Invoice Management System (IMS) under GST Acceptance, Rejection & Pending Actions on document

Summary: The Invoice Management System (IMS) under GST is a newly introduced mechanism enabling registered taxpayers to manage purchase-related documents such as invoices, debit notes, and credit notes by accepting, rejecting, or keeping them pending before Input Tax Credit (ITC) flows into GSTR-3B. IMS primarily applies to forward charge invoices/debit notes/credit notes and import of goods invoices, while transactions like RCM, ISD, import of services, and POS-restricted ITC remain outside its scope. Accepted documents auto-populate ITC in GSTR-3B, whereas rejected or pending documents do not. Once accepted or rejected and GSTR-3B is filed, no further action can be taken, but pending documents can be acted upon in subsequent periods. Import of goods invoices can only be accepted or kept pending. Supplier tax liability generally remains unaffected by buyer actions on invoices or debit notes, but rejection of a credit note prevents reduction of supplier liability under Section 34. The article also clarifies treatment of expired ITC timelines, deemed acceptance provisions, next-month invoices appearing in current IMS, and practical issues related to portal functionality. IMS aims to give buyers greater control over ITC reconciliation and document validation while ensuring better matching between supplier disclosures and recipient ITC claims under GST compliance.

1. Coverage of this article:

a. In this article, I am discussing the features of IMS in GST. It stands for “Invoice Management System”.

b. It has been introduced for the purpose of taking control over the purchase invoices including debit note and credit note which I am explaining this in details in this article

c. How it impacts the supplier liability and buyer ITC

d. Multiple times action on various documents

e. Can we take action after filing of GSTR-3B?

f. Other practical scenarios

2. Full form of IMS:

Full form of IMS is “Invoice Management System”.

3. What is IMS in GST:

a. IMS is used for taking action on documents.

b. Action can be either accepted, rejected or pending.

4. Applicability of IMS on which transactions:

a. There are various types of transactions on which a registered person is claim the input.

b. It may be goods, services or capital goods.

| S No | Nature of transactions | Nature of documents | Part of IMS or not |

| 1 | Import of goods | Invoice | Yes |

| 2 | Import of goods | Debit Note | No |

| 3 | Import of goods | Credit Note | No |

| 4 | Import of Services | Invoice | No |

| 5 | Import of Services | Debit Note | No |

| 6 | Import of Services | Credit Note | No |

| 7 | RCM transactions | Invoice | No |

| 8 | RCM transactions | Debit Note | No |

| 9 | RCM transactions | Credit Note | No |

| 10 | ISD transactions | Invoice | No |

| 11 | ISD transactions | Debit Note | ISD cannot issue DN |

| 12 | ISD transactions | Credit Note | No |

| 13 | FCM transactions | Invoice | Yes |

| 14 | FCM transactions | Debit Note | Yes |

| 15 | FCM transactions | Credit Note | Yes |

| 16 | ITC not allowed due to POS rules | Invoice | No |

| 17 | ITC not allowed due to POS rules | Debit Note | No |

| 18 | ITC not allowed due to POS rules | Credit Note | No |

| 19 | ITC lapsed us 16(4) | Invoice | No |

| 20 | ITC lapsed us 16(4) | Debit Note | No |

a. Yes, means these documents is a part of IMS. A person can take the action on it.

b. No means these documents is not a part of IMS. A person is not required to take the any action upon it.

5. Actions on documents:

| S No | Nature of documents | Action in IMS |

| 1 | Invoice | Accept |

| 2 | Invoice | Reject except import of goods invoices |

| 3 | Invoice | Pending |

| 4 | Debit Note | Accept |

| 5 | Debit Note | Reject |

| 6 | Debit Note | Pending |

| 7 | Credit Note | Accept |

| 8 | Credit Note | Reject |

| 9 | Credit Note | Pending option enable from Oct 2025 return for a limited period |

a. We can take multiple action in IMS but credit note can be in pending only for 1 return period.

b. Invoice related to IOG can only be accept or kept in pending. Rejection options is not available for Import of goods invoices.

6. Impact of action in IMS in the GSTR-3B & in ITC:

| S No | Nature of documents | Action in IMS | Impact on ITC in GSTR-3B |

| 1 | Invoice | Accept | ITC will be transferred in 3B |

| 2 | Invoice | Reject | ITC will not be transferred in 3B |

| 3 | Invoice | Pending | ITC will not be transferred in 3B |

| 4 | Debit Note | Accept | ITC will be transferred in 3B |

| 5 | Debit Note | Reject | ITC will not be transferred in 3B |

| 6 | Debit Note | Pending | ITC will not be transferred in 3B |

| 7 | Credit Note | Accept | ITC will be transferred in 3B |

| 8 | Credit Note | Reject | ITC will not be transferred in 3B |

| 9 | Credit Note | Pending option enable from Oct 2025 return | ITC will not be transferred in 3B |

a. Accepted:

If any document is accepted, the impact will be taken in GSTR-3B.

b. Rejected:

If any document is rejected, the impact will not be taken in GSTR-3B.

c. Pending:

If any document is kept pending, the impact will not be taken in GSTR-3B.

7. Documents will be removed from IMS or not:

| S No | Nature of documents | Action in IMS | Impact on ITC in GSTR-3B |

| 1 | Invoice | Accept | After filing of GSTR-3B, it will be removed from IMS |

| 2 | Invoice | Reject | After filing of GSTR-3B, it will be removed from IMS |

| 3 | Invoice | Pending | After filing of GSTR-3B, it will not be removed from IMS |

| 4 | Debit Note | Accept | After filing of GSTR-3B, it will be removed from IMS |

| 5 | Debit Note | Reject | After filing of GSTR-3B, it will be removed from IMS |

| 6 | Debit Note | Pending | After filing of GSTR-3B, it will not be removed from IMS |

| 7 | Credit Note | Accept | After filing of GSTR-3B, it will be removed from IMS |

| 8 | Credit Note | Reject | After filing of GSTR-3B, it will be removed from IMS |

| 9 | Credit Note | Pending option enable from Oct 2025 return | After filing of GSTR-3B, it will not be removed from IMS |

a. Accepted:

If any document is accepted & GSTR-3B has been filed, after that these will be removed from IMS.

b. Rejected:

If any document is rejected & GSTR-3B has been filed, after that these will be removed from IMS.

c. Pending:

If any document is kept pending & GSTR-3B has been filed, after that these will not be removed from IMS until & unless they are accepted or rejected.

8. Further actions after filing of GSTR-3B:

| S No | Nature of documents | Action in IMS | Further actions after filing of 3B |

| 1 | Invoice | Accept | After filing of GSTR-3B, further actions cannot be taken |

| 2 | Invoice | Reject | After filing of GSTR-3B, further actions cannot be taken |

| 3 | Invoice | Pending | After filing of GSTR-3B, further actions can be taken in next month |

| 4 | Debit Note | Accept | After filing of GSTR-3B, further actions cannot be taken |

| 5 | Debit Note | Reject | After filing of GSTR-3B, further actions cannot be taken |

| 6 | Debit Note | Pending | After filing of GSTR-3B, further actions can be taken in next month |

| 7 | Credit Note | Accept | After filing of GSTR-3B, further actions cannot be taken |

| 8 | Credit Note | Reject | After filing of GSTR-3B, further actions cannot be taken |

| 9 | Credit Note | Pending | After filing of GSTR-3B, further actions can be taken in next month |

a. Accepted:

If any document is accepted & GSTR-3B has been filed, after that further action cannot be taken in the same or subsequent month.

b. Rejected:

If any document is rejected & GSTR-3B has been filed, after that further action cannot be taken in the same or subsequent month.

c. Pending:

If any document is kept pending & GSTR-3B has been filed, after that further action can be taken only in the subsequent month GSTR-3B.

9. Which table of GSTR-3B covered in IMS:

| S No | Nature of transactions | Table of 3B | Part of IMS |

| 1 | Import of goods | 4A(1) | Yes |

| 2 | Import of Services | 4A(2) | No |

| 3 | RCM transactions | 4A(3) | No |

| 4 | ISD transactions | 4A(4) | No |

| 5 | FCM transactions | 4A(5) | Yes |

a. We can take the action only on those invoices which is covered under FCM & Import of goods.

b. It means after accepting the invoices, ITC will be auto populated in the 4A(5) or 4A(1) table of the GSTR-3B.

10. Impact on supplier liability and buyer ITC after taking actions on invoices:

| S No | Action on invoices | Supplier liability | Buyer ITC |

| 1 | Accept | He needs to pay the tax | ITC will be credited in GSTR-3B |

| 2 | Reject | He needs to pay the tax | ITC will not be credited in GSTR-3B |

| 3 | Pending | He needs to pay the tax | ITC will not be credited in GSTR-3B |

a. Supplier liability will not be reduced whether buyer has accepted the invoice or not.

b. Supplier will pay the tax even if buyer has rejected the invoice.

11. Impact on supplier liability and buyer ITC after taking actions on debit note:

| S No | Action on debit note | Supplier liability | Buyer ITC |

| 1 | Accept | He needs to pay the tax | ITC will be credited in GSTR-3B |

| 2 | Reject | He needs to pay the tax | ITC will not be credited in GSTR-3B |

| 3 | Pending | He needs to pay the tax | ITC will not be credited in GSTR-3B |

a. Same provisions are applicable which is applicable in case of invoices.

b. Supplier will pay the tax even if buyer has rejected the debit note.

12. Impact on supplier liability and buyer ITC after taking actions on credit note:

| S No | Action on credit note | Supplier liability | Buyer ITC |

| 1 | Accept | Liability will be reduced | ITC will be reduced in GSTR-3B |

| 2 | Reject | Liability will not be reduced as per Sec 34 | ITC will not be reduced in GSTR-3B |

| 3 | Pending | Liability will be reduced | ITC will not be reduced in GSTR-3B |

a. If buyer ITC has been reduced then supplier liability will also be reduced.

b. If buyer has not reduced the ITC as per Section 34 then supplier liability will also not be reduced. This is the reason supplier liability disclosed in the GSTR-1 is mismatched with the GSTR-3B liability.

c. Credit note can remain pending in IMS only for one tax return period. In the next month, this option will be disable. He should accept or reject the credit note in next month return & accordingly supplier liability will be impact.

13. Impact on supplier liability if buyer has rejected the credit note:

Supplier liability will be increased if buyer has rejected the credit note.

14. In which month supplier liability will be increased?

a. Suppose Mr Ankit disclosed the credit note in Oct 2025 return and buyer has rejected the CN in the same month.

b. In November GSTR-3B supplier liability will be increased.

c. Impact of rejected credit note will be shown in next month 3B.

15. Ineligible ITC due to POS rules:

a. Ineligible ITC due to POS rules is also not a part of IMS.

b. There is no option available in IMS to take any action on these invoices.

c. It will only be report in table 4D(2) of GSTR-3B.

16. Time limit of ITC is expired:

a. If any invoice or debit note is shown as pending & time limit of ITC is expired which is 30th November of next year or date of filing of GSTR-9 whichever is earlier.

b. It will be removed from IMS after expiry of this period.

c. It is advisable to accept the invoice & debit note before expiry otherwise your ITC will be lapsed.

17. Next month documents reflected in current month IMS:

Suppose we are filing the GSTR-3B for the month of December 2025. In IMS, invoices are reflected which is related to the January 2026.

a. Why such invoices are becoming part of December IMS?

Answer: If e invoicing is applicable on the supplier then after generating the e invoice it will be shown in IMS even GSTR-1 is not filed for that period.

b. Action on such invoices are required?

Answer: There is no requirement to take any action on such invoices because these invoices is not a part of GSTR-2B of December. These invoices will become part of January GSTR-2B.

c. We need to take action against all those documents which is a part of current month GSTR-2B.

d. Deemed accepted:On such type of documents, deemed acceptance provision will not be applicable. It means they will not be deemed accepted.

18. Amendment in IMS related to Import of goods:

Advisory issued on 30th October 2025 for implementing IMS on IOG.

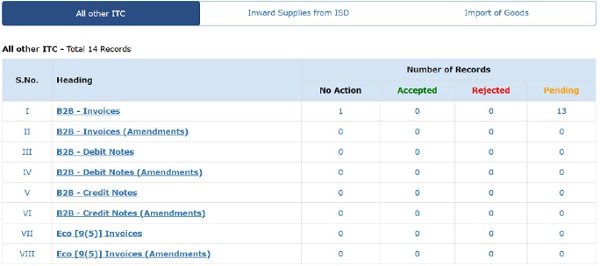

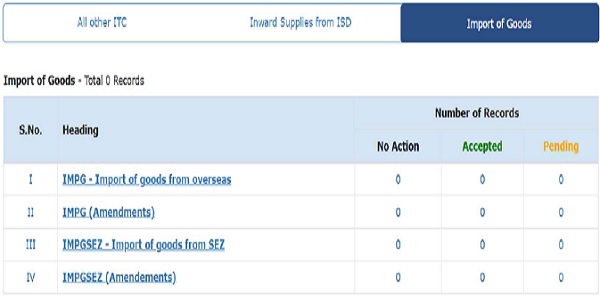

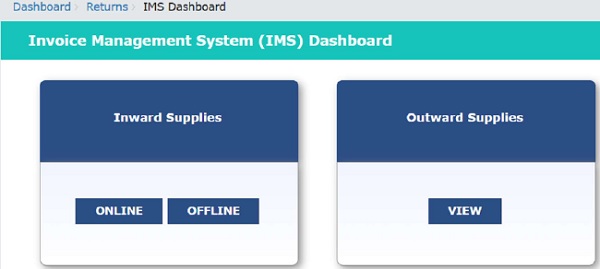

19. Portal screenshot:

a. Forward charge documents:

b. Import of goods invoices:

c. Path of IMS:

*****

If you have any queries, you can reach the author by email at caashishsingla878@gmail.com.

Disclaimer: The views and opinions expressed in this article are those of the author. This article is intended for general information purposes only and does not constitute professional advice. Readers are strongly advised to consult a qualified professional for guidance specific to their individual situation before making any financial, legal, or tax-related decisions. The author shall not be held liable for any loss or damage of any kind incurred as a result of the use of this information or for any actions taken based on the content of this article.

Author Bio