Case Law Details

In re Lupin Limited (CAAR Mumbai)

The Customs Authority for Advance Rulings (CAAR), Mumbai, considered an application seeking clarification on the applicability of concessional customs duty under Notification No. 45/2025-Customs for goods imported by a pharmaceutical company’s DSIR-recognized Research and Development (R&D) units. The applicant sought rulings on three issues: whether its DSIR-recognized R&D units qualified as eligible research institutions; whether R&D goods imported for activities before manufacture of an Exhibit Batch qualified for the concession; and whether goods imported for manufacture of an Exhibit Batch were also eligible.

The applicant explained that it operates DSIR-recognized in-house R&D facilities at Pune and Aurangabad engaged in pharmaceutical research. It described its multi-stage R&D process, beginning with project initiation, obtaining test and import licences where required, formulation development, analytical testing, stability studies, bioequivalence studies, and finally manufacture of an Exhibit Batch under technical supervision before seeking regulatory approval. According to the applicant, the imported materials—including Reference Listed Drugs (RLDs), Active Pharmaceutical Ingredients (APIs), impurities, chemicals, reagents, enzyme powders, packaging materials, vials, canisters, pre-filled syringes and similar goods—are used exclusively for research and are substantially or wholly consumed during experimentation, testing and analytical processes.

The applicant submitted that Notification No. 45/2025-Customs grants concessional customs duty to DSIR-recognized research institutions importing specified goods, including consumables, subject to prescribed conditions such as certification by the Head of the institution and exclusive research use. It argued that its R&D units fulfilled these conditions and that the imported materials should qualify as consumables because they are exhausted during research. It also contended that manufacture of the Exhibit Batch is an inseparable extension of the R&D process, undertaken solely for validation, testing and regulatory purposes without any commercial sale, and therefore imports for that stage should also qualify for the concession.

The jurisdictional Commissionerate did not furnish comments despite being requested. During the personal hearing, the applicant reiterated that it complied with all conditions of the notification and explained that higher-volume testing at the factory was necessary for obtaining commercial approval. No departmental representative appeared at the hearing.

The Authority held that the application was maintainable since it concerned the applicability of an exemption notification issued under the Customs Act. It observed that Notification No. 45/2025-Customs grants concessional customs duty only when all prescribed conditions are cumulatively satisfied. These include DSIR recognition of the importing institution, import of specified goods, certification by the Head of the institution that the goods are essential for research purposes, exclusive research use, and compliance with post-import conditions, including the restriction against transfer or sale of imported goods. The Authority emphasized that DSIR recognition alone does not automatically confer eligibility.

After examining the applicant’s documents, the Authority found that the applicant’s R&D centres at Pune and Aurangabad possessed valid DSIR recognition and therefore satisfied the institutional eligibility requirement under the notification. However, it clarified that eligibility also depended on whether the imported goods met the substantive conditions prescribed in the notification.

Regarding goods imported before manufacture of the Exhibit Batch, the Authority accepted that the notification covers consumables used in research. It noted that the expression “consumables” is undefined in the notification but agreed that goods substantially consumed during experimentation, formulation development, analytical evaluation, validation, stability studies and similar research activities could generally fall within that expression. Accordingly, materials such as RLDs, APIs, impurities, chemicals, reagents, enzyme powders and similar research materials imported by the DSIR-recognized R&D units would generally qualify as consumables, provided all conditions of the notification are fulfilled and the nature and end-use of each import are verified at the time of import.

The Authority separately considered imports connected with manufacture of the Exhibit Batch. It acknowledged that the Exhibit Batch forms an important stage of pharmaceutical development and is manufactured for validation and regulatory purposes rather than commercial sale. However, it held that the notification grants exemption only where the importing entity itself is a DSIR-recognized research institution and all prescribed conditions are strictly complied with. The Authority distinguished two situations: first, where goods imported by the R&D unit are later transferred to a manufacturing facility; and second, where the manufacturing facility directly imports the goods. In the first situation, transfer of imported goods to the manufacturing facility violates the notification’s prohibition on transfer for five years after import. In the second situation, the manufacturing facility itself is not a DSIR-recognized research institution and therefore does not satisfy the primary eligibility requirement. Consequently, goods imported for manufacture of the Exhibit Batch do not qualify for the concessional benefit in either scenario.

Accordingly, the Authority ruled that the applicant’s DSIR-recognized R&D centres are eligible research institutions under Notification No. 45/2025-Customs. It further held that RLDs, APIs, impurities, chemicals, reagents, enzyme powders and similar materials consumed or substantially utilized in research activities undertaken by those R&D centres qualify as consumables eligible for the notification, subject to compliance with all prescribed conditions. However, goods transferred from the R&D centres to a manufacturing facility for manufacture of an Exhibit Batch, as well as goods imported directly by a manufacturing facility for that purpose, are not eligible for the concessional customs duty benefit.

FULL TEXT OF THE ORDER OF CUSTOMS AUTHORITY OF ADVANCE RULING, MUMBAI

Lupin Limited (having IEC No. 0391156853) (hereinafter referred to as ‘the applicant’, in short) filed application (CAAR-1) for advance ruling before the Customs Authority for Advance Rulings, Mumbai (CAAR in short). The said application was received in the secretariat of the CAAR, Mumbai on 23.02.2026 along with enclosures in terms of Section 28H (1) of the Customs Act, 1962 (hereinafter referred to as the ‘Act’ also).

2. The Applicant seeks clarification on following specific queries:

i. Whether the Applicant’s R&D units are eligible to avail the concessional Customs duty benefit under Notification 45/25?

ii. Whether R&D Goods imported by the Applicant’s R&D unit would qualify for the above concessional Custom duty benefit? Essentially these include all goods imported for the stage prior to manufacture of Exhibit Batch.

iii. Whether the R&D goods imported by the Applicant for the Exhibit Batch are eligible for availing the concessional Customs duty benefit under Notification 45/25?

3.Submission by Applicant-

3.1. OVERVIEW OF BUSINESS

3.1.1. Lupin Limited (hereinafter referred to as the ‘Applicant’) is an Indian multinational pharmaceutical company engaged in the manufacture and supply of a pharmaceutical formulations and allied products. The Applicant holds a valid Importer Exporter Code (`IEC’) bearing no. 0391156853.

3.1.2. Recognizing innovation as a key driver for long-term growth, the Applicant has consistently invested in Research and Development (`R&D’) activities. Such activities are undertaken by the Applicant from its dedicated in-house R&D facilities located in Pune & Aurangabad (`R&D units’). These R&D units are duly registered and recognized by the Department of Scientific and Industrial Research (`DSIR’).

3.1.3. In the course of carrying out such R&D activities, the Applicant procures various goods from domestic as well as overseas suppliers. An illustrative list of goods imported by the Applicant, for the purpose of its R&D activities inter alia includes Reference Listed Drugs (`RLD’), Active Pharmaceutical Ingredients (`APP), Impurities, Pre-filled Syringes, Chemicals, Packaging Materials, Vials, Canister, Enzyme Powder, Reagents and Other Allied Goods (collectively, ‘R&D Goods’). The Applicant hereby reiterates that the aforementioned list is merely illustrative in nature. Depending upon the specific requirements of each R&D project, the Applicant may import additional category of goods for R&D purposes on a project by project basis.

3.1.4. The R&D process encompassing the manner of import of R&D Goods as well as the deployment and utilization thereof across the R&D lifecycle, is explained comprehensively in the ensuing paragraphs:

3.2 OVERVIEW OF THE R&D PROCESS

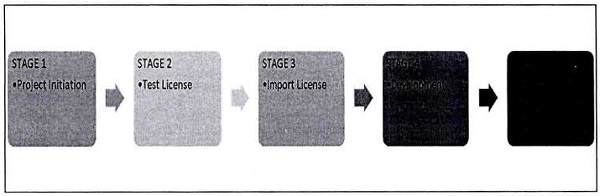

3.2.1 Pharmaceutical R&D is a highly regulated process involving multiple mutually exclusive stages as outlined below:

STAGE 1— PROJECT INITIATION

3.2.2 The R&D process begins with initiation of a project for development of a new product. At this preliminary stage, the R&D team defines the intended product characteristics, articulates the key development objectives and identifies the applicable regulatory considerations that will govern the development lifecycle.

3.2.3 This stage also includes identification of the RLD and the formulation of a Target Product Profile (`TPP’). The RLD is the approved benchmark product against which the quality, efficacy and bioequivalence of a proposed generic product are evaluated whereas the TPP delineates the intended quality attributes, bioequivalence and stability parameters that the proposed product is expected to meet, and accordingly serves as the primary reference framework guiding formulation development and associated R&D activities.

STAGE 2 — TEST LICENSE

3.2.4 Pharmaceutical R&D activities in India are regulated under the Drugs and Cosmetics Act, 1940, the Drugs and Cosmetics Rules, 1945, and the New Drugs and Clinical Trials Rules, 2019. Under this regulatory framework, a Test License is mandatory for undertaking the manufacture of drugs for examination, testing, or analysis as part of R&D.

3.2.5 Accordingly, prior to commencing any research, examination or testing of a drug for R&D purposes, the Applicant is required to obtain a Test License in Form 29. The scope of such Test License is confined to limited-scale manufacture, exclusively for R&D and testing purposes, and does not extend to commercial production.

3.2.6 The application for grant of a Test License is submitted in Form 30/ CT-11 inter alia specifying the relevant R&D facility and the products proposed to be developed. The application inter alia sets out particulars of R&D facility, details of drug proposed to be manufactured for examination, test and analysis, etc. Upon evaluation, the Licensing Authority grants the Test License for a specified period of validity.

STAGE 3 — IMPORT LICENSE

3.2.7 As stated above, for undertaking R&D activities, the Applicant is required to import R&D Goods that are essential for formulation development and analytical testing. Such requirements are duly certified by the Head of Applicant’s R&D units i.e., procurement anticipated & essential for research purposes.

3.2.8 Under the extant Foreign Trade Policy (`FTP 2023′), the import of several R&D Goods including API(s) and RLD(s) may be categorized as restricted and the imports of the same are permitted only pursuant to the grant of a specific import license (typically encompasses reference drugs, new drugs, investigational new drug, etc., meant for R&D purpose). However, other import requirements of a given R&D project may not, per se, be restricted and hence, import may not require any import license, by whatever name called, as such.

3.2.9 In compliance with the applicable regulatory framework, upon obtaining the Test License, the Applicant applies for an Import License (wherever required). Upon due scrutiny of the application and satisfaction of the prescribed conditions, the regulatory authority grants an import license in CT-17 (Import License’), authorizing the import of the specified goods solely for examination, testing and analysis in the course of R&D activities and not for commercial sale or distribution. In all other cases, where the imports are not restricted by any licensing requirements) say standard laboratory consumables, excipients or ancillary analytical materials, the Applicant may directly order or procure such goods, without the need of any regulatory intervention.

STAGE 4 — DEVELOPMENT

3.2.10 Upon receipt of the requisite materials, the R&D unit undertakes necessary inward verification and testing of the imported products to confirm their suitability for use in R&D activities i.e., as per internal Standard Operating procedures and protocols (`SOP’). Thereafter, the R&D unit commences the pre-formulation and formulation development activities, wherein trial/ development batches are prepared using the imported materials strictly for R&D purposes, with the objective of achieving and validating the parameters set out in the TPP. These batches are subjected to comprehensive analytical, dissolution, stability and performance studies to assess alignment with the TPP and to compare results against the identified RLD(s). Where required, bioequivalence studies are also conducted in accordance with applicable regulatory standards and protocols.

3.2.11 The manner of utilization of the imported R&D Goods in the development stage are summarized below:

| No | Product | Manner of utilization |

| 1 | RLD(s) | The RLD(s) are utilized as approved benchmark products for comparative testing to establish equivalence evaluation of the developed formulation. Samples of RLD(s) are subjected to detailed analytical and comparative studies, including dissolution profiling, stability assessment, impurity characterization, and performance testing, in order to establish equivalence with the proposed formulation. The RLD samples are entirely consumed during testing and analysis, with no recoverable quantity remaining post-use. |

| 2 | API(s) | API(s) are utilized as the core component in pre-formulation and formulation development activities.

The API(s) are employed in solubility, stability, and compatibility studies with excipients, followed by incorporation into laboratory-scale formulations and trial or development batches to evaluate dosage form, bioavailability, and stability parameters. During processing and testing, the API(s) undergo physical and chemical transformation and are fully consumed in the R&D process, leaving no residual material capable of recovery or reuse. |

| 3 | Impurities | Imported impurity standards are utilized for development, identification, and quantification of the impurity profile of the trial formulation. These materials are used during analytical method development, calibration exercises, validation studies, and stability testing. The impurities are consumed in micro-quantities and are completely exhausted during analytical use, with no recoverable material remaining thereafter. |

| 4 | Pre-filled syringes | Pre-filled syringes are utilized to evaluate container–closure integrity, device compatibility, sterility, and performance characteristics of the developed formulation. These syringes are used during filling operations, stability studies, sterility testing, and functional performance evaluations. The integrity of the device is irreversibly compromised during such studies, rendering the syringes unfit for reuse or recovery and resulting in complete consumption during R&D activities. |

| 5 | Chemicals | Chemicals are utilized across formulation development, analytical testing, and stability studies, including as reagents, solvents, and processing aids. Such chemicals are consumed during experimentation, sample preparation, analytical runs, and stability evaluations. By their very nature, these chemicals are fully used up or rendered unusable during the conduct of R&D activities, leaving no recoverable quantity post-consumption. |

| 6 | Packaging Materials | Packaging Materials inter alia include bottles, bottle caps, capsules, and other primary and secondary packaging materials intended for filling, storage, and evaluation of the drug product. These goods are integral to the R&D process, as they are required to assess container–closure integrity, product–pack interaction, protection against environmental factors, and overall suitability of the packaging configuration in alignment with the TPP and applicable regulatory expectations. Such packaging materials are utilized strictly in accordance with approved development and testing protocols during trial and development batches, stability studies, and performance evaluations. They are used for filling, sealing, storage, and testing under prescribed conditions and are, by their nature, fully consumed in the R&D process. These goods are incapable of reuse or diversion for commercial purposes and are exhausted entirely during formulation development, analytical testing, and stability assessments. |

| 7 | Other consumable goods including Vials, Canister, Enzyme Powder, Reagents | Other consumable goods inter alia include vials, canisters, enzyme powders and reagents, are utilized as essential inputs in the R&D process. These goods are employed at various stages of R&D inter alia for sample preparation, formulation development, analytical testing, method validation, process optimisation, and stability and performance studies, strictly in accordance with approved study protocols and internal standard operating procedures. By their very nature, these R&D goods are used only for experimental, testing, and analytical purposes and are entirely consumed, depleted, or rendered unusable during the course of the R&D process. |

3.2.12 During the development stage, the imported R&D Goods are subjected to various processing, formulation, and reaction stages, as a result of which their physical and chemical characteristics undergo transformation in the course of the R&D activities. Further, certain imported goods are meant for bulk or unit storage of the drug at different stages, which once used for this purpose and are not re-usable again and hence, are fully expended or consumed in this process thus overall contributing to the R&D project as such.

3.2.13 In view of the above, the imported R&D Goods are consumed during the development stage. Any quantities remaining unutilized are securely stored within the R& D unit as per SOPs . Further, all materials utilized for R&D purposes are separately recorded in the Applicant’s accounting system, and appropriate records are maintained to track their usage and movement.

3.2.14 Following successful completion of the laboratory-scale and pilot-scale development activities, the R&D output is progressed to the next stage of development and regulatory compliance, as outlined below.

STAGE 5 — DEVELOPMENT REPORT AND INITIATION OF TECH TRANSFER

3.2.15 Following successful completion of development stage, the R&D unit document the outcomes of the development activities in the form of a Lab Report. The Lab Report inter alia captures the formulation rationale, development data, manufacturing process, product specifications, analytical methods and stability results, and serves as the foundational technical document for progression of the product to the subsequent stage, namely, manufacture of the Exhibit Batch (also referred to as the confidence building batch or scale-up batch).

3.2.16 While the development activities up to this stage are undertaken entirely by the R&D units, the next stage necessitates execution of the developed process under manufacturing conditions to thoroughly check the scalability of the product. For this limited purpose, the R&D units engage the Applicant’s own manufacturing facility (`Factory’), which is physically outside the R&D unit, to carry out the manufacture of the Exhibit Batch in accordance with the specifications and process parameters set out in the Lab Report. This outsourcing of the Exhibit Batch manufacturing is akin to getting the product manufactured through a job worker/ contract manufacturer (though in Applicant’s case both are housed in same legal entity). Such scale-up batch manufacturing is undertaken under the technical supervision and control of the R&D units at all times, with the Factory functioning as an execution site for scale-up and validation of the developed formulation process, rather than as a commercial manufacturing unit. The batches so manufactured are neither put up for sale nor distribution under any circumstances.

3.2.17 Upon completion, the manufacturing and testing outcomes are documented and transmitted back to the R&D units for evaluation and further analysis.

3.2.18 For undertaking the manufacture Of the Exhibit Batch upon requisition by the R&D unit, the Factory is required to obtain a license to manufacture for test and analysis purposes. In accordance with the applicable regulatory protocol and Good Manufacturing Practices (`GMP’) requirements, the materials used for manufacturing the Exhibit Batch are imported directly by the Factory although the list of goods to be imported are approved by the Head of the R&D institution or units (a re-confirmation or corroboration that the manufacturing is being done at behest and for the R&D unit and not on manufacturing unit’s own account). Where such procurement involves imports, the Factory files a separate application for an Import License (if applicable). The import of overall approved list of goods (whether or not requiring an import license) is effectuated on behalf of the R&D unit.

3.2.19 The Exhibit Batch is thereafter subjected to the prescribed testing, including analytical, dissolution, stability and, where applicable, bioequivalence studies, some of which may be undertaken at the factory site itself and remainder at the R&D unit or at any Contract Site (Research Unit or Testing lab). The results are later, in totality, compiled at the R&D unit and the data so generated forms .the basis for regulatory submission by the R&D unit for eventual approval by the regulatory authorities. Based on its evaluation, the regulatory authority may grant necessary approvals allowing for commercial production.

3.2.20 It is peculiar to note that all activities undertaken prior to the approval for commercial production are viewed as R&D activities as any produced batch (whether a small batch at R&D unit or an Exhibit Batch at the Factory at behest of the R&D unit) are neither sold or distributed in the market. This implies that all procurements up to the production of Exhibit Batch corresponds to R&D activity and hence, should be construed as such.

3.2.21 At this stage, it is pertinent to note that the Exhibit Batch, in itself, constitutes an integral part of the R&D activities. The central objective of this stage is to evaluate the feasibility and robustness of the formulation and process when manufactured at larger, representative scales (a regulatory requirement to approved the research for eventual commercial production). The Applicant is not permitted to utilize or sell the goods manufactured under the Exhibit Batch for any commercial purpose, and such goods are restricted exclusively for R&D, testing, and regulatory evaluation. Accordingly, the Exhibit Batch squarely forms part of the R&D activities.

3.2.22 Notably, the entire R&D activity is directed towards drug or formulation discovery and development, and not towards commercial manufacture, as no goods are sold or distributed at this stage. The R&D process ultimately culminates in the generation of scientific data and technical reports to be used for regulatory approval. Accordingly, the nature and character of the output arising from the R&D process must be appreciated and construed within this regulatory and scientific context.

3.2.23 In certain cases, the R&D projects may be discontinued post-initiation due to scientific or commercial considerations. In such instances, the R&D unit undertakes a material reconciliation, and any residual stock is either (a) disposed or written off; or (b) transferred to other R&D projects. Hence, the essential purpose the goods are applied to remained R&D. Assuming at some stage, the underlying goods expire (being a naturally occurring event in the business/ process as such), the same are also disposed off as per applicable regulations, if any. The entire process reinforces that the goods once imported by the Applicant for R&D purposes, are not applied to any other purpose in any circumstance.

4. CONTEXTUAL CUSTOMS DUTY EXEMPTION / CONCESSION

4.1. The Central Government, vide Notification No. 51/1996 — Customs dated July 23, 1996 (`Notification 51/96′), offered concessional Customs duty benefit to DSIR-recognized R&D institutions, for the import of specified goods. The said notification has recently been subsumed and continued into a master Notification No. 45/2025—Customs dated October 24, 2025, effective from November 1, 2025 (`Notification 45/25′).

5. Applicants’ interpretation of Law:-

5.1. The Applicant firmly believes that the R&D Goods imported by the Applicant for the purposes of carrying out R&D activities, either at the R&D unit or at Factory, are eligible for the concessional Customs duty rate as per Notification 45/25.

5.2. In the ensuing paragraphs, the Applicant submits its interpretation of the law and the justification as to why the Applicant is entitled to avail concessional Customs duty benefit on the import of the R&D Goods.

STATUTORY FRAMEWORK GOVERNING CONCESSIONAL CUSTOMS DUTY FOR R&D IMPORTS

5.3. Under the Customs regulatory framework, the Government of India has, from time to time, extended various Customs duty concessions/ exemptions with the objective of encouraging and facilitating the R&D activities in India. In furtherance to this policy intent, several standalone exemption notifications have been issued over the years, including Notification 51/96, which provided concessional Customs duty benefit to DSIR-recognized R&D institutions, for the import of specified goods.

5.4. The aforesaid notification has recently been subsumed and continued under Notification 45/25. The relevant extract of Notification 45/25, insofar as it pertains to R&D-related imports, is reproduced below for ease of reference:

G.S.R. 781(E).— In exercise of the powers conferred by sub-section (1) of section 25 of the Customs Act, 1962 (52 of 1962) and sub-section (12) of section 3 of the Customs Tariff Act, 1975 (51 of 1975)… …the Central Government…, hereby exempts -….

(b) the goods of the description specified in column (3) of the Table II below or column (3) of the said Table .., when imported into India, –

(i) from so much of the duty of customs leviable thereon under the said First Schedule as is in excess of the amount calculated at the standard rate specified in the corresponding entry in column (4) of the said Table; and

(ii) from so much of the integrated tax leviable thereon under sub-section (7) of section 3 of said Customs Tariff Act…..

| No | Chapter or Heading | Description of goods | Standard rate | IGST | Condition No. |

| 70 | Any Chapter | (a) Scientific and technical instruments, apparatus, equipment (including computers);

(b) accessories, parts, consumables and live animals (for experimental purposes); (c) computer software, Compact Disc-Read Only Memory (CD-ROM), recorded magnetic tapes, microfilms, microfiches; (d) prototypes, the C.I.F. value of which does not exceed rupees .fifty thousand in a financial year , Provided it is imported by Research institutions, other than a hospital; Provided further that nothing contained in this S.No. shall have effect after the 31 st March, 2029 |

5% | – | 24 |

Condition 24 if,-

(A)

(1) The importer —

(i) is registered with the Government of India in the Department of Scientific and Industrial Research;

(ii)produces a certificate from the Head of the institution, in each case of import, certifying that the said goods are essential for research purposes and will be used for the stated purpose only,.

(iii)

(2) The goods falling under (1) above shall not be transferred or sold for a period office years .from the date of importation;

(B)….

Explanation. – For the purposes of this entry, the expression, –

(c) “Head” means —

in relation to an institution, the Director thereof (by whatever name called);

5.5. From the above, it can be observed that in order to avail concessional Customs duty benefit under Notification 45/25, the importer is required to satisfy the following key conditions:

- Qualification as a Research Institution (other than hospital) registered with DSIR;

- The imported goods should qualify as scientific instruments, equipment, parts, consumables, software or prototype (within specified value limit);

- A certificate from the Head of the Institution (i.e., the Director), certifying that the goods are essential for research purposes and will be used solely for the stated purpose only

5.6. Upon meeting the above conditions, the importer should be eligible to import goods at concessional Customs duty under Notification 45/25, subject to post-import compliance, including exclusive use of goods for research and non-transfer or sale of imported goods for 5 years from the date of importation.

5.7. Having outlined the statutory framework governing concessional Customs duty benefits, the applicability thereof to the Applicant’s imports is examined in the ensuing paragraphs.

5.8 Whether the Applicant’s R&D units are eligible to avail the concessional Customs duty benefit under Notification 45/25?

5.8.1 Notification 45/25 stipulates that concessional Customs duty is available only where the importer is a Research Institution duly recognized by the DSIR.

5.8.2 The Applicant’s in-house R&D units located at Pune and Aurangabad are engaged in research activities and are duly recognized by the DSIR vide certificate dated May 14, 2025. Accordingly, these units should qualify as eligible research institution for the purpose of availing the concessional Customs duty benefit under Notification 45/25, subject to fulfilment of other conditions specified in the said notification.

5.8.3 Thus, the Applicant’s in-house R&D units shall be eligible to avail the concessional Customs duty benefit under Notification 45/25.

5.9 Whether R&D Goods imported by the Applicant’s R&D units would qualify for the above concessional Custom duty benefit? Essentially these include all goods imported for the stage prior to manufacture of Exhibit Batch.

5.9.1 To assess the eligibility of R&D Goods for the concessional Customs duty benefit, it is necessary to examine whether such goods fall within the scope of goods specified under Notification 45/25. The relevant extract of the notification reads as under

” (a) Scientific and technical instruments, apparatus, equipment (including computers)

(b) accessories, parts, consumables and live animals (for experimental purposes) “

5.9.2 Amongst the goods listed above, the category of ‘consumables’ is of relevant import for the Applicant’s R&D Goods. However, the term “consumables” is not defined under Notification 45/25, its predecessor notifications, or under the Customs Act, 1962. Accordingly, its interpretation shall be derived through settled principles of statutory construction, which entail making reference to external aids such as allied regulations, dictionaries and judicial pronouncements.

5.9.3 Etymologically, the term “consumable” originates from the Latin word “consumer”, meaning “to use up” or “eat” or “exhaust”. According to the Chambers Dictionary (Deluxe Edition), consumable denotes “something that can be consumed”, while the term consume connotes “to use up; to devour; to exhaust or spend;…, etc.”. Thus, the word consume contemplates either complete exhaustion of goods in the process or losing their identity completely.

5.9.4 Further, the FTP 2023 defines “consumables” as:

“11.11 “Consumables” means any item, which participates in or is required for a manufacturing process, but does not necessarily form part of end-product. Items, which are substantially or totally consumed during a manufacturing process, will be deemed to be consumables.”

5..9.5 Thus, the term “consumable” refers to any article, material or substance that is used or expended in the course of a process. The use of the expression “not necessarily” clarifies that such goods may or may not form part of the end-product, and their classification as consumable does not turn on their final product. It includes items which are substantially or wholly consumed during such use. Also, it may be gently reminded that the process/ goal here is R&D and hence, a direct or indirect contribution to that process alone shall determine the consumable status.

5.9.6 In this regard, reference may also be drawn to the following judicial precedents which, directly or incidentally, examines the scope of the term “consumables”:

-

- In Vikram Sarabhai Space Centre v. Collector of Customs, Madras [1998 (98) ELT 714 (Tri-Del)], the issue under consideration was whether steel sheets and plates imported for one-time use in fabricating sub-systems of rocket motors qualified as consumable goods. In this regard, the CEGAT held as follows:

. . The consumable is one that can be consumed, that is used up, wasted away. The steel sheets/plates which are used in the fabrication of rocket motors did not loose their identity as sheets and plates. No other goods were produced out of such sheets and plates which had been imported cut to specific sizes…

9. In exemption notification the exemption is provided to the consumable goods required for the purpose of research. The various chemicals assets and other items required for research which are used up in the process of research will be covered by this exemption notification…”

-

- Similar views have been expressed by the CEGAT in Indian Telephone Industries Ltd., Madras v. Collector of Customs, Madras [1983 (13) ELT 1012 (Tri-Del)].

- In Bangalore Genei Pvt. Ltd vs. CCE Bangalore [2010 (261) ELT 1079 (Tri-Bang)], the CESTAI’ held that enzymes used in DNA and RNA research were consumables, as they were used in scientific equipment where they underwent chemical reactions and were fully consumed in the analytical process. Based on the certificate from research institution and their complete consumption, the exemption under the notification was upheld,

5.9.7 Thus, the term “consumable” is of wide import as it has a broad, functional meaning encompassing any material or substance that participates in, facilitates, or enables a process and is expended or used up. Since the duty exemption is allowed for use of goods in the R&D process, the scope of exemption should also be of wide import and broad connotation such that effect of the exemption could be maximized. In our view, it includes all items essential to a process, whether directly contributing to the outcome or merely assisting it including say items meant to be used for or assess storage, etc., whose use results in their exhaustion or loss of functional character or reusability, while yielding information regarding sustainability of the API/ Drug/ Formulation being worked or researched upon. In an R&D setting, this covers all materials used up during experimentation, testing, or analysis, where the objective is to generate scientific knowledge. During the R&D process, the imported R&D Goods are completely consumed in the manner specified hereinafter:

Below is the table converted from the PDF in the same column format.

| No | Product | Manner of utilization |

| 1 | RLD(s) | The RLD(s) are utilized as approved benchmark products for comparative testing to establish equivalence evaluation of the developed formulation. Samples of RLD(s) are subjected to detailed analytical and comparative studies, including dissolution profiling, stability assessment, impurity characterization, and performance testing, in order to establish equivalence with the proposed formulation. The RLD samples are entirely consumed during testing and analysis, with no recoverable quantity remaining post-use. |

| 2 | API(s) | API(s) are utilized as the core component in pre-formulation and formulation development activities. The API(s) are employed in solubility, stability, and compatibility studies with excipients, followed by incorporation into laboratory-scale formulations and trial or development batches to evaluate dosage form, bioavailability, and stability parameters. During processing and testing, the API(s) undergo physical and chemical transformation and are fully consumed in the R&D process, leaving no residual material capable of recovery or reuse. |

| 3 | Impurities | Imported impurity standards are utilized for development, identification, and quantification of the impurity profile of the trial formulation. These materials are used during analytical method development, calibration exercises, validation studies, and stability testing. The impurities are consumed in micro-quantities and are completely exhausted during analytical use, with no recoverable material remaining thereafter. |

| 4 | Pre-filled syringes | Pre-filled syringes are utilized to evaluate container–closure integrity, device compatibility, sterility, and performance characteristics of the developed formulation. These syringes are used during filling operations, stability studies, sterility testing, and functional performance evaluations. The integrity of the device is irreversibly compromised during such studies, rendering the syringes unfit for reuse or recovery and resulting in complete consumption during R&D activities. |

| 5 | Chemicals | Chemicals are utilized across formulation development, analytical testing, and stability studies, including as reagents, solvents, and processing aids. Such chemicals are consumed during experimentation, sample preparation, analytical runs, and stability evaluations. By their very nature, these chemicals are fully used up or rendered unusable during the conduct of R&D activities, leaving no recoverable quantity post-consumption. |

| 6 | Packaging Materials | Packaging Materials inter alia include bottles, bottle caps, capsules, and other primary and secondary packaging materials intended for filling, storage, and evaluation of the drug product. These goods are integral to the R&D process, as they are required to assess container–closure integrity, product–pack interaction, protection against environmental factors, and overall suitability of the packaging configuration in alignment with the TPP and applicable regulatory expectations. Such packaging materials are utilized strictly in accordance with approved development and testing protocols during trial and development batches, stability studies, and performance evaluations. They are used for filling, sealing, storage, and testing under prescribed conditions and are, by their nature, fully consumed in the R&D process. These goods are incapable of reuse or diversion for commercial purposes and are exhausted entirely during formulation development, analytical testing, and stability assessments. |

| 7 | Other consumable goods including Vials, Canister, Enzyme Powder, Reagents | Other consumable goods inter alia include vials, canisters, enzyme powders and reagents, are utilized as essential inputs in the R&D process. These goods are employed at various stages of R&D inter alia for sample preparation, formulation development, analytical testing, method validation, process optimisation, and stability and performance studies, strictly in accordance with approved study protocols and internal standard operating procedures. By their very nature, these R&D goods are used only for experimental, testing, and analytical purposes and are entirely consumed, depleted, or rendered unusable during the course of the R&D process. |

5.9.8 In view of the foregoing and considering that research activity inherently involves consumption of materials in the course of experimentation rather than commercial production, the materials so utilized are, in substance, consumables. Accordingly, the R&D Goods may qualify as “consumables”.

5..9.9 It is a well-established principle that exemption notifications designed to promote a specific purpose shall receive a liberal and purposive construction, so as to advance the legislative intent rather than defeat it by a narrow or literal reading. This principle was lucidly affirmed in Kidwai Memorial Institute of Oncology vs Commissioner of Customs [1999 (111) ELT 698 (“Fri)), where the Tribunal observed that the term “consumable stores”, being undefined, must be construed liberally in light of the object of the notification and purpose of use. This approach has been consistently affirmed, including in Featherlite Products Pvt. Ltd [2007 (208) ELT 143 (Tri-Bang)], where ergonomically designed laboratory furniture facilitating research was held eligible for exemption.

5.9.10 Notification 45/25 is an instrument to foster indigenous R&D, innovation and scientific advancement in India by reducing the cost burden on research institutions. In this context, R&D Goods imported for R&D purposes constitute an essential component of such activities. Accordingly, its provisions warrant a purposive and liberal interpretation to ensure that the beneficial intent of facilitating research is fully realized and not defeated by restrictive construction.

5..9.11 Basis the above, the Applicant believes that the R&D goods proposed to be imported, and meant for stages prior to manufacturing of the Exhibit Batch, are entitled to exemption under Notification 45/25. These R&D goods illustratively include alia includes RLDs, APIs, Impurities, Pre-filled Syringes, Chemicals, Packaging Materials, Vials, Canister, Enzyme Powder, Reagents and other consumable goods.

5.10 Whether the R&D goods imported by the Applicant for the Exhibit Batch are eligible for availing the concessional Customs duty benefit under Notification 45/25?

5..10.1 As previously stated, once the development stage is successfully concluded, the Exhibit Batch process is required to be executed under manufacturing conditions in order to assess its scalability and reproducibility. For this limited and specific purpose, the R&D unit engages its own Factory (in a pseudo job worker/ contract manufacturer capacity) to undertake manufacture of the Exhibit Batch in accordance with the specifications, process parameters, and controls documented in the Lab Report. Such manufacture is undertaken under the technical supervision, direction, and oversight of the R&D units, with the. Factory merely serving as the execution site for scale-up, process validation, and confidence building, and not as a commercial manufacturing unit for the said manufacture. Upon completion of manufacture and prescribed testing, the outcomes and data generated are, in totality, compiled at the R&D unit and the data so generated forms the basis for regulatory submission by the R&D unit for eventual approval by the regulatory authorities.

5.10.2 The development and manufacture of the Exhibit Batch, in substance and intent, constitute an inseparable extension of the R&D activities. The sole objective of this stage is to evaluate the feasibility, robustness, and consistency of the formulation and manufacturing process when operated at larger, yet representative, scales. The Applicant is expressly prohibited from utilizing, selling, or otherwise commercially exploiting the goods manufactured under the Exhibit Batch, and such goods are restricted exclusively for R&D, testing, stability assessment, and regulatory evaluation. Accordingly, the Exhibit Batch is intrinsically and unequivocally part of the R&D activities, notwithstanding that manufacturing infrastructure is utilized for its execution.

5.10.3 At this juncture, it is highlighted that all imports for the purposes of Exhibit Batch are separately identifiable at all stages and any diversion or misuse is not permitted within Applicant’s internal SOP. A full account of same can be given at any stage, if needed, with proper evidence and corroboration.

5.10.4 In light of the foregoing facts and the detailed reasoning already set out in response to Question 1 and Question 2, which are not reiterated herein for the sake of brevity, the Applicant submits that the R&D goods imported by the Factory for the limited purpose of carrying out the aforesaid R&D activities are likewise eligible for the applicable concessional Customs duty benefit. The mere involvement of the Factory as an execution site for R&D-driven scale-up and validation does not alter the essential character or purpose of such imports as being exclusively for R&D.

5.10.5 It is also pertinent to note that the exemption notification by itself does not restrict the use of the imported materials outside the R&D unit as such and hence, it would be far fetched to conclude that merely since the Exhibit Batch manufacturing and analysis is done outside the R&D unit, the same renders the underlying import as ineligible for exemption above.

5.10.6 Lastly, for conformance, the Applicant requests this Hon’ble Customs Authority for Advance Rulings (`CAAR.’) to pronounce a ruling on this aspect, providing clarity on the questions/ concerns raised in this advance ruling application.

5.11 In view of the facts and circumstances set out hereinabove, the Applicant submitted to:

- take the present application on record and pronounce an advance ruling on the questions raised herein, in light of the attendant facts, applicable statutory provisions, and the prevailing legal and judicial position;

- pass such further or other orders as this Hon’ble Authority may deem fit and proper in the facts and circumstances of the case, in the interest of justice, equity and good conscience; and

- direct that the contents of the present application, including factual disclosures, technical processes, supporting documents and the final order passed thereon, be treated as confidential and not be disclosed, published or uploaded in the public domain, as the same contain sensitive and proprietary business information/ document and document references, disclosure of which may materially and adversely affect the Applicant’s commercial interests.

6. Port of Import and reply from jurisdictional Commissionerate:

The applicant in their CAAR-1 indicated that they intend to import the subject goods from O/o the Office of the Principal Commissioner of Customs (Imports), Jawaharlal Nehru Customs House (‘INCH’), Nhava Sheva-I Taluka-Uran, Raigad, Maharashtra. The application was forwarded to the jurisdiction of O/o the Office of the Principal Commissioner of Customs (Imports), Jawaharlal Nehru Customs House (‘INCH’), Nhava Sheva-I Taluka-Uran, Raigad, Maharashtra, for comments on 20.03.2026, 09.04.2026,23.04.2026 and 13.05.2026.

However, no comments were received from the said Commissionerate.

7.Details of Personal Hearing:

A personal hearing in this matter was held on 05.06.2026 at 11:30am. The Authorized representative of the applicant attended the PH and maintained his stand as stated in written submission about Applicability of concessional rate of customs duty to import of goods for R&I) purpose under Notification No. 45/2025. Conditions as mentioned in said notification require few compliances, representative reiterated that they fulfill all of them. Question with respect to Test on higher volume of R&D, at another unit i.e. factory unit for manufacturing of exhibit batch, is also raised & representative explained that commercial quantity Test is required to obtain Commercial License.

No representative from Department side appeared.

80 DISCUSSION AND FINDINGS

8.1 I have carefully considered the application filed by M/s. Lupin Limited, the statement of facts, written submissions, documents placed on record, records furnished during the course of proceedings, and the applicable statutory provisions. I proceed to pronounce this ruling on the basis of the information available on record and the legal framework governing the issue.

8.2 At the outset, I find that the present application seeks a ruling on the applicability of Notification No. 45/2025-Customs dated 24.10.2025, issued under Section 25(1) of the Customs Act, 1962, to various goods proposed to be imported by the applicant for use in its research and development activities. Since the questions raised relate to the applicability of an exemption notification issued under the Customs Act, 1962, the same are covered by Section 28H(2) of the Act and are therefore admissible for determination under the advance ruling mechanism.

8.3 7.3 Before examining the specific questions raised, it is necessary to consider the statutory framework governing the exemption claimed by the applicant. Classification and applicability of exemption notifications are governed by the Customs Tariff Act, 1975, read with the General Rules for Interpretation, the relevant Section Notes and Chapter Notes, and the conditions prescribed in the exemption notification itself.

It is a settled principle of law that an exemption notification must be construed strictly and the burden lies upon the person claiming the exemption to establish that its case falls squarely within the terms of the notification. The Constitution Bench of the Hon’ble Supreme Court in Commissioner of Customs (Import), Mumbai v. Dilip Kumar & Company 12018 (361) ELT 577 (SC)] has authoritatively held that eligibility to an exemption must be demonstrated strictly in accordance with the language employed in the notification and all substantive conditions prescribed therein must be satisfied.

8.4 The applicant is engaged in pharmaceutical research and development and operates in-house Research and Development Centres situated at Pune and Aurangabad. The said facilities have been recognized by the Department of Scientific and Industrial Research (DSIR), Ministry of Science and Technology, Government of India. The applicant seeks a ruling on the applicability of Notification No. 45/2025-Customs dated 24.10.2025 in respect of various categories of goods proposed to be imported for research and development activities undertaken at its DSIR-recognized facilities.

The principal issues requiring determination are:

(i) whether the applicant’s DSIR-recognized R&D facilities qualify as eligible research institutions for the purposes of Notification No. 45/2025-Customs;

(ii) whether goods imported and utilized during the research and development stage prior to manufacture of the Exhibit Batch are eligible for the benefit of the notification; and

(iii) whether goods imported for manufacture of the Exhibit Batch are eligible for the benefit of the notification.

8.5 Before examining the questions raised by the applicant, it is necessary to consider the scope and scheme of Notification No. 45/2025-Customs dated 24.10.2025 issued under Section 25(1) of the Customs Act, 1962. The said notification grants concessional rates of customs duty and integrated tax in respect of specified goods imported by eligible institutions subject to fulfilment of prescribed conditions.

Relevant portion of Sl. No. 70 of Table II to the said notification reads as under:

G.S.R. 781(E).— In exercise of the powers conferred by sub-section (1) of section 25 of the Customs Act, 1962 (52 of 1962) and sub-section (12) of section 3 of the Customs Tariff Act, 1975 (51 of 1975)… …the Central Government…, hereby exempts -….

(b) the goods of the description specified in column (3) of the Table II below or column (3) of the said Table .., when imported into India, –

(iii)from so much of the duty of customs leviable thereon under the said First Schedule as is in excess of the amount calculated at the standard rate specified in the corresponding entry in column (4) of the said Table; and

(iv)from so much of the integrated tax leviable thereon under sub section (7) of section

| 3 of said Customs Tariff Act … | |||||

| No | Chapter or Heading |

Description of goods | Standard rate | IGST | Condition No. |

| 70 | Any Chapter |

(e) Scientific and technical instruments, apparatus, equipment (including computers);

(f) accessories, parts, consumables and live (g) computer software, Compact Disc-Read Only Memory (CD-ROM), recorded magnetic (h) prototypes, the CIF value of which does not exceed rupees fifty thousand in a financial year: Provided it is imported by Research institutions, other than a hospital: Provided further that nothing contained in this S. No. shall have effect after the 31st March, 2029 |

5% | – | 24 |

| Condition 24 If

(A) (3) The importer (iv) is registered with the Government of India in the Department of Scientific and Industrial Research; (v) produces a certificate from the Head of the institution, in each case of import, certifying that the said goods are essential for research purposes and will be used for the stated purpose only; (vi) .. (4) The goods falling under (1) above shall not be transferred or sold .for a period of Dye years from the date of importation, (B) …. Explanation. – For the purposes of this entry, the expression, (d) “Head” means in relation to an in relation to an institution, the Director thereof (by whatever name called) , |

|||||

8.6 A conjoint reading of Sl. No. 70 and Condition No. 24 makes it evident that the exemption is not available merely because an importer possesses DSIR recognition. The notification envisages satisfaction of multiple substantives as well as procedural requirements, all of which are cumulative in nature.

8.7 A plain reading of the notification demonstrates that the benefit is available only when the following conditions are cumulatively satisfied:

(a) the importer is a research institution duly registered/recognized by the Department of Scientific and Industrial Research (DSIR);

(b) the imported goods must fall within the categories specifically enumerated in Si. No. 70 of the notification.

(c) Head of the Institution must certify, in respect of each import, that the goods are essential for research purposes.

(d) the goods are intended to be used solely for such research purposes; and

(e) the importer must comply with the post-importation obligations prescribed under the notification, including the restriction on transfer or sale of the imported goods.

8.8 Thus, mere DSIR recognition by itself does not automatically confer entitlement to the exemption. he imported goods must independently satisfy the substantive requirement of being intrinsically connected with, and essential for, the conduct of research activities contemplated by the notification. The exemption is not attached to the institution in the abstract; rather, it is attached to specified goods imported by an eligible institution for a specified purpose, namely research. The notification thus grants the benefit not on the basis of the status of the importer alone, but on the combined fulfilment of the twin requirements of institutional eligibility and research-specific use of the imported goods.

8.9 Accordingly, Thus, DSIR recognition, though a necessary condition, is not by itself sufficient to confer entitlement to the exemption. The benefit attaches only to specified goods imported by an eligible institution for approved research purposes and subject to strict compliance with the conditions prescribed under the notification.

Whether the applicant’s R&D units are eligible research institutions under Notification No. 45/2025-Customs

8.10 The applicant has placed on record the DSIR Recognition Certificate dated 14.05.2025 issued by the Department of Scientific and Industrial Research recognizing its in-house Research and Development Centres situated at Pune and Aurangabad. The applicant has also furnished the relevant registration certificates issued for availing customs duty exemption benefits.

8.11 Condition No. 24 requires that the importer be registered with the Department of Scientific and Industrial Research. Upon examination of the documents placed on record, I find that the applicant’s R&D Centres possess valid DSIR recognition and registration during the relevant period. No material has been placed before me to indicate that such recognition has been suspended, withdrawn or subjected to any restriction affecting eligibility under the notification.

8.12 Accordingly, I observe that the applicant’s DSIR-recognized Research and Development Centres situated at Pune and Aurangabad satisfy the institutional eligibility requirement prescribed under Notification No. 45/2025-Customs and qualify as eligible research institutions for the purposes of the said notification.

However, satisfaction of the institutional eligibility requirement does not by itself confer entitlement to the exemption. The applicant must further establish that the goods proposed to be imported are covered by the notification, are essential for research purposes, and satisfy all other substantive and procedural conditions prescribed therein.

Whether goods imported by the R&D units prior to Exhibit Batch manufacture are eligible for the benefit?

8.13 The applicant has provided a detailed explanation of the pharmaceutical research and development process undertaken at its DSIR-recognized R&D units. The goods imported prior to the manufacture of the Exhibit Batch include Reference Listed Drugs (RLDs), Active Pharmaceutical Ingredients (APIs), impurities, chemicals, reagents, enzyme powders, pre-filled syringes, packaging materials, vials, canisters and similar items. According to the applicant, these goods are used during formulation development, pre-formulation studies, analytical method development and validation, stability studies, bio-equivalence studies and other research activities. It has been submitted that such goods are substantially consumed during the course of research and therefore qualify as “consumables” for the purposes of Notification No. 45/2025-Customs.

8.14 I find that the expression “consumables” has not been specifically defined under Notification No. 45/2025-Customs. The applicant has relied upon the definition contained in the Foreign Trade Policy, 2023 as well as judicial precedents, including:

- Vikram Sarabhai Space Centre v. Collector of Customs [1998 (98) ELT 714 (Tri.-Del.)];

- Indian Telephone Industries Ltd. v. Collector of Customs [1983 (13) ELT 1012 (Tri.-Del.)]; and

- Bangalore Genei Pvt. Ltd. v. CCE [2010 (261) ELT 1079 (Tri.-Bang.)].

The aforesaid decisions broadly support the principle that goods which are wholly or substantially consumed, exhausted or expended during the course of research, testing, experimentation or development activities may appropriately be regarded as consumables.

8.15 I observe considerable merit in the applicant’s contention that goods imported by a DSIR-recognized R&D unit and directly used in experimentation, analytical evaluation, formulation development, testing, validation, stability studies and related research activities are intended to facilitate and advance scientific research. The notification itself extends the benefit not only to instruments and equipment but also to “consumables”, thereby indicating the legislative intent to cover materials that are consumed or substantially utilized in the course of research and development activities.

8.16 At the same time, the benefit of the notification cannot be extended on the assumption that every item imported by a DSIR-recognized institution would automatically qualify for exemption. The eligibility of the goods must necessarily be examined with reference to the nature and intended use of each import. The importer is required to establish:

- that the goods fall within the scope and description contemplated under the notification;

- that the goods are required and essential for the approved research and development activities of the institution;

- that the certificate and other documentary requirements prescribed under Condition No. 24 are duly fulfilled; and

- that the goods are actually used for the stated research purposes.

8.17 In view of the foregoing, I observe that goods such as Reference Listed Drugs (RLDs), Active Pharmaceutical Ingredients (APIs), impurities, chemicals, reagents, enzyme powders and other similar materials imported by a DSIR-recognized R&D unit, which are consumed or substantially utilized in research, testing, analytical evaluation, formulation development, validation and stability studies, would generally fall within the scope of the term “consumables” for the purposes of Notification No. 45/2025-Customs. However, the benefit would remain subject to fulfilment of all conditions prescribed under the notification and verification of the nature and end-use of the goods at the time of import.

Whether goods imported for manufacture of Exhibit Batch are eligible for the benefit of Notification No. 45/2025-Customs?

8.18 This question requires separate consideration as the applicant itself has distinguished the imports covered under the present question from those covered under Question No. 2. The applicant has explained that, upon completion of laboratory-scale development activities at its DSIR-recognized Research and Development (“R&D”) unit, an Exhibit Batch is manufactured at a manufacturing facility situated outside the recognized R&D unit. The applicant has further stated that, for manufacture of the Exhibit Batch, the required materials may either be imported directly by the manufacturing facility itself or may originate from materials imported and utilized by the R&D unit during the development stage. According to the applicant, the Exhibit Batch is manufactured under the technical guidance, supervision and control of the R&D unit for the purposes of scale-up, process validation, testing, stability evaluation and regulatory submission.

8.19 The principal contention of the applicant is that manufacture of the Exhibit Batch constitutes an integral and inseparable component of the overall pharmaceutical research and development process. It is submitted that:

(i) the Exhibit Batch is not intended for commercial sale or distribution;

(ii) the batch is manufactured solely for developmental, validation, testing and regulatory purposes;

(iii) the manufacturing facility functions merely as an execution site akin to a job worker acting under the directions of the R&D unit; and

(iv) commercial production commences only after obtaining the requisite statutory approvals from the regulatory authorities.

On the basis of the above submissions, it has been argued that imports connected with the manufacture of the Exhibit Batch should also be regarded as imports for research purposes and therefore qualify for the benefit of Notification No. 45/2025-Customs.

8.20 I have carefully considered the submissions of the applicant. There can be no dispute that manufacture of an Exhibit Batch constitutes an important stage in the pharmaceutical product development and regulatory approval process The material placed on record indicates that such batches are manufactured for evaluating scalability, reproducibility, process robustness and regulatory compliance, and are not intended for commercial sale. However, the issue before this Authority is not whether the Exhibit Batch forms part of the broader research and development lifecycle. The issue for determination is whether imports associated with such manufacture satisfy the specific conditions prescribed under Notification No. 45/2025-Customs.

The notification grants concessional duty only in respect of specified goods imported by a research institution registered with the Department of Scientific and Industrial Research (DSIR) and certified by the Head of such institution as being essential for research purposes. The exemption is institution-specific and conditional. It does not provide that every import connected with a research project automatically qualifies for the benefit irrespective of the identity of the importer or the manner in which the imported goods are subsequently deployed.

8.21 Entry No. 70 read with Condition No. 24 of Notification No. 45/2025-Customs, inter alia, requires that:

(a) the importer must be a research institution registered with DSIR;

(b) the Head of the institution must certify that the imported goods are essential for research purposes and will be used solely for the stated purpose; and

(c) the imported goods shall, not be transferred or sold for a period of five years from the date of importation.

These are substantive conditions governing eligibility to the exemption and must be strictly satisfied.

8.22 On the facts presented, two distinct situations emerge:

(i) goods are imported by the DSIR-recognized R&D unit and subsequently moved to a manufacturing facility for manufacture of the Exhibit Batch; or

(ii) the manufacturing facility itself imports the goods required for manufacture of the Exhibit Batch, albeit under the technical supervision and control of the R&D unit.

Each situation requires independent examination in the context of the conditions prescribed under the notification.

8.23 In the first situation, the goods are imported by a DSIR-recognized research institution and, therefore, the requirement relating to the identity of the importer is initially satisfied. However, Condition No. 24(A)(2) expressly stipulates that goods imported under the notification shall not be transferred or sold for a period of five years from the date of importation. This restriction is a substantive condition attached to the exemption and is intended to ensure that goods imported at the concessional rate remain with, and are utilized by, the eligible research institution for the approved research purposes.

The notification contains no provision permitting the transfer of such goods to a manufacturing facility merely because the facility is engaged in activities connected with the same research project. Consequently, once the imported goods are moved, supplied, or transferred from the DSIR-recognized institution to a manufacturing facility for manufacture of an Exhibit Batch, the goods cease to remain with the eligible institution and the express condition prohibiting transfer stands violated. Thus, although the importer may initially satisfy the eligibility requirement prescribed under the notification, the exemption becomes unavailable on account of breach of a substantive

8.24 The second situation concerns imports undertaken directly by the manufacturing facility for manufacture of the Exhibit Batch. In such :cases, the importer is not the DSIR-recognized research institution contemplated under the notification, but the manufacturing facility itself.

While the Exhibit Batch may be manufactured exclusively for developmental, validation, testing or regulatory purposes, the notification does not grant exemption merely on the basis of the end-use of the imported goods. The notification specifically requires that the importer itself must be an eligible DSIR-recognized research institution and must independently satisfy all prescribed conditions. Therefore, the exemption cannot be extended merely because the manufacturing activity is undertaken under the supervision or guidance of the R&D unit.

8.25 It is well settled that exemption notifications are required to be construed strictly. In Commissioner of Customs (Import), Mumbai v. Dilip Kumar & Company .12018 (361) ELT 577 (SC)A, the Constitution Bench of the Hon’ble Supreme Court held that the burden lies upon the claimant to establish that its case falls squarely within the terms of the exemption notification and that any ambiguity must be resolved in favour of the Revenue.

Similarly, in Novopan India Ltd. v. Collector of Central Excise and Customs [1994 (73) ELT 769 (SC)], the Hon’ble Supreme Court held that a person claiming exemption must clearly establish compliance with all conditions prescribed therein and that exemption provisions cannot be enlarged by implication.

The same principle was reiterated in Hari Chand Shri Gopal v. Commissioner of Central Excise [2010 (260) ELT 3 (SC)1, wherein the Hon’ble Supreme Court held that substantive conditions attached to an exemption notification are mandatory and must be strictly complied with before the benefit can be availed.

8.26 Applying the above principles, eligibility under Notification No. 45/2025-Customs must be determined strictly in accordance with the language employed therein. The Authority cannot expand the scope of the exemption by treating every activity connected with research and development as automatically qualifying for the concession. Had the legislature intended to extend the benefit to manufacturing facilities engaged in pilot-scale production, validation batches, scale-up batches or other pre-commercial manufacturing activities connected with research projects, it could have expressly provided so. No such provision is found in the notification.

Acceptance of the applicant’s interpretation would substantially enlarge the scope of the exemption beyond its express terms and dilute the institutional restrictions consciously incorporated in the notification. Such an interpretation would be contrary to the settled principles governing construction of exemption notifications.

8.27 In view of the forgoing discussion it is evident that the scientific or developmental character of the Exhibit Batch, by itself, is insufficient to determine eligibility under Notification No. 45/2025-Customs. What is material is whether the importer satisfies the institutional eligibility requirements prescribed by the notification and whether all substantive conditions attached to the exemption stand fulfilled. Therefore:

(i) Goods imported by a DSIR-recognized research institution are eligible for the benefit of Notification No. 45/2025-Customs only when such goods are imported, retained and utilized by the said institution in compliance with all conditions prescribed under the notification.

(ii) Goods imported under the notification by a DSIR-recognized research institution and thereafter transferred, supplied or moved to a manufacturing facility for manufacture of an Exhibit Batch cease to satisfy the requirements of Condition No. 24(A)(2), which expressly prohibits transfer or sale of the imported goods for a period of five years from the date of importation. Consequently, such goods are not eligible for the benefit of the notification.

(iii) Where the goods are imported directly by a manufacturing facility for manufacture of an Exhibit Batch, the benefit of Notification No. 45/2025-Customs is not available ab initio, since the importer itself is not a DSIR-recognized research institution and therefore does not satisfy the primary eligibility condition prescribed under Entry No. 70 read with Condition No. 24 of the notification.

(iv) Accordingly, goods imported for manufacture of an Exhibit Batch do not qualify for the benefit of Notification No. 45/2025-Customs in either of the above situations. As the benefit of Notification No. 45/2025-Customs is available only where the importing entity itself is an eligible DSIR-recognized research institution and independently satisfies all substantive conditions prescribed under the notification.

8.28 In view of the facts and circumstances of the case, forgoing discussion and analysis, I come to conclusion that:

(a) The applicant’s DSIR-recognized Research and Development Centres situated at Pune and Aurangabad satisfy the institutional eligibility requirement prescribed under Notification No. 45/2025-Customs dated 24.10.2025 and qualify as eligible research institutions for the purposes of the said notification.

(b) Goods such as Reference Listed Drugs (RLDs), Active Pharmaceutical Ingredients (APIs), impurities, chemicals, reagents, enzyme powders and other similar materials, which are consumed or substantially utilized in formulation development, analytical evaluation, testing, validation, stability studies and other research activities undertaken by the applicant’s DSIR-recognized R&D Centres, are covered within the scope of the expression “consumables” under Si. No. 70 of Notification No. 45/2025-Customs and are eligible for the benefit of the notification, subject to fulfilment of the conditions prescribed therein.

(c) Goods imported by the DSIR-recognized R&D Centres and thereafter transferred, supplied or moved to a manufacturing facility for manufacture of an Exhibit Batch are not eligible for the benefit of Notification No. 45/2025-Customs, as such transfer is contrary to Condition No. 24(A)(2), which prohibits transfer or sale of the imported goods for a period of five years from the date of importation.

(d) Goods imported directly by a manufacturing facility for manufacture of an Exhibit Batch are not eligible for the benefit of Notification No. 45/2025-Customs, since the importing entity is not a DSIR-recognized research institution as required under the notification.

(e) Accordingly, the benefit of Notification No. 45/2025-Customs is available only in respect of imports made by the eligible DSIR-recognized research institution for its research activities and in compliance with all conditions prescribed under the notification.

I rule accordingly.

Author Bio