion mapping or internal mapping. This technology is crucial for the subsequent steps of diamond planning and cutting, as it creates a detailed 3D model that allows the planner to determine the optimal way to cut the rough stone to maximize its value, minimize imperfections, and achieve the best possible polished diamond. However, the process does not involve any activity amounting to ‘simply sawn’. ‘cleaved’ or ‘batted’. In fact the technology is a non-invasive scanning process. Therelbre, the natural rough diamond remains unworked and therefore, classifiable at CTH-7102 3100 and eligible for exemption under Sr. No. 345 of the Notification No. 50/2017-cus dated 30.06.2017. However, learning from the past experiences, the applicant made this application for advance ruling on the classification and eligibility under Sr. No. 345 of the Notification No. 50/207-cus dated 30.06.2017 to avoid future litigation, if any.

2.6 NATURE OF ACTIVITY (PROPOSED/PRESENT) ON WHICH ADVANCE RULING IS SOUGHT (6)

The applicants propose to import Natural Rough Diamonds duly mapped (line, dots & numbers) on the surface using Sarine Galaxy® system. That means rough, uncut natural diamond has undergone a detailed analysis using advanced scanning and imaging technology to create a precise 3D map of its internal structure. This mapping process allows expert diamond cutters to plan the optimal way to cut and polish the stone to maximize its value, yield (the amount of usable diamond), and brilliance

The core functionality of the Sarine Galaxy® system for mapping a rough diamond’s internal inclusions is performed without physically disturbing or altering the diamond’s surface. The technology is a non-invasive scanning process.

How it Works

The system works by using a proprietary scanner (similar to medical MRI technology) to “see through” the rough stone and create a high-resolution 3D map of its internal features, such as inclusions and flaws. This process is possible due to a material engineering breakthrough that makes the diamond virtually transparent to the scanner, allowing for internal assessment without requiring any physical changes to the stone.

Key features of this non-invasive process include:

> No “windows” are opened: In older, alternative techniques, manufacturers had to polish “windows” on the rough diamond to view internal inclusions, which is not necessary with the Galaxy system.

> No pre-processing: The scanning is done automatically on the rough stone, regardless of frosting or minor coatings on its natural surface.

> Separate surface mapping: While the Galaxy maps internal inclusions, the external surface is mapped using a separate, also non-invasive, laser technology called the DiaExpert® system, which creates a 3D model of the outer texture and grooves.

This non-invasive approach is a major advancement in the diamond industry, enabling manufacturers to plan the optimal way to cut and polish a diamond to maximize its value without the risks associated with physically altering the rough stone beforehand

3. Applicant’s interpretation of laws/facts:

QUESTION OF LAW OR FACT ON WHICH ADVANCE RULING REQUIRED-

(I) classification of goods under the Customs ‘Tariff Act, 1975;

(II) Applicability of Sr. No. 345 of Notification No. 50/2017-cus

3.1 STATEMENT OF RELEVANT FACTS HAVING A BEARING ON THE QUESTION(S) RAISED:

This is to humbly submit that `DiaExpert markings’ are surface-level specific planning marks are distinct from permanent engravings. These markings serve as guides for sawing, cutting, and polishing the rough stone to achieve the optimal polished diamond. In other words, markings created by the Sarin DiaExpert system on a surface of the rough diamond are highly precise and used for planning the cutting process; they are not permanent engravings. Instead, they are typically temporary marks designed to guide the manufacturing process and are removed during the polishing and cutting stages. In the light of the nature of marking, the classification of the such diamonds and applicability of the exemption notification are stated hereunder:

3.2 Statement containing the applicant’s interpretation of law and/or facts, as the case may be, in respect of the aforesaid question(s) Classification of Natural Rough Diamond:

Sub-heading 7102.31 covers:

(1) Diamonds in their natural state, i, e., they they occur in deposits or extracts from the parent rock, sorted into lots or parcels;

(ii) Diamond simply sawn, cleaved (by splitting along the natural plane of the layers), buried or which have only a small number of polished facets (e.g. so-called windows, which are mostly made to allow expert examination of the infernal characteristics of the rough diamonds), stones which have only a provisional shape and clearly have to be .further worked;

(iii) Tumbled diamonds of which the surface has been rendered glossy and shiny by chemical treatment, also known a chemical polishing. Chemical polishing is different from traditional abrasive polishing in that the diamonds are not mounted individually and polished on the polishing wheel, but are loaded in hulk into a chemical reactor.

In the instant case ‘Natural Rough Diamonds’ falls in the category (i) above and therefore, rightly classifiable at CTII-7102.31.

3.3 ‘Natural Rough Diamond bearing `DiaExpert markings’ on surface are covered under Sr. No. 345 of the Notification No. 50/2017-cus:

Sr. No. 345 of the Notification No. 50/2017-cus dated 30.06.2017 covers ‘Rough diamonds (industrial or non- industrial)’ whereas, Sr. No. 345 A covers ‘Simply Sawn Diamonds’. As said diamonds arc not sawn, it is rightly covered Sr. No. 345.

Further. Sr. No. 350 covers ‘Diamonds including lab grown diamonds-which are semi-processed. half-cut or broken. As cutting process is not involved in the instant case, the said Sr. No. 350 is also ruled out.

Port of Import and reply from concerned jurisdictional Commissionerate

4.1 The applicant in their CAAR-1 indicated that they intend to import the subject goods i.e. classification of the rough diamond stones with Galaxy mark on them at the jurisdiction of Office of the Commissioner of Customs, Surat Diamond Bourse, Surat, Ahmedabad. The application was forwarded to the Office of the concerned Commissionerate for their comments on 23.01.2026, 13.02.2026, 02.03.2026 and 20.03.2026. Comments were received from the jurisdictional Commissionerate vide letter dated–26.03.2026 wherein it is submitted that:

4.1.1 The applicant seeks to import diamonds bearing planning and surface markings as unworked rough stones on nil duty. However, the facts and legal framework demonstrate that such diamonds have undergone a stage of processing and therefore, the Galaxy / DiaExpert marked diamonds should not be treated as “Rough Diamonds” Under Sr. No. 345 of the Notification No. 50/2017 dated 30.06.2017 on the following grounds.

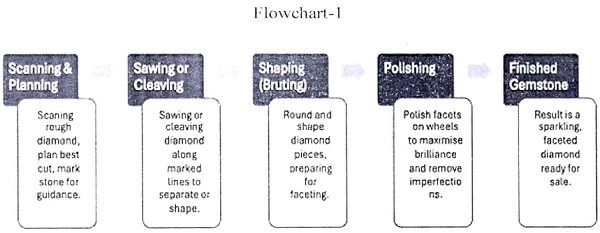

4.1.2 Cutting and polishing a diamond begins with scanning and planning of the rough stone to determine the best yield. The diamond is then sawn or cleaved, shaped through bruiting, and finally polished on rotating wheels to create facets that maximise brilliance. Each stage removes imperfections and gradually transforms the rough crystal into a finished, sparkling gemstone. A. flowchart has been prepared for ready reference below:

4.2 Legal Framework

Tariff Heading 7102

CTH 7102 covers diamonds “whether or not worked, but not mounted or set.” However, the HSN Explanatory Notes clarify that rough diamonds under sub-heading 7102.31 are:

“Diamonds in their natural state.–

Any activity that alters the natural state—physically’ or commercially –removes the stone from this category. Therefore, once the diamonds go through scanning and planning phase and marked by laser, the same stop falling under the category of being in natural state.

4.4 Exemption Notification No. 50/2017 dated 30.06.2017 dated 30.06.2017.

| Sr. No. | Chapter or Heading or sub-heading or Tariff item | Description of goods | Std rate | Integrated goods and service tax | Condition No. |

| 345 | 71 | Rough diamonds (industrial or non-industrial) | Nil | — | – |

| 350 | 71 | Diamonds including lab grown diamonds – semi-processed, half-cut or broken | 5% | – | – |

Sr. No. 345 grants NIL duty only to:

“Rough diamonds (industrial or non-industrial).”

Exemptions must he interpreted strictly, and the burden lies on the applicant to prove eligibility.

Further, Sr. No. 350 of Notification No. 50/2017 dated 30.06.2017 Semi-processed diamonds

Sr. No. 350 covers:

“Diamonds which are semi-processed, half-cut or broken.” From the above discussion, it may be inferred that the diamonds gone through galaxy marking enters into the phase of processing, hence falls under the criteria of Semi-processed diamonds, therefore the benefit of Sr. NO. 350 of Notification No. 50/2017 dated 30.06.2017 should not he extended to the goods under question.

4.5 Factual Position: The applicant has admitted that:

- The diamonds undergo Galaxy scanning for internal mapping.

- The DialExpert system applies surface markings (lines, dots, numbers).

- These markings guide sawing, cleaving. ;Ind.

- The markings are applied before import.

These facts demonstrate that the diamonds are not in their natural state at the time of import.

4.6 Arguments Against Classification as Rough Diamonds

i. Physical markings constitute “working” or “processing”

The applicant claims the process is “non-invasive,” but this is contradicted by their own admission that markings are physically applied to the surface. Any physical alteration– temporary or permanent—constitutes working under tariff interpretation principles.

ii. Planning and marking arc integral stages of manufacturing

In the diamond industry; planning is the first step of processing. The markings are not incidental; they are functional manufacturing inputs. Once a diamond is marked for cutting, it has entered the production workflow, and cannot be treated as an untouched rough stone.

iii. Condition at the time of importation

Classification and eligibility of notification benefit depend on the condition of the goods at the time of importation i.e. the condition in which the goods arrive in India. Even if markings are later removed, the imported goods are marked and altered, and therefore not in “rough form”.

4.7 Marked diamonds have a different commercial identity

A diamond that has undergone planning and marking is no longer traded as a raw commodity. Its commercial identity is that of a pre-processed stone, prepared for cutting. Classification must reflect commercial reality.

4.8 In case of simply sawn diamonds, the Notification No. 50/2017 dated 30.06.2017 was amended and Sr. No. 345A of the with a policy condition as mentioned therein was inserted. On the same line, since there is no clear notification Sr No. for the said goods and the nature of the goods are not in their natural state at the time of importation, this office opines that the benefit of Sr. No. 345 of the Notification No. 50/2017 dated 30.06.2017 should not he extended to such goods.

For the reasons stated above, it is submitted that:

- Galaxy/DiaExpert-marked diamonds should not be considered as rough diamonds in their natural state.

- They have undergone processing and physical alteration.

- They do not appear to qualify for exemption under Sr. No. 345.

- They are appropriately assessable on merit duty against Sr. No. 350 of Notification No. 50/2017 dated 30.06.2017.

The application for advance ruling should therefore be rejected. and the goods should be assessed on merit duty as per Sr. No. 350 of Notification No. 50/2017 dated 30.06.2017.

Details of Hearing

5.1 A hearing was held on 13.02.2026 wherein the authorised representative appeared for the P11 on behalf of the applicant and reiterated the contention submitted with the application. Ile contended that the subject goods arc rough diamond stones with Galaxy mark. classifiable under Oil 710231 and are eligible for notification benefit of Sr. No. 345 of the Notification No. 50/2017 dated 30.06.2017. Further, they requested for another personal hearing.

In this regard, personal hearing was scheduled on 25.02.2026. 24.03.2026. 06.04.2026, 13.05.2026 and 19.05.2026 but no one appeared on behalf of the applicant. Also. the applicant has not requested for further adjournment.

5.2 Nobody appeared for PI-I from the department side.

Discussion and findings

6.1 I have considered all the materials placed before me in respect of the subject goods. I have gone through the submissions made by the applicant during the personal hearing. I proceed to pronounce a ruling on the basis of information available on record as well as existing legal framework.

6.2 At the outset, I find that the issue raised in the question in the Form CAAR-I is squarely covered under Section 2811(2) of the Customs Act, 1962. being a matter related to classification of goods under the provisions of this Act.

6.3 Before deciding the issue, let me deliberate on the legal framework prescribed in Customs Tariff Act, 1975; Chapter/ Section notes along with HSN explanatory notes. As per Rule 1 of GRI. the titles of Sections, Chapters and sub-Chapters arc provided for ease of reference only for legal purposes, classification shall he determined according to the terms of the headings and any relative Section or Chapter Notes.

6.4 Rule 1 of the General Rules for Interpretation provides that the classification of goods shall be determined according to the terms of the headings of the tariff and any relative Section notes or Chapter notes and thus, gives precedence to this while classifying a product. Rules 2 to 6 provide the general guidelines for classification of goods under the appropriate sub-heading. In the event the goods cannot be classified solely on the basis of Rule 1, and if the headings and section or chapter notes do not otherwise require, the remaining Rules 2 to 6 may then be applied in sequential order.

6.5 Also. it is pertinent to mention the para 19 of the CAAR regulations, 2021, which provides that

19. Hearing of application ex parte. – Where on the day fixed for hearing or any other day to which the case is adjourned, the applicant or the Principal Commissioner or Commissioner does not appear in person or through an authorised representative when the application is called for hearing, the Authority may dispose of the application ex parte on merits :

Provided that where an application has been disposed of under this rule and the applicant or the Principal Commissioner or Commissioner, as the case may be, applies within seven days

of receipt copy of the order or advance ruling and the Authority is satisfied that there Was sufficient cause “Or his non-appearance when the application was called for hearing, the Authority may, after allowing the opposite party a reasonable opportunity of being heard, make an order setting aside the cx parte order or advance ruling and restore the application for fresh hearing?.

It is observed that adequate opportunities of personal hearing were granted to the applicant. However, none appeared on behalf of the applicant despite the opportunities so afforded. Therefore, in terms of the powers conferred under the CAAR Regulations, 2021, the application is being taken up for decision on the basis of the material available on record and on merits.

6.6 At first, I will discuss the classification of goods i.e. rough diamond stones with Galaxy mark on them- In the present case, the applicant proposes to import Natural Rough Diamonds duly mapped (line. dots & numbers) on the surface using Sarine Galaxy® system. The core functionality of the Sarine Galaxy® system for mapping a rough diamond’s internal inclusions is performed without physically disturbing or altering the diamond’s surface. The technology is a non-invasive scanning process.

The system works by using a proprietary scanner (similar to medical MRI technology) to “see through” the rough stone and create a high-resolution 3D map of its internal features, such as inclusions and flaws. This

Key features of this non-invasive process include:

> No “windows” are opened: In older, alternative techniques, manufacturers had to polish “windows” on the rough diamond to view internal inclusions, which is not necessary with the Galaxy system.

> No pre-processing: The scanning is done automatically on the rough stone, regardless of frosting or minor coatings on its natural surface.

> Separate surface mapping: While the Galaxy maps internal inclusions. the external surface is mapped using a separate, also non-invasive, laser technology called the DiaExpert®®® system, which creates a 3D model of the outer texture and grooves.

The applicant submitted that ‘DiaExper markings’ are surface-level specific planning marks are distinct from permanent engravings. These markings serve as guides for sawing, cutting, and polishing the rough stone to achieve the optimal polished diamond. In other words, markings created by the Sarin DiaExpert system on a surface of the rough diamond are highly precise and used for planning the cutting process: they are not permanent engravings. Instead, they are typically temporary marks designed to guide the manufacturing process and are removed during the polishing and cutting stages.

6.6.2 As per Schedule I of ITC(HS) based import policy, relevant entries of heading, subheading and tariff item are as under:

The relevant HSN explanatory notes are reproduced here:

The heading covers unworked stones, and stones worked, e.g., by cleaving, sawing, hinting, tumbling. „feting, grinding. polishing, drilling, engraving (including cameos and intaglios). preparing as doublets, provided they are neither set nor mounted.

Sub-heading 710′.31 and 7102.39:

These subheadings cover natural diamonds which, because of their characteristic features (colour, clarity or purity;, transparency, ‘etc.) are suitable for use by jewellers, goldsmiths or silversmiths.

Sub-heading 7102.31 covers:

(i) Diamonds in their natural state, i. e., as they occur in deposits or extracts from the parent rock, sorted into lots or parcels;

(ii) Diamond imply sawn, cleaved (by splitting along the natural plane of the layers), bruted or which have Only a -small number of polished .facets (e.g. so-called Windows, which are mostly made to allow expert examination of the internal characteristics of the rough diamonds), stones which have only a provisional shape and clearly have to be further worked:

(iii) Tumbled diamonds of which the surface has been rendered glossy and shiny by chemical treatment, also known a chemical polishing. Chemical polishing is different from traditional abrasive polishing in that the diamonds are not mounted individually and polished on the polishing wheel, but are loaded in bulk into a chemical reactor.

Subheading 7102.39 covers:

(1) Polished diamonds having multiple flat polished surfaces or facets, which do not require to he further worked before being used in jewellery;

(2) Drilled diamonds., engraved diamonds (including cameos and intaglios) and diamonds prepared as doublets or triplets.

(3) Diamonds which were subjected to polishing and drilling or engraving and were broken during these operations, as well as polished diamonds broken during their transaction or storage.

In the present case, as per the additional documents i.e. user guide by Sarin technologies Ltd. submitted by the applicant, the rough diamonds are going to be scanned and then duly mapped (line, dots & numbers) on the surface using Sarine Galaxy® system and the external surface is mapped using a separate, also non-invasive, laser technology called the DiaExpert system, which creates a 3D model of the outer texture and grooves. In order to determine the CTH, it is pertinent to discuss that imported goods are diamonds inn their natural states or not and markings on the diamond can be considered as engraving or not.

The HSN explanatory notes of CTEI 7102.31 provides that “Diamonds in their natural state, i. e., as they occur in deposits or extracts from the parent rock, sorted into lots or parcels;”, it only covers those diamonds which are occurred in deposits or extracts from the parent rock, sorted into lots or parcels, however, inn the present case, diamonds occurred naturally are processed further by way of scanning, planning and laser marking/engraving. Also, a diamond that has undergone planning and marking is no longer traded as a raw commodity. Its commercial identity is that of a pre-processed stone, prepared for cutting. In view of the above, it is implied that the subject goods cannot be considered as diamond in their natural state.

The jurisdictional Commissionerate commented that-

Any activity that alters. the natural state physically or commercially removes the stone from this category. Therefore, once the diamonds go through scanning and planning phase and marked by laser, the same stop falling under the category of being in natural state.

Further, in the diamond industry; planning is the first step of processing. The markings are not incidental; they are functional manufacturing inputs. Once a diamond is marked for cutting, it has entered the production workflow, and cannot be treated as an untouched rough stone. I also concur with the above findings and reasoning that scanning and planning is an important part of obtaining a finished diamond from the raw diamonds.

It is also observed that the term “engraving is not defined in chapter 71. According to Oxford Dictionary the word “Engrave” means cut (a design) as lines on a metal plate for printing. Also, reference is taken from the HSN explanatory notes of heading 8456 provides-

(A) MACHINE-TOOLS FOR VIORKING BY LASER OR OTHER LIGHT OR PHOTON BEAM PROCESSES

Laser-beam machining (photonic machining) consists of bombarding a target with photons. This group covers, in particular, Machines for drilling (metals., rubies for watches, etc.), machines for cutting metal or other hard materials and machines for engraving (figures, letters, lines etc.) on various highly resistant materials.

From the above, it is clear that lines on diamond come under definition of engraving. Since, the subject goods proposed to be imported are diamonds with mapped (line. dots & numbers) on the surface and with, Further, the subject goods are not sawn. bruted or cleaved, therefore, the subject goods fall under purview of engraved diamond merit classification under CTI 71023990.

6.7 Now, I will discuss about the exemption benefit sr no. 345 of notification no. 50/2017-cus dated 30.06.2017. The relevant part of the notification is as under:

| Item | Chapter / Heading / Sub-heading / Tariff Item | Description of Goods | Std Rate | Integrated Goods and Services Tax | Condition No. |

| (1) | (2) | (3) | (4) | (5) | (6) |

| 345 | 71 | Rough diamonds (industrial or non-industrial) | Nil | – | – |

| 345A | 7102.21 & 7102.31.00 | Simply Sawn Diamonds | NIL | – | 110 |

| 350 | 71 | Diamonds including lab grown diamonds – semi-processed, half-cut or broken | 5% | – | – |

In –view of the above discussion, I am of the opinion that the subject goods have undergone scanning and plane marking process by laser which render the goods under processed diamond. I agree with the jurisdictional Commission rate’s point of view that any kind of activity that alter the natural state physically or commercially removes the diamonds from category (i) of the sub-heading 7102.31, as described in the IISN Explanatory Notes to Heading 7102.

The subject goods arc marked in such a way that allows expert to plan the optimal way to cut and polish the stone to maximize its value, yield and brilliance. Such operations arc undertaken with a definite manufacturing objective and impart a distinct commercial utility to the diamonds. It is implied that diamonds extracted naturally and diamonds duly mapped have different commercial identity and duly mapped diamonds command a value attributable to the processing already undertaken. Therefore, the subject goods fall under the category of semi-processed diamonds as the diamonds arc engraved; therefore, sr. no. 345 of the notification no. 50/2017 dated 30.06.2017 is not applicable in the present case.

8. In view of the above facts and circumstances of the case, I reach to conclusion that

The product in question i.e. diamond stones with Galaxy mark on them would attracts, merit classification under C71 71023390 as other of the First Schedule of the Custom Thrill’ Act, 1975 and since the subject goods- falls under purview of semi-processed diamond, therefore, sr. no. 345 of the notification no. 50/2017 dated 30.06.2017 is not applicable.

9. I rule accordingly.

Author Bio